ReportKoei Tecmo

Financial Highlights: 3rd Quarter of the Fiscal Year Ending March 2016

2 pages~4 min full read

Key insights

7 takeaways · ~3 min read- 01

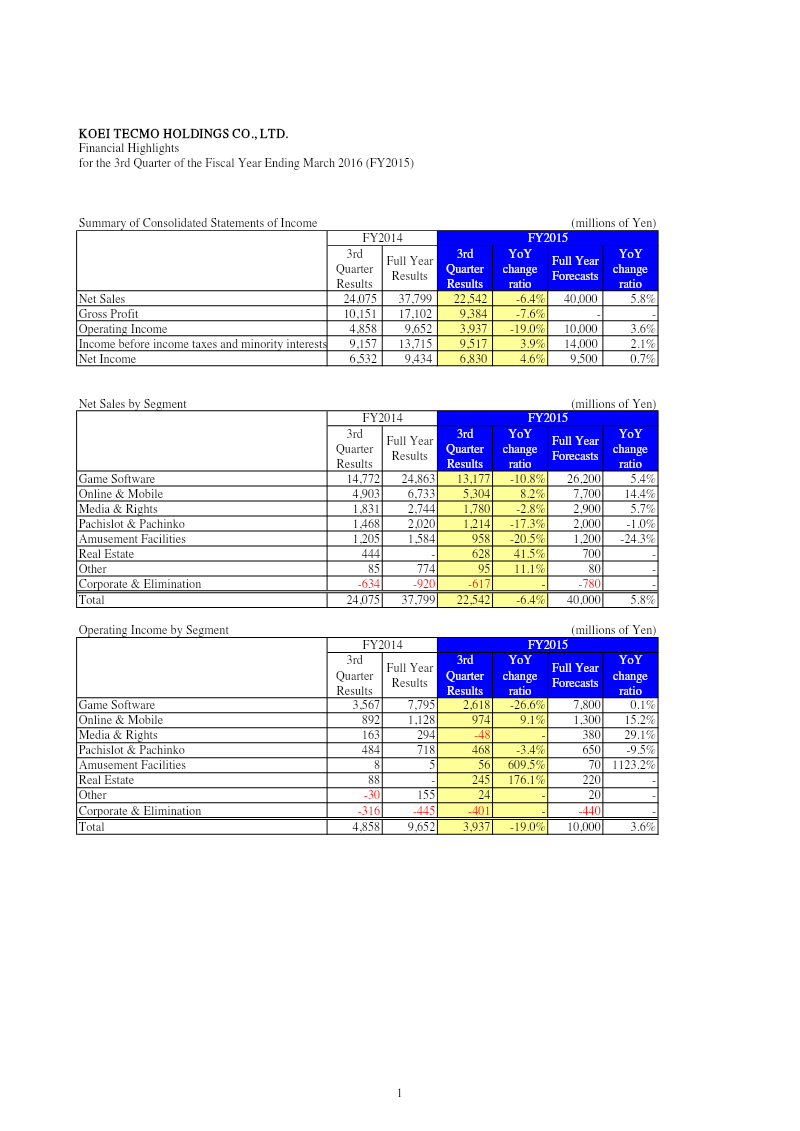

Koei Tecmo reported net sales of ¥37.8 billion for Q3 FY2015, a 6.4% year-over-year increase that exceeded the company's ¥40 billion forecast by 5.8%.

See it on page 1 - 02

Operating income rose 19% year-over-year to ¥9.65 billion, though this result fell 3.6% short of the ¥10 billion target.

See it on page 1 - 03

Net income reached ¥9.43 billion, representing a 4.6% year-over-year increase but missing the ¥9.5 billion forecast.

See it on page 1 - 04

The Game Software segment, the company's primary revenue driver, generated ¥24.86 billion in sales, marking a 10.8% decline from the previous year.

See it on page 1 - 05

Online & Mobile sales grew by 8.2% to ¥6.73 billion, outperforming the segment's forecast by 14.4%.

See it on page 1 - 06

Total assets decreased to ¥104.5 billion from ¥115.2 billion a year prior, while current liabilities were halved to ¥5.38 billion, reflecting a significant tightening of the balance sheet.

See it on page 2 - 07

Real Estate sales saw the highest growth rate among all segments, rising 41.5% year-over-year to ¥628 million.

See it on page 1