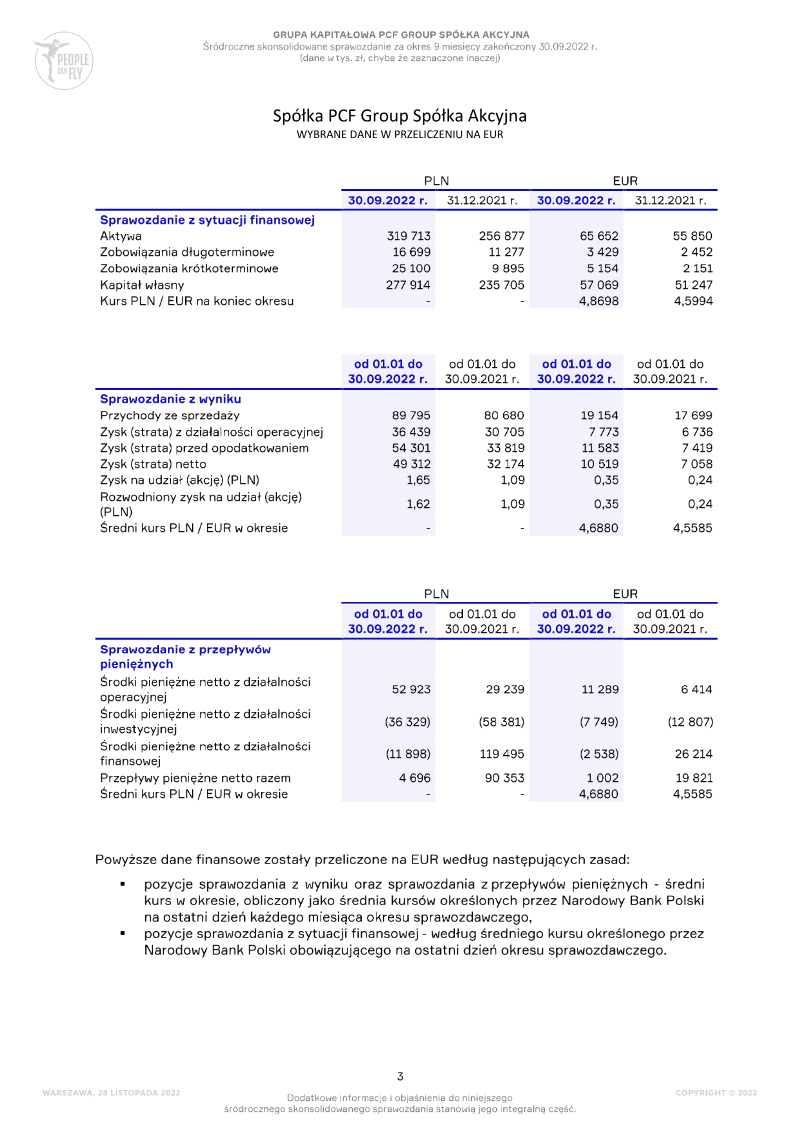

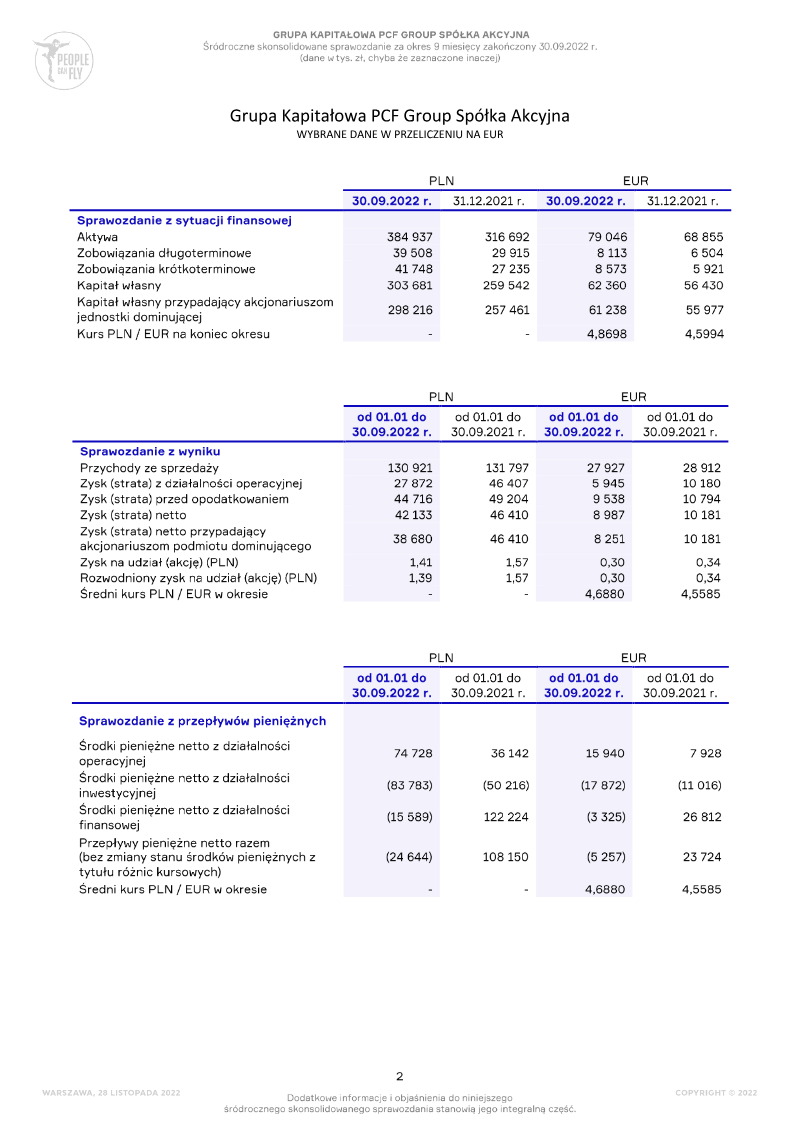

Market Analysis

Report

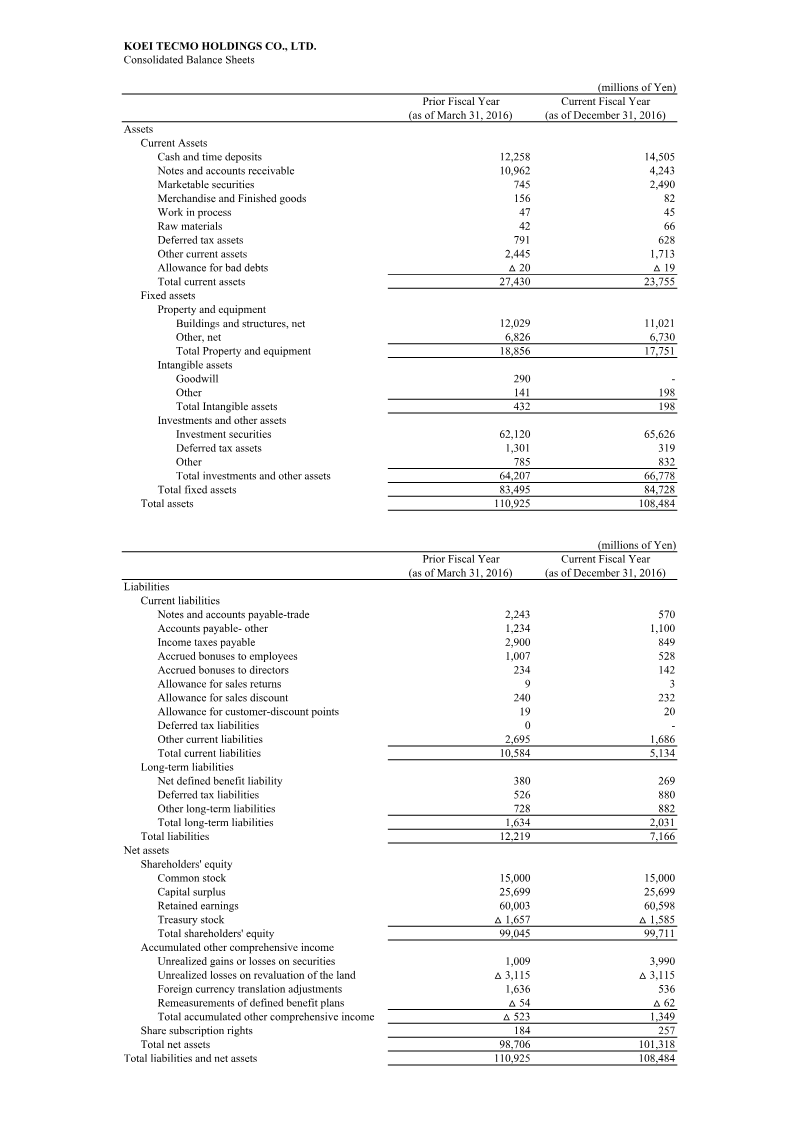

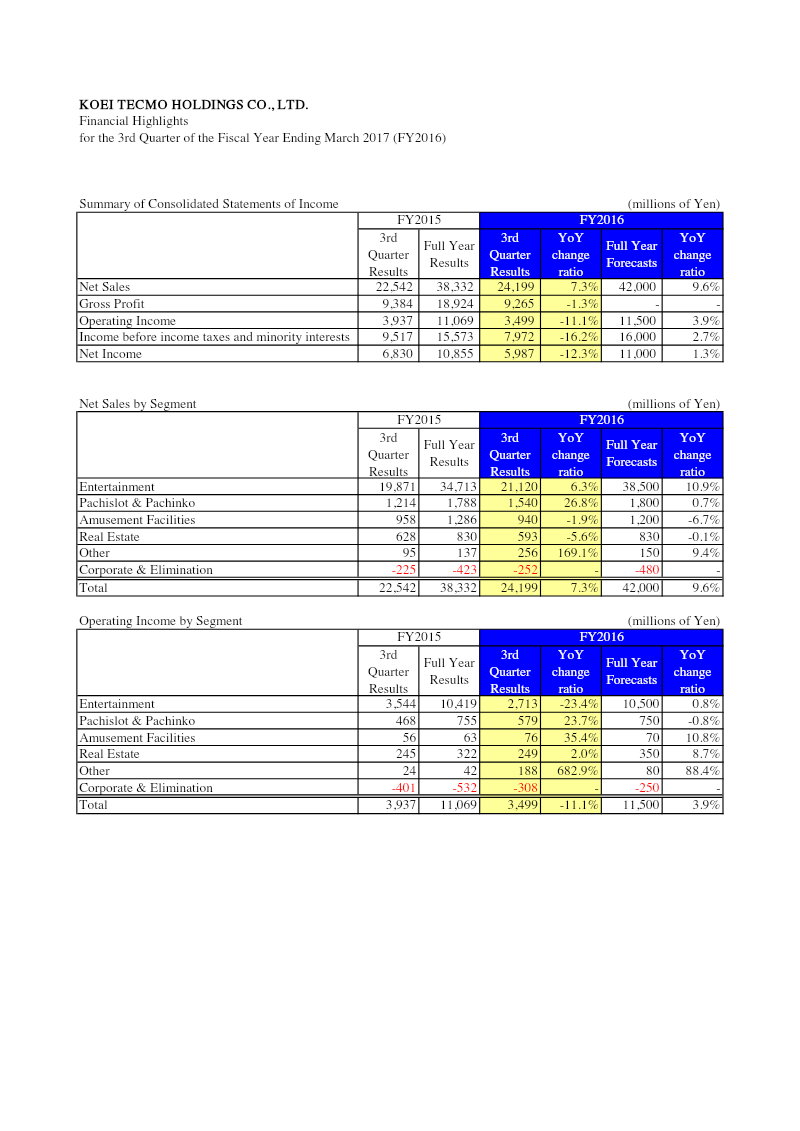

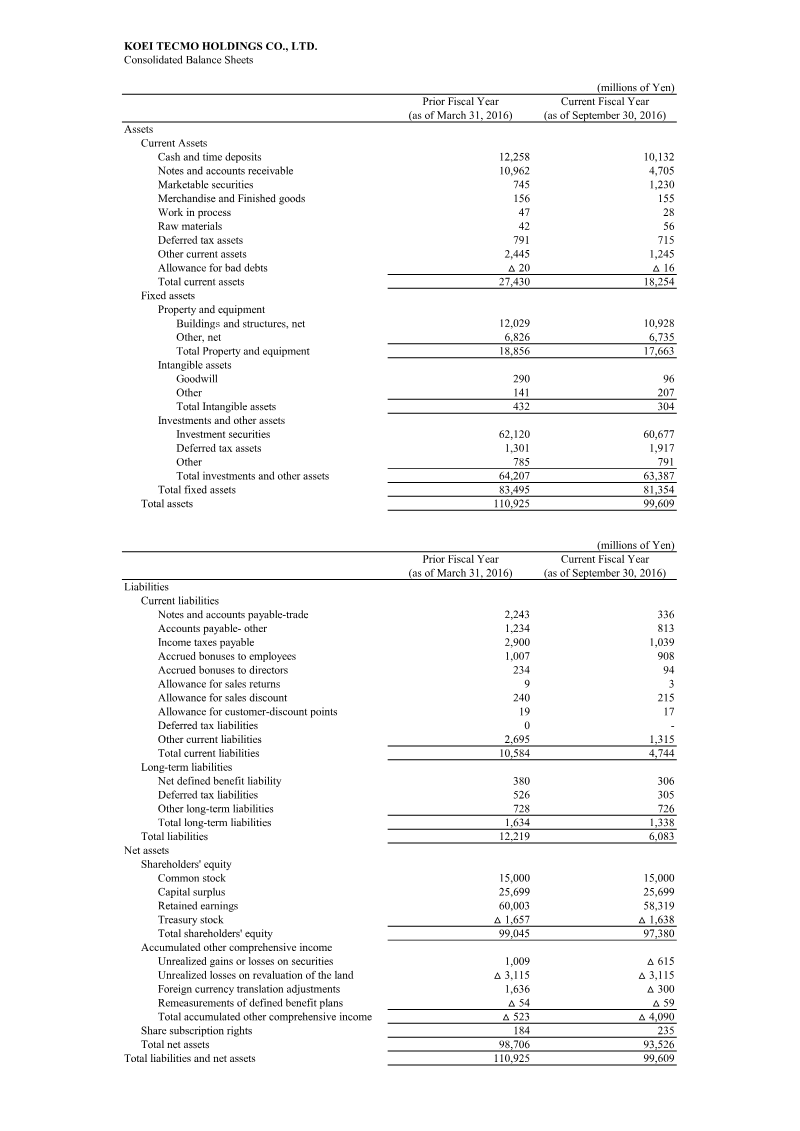

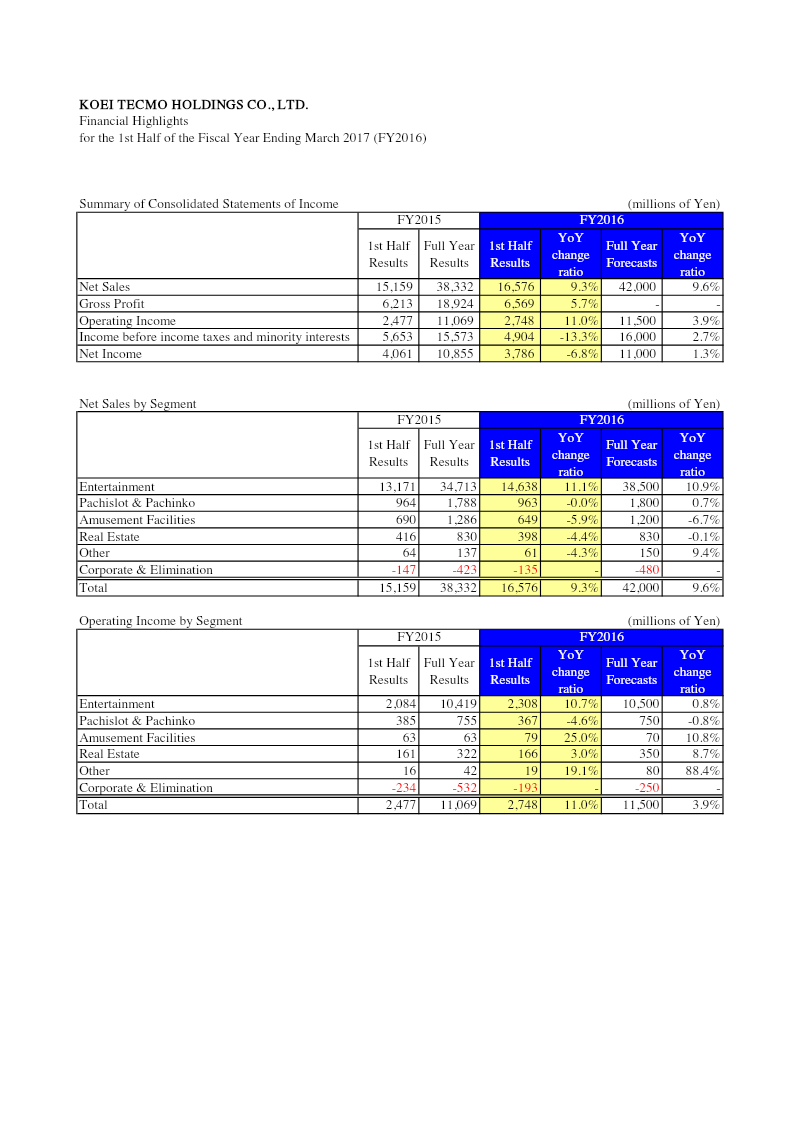

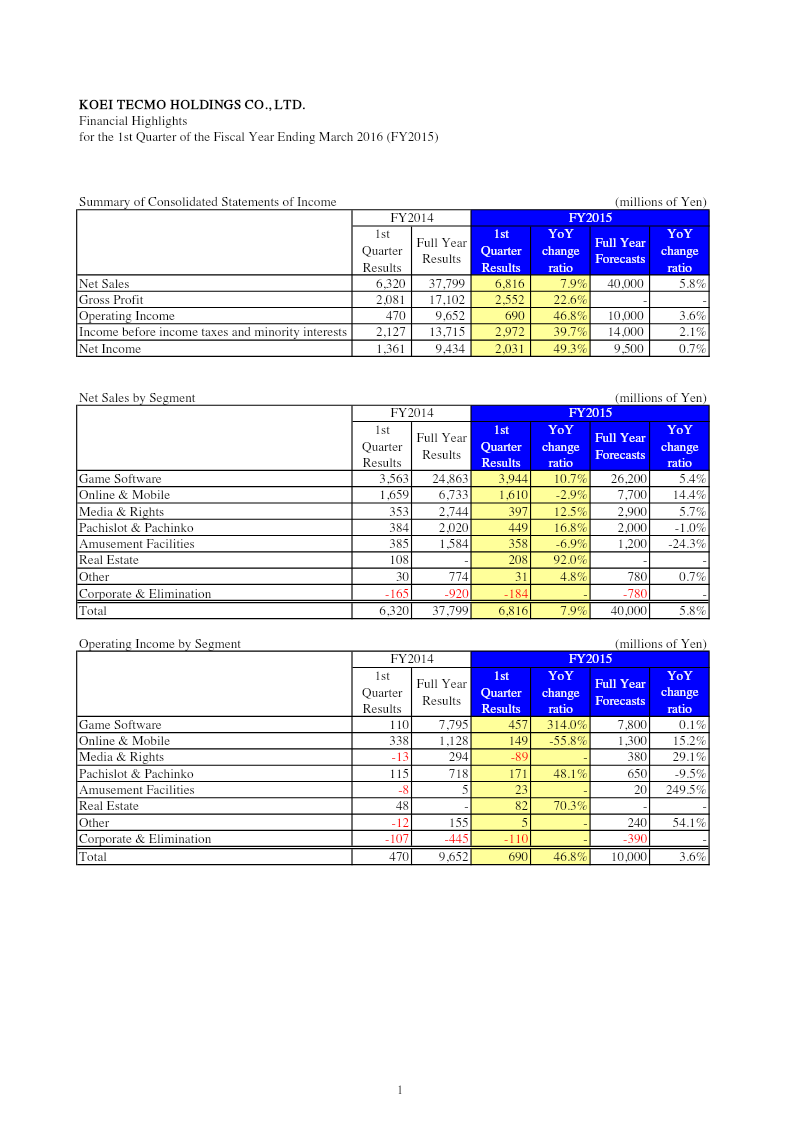

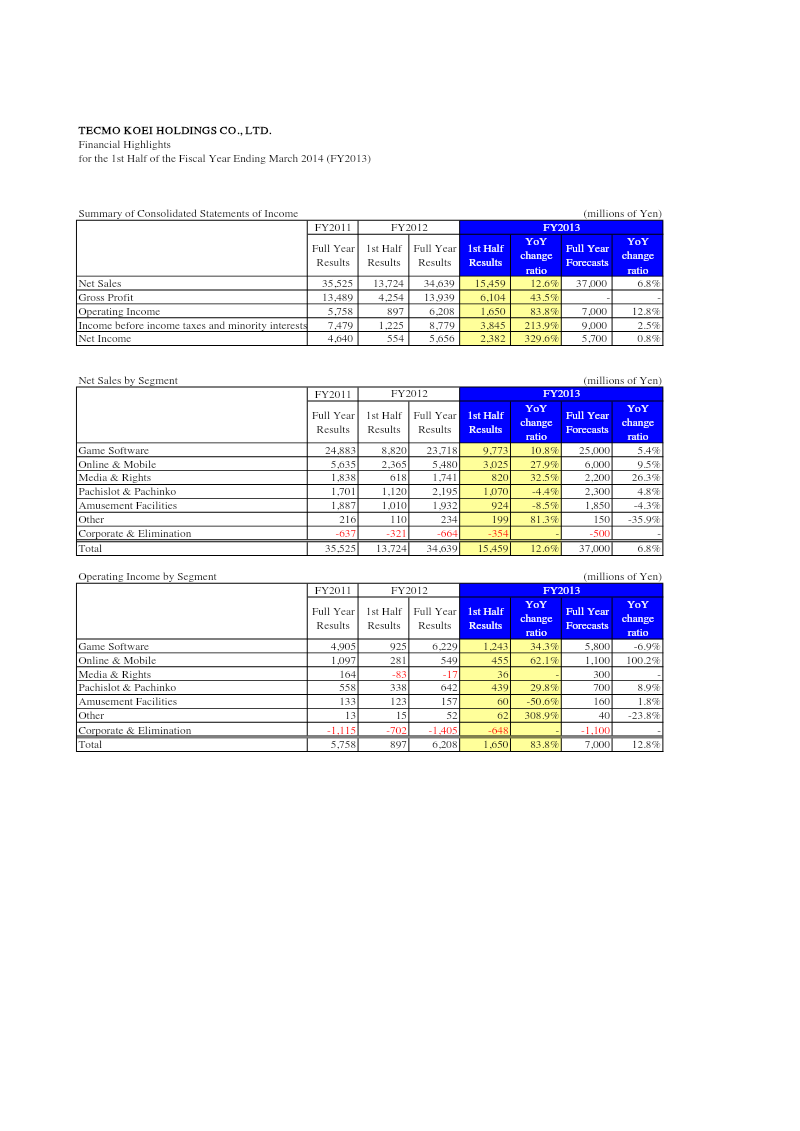

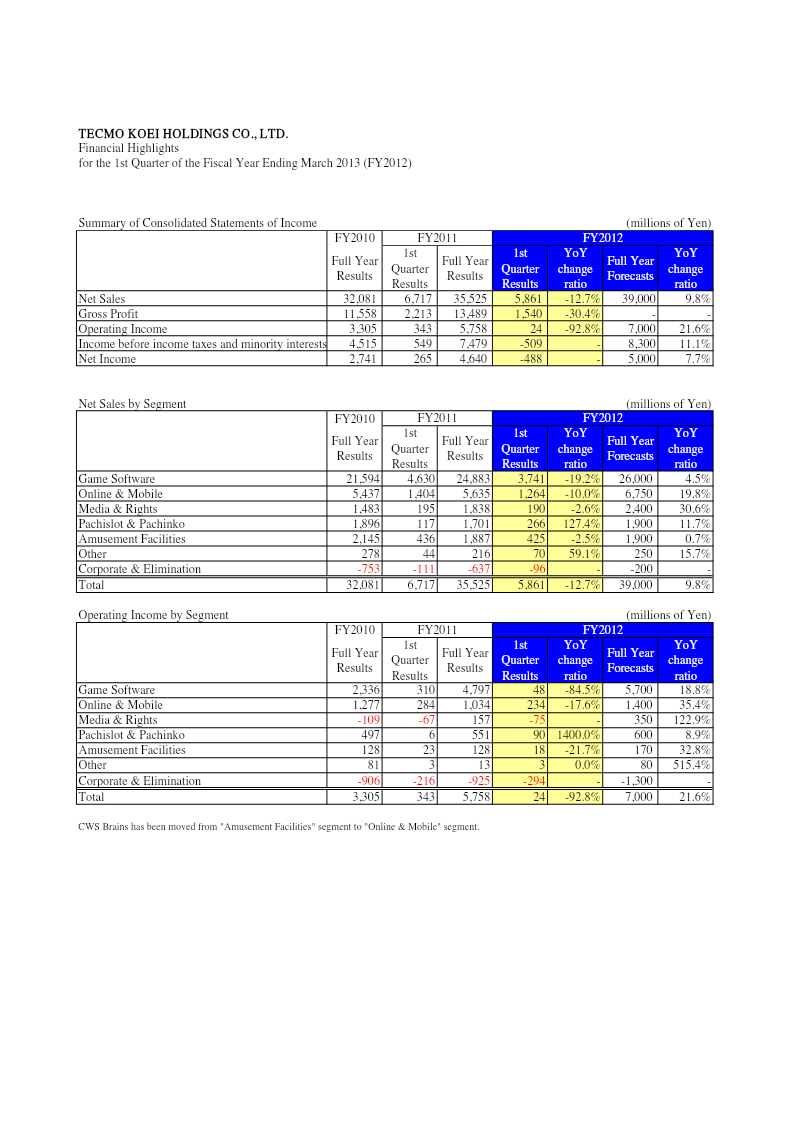

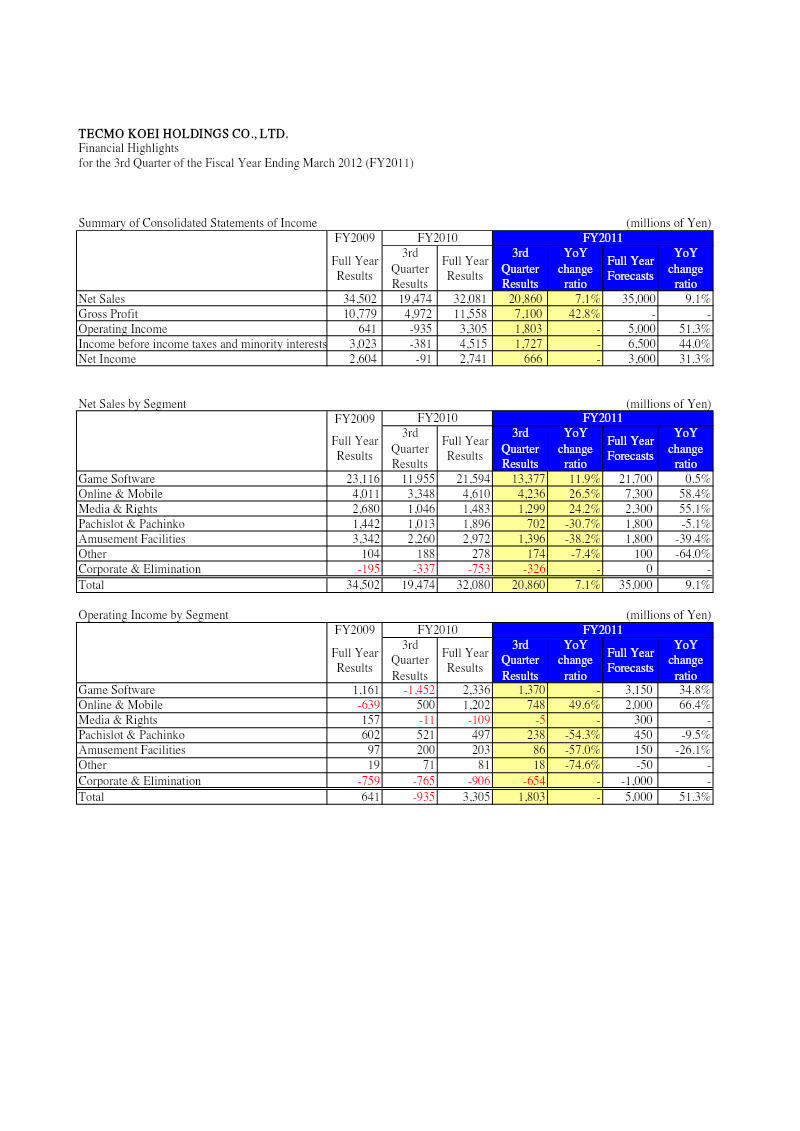

Financial Highlights: Fiscal Year Ending March 2017

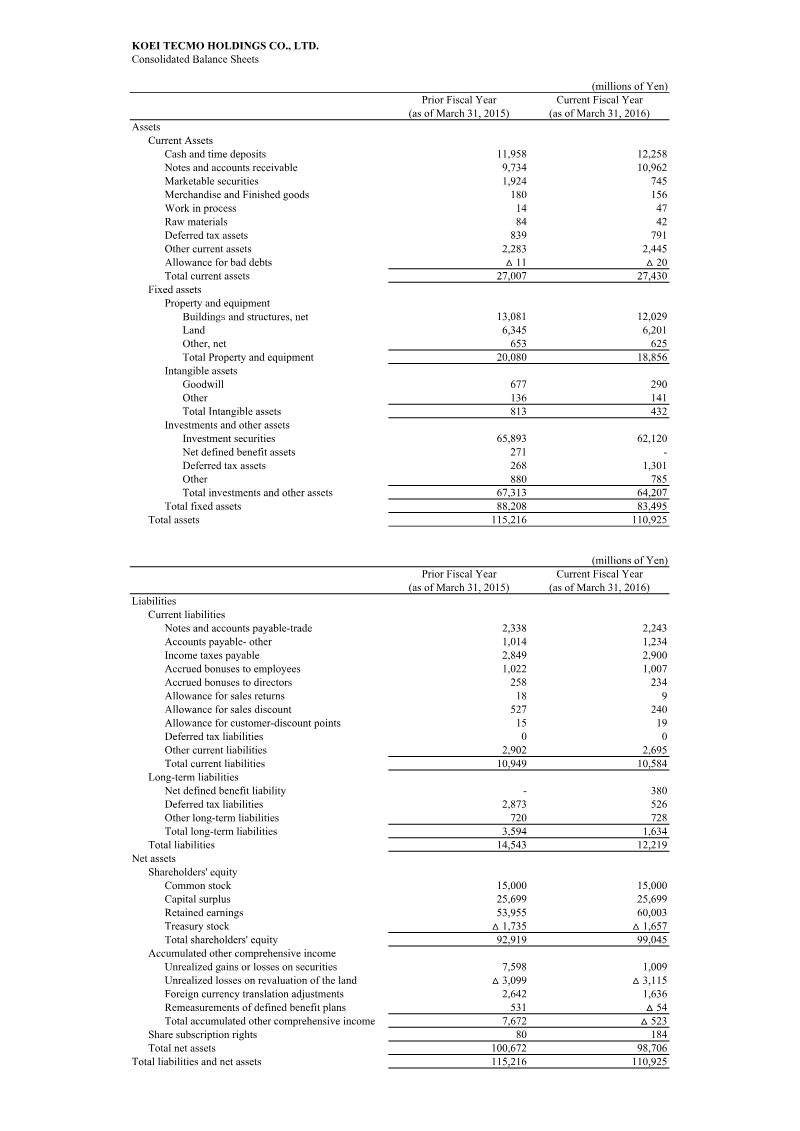

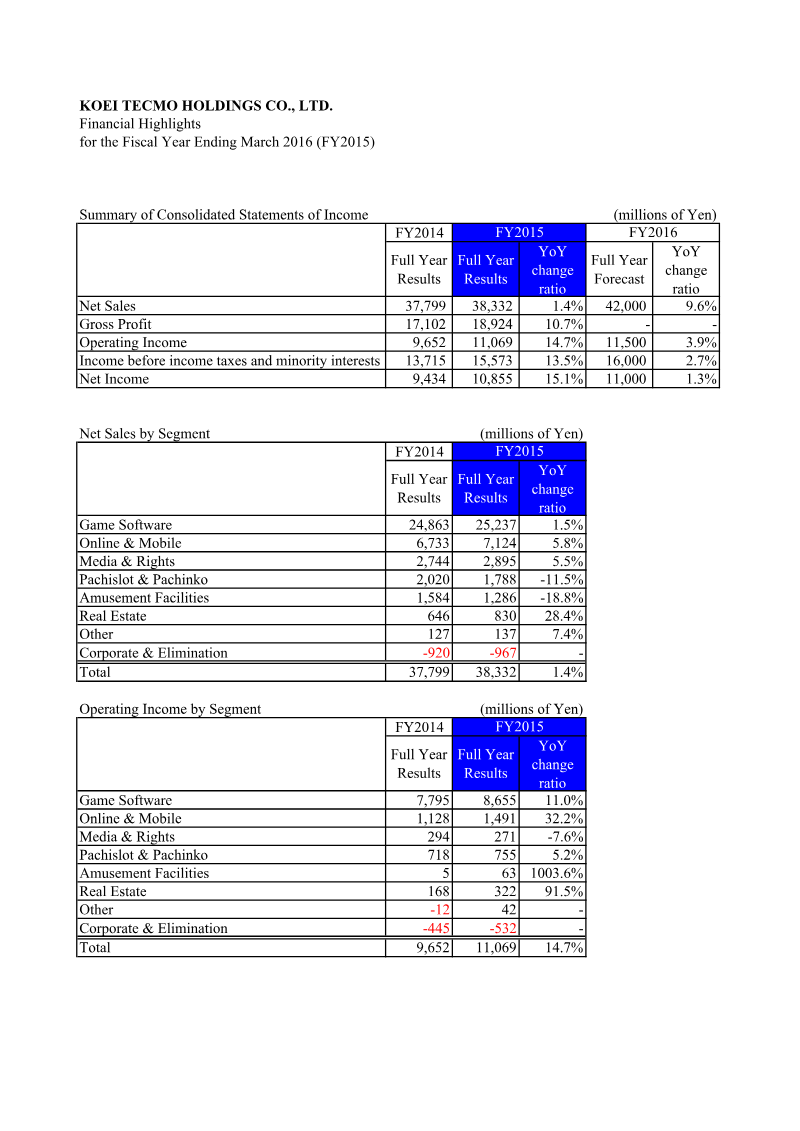

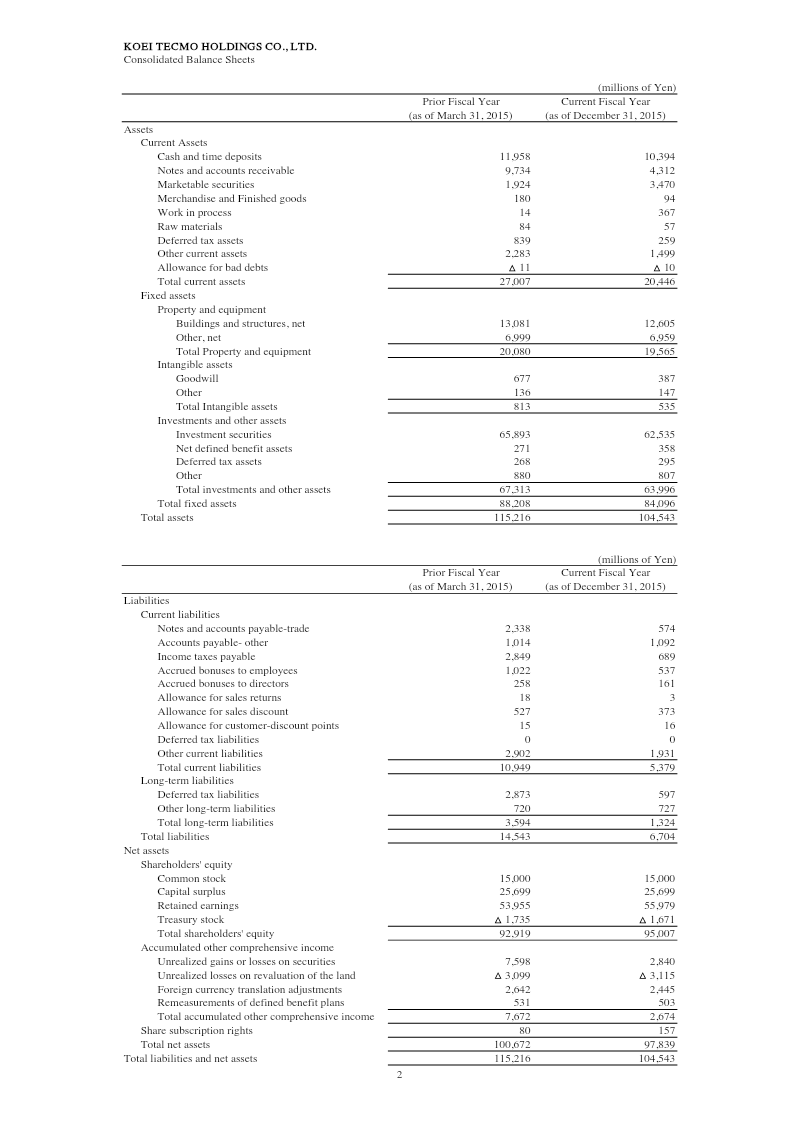

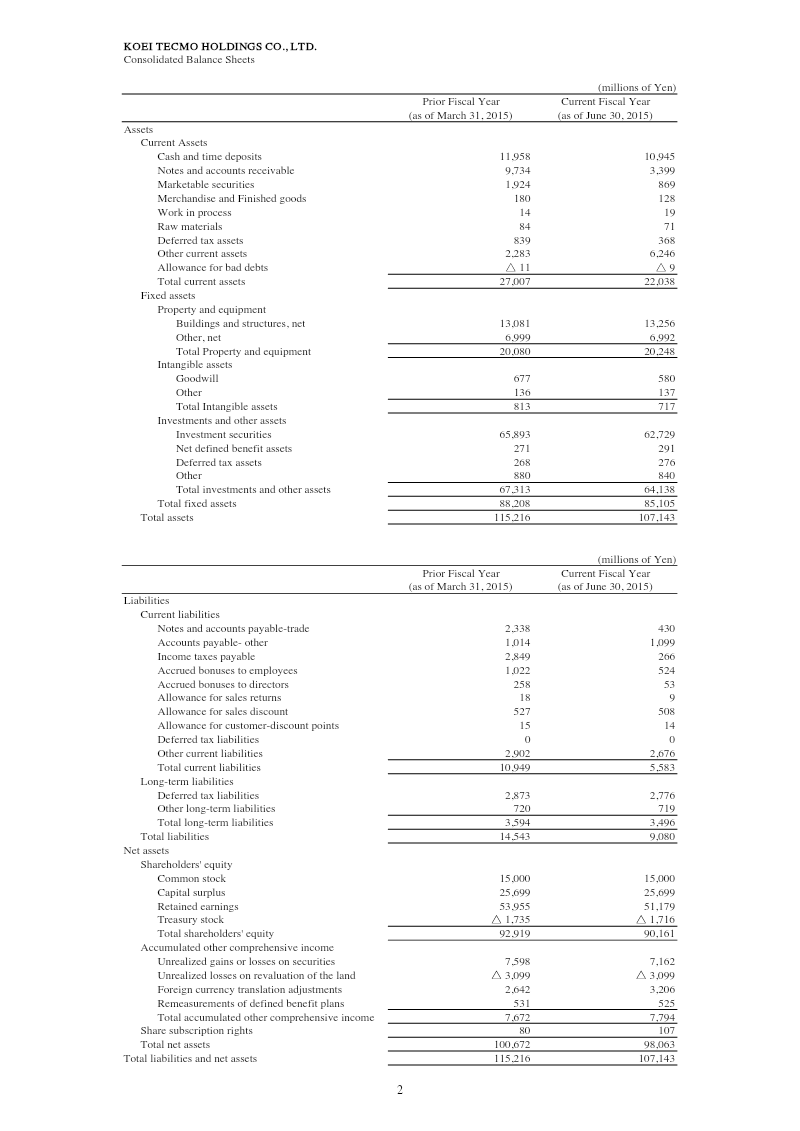

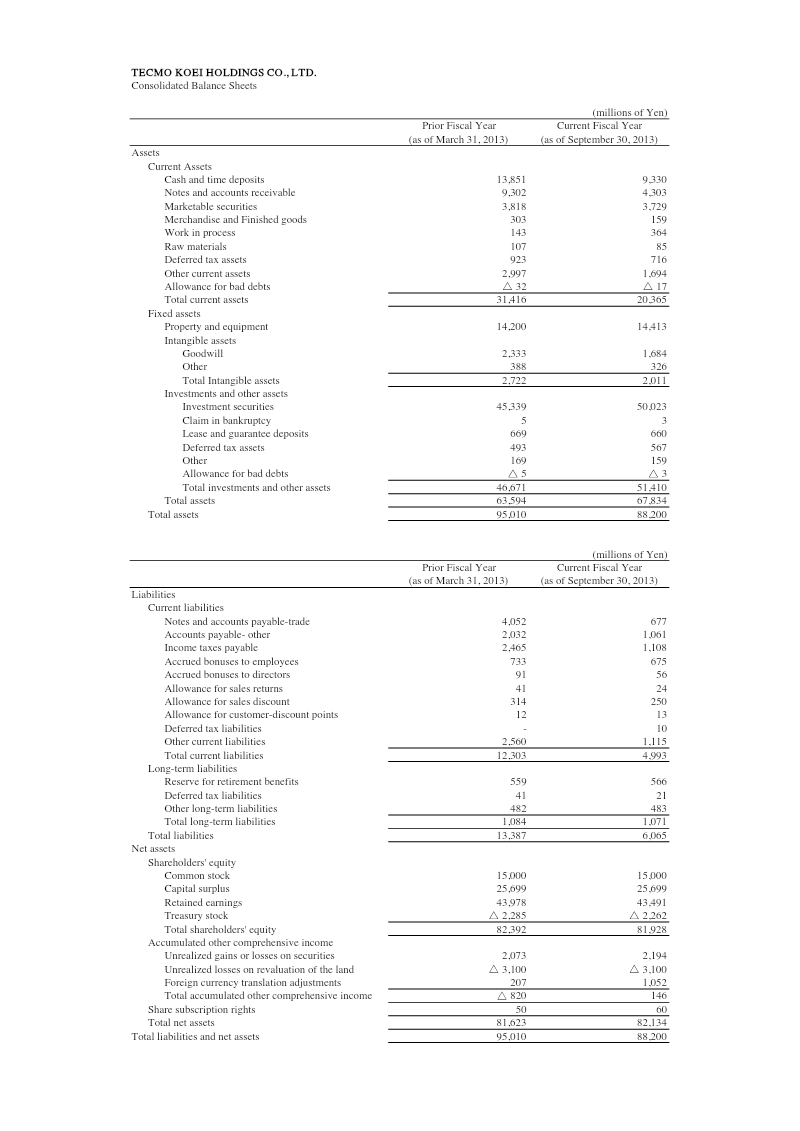

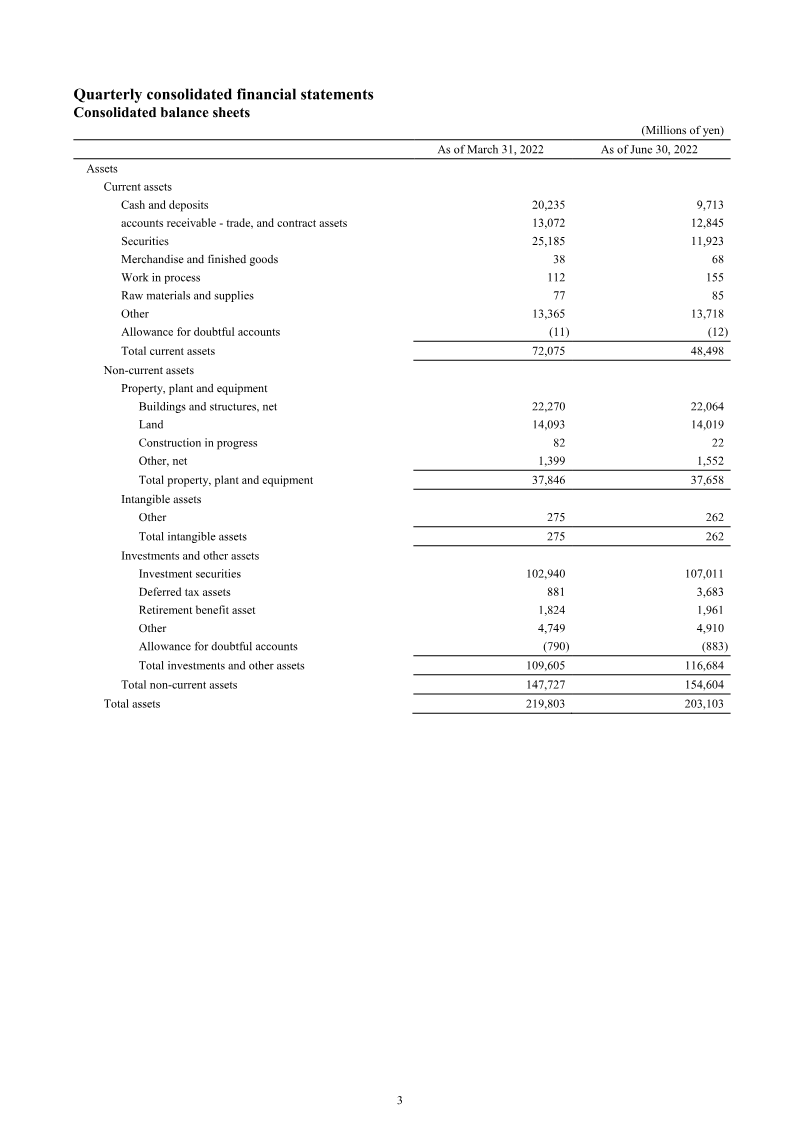

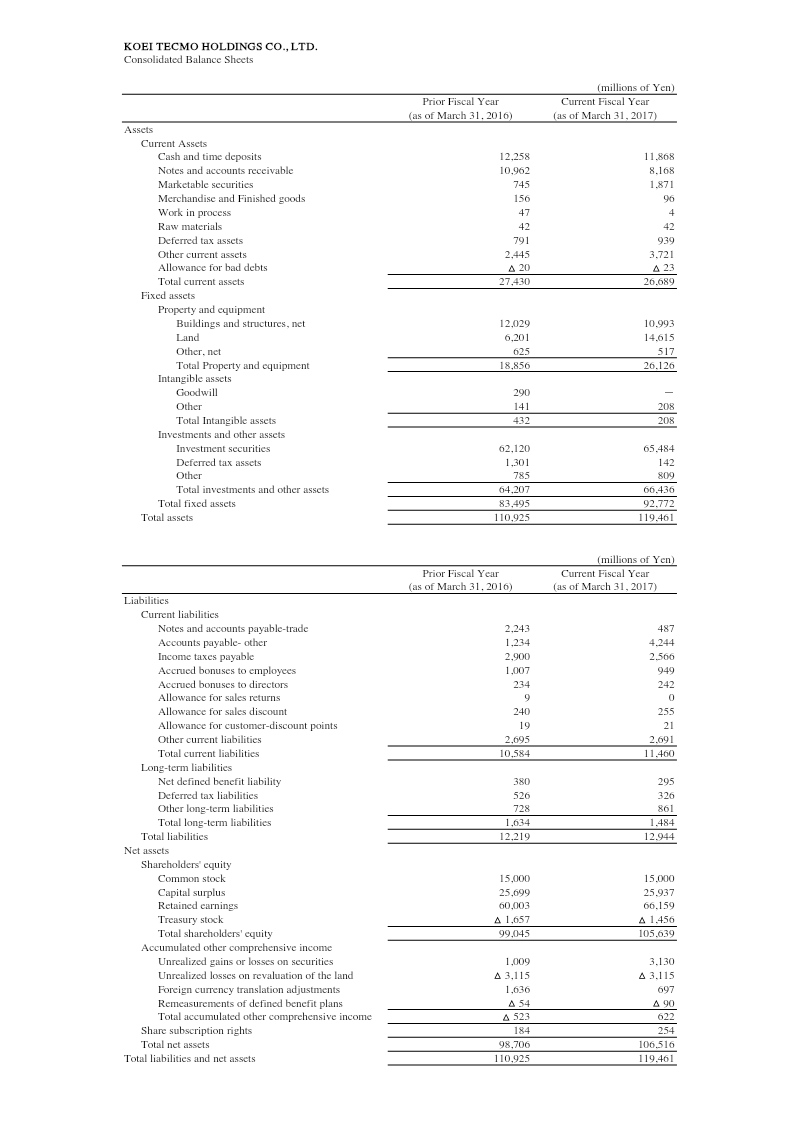

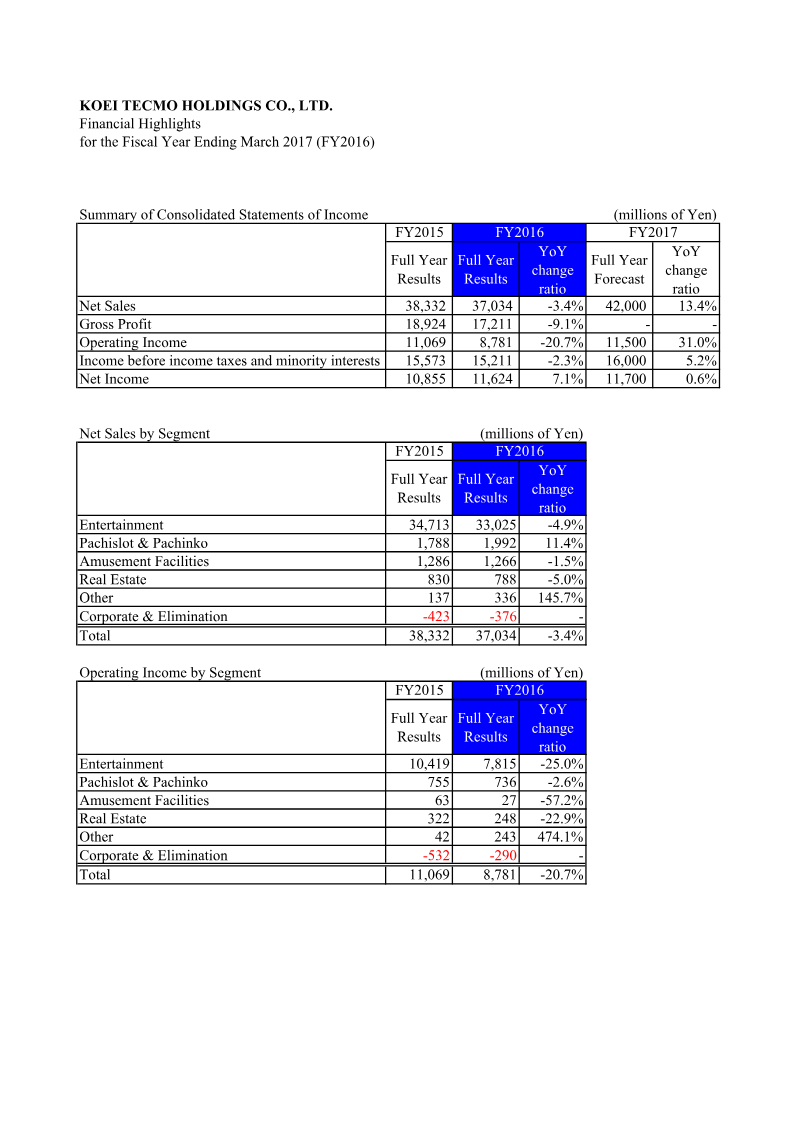

Koei Tecmo Holdings reported a modest improvement in fiscal performance for the year ending March 2017 compared with the prior year. Net sales fell 3.4 % to ¥37,034 million, largely due to a 4.9 % decline in the entertainment segment and a 1.5 % drop in amusement facilities, while pachislot & pachinko sales rose 11.4 %. The “Other” segment, which includes real estate and ancillary activities, grew 145.7 %, offsetting declines in core gaming operations. Operating income contracted 20.7 % to ¥8,781 million, driven by a 25 % reduction in entertainment operating profit and a 57.2 % decline in amusement facilities; the “Other” segment’s operating profit surged 474.1 %. Net income increased 7.1 % to ¥11,624 million, reflecting a 0.6 % rise in the forecasted year and a modest improvement over the previous fiscal period. Balance‑sheet analysis shows total assets rising 7.9 % to ¥119,461 million, mainly due to higher investment securities and land values. Current assets decreased slightly as cash and receivables fell, while fixed assets grew from ¥83,495 million to ¥92,772 million, largely driven by land acquisitions. Total liabilities increased 5.8 % to ¥12,944 million, with current liabilities rising and long‑term liabilities falling. Shareholders’ equity expanded to ¥105,639 million, supported by retained earnings growth and a reduction in treasury stock. The financial highlights cover Japan‑based operations for FY2016, presenting consolidated income statements and balance sheets in millions of yen. Data are derived from audited financial statements, with segment performance broken down by entertainment, pachislot & pachinko, amusement facilities, real estate, and other activities. The report underscores a shift toward diversified revenue streams amid declining core gaming sales.

Koei Tecmo

Report

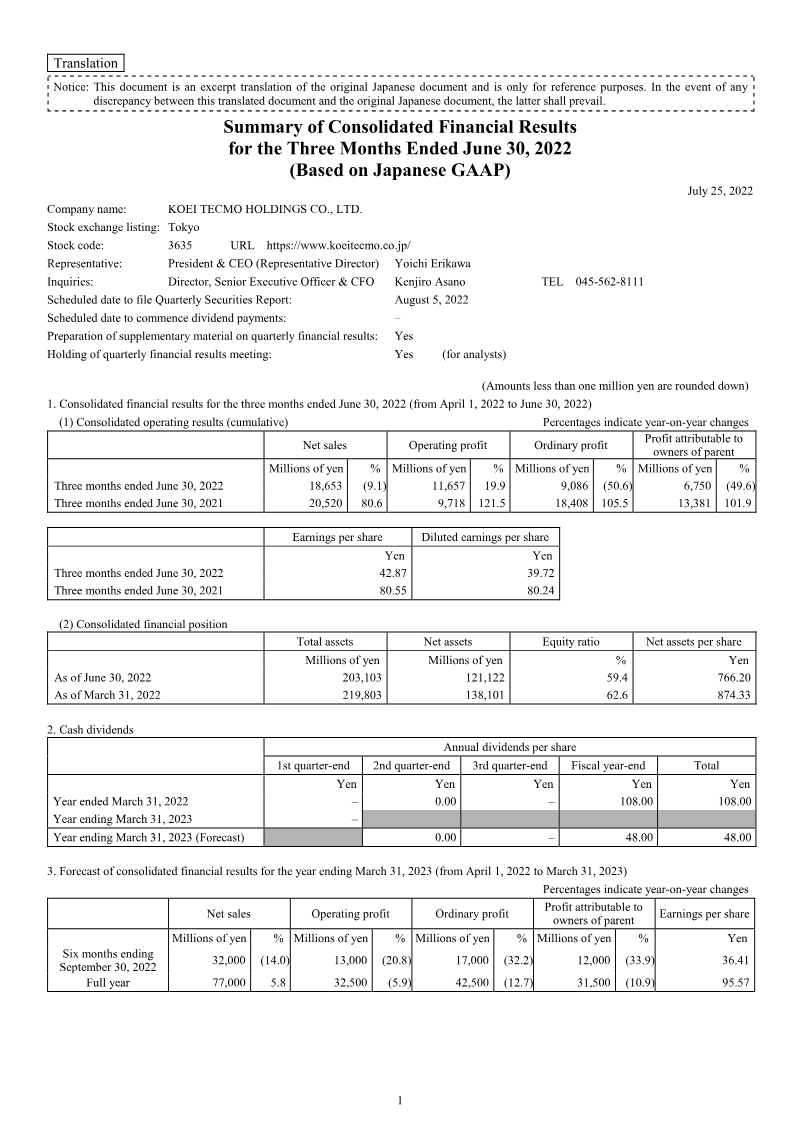

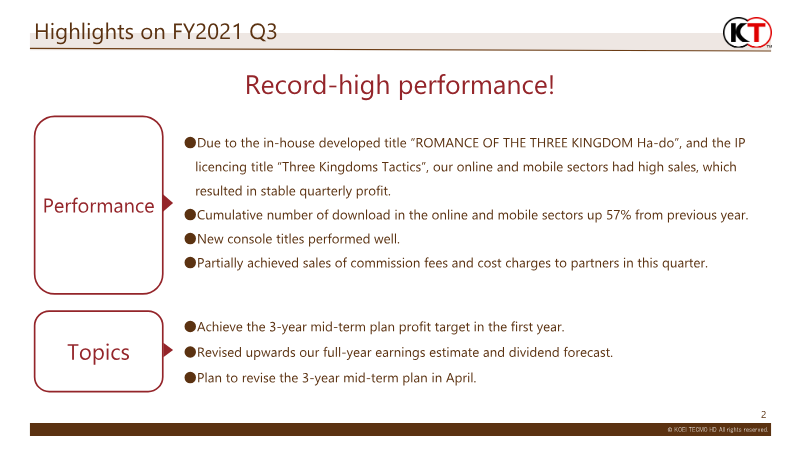

Financial Results for the Third Quarter of the Fiscal Year Ending March 2022

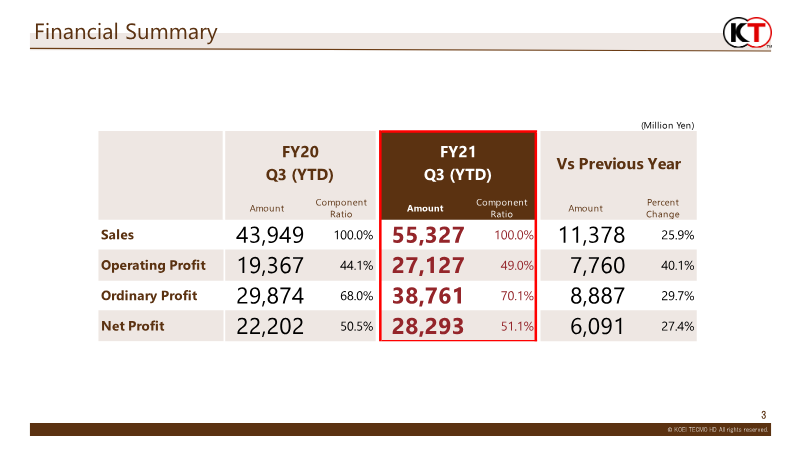

The quarterly report for the third quarter of fiscal 2022 highlights a record‑high performance driven primarily by strong sales in the online and mobile sectors, supported by the in‑house title “Romance of the Three Kingdoms Ha‑do” and the IP‑licensing title “Three Kingdoms Tactics.” Cumulative downloads in these sectors rose 57 % year‑over‑year, contributing to a 25.9 % increase in total sales from ¥43.95 billion to ¥55.33 billion, and a 40.1 % rise in operating profit to ¥27.13 billion. The entertainment segment alone grew 26.3 % in sales, with overseas markets accounting for over half of the increase. Console performance remained solid, with new releases such as “Blue Reflection: Second Light” and “Dynasty Warriors 9 Empires” achieving strong launch sales, while the overall console unit sales declined by 30.1 % compared to the prior year due to a shift toward digital and mobile offerings. Digital download sales surged 35.2 %, and mobile smartphone/social game revenue grew 67.9 % to ¥25.74 billion, reflecting a strategic pivot toward digital distribution. Operating costs rose 13.4 % in cost of goods sold and 11.9 % in selling‑general‑administrative expenses, partially offset by a 63.3 % increase in advertising spend that supported the rapid download growth. Headcount increased by 3.6 % to 2,075 employees. The company revised its full‑year earnings estimate upward, projecting operating profit of ¥31.5 billion versus the prior plan of ¥24.5 billion, and raised its dividend forecast from 81 to 98 yen per share. The mid‑term three‑year plan is slated for revision in April, with the first year already achieving its profit target.

Koei Tecmo