Back to Writers

Koei Tecmo

Game Co.

212 documents

Japanese developer/publisher. Dynasty Warriors, Nioh, Dead or Alive, Atelier, Romance of the Three Kingdoms.

Documents

Report

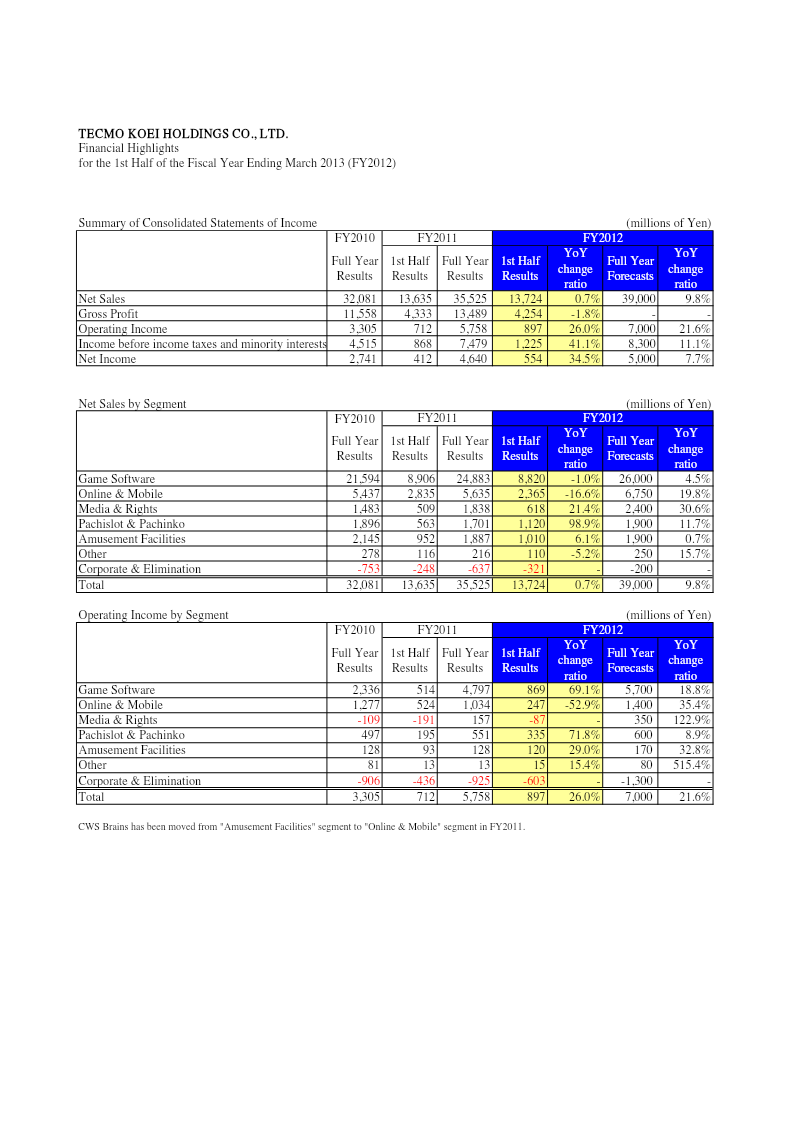

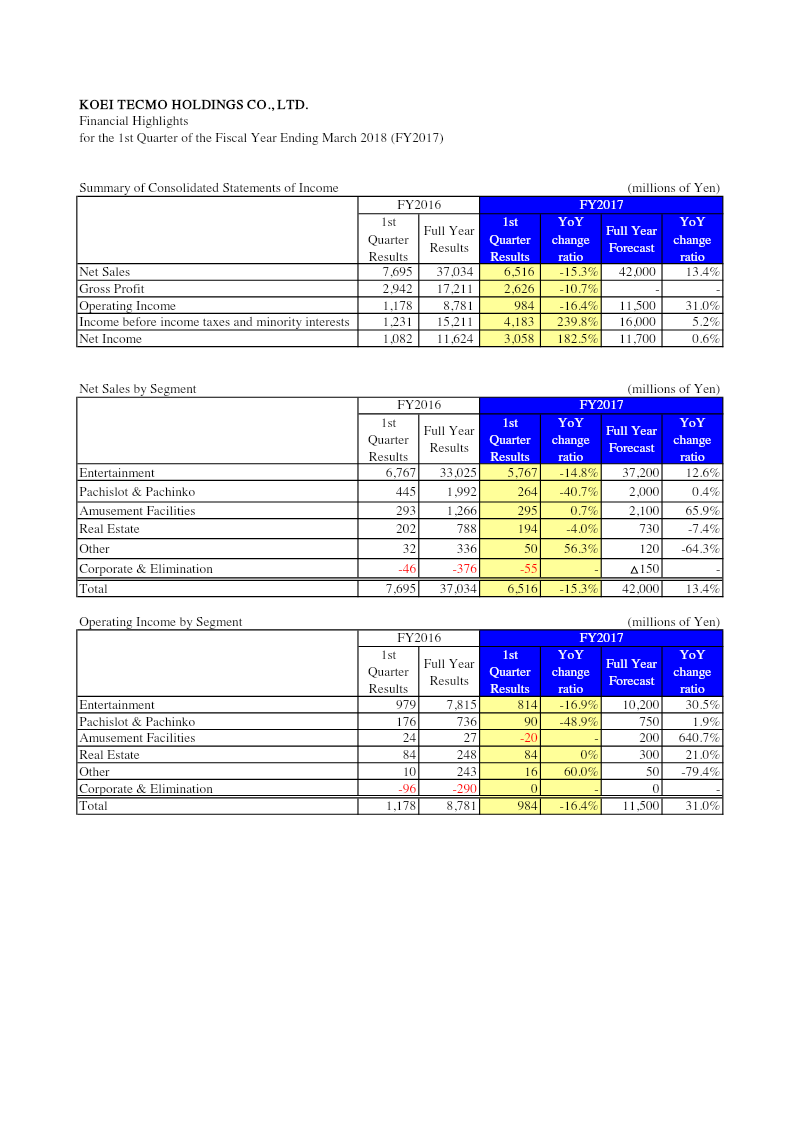

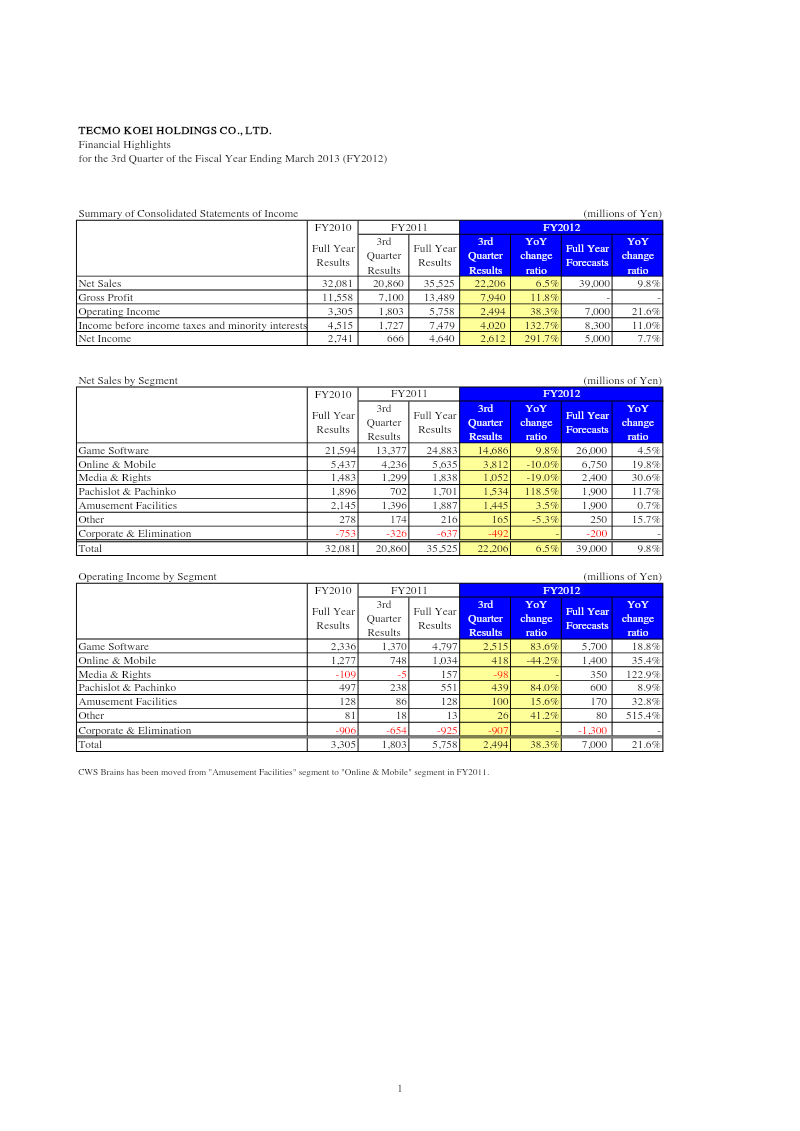

Financial Highlights: 3rd Quarter of the Fiscal Year Ending March 2013

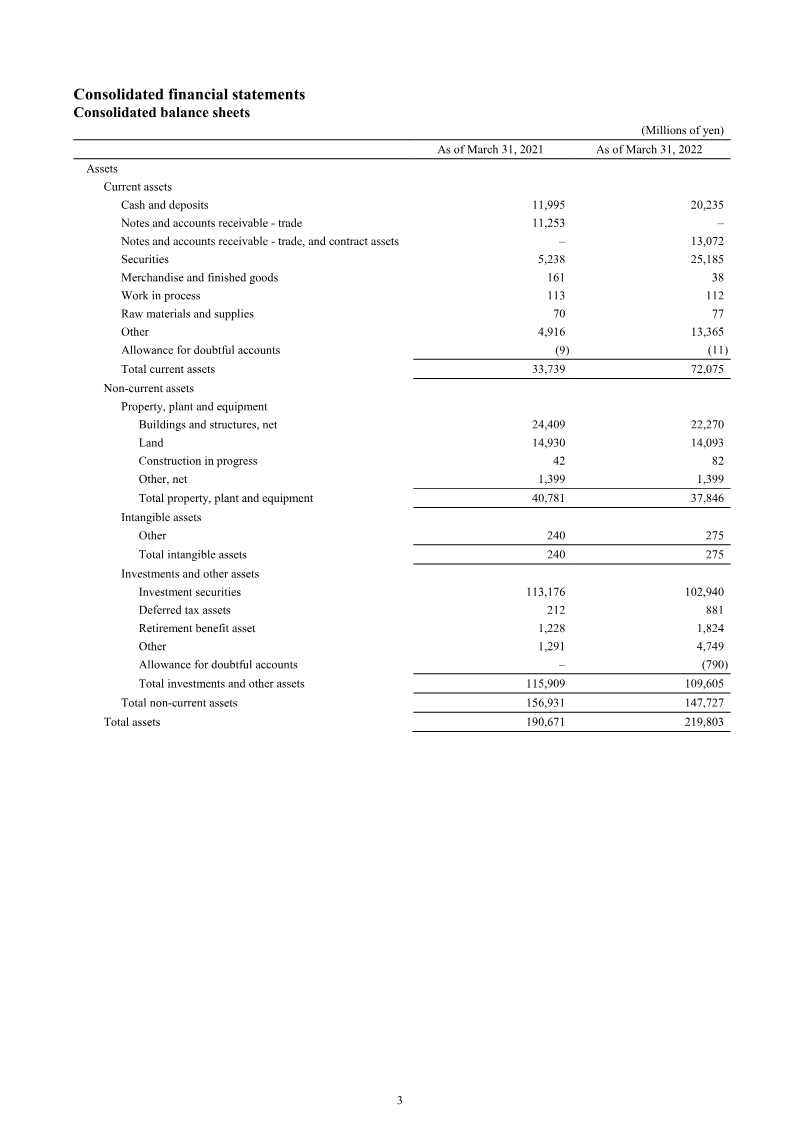

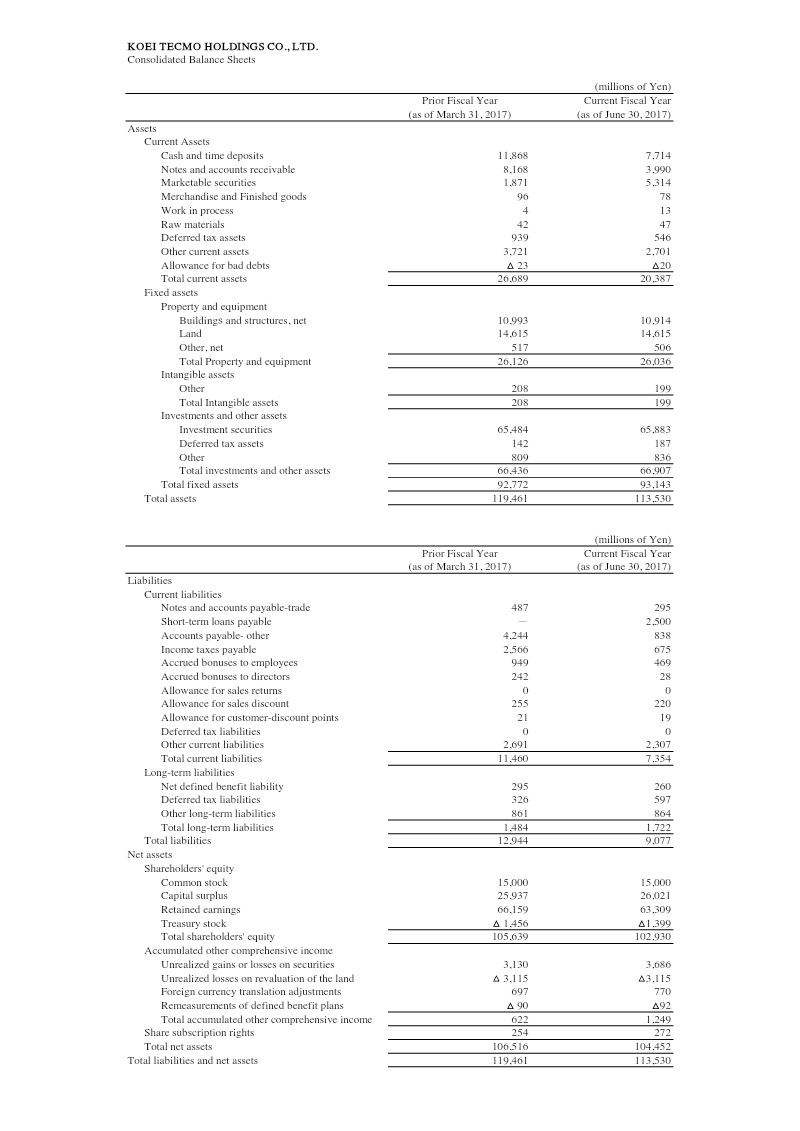

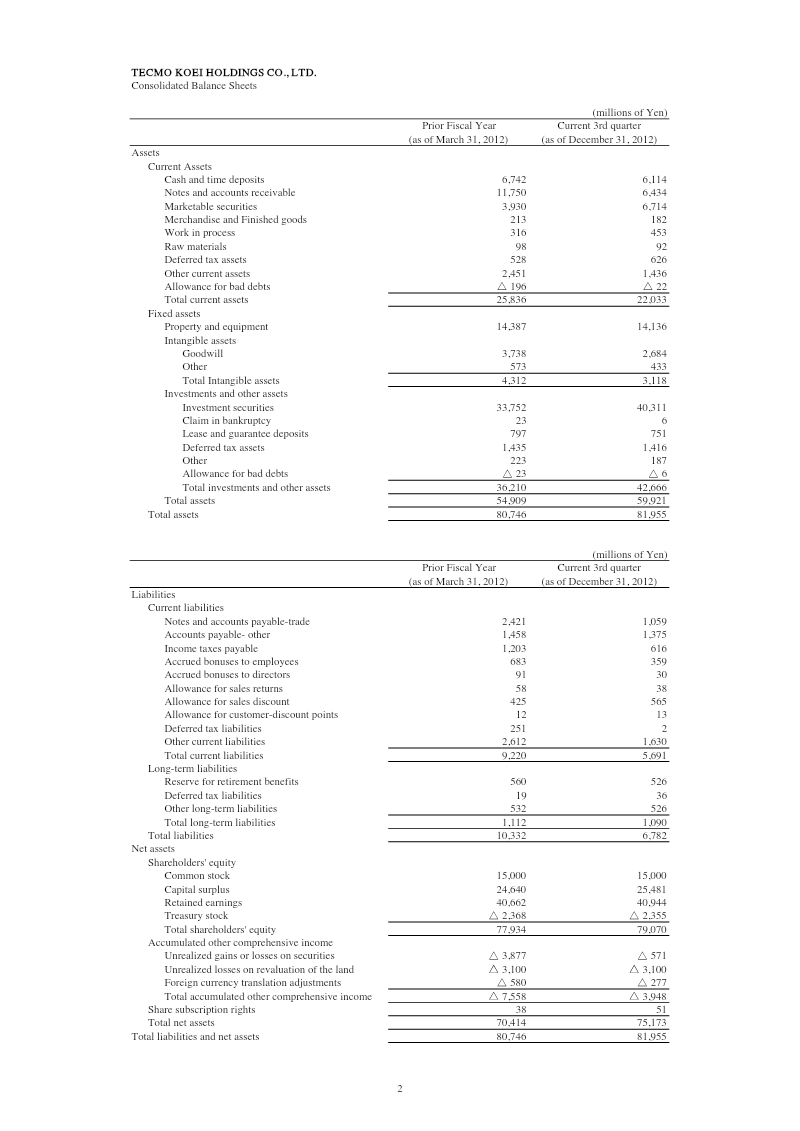

Financial highlights for the third quarter of fiscal year 2012 demonstrate robust growth across Tecmo Koei Holdings’ core segments. Net sales rose to ¥35,525 million from ¥32,081 million in the prior year, a 6.5% increase that exceeded the forecasted 9.8%. Gross profit climbed to ¥13,489 million, up 11.8% year‑on‑year, while operating income surged to ¥5,758 million, a 38.3% rise driven largely by the Game Software segment, which contributed ¥4,797 million in operating profit—an 83.6% jump from the previous year’s ¥2,336 million. Online & Mobile sales increased modestly to ¥5,635 million, though operating income in that segment fell 44.2% to ¥1,034 million due to higher marketing costs. Media & Rights experienced a 98% increase in operating income, moving from a loss of ¥109 million to a profit of ¥157 million. Pachislot & Pachinko and Amusement Facilities also posted gains, with operating incomes of ¥551 million (84.0% increase) and ¥128 million (15.6% increase), respectively. Net income for the quarter reached ¥4,640 million, a 291.7% increase over the prior year’s ¥666 million, reflecting higher operating margins and favorable tax treatment. The company’s balance sheet strengthened, with total assets rising to ¥59,921 million and shareholders’ equity increasing to ¥79,070 million. Current assets grew from ¥25,836 million to ¥22,033 million, while current liabilities fell from ¥9,220 million to ¥5,691 million, improving liquidity. Investment securities expanded significantly, contributing to the asset growth. The report covers Japan‑based operations for FY2012, with data presented in millions of yen. Key metrics are derived from consolidated financial statements and segment reporting, offering a comprehensive view of performance trends across gaming software, online/mobile, media rights, and amusement sectors.

Koei Tecmo

Report

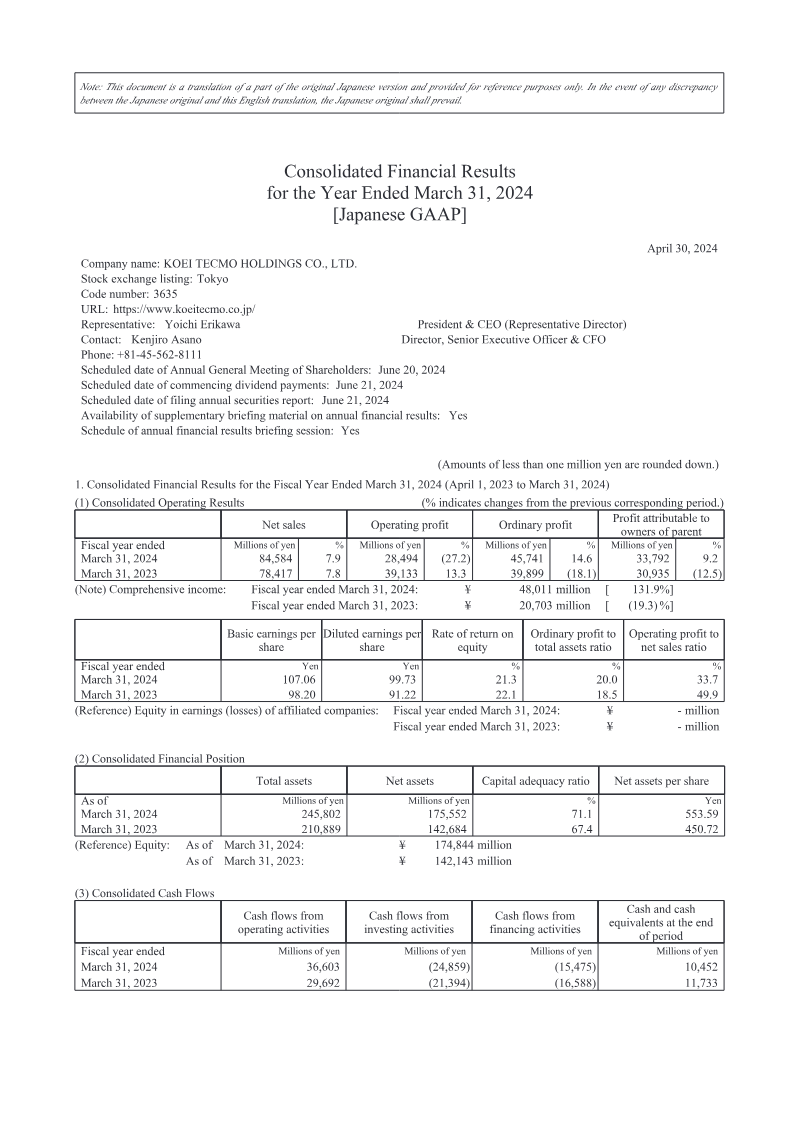

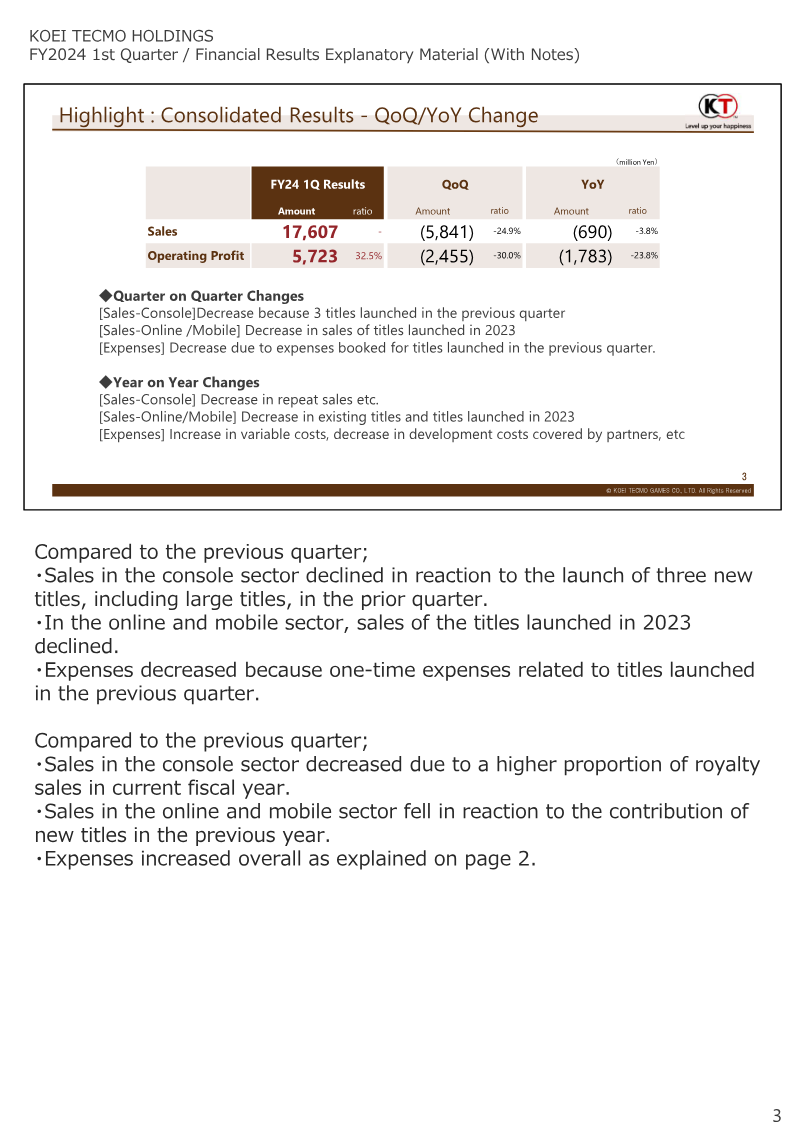

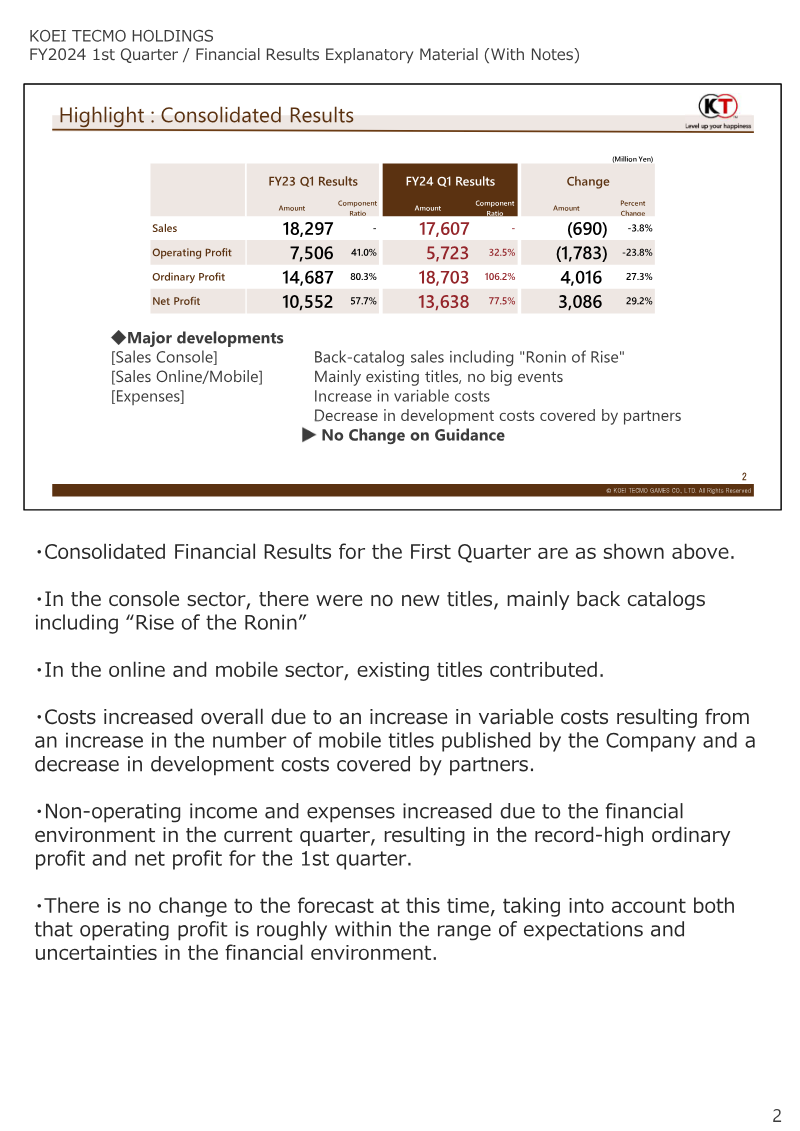

Financial Results for the First Quarter: Fiscal Year Ending March 2025

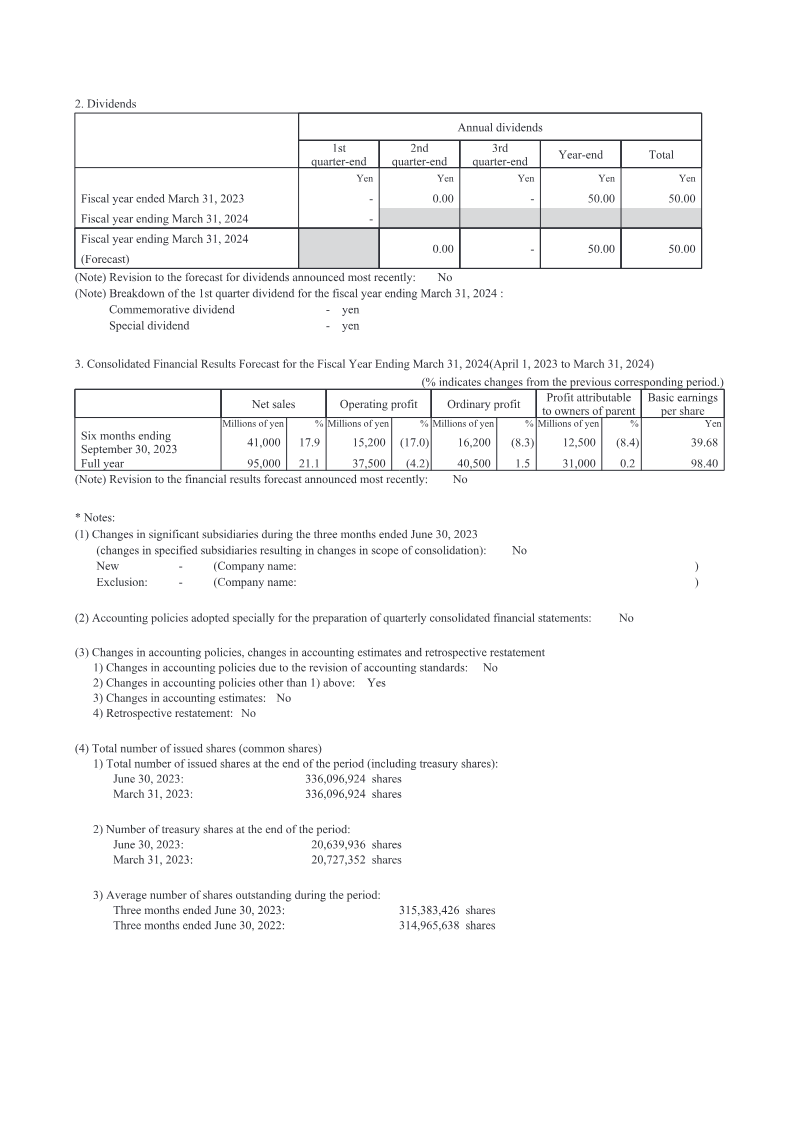

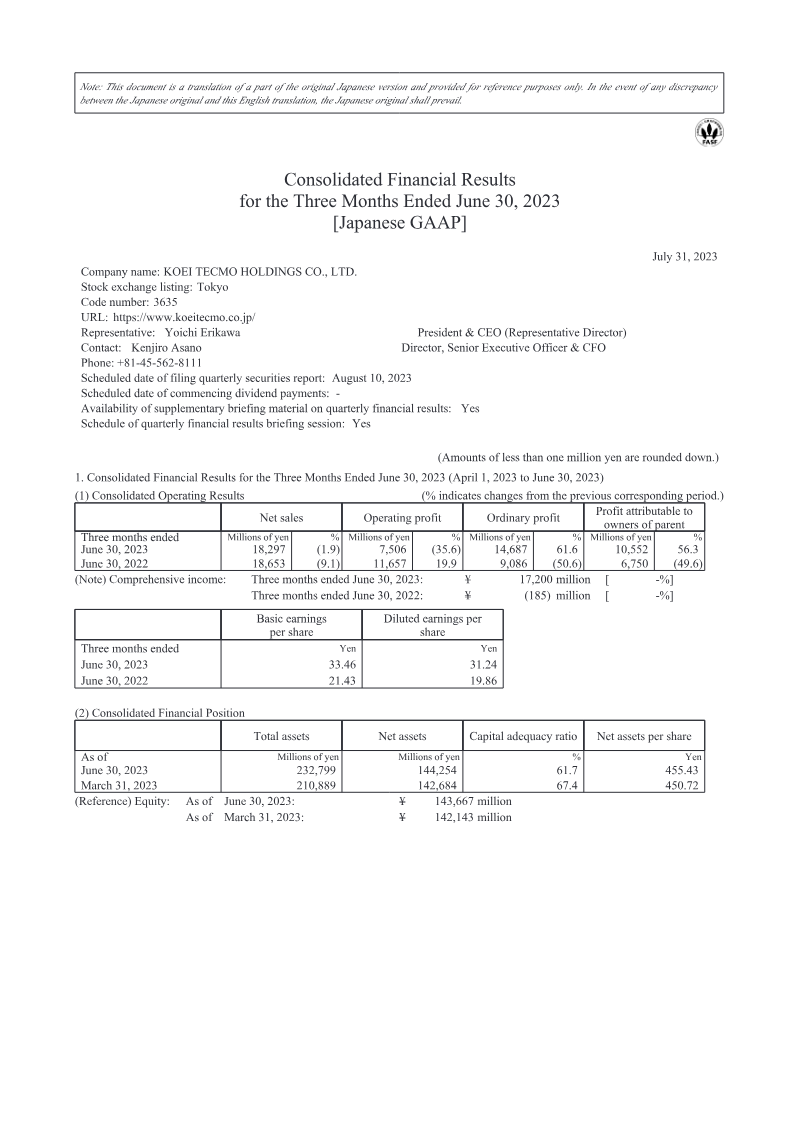

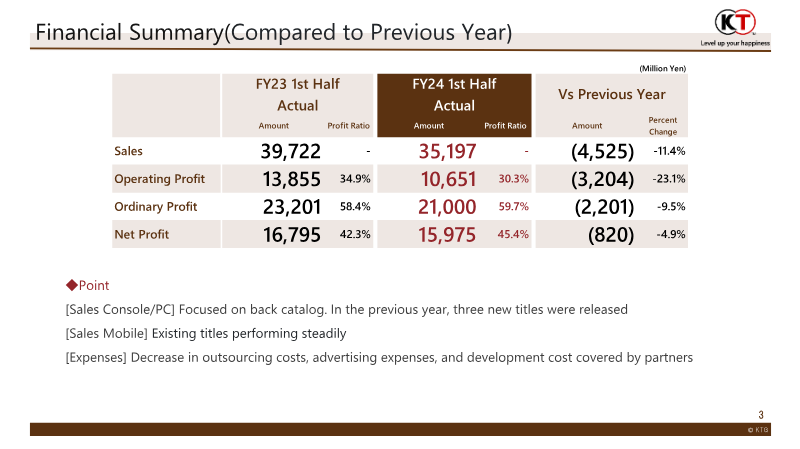

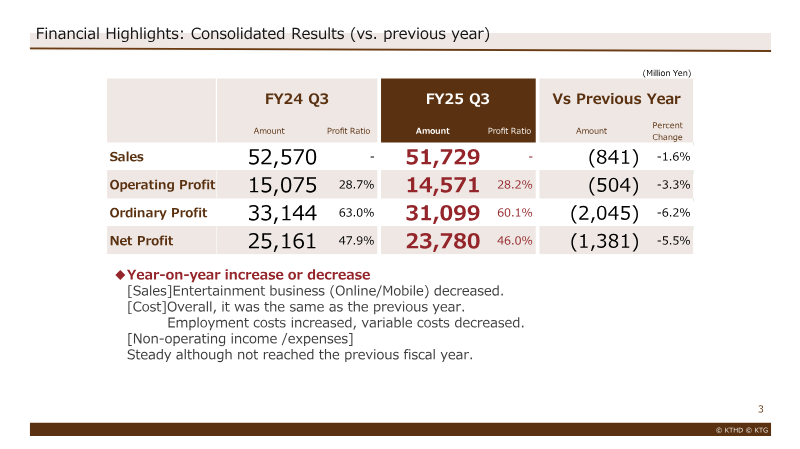

Financial results for the first quarter of fiscal year ending March 2025 show a modest decline in consolidated sales to ¥17.6 billion, down 3.8 % YoY and 24.9 % QoQ, driven by weaker console sales after a strong launch in the prior quarter and declining online/mobile revenue from titles introduced in 2023. Operating profit fell ¥1.78 billion, a 23.8 % YoY drop and 30 % QoQ decline, largely due to higher variable costs from an expanded mobile portfolio and reduced partner‑covered development expenses. Ordinary profit rose ¥4.02 billion (27.3 % YoY) and net profit increased to ¥13.64 billion (29.2 % YoY), supported by higher non‑operating income amid a volatile financial environment. Segment analysis indicates the entertainment division—comprising console and mobile businesses—experienced a 3.1 % sales decline, with physical console units falling 7.4 % and digital downloads dropping 5.9 pp. The amusement segment saw a modest sales drop, while real‑estate sales decreased due to property disposals but profit rose from lower repair costs. Regional performance shows Japan sales down 6.9 %, overseas up 0.5 %, North America up 5.3 %, Europe up 101.7 % (though still small in volume), and Asia down 11.3 %. Methodologically, the report aggregates quarterly data from all operating segments, with expense breakdowns by employment, outsourcing, and advertising costs. No change to FY 2024 guidance is announced; the company maintains a conservative plan of ¥90 billion sales and ¥30 billion operating profit for the full year, with a focus on repeat console titles, steady online/mobile revenue, and incremental royalty income.

Koei Tecmo