Report

Netherlands Games Monitor 2024

AUTHORS SPECIAL THANKS TO Manuel Kerssemakers (Abbey Christel van Grinsven APPLIED Games) Arjan Terpstra Bowie Derwort (Game Tailors) Laurens Rutten (CoolGames Matthijs Dierckx Michaël Bas (&ranj) & Dutch Games Association) Roger ter Heide (Improvive) Tuur Hendrikx (Sonic Picnic) RESEARCH CHAPTER 1 ...

Dutch Games AssociationJan 2024

Report

Dutch Games Monitor 2022: Factsheet

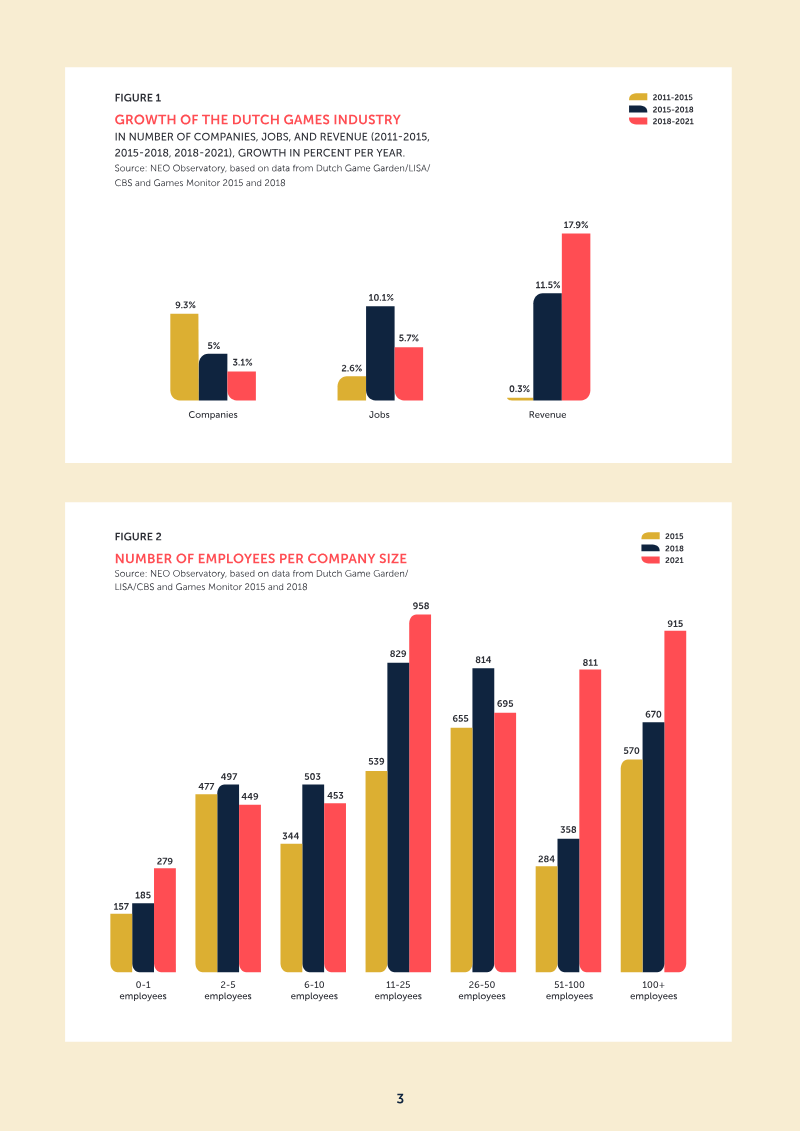

The Dutch Games Monitor 2022 provides a comprehensive analysis of the Netherlands' video game industry, covering the period from 2018 to 2021. The primary objective is to evaluate the sector's growth, maturity, and structural evolution. The research methodology incorporates desk research, roundtable discussions, and a survey of approximately 500 companies, yielding nearly 200 responses. The analysis focuses on two distinct domains: entertainment games and applied (serious) games, which serve sectors such as healthcare and education. The industry demonstrates significant maturation, characterized by a shift from an initial increase in the number of companies to a more recent surge in revenue and employment. By the end of 2021, the sector comprised 630 companies, generating between €420 million and €440 million in annual revenue. This represents an average annual revenue growth of nearly 18%, outpacing global industry averages. Employment also expanded, reaching 4,560 jobs with an annual growth rate exceeding 5%. This job creation is particularly concentrated in larger organizations, with the number of scale-ups employing over 50 people doubling to 12 companies over the three-year period. Geographically, the Greater Amsterdam region leads in total employment, while Utrecht maintains the highest concentration of applied game developers. Although the number of dedicated game education programs has slightly decreased, the industry is seeing a rise in diversity, with the percentage of women in the workforce reaching 23% by 2021. Furthermore, the sector is increasingly characterized by international expansion, a rise in external investments, and a growing number of mergers and acquisitions, signaling that the Dutch games industry is successfully transitioning into a more mature and globally competitive market.

Dutch Games AssociationJan 2022

Report

Dutch Games Monitor 2022

TEXT AND ANALYSIS DESIGN All rights reserved NEO Observatory COVER IMAGE This publication is made possible with Walter Manshanden Horizon Forbidden West the support of Province of Utrecht, by Guerrilla Games Gemeente Utrecht, HKU: University of PROOFREADING AND the Arts Utrecht, Breda University of GENERAL SUPPORT SPECIAL THANKS TO Applied Sciences (BUAS), Hanze Marilla Valente ...

Dutch Games AssociationJan 2022

Report

Games Monitor: The Netherlands 2020 Update – COVID Impact

This update provides an analysis of the Dutch video game industry’s performance during 2020, specifically examining the operational and economic impacts of the COVID-19 pandemic. The findings are based on a survey of over 100 industry professionals conducted in late 2020, supplemented by desk research and database updates. The report tracks industry growth, employment trends, and the shift in business dynamics necessitated by global lockdowns. The Dutch games sector demonstrated resilience, growing from 575 companies in 2018 to 615 by the end of 2020, with total employment reaching approximately 4,000 jobs. While the industry largely transitioned to remote work with minimal impact on output quality, the pandemic created a divide between business-to-consumer (B2C) and business-to-business (B2B) entities. B2C entertainment companies generally benefited from increased consumer demand for home-based entertainment. Conversely, B2B and applied game developers faced significant challenges in the spring of 2020 as client projects were paused or canceled, though some firms in the healthcare sector identified new opportunities. Operational challenges were primarily centered on human resources and networking. While productivity remained stable for most, employee engagement declined due to the loss of informal office culture, and nearly half of respondents reported increased stress levels. The absence of physical industry events hindered the establishment of new business relationships, with one-third of respondents unable to pursue new business opportunities effectively. Despite these hurdles, the industry maintained its growth trajectory, supported by government labor cost subsidies that assisted approximately 85 companies during the initial lockdown phases. Overall, the sector proved adaptable, leveraging digital infrastructure to sustain operations while navigating a volatile market environment.

Dutch Game GardenJan 2020

Report

The Games Monitor 2018

We are honored to present The Games Monitor 2018 edition with the latest facts, figures, trends and developments in the Dutch games industry. The Games Monitor was first published in 2012 and was followed by new research in 2015. Both reports generated a lot of interest into the Dutch games industry’s facts and figures, which is why we are pleased to be able to provide you with an update for 2018.

Dutch Games AssociationJan 2018

Report

Games Monitor: The Netherlands 2018

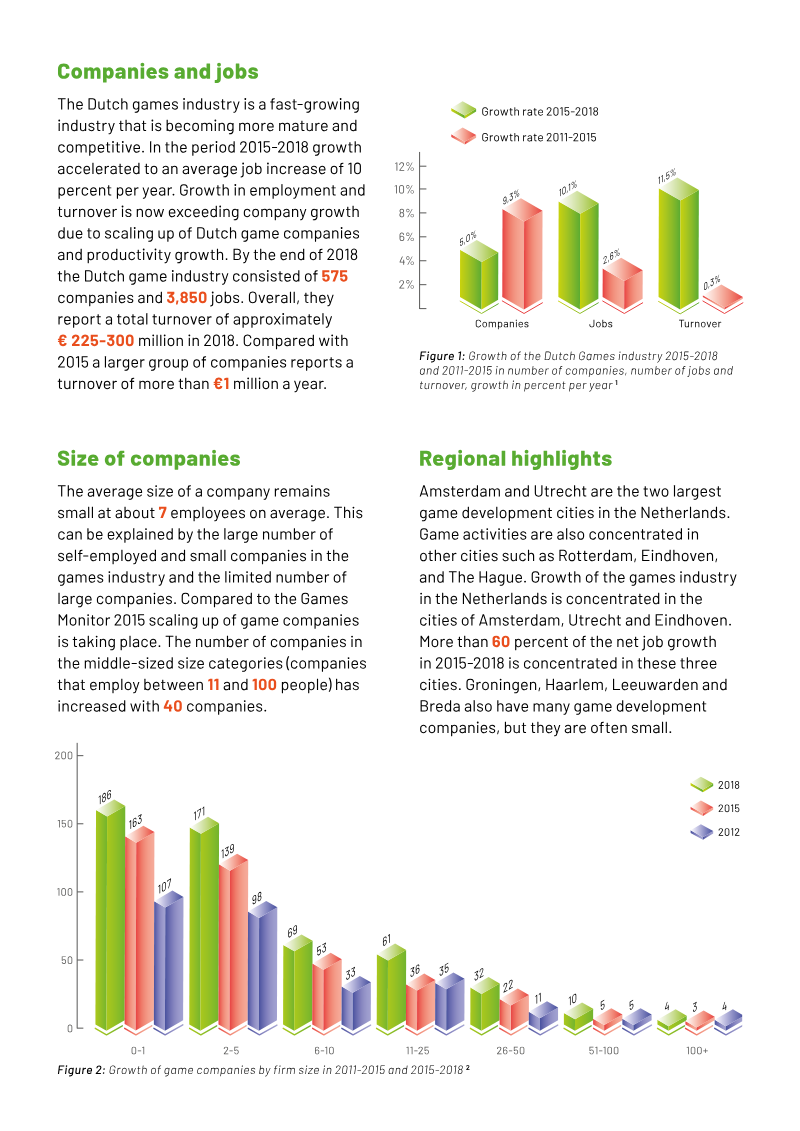

The Games Monitor 2018 provides a comprehensive analysis of the Dutch video games industry, tracking its evolution and maturation between 2015 and 2018. The industry is defined by companies whose core activities involve the development, production, publication, or distribution of electronic games, categorized into entertainment and applied (serious) games. The research methodology combined desk research with a survey of 165 companies, supplemented by industry roundtable discussions to validate findings. The Dutch games sector experienced accelerated growth during the 2015–2018 period, characterized by an average annual job increase of 10 percent. By the end of 2018, the industry comprised 575 companies and 3,850 jobs, generating an estimated annual turnover of €225–300 million. While the average company size remains small at approximately seven employees, there is a clear trend toward scaling up, evidenced by a significant increase in mid-sized firms employing between 11 and 100 people. Geographically, the industry is concentrated in major urban centers, with Amsterdam, Utrecht, and Eindhoven accounting for over 60 percent of net job growth. Market dynamics show a strong expansion in entertainment game development, which grew by 33 percent, while the applied games sector—primarily serving healthcare, education, and government—has stabilized. Business models in the entertainment sector rely heavily on premium monetization and in-app advertising, whereas applied studios frequently utilize work-for-hire models. The educational landscape remains robust, with 44 game-related study programs producing over 900 graduates annually. Overall, the industry is transitioning toward a more mature, competitive state, marked by increased productivity, strategic acquisitions, and international expansion.

Dutch Games AssociationJan 2018

Report

Dutch Games Monitor: Main Facts & Figures 2015

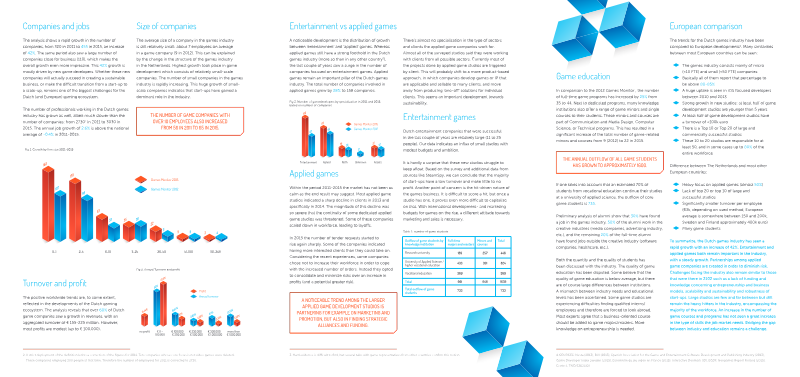

The Dutch games industry experienced significant expansion between 2011 and 2015, characterized by a 42% increase in the number of companies, which grew from 320 to 455. This growth was primarily driven by a surge in new, small-scale game development studios. Despite this rise in firm count, the industry remains dominated by micro-enterprises with an average of seven employees. While the total workforce expanded from 2,730 to 3,030 professionals, the rate of job creation was slower than the rate of company formation, reflecting the challenges start-ups face in scaling operations and achieving long-term sustainability. The industry is bifurcated into entertainment and applied games, with the latter maintaining a particularly strong foothold in the Netherlands compared to other European nations. Applied game studios, which focus on training, education, and health, faced significant market volatility between 2013 and 2014, though demand for these services rebounded sharply by 2015. To mitigate risks associated with the hit-driven nature of the entertainment market and the project-based cycles of applied games, many studios are shifting toward product-based models and forming strategic alliances for marketing and funding. Data for this analysis was gathered through a questionnaire sent to over 400 companies, with 130 responses, supplemented by industry roundtable discussions and existing databases. Financial performance remains modest, with most companies reporting annual profits under €100,000. While the number of game-related educational programs has increased by 25%, a persistent skills gap remains, as studios struggle to find employees with the necessary entrepreneurial and business acumen. Ultimately, while the Dutch ecosystem shows robust growth, the industry continues to grapple with the difficulty of transitioning from small start-ups to larger, commercially stable entities.

Dutch Games AssociationJan 2015

Report

Dutch Games Monitor: The Netherlands 2015

In 2012 the first edition of the Dutch Games Monitor was presented. Whilst maybe not the first research focusing on the Dutch games industry, it was the first where an extensive survey and a series of interviews provided a broad insight into the state of the industry. In the past few years interest in games and data about the games industry has increased. Many people were interested in an updated version of the Games Monitor .

Dutch Games AssociationJan 2015

Report

Gamesmonitor '12: Gamesindustrie Onderzocht

Sinds entertainment games ook de smartphones en tablets hebben ver - overd dankzij hits als Wordfeud en Angry Birds, staat de gamesindustrie volop in de schijnwerpers. Met deze casual games is het spelen van com - puterspelletjes doorgedrongen tot het grote publiek en tot elk moment van de dag. Een laagdrempelig, onderhoudend tijdverdrijf, waarmee mensen zich op een speelse manier kunnen meten met tegenstrevers.

Dutch Games AssociationJan 2012