Back to Writers

Koei Tecmo

Game Co.

212 documents

Japanese developer/publisher. Dynasty Warriors, Nioh, Dead or Alive, Atelier, Romance of the Three Kingdoms.

Documents

Report

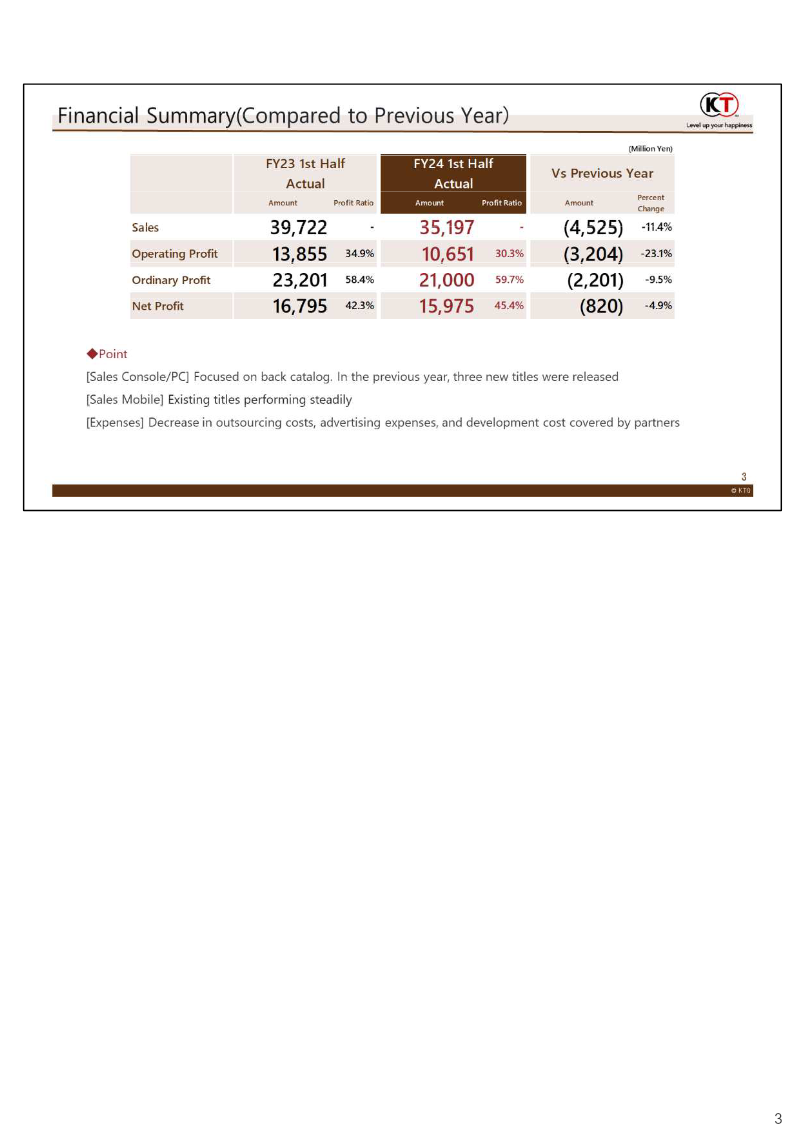

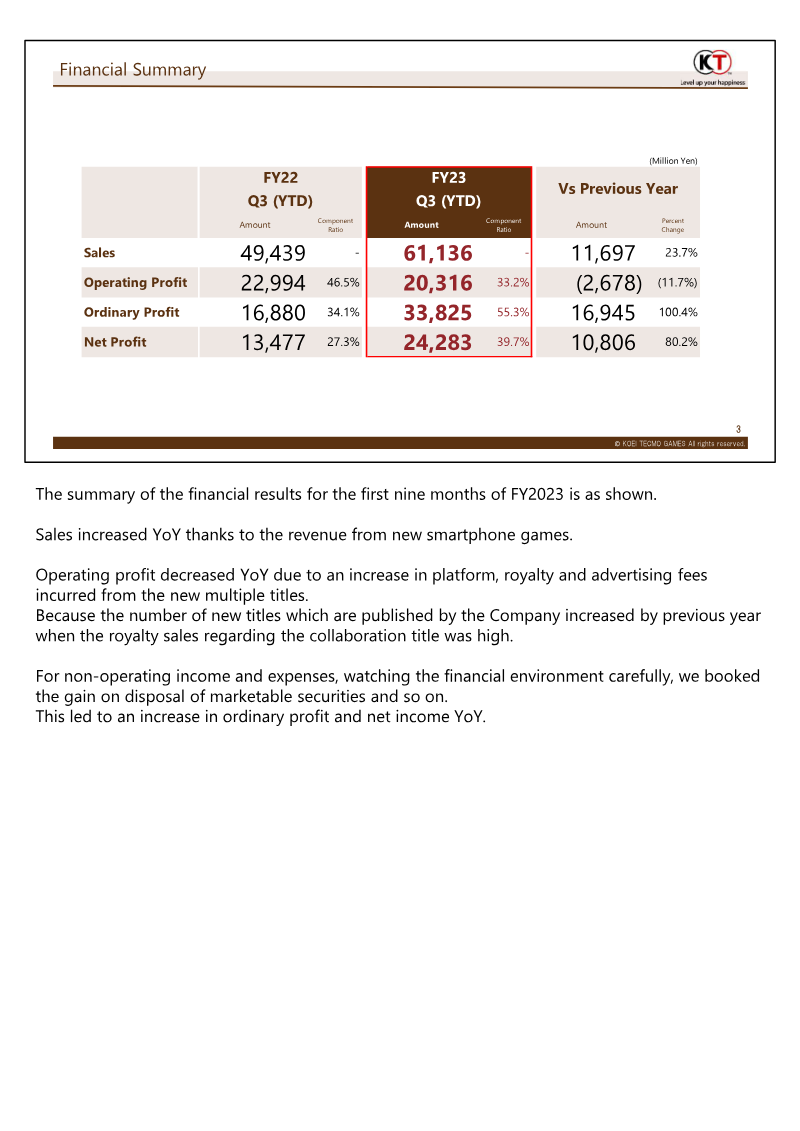

Financial Results for the Third Quarter: Fiscal Year Ending March 2024

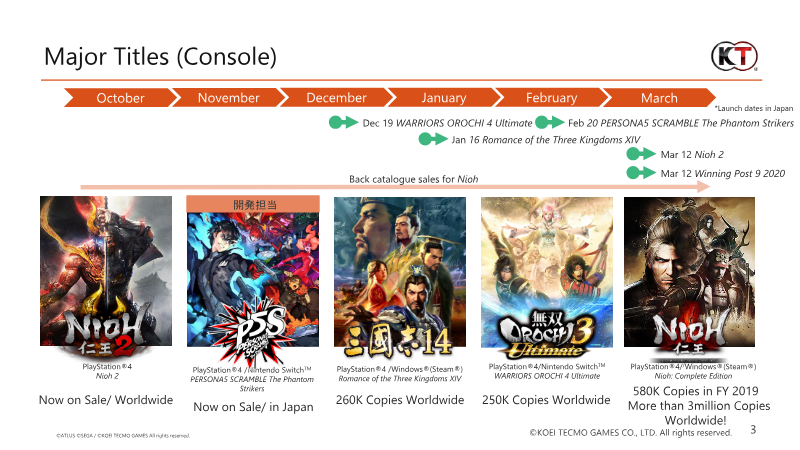

The quarterly financial release outlines KOEI TECMO HOLDINGS CO., LTD.’s performance for the first nine months of fiscal 2023, ending March 2024. Total sales rose 23.7 % YoY to ¥61,136 million, driven primarily by new mobile titles that boosted online and mobile game revenue. Operating profit fell 11.7 % to ¥20,316 million due to higher platform, royalty and advertising costs associated with the expanded title portfolio. Ordinary profit increased 100.4 % to ¥33,825 million and net profit grew 80.2 % to ¥24,283 million, largely supported by gains from marketable securities and other non‑operating items. Geographically, Japan contributed 61.1 % of sales while overseas sales accounted for 38.9 %, with the United States and Europe showing modest declines in unit volumes but maintaining strong digital sales. The entertainment segment recorded a 24 % YoY sales increase, with mobile and online channels contributing 47.1 % of segment revenue; console package sales declined by 10.3 %. Digital sales ratio for the entertainment sector rose to 84.2 %, reflecting a shift toward downloadable content and mobile downloads. Cost analysis revealed a 12.9 % rise in employment costs, a 78.8 % jump in subcontracting expenses, and a 92.8 % increase in advertising spend, all linked to new title launches. The company maintains its FY2024 operating profit target of ¥37,500 million, citing anticipated revenue from the March release of “Rise of the Ronin” and continued expansion in mobile markets.

Koei Tecmo

Report

Financial Results for the Fiscal Year Ending March 2020

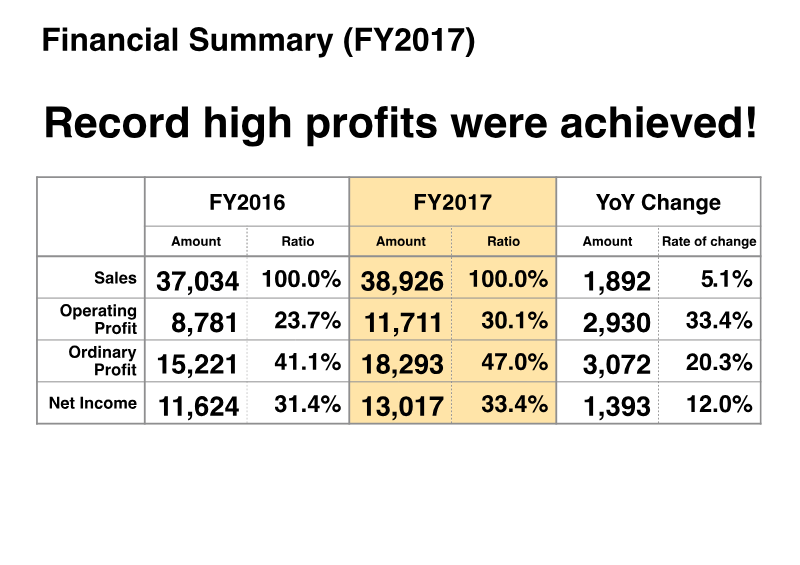

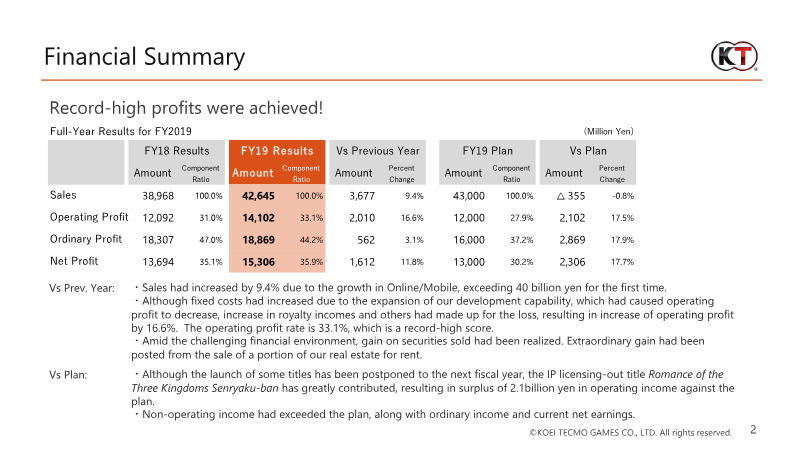

The fiscal year ending March 2020 saw KOEI TECMO HOLDINGS achieve record‑high profitability, with sales rising 9.4 % to ¥42.6 billion and operating profit increasing 16.6 % to ¥14.1 billion, a 33.1 % operating margin that tops the company’s historical peak. Net profit climbed 11.8 % to ¥15.3 billion, supported by gains on securities and real‑estate sales, offsetting higher fixed costs from expanded development capacity. The company’s earnings plan for FY 2019 was surpassed, largely due to the licensing‑out success of “Romance of the Three Kingdoms Senryaku‑ban,” which generated substantial royalty income, and strong performance in new console titles such as Nioh 2. Geographically, overseas sales grew 27.1 % to ¥15.8 billion, with Asia contributing the largest share of growth (52 % increase in unit sales). Digital downloads and DLCs also expanded, with console download sales up 39.6 % to ¥7.9 billion and DLC revenue rising 35.2 %. The entertainment segment’s online/mobile division drove a 42.4 % jump in mobile and social game revenue, reflecting successful IP licensing and self‑developed titles. Operationally, headcount rose 4.4 % to 1,835 employees, and capital expenditures reached ¥14.3 billion for the new Minato‑Mirai office and music hall. Management emphasized cautious earnings guidance for FY 2020 amid COVID‑19 uncertainty, while outlining a mid‑term strategy focused on global IP creation, multi‑platform expansion, and ESG commitments. Dividend policy maintained a 50 % payout ratio, with FY 2019 dividends planned at ¥61 per share.

Koei Tecmo