ReportSlovak Game Developers Association

Slovak Game Development Industry 2023

1 Jan 20234 pages~4 min full read

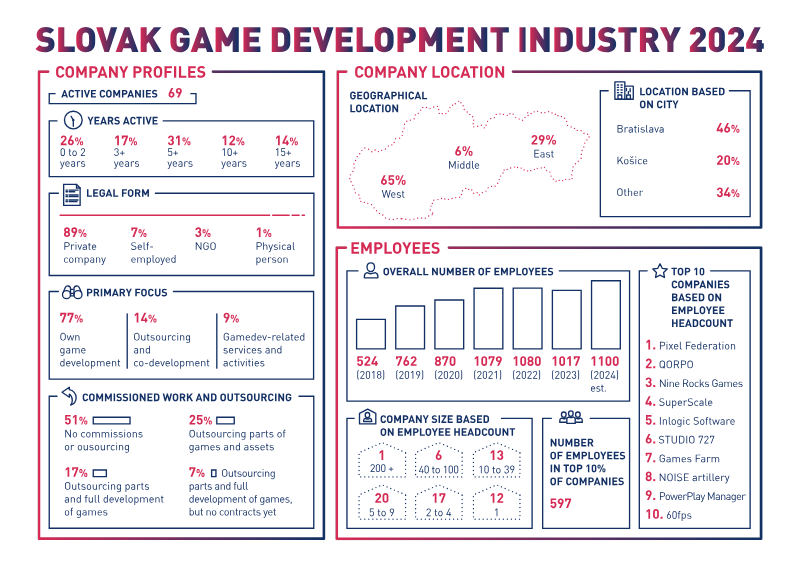

The Slovak game industry is highly centralized, with the top 10% of companies accounting for 60% of the 1,120-person workforce and 84.6% of the total annual turnover.

Industry revenue has plateaued, with turnover reaching €77.1 million in 2022 and an estimated €76.9 million in 2023.

Pixel Federation, SuperScale, and Inlogic Software are the dominant market leaders in both headcount and revenue.

The workforce has grown significantly since 2017, rising from 476 employees to 1,120 by 2023, though recruitment for specialized roles like programmers and designers remains difficult.

While 89% of companies utilize remote or hybrid work models, firms are increasingly reliant on international talent, with nearly half employing staff from countries like Czechia and Ukraine.

PC is the primary development platform, yet 50% of all projects remain unpublished, and most released titles are self-published via digital storefronts.

Public funding is utilized by 37.9% of companies, though industry stakeholders are actively lobbying for expanded state support through tax incentives and improved digital arts education.

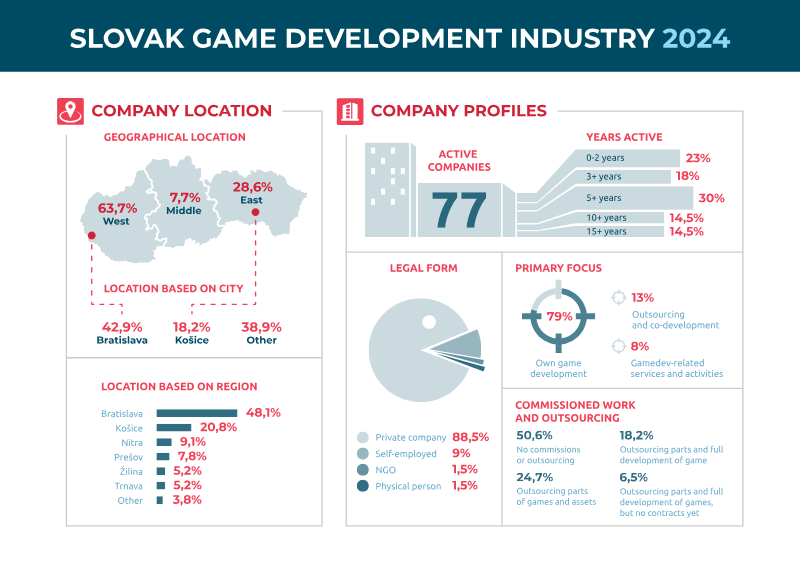

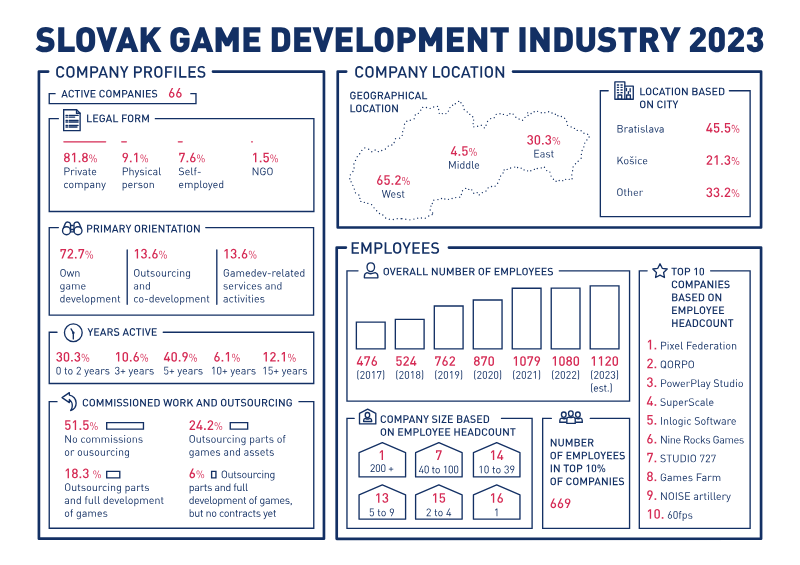

The Slovak game development industry in 2023 is characterized by a stable ecosystem of 66 active companies, primarily concentrated in the western region of the country. The sector is dominated by private entities, with 72.7% focusing on core game development and the remainder providing outsourcing or specialized services. While the industry features a mix of experience levels, over 40% of companies have been active for more than five years. The workforce has seen consistent growth, rising from 476 employees in 2017 to an estimated 1,120 in 2023. However, the industry exhibits significant centralization, with the top 10% of companies employing approximately 60% of the total workforce and generating 84.6% of the annual turnover.

Financial data indicates a mature but plateauing market, with an overall turnover of €77.1 million in 2022 and a nearly identical estimate of €76.9 million for 2023. Pixel Federation, SuperScale, and Inlogic Software lead the market in both headcount and revenue. Development is largely self-funded, though 37.9% of companies utilize public funding. PC remains the primary target platform for development, followed by mobile and consoles. Notably, half of all projects remain unpublished, while those that reach the market are predominantly self-published via digital storefronts like Steam, Google Play, and the App Store.

The labor market reveals a workforce with a median age of 30, where women represent 19% of the total headcount, primarily occupying roles in graphic arts and community management. Recruitment remains a challenge for specialized roles, particularly for programmers and game designers. To address talent shortages, nearly half of Slovak firms employ international staff, largely from Czechia and Ukraine. Operational trends show a decisive shift toward flexible work arrangements, with over 89% of companies utilizing remote or hybrid office models. Industry stakeholders express a strong desire for increased state support, specifically through tax incentives and improved education for the digital arts.