FinancialKoei Tecmo

Consolidated Financial Results: FY2025 2nd Quarter Data Appendix

8 pages~16 min full read

Key insights

7 takeaways · ~3 min read- 01

The entertainment segment is the primary revenue driver, consistently contributing over 90% of total sales and fueling a peak quarterly revenue of ¥28,978 million in FY25 Q4.

See it on page 2 - 02

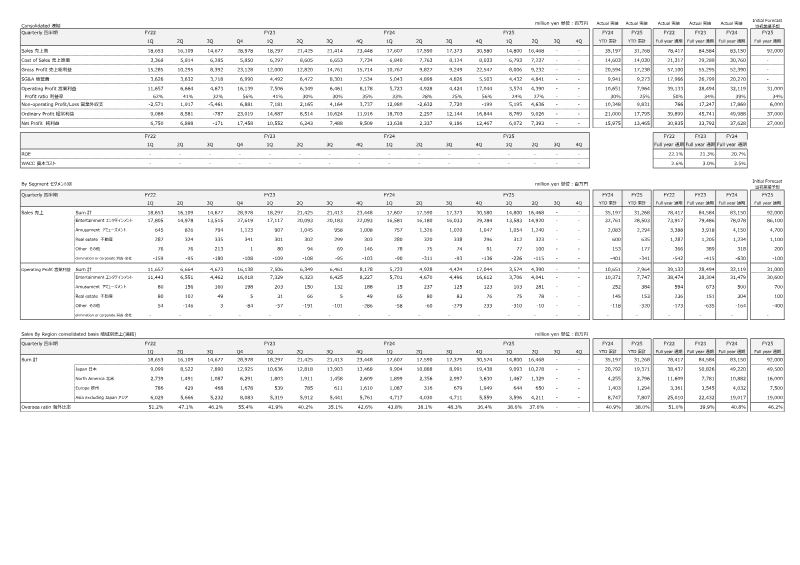

Gross profit margins have experienced significant compression, falling from 62% in FY22 Q1 to 30% by FY25 Q2 due to rising costs of sales.

See it on page 1 - 03

The company has successfully pivoted to a digital-first model, with digital sales accounting for approximately 70% of revenue and online/mobile units representing 60–80% of total sales volume.

See it on page 2 - 04

Financial performance showed a strong recovery in FY25 Q4 with ¥16,139 million in operating profit and ¥17,458 million in net profit, following a period of volatility that included a net loss in FY24 Q3.

See it on page 1 - 05

Japan remains the core market at 49% of total sales, while the company maintains a global footprint with overseas revenue ratios fluctuating between 35% and 55%.

See it on page 1 - 06

Capital expenditure more than doubled from ¥789 million in FY22 to ¥1,967 million in FY24, primarily directed toward real estate and equipment investments.

See it on page 2 - 07

Corporate expansion is evidenced by headcount growth from 2,413 employees in FY22 Q1 to 2,873 by FY25 Q4.

See it on page 2