Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

223 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Japan

Market Analysis

Investment

Mobile

Global

Game Publishing

Advertising

Monetization

Game Development

Console

Asia

Marketing

RPG

Player Behavior

Market Forecast

Mergers & Acquisitions

USA

South Korea

Clear

Filters

1

Japan

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

2 pages

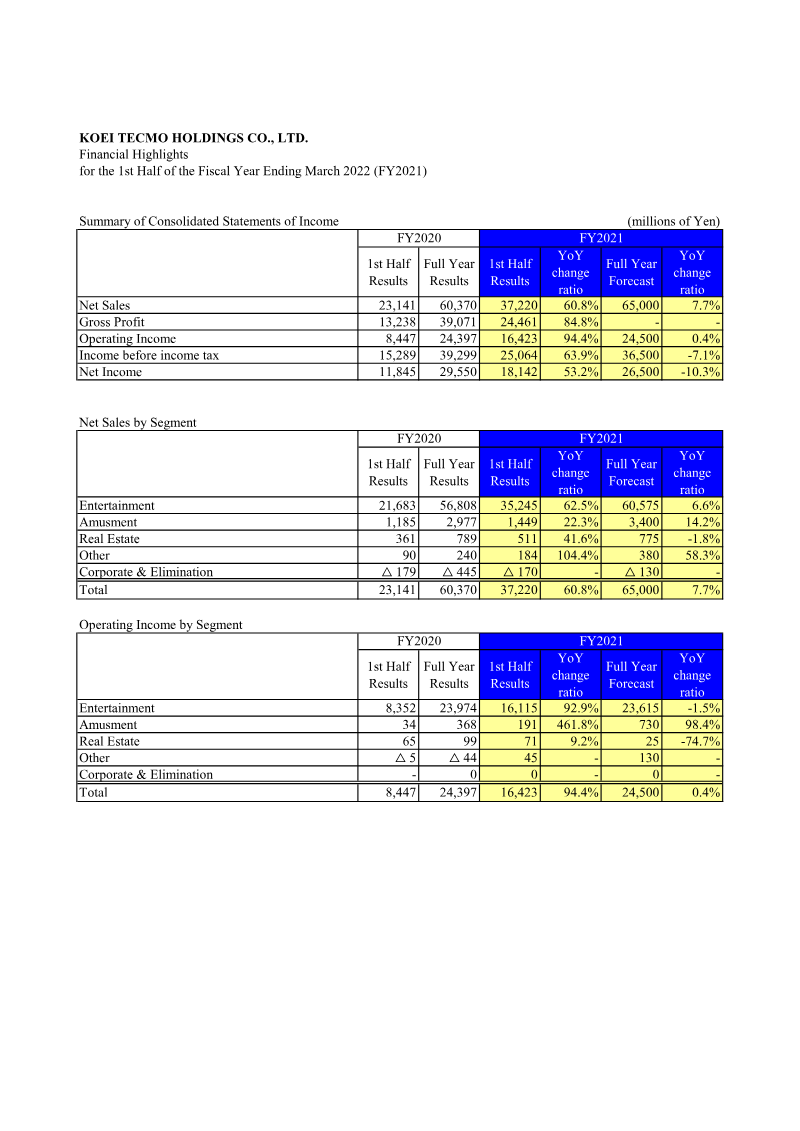

Financial Highlights: 1st Half of the Fiscal Year Ending March 2022

KOEI TECMO Holdings achieved a 60.8% year-over-year increase in net sales to ¥23,141 million for the first half of the fiscal year ending March 2022.

Operating income nearly doubled, rising 94.4% to ¥8,447 million, while net income grew 53.2% to ¥11,845 million due to improved profitability and cost management.

The Entertainment segment served as the primary growth engine, contributing 62.5% of the total sales increase and 92.9% of the gain in operating income.

Market Analysis

Investment

Japan

Koei Tecmo

Report

2 pages

Koei Tecmo Holdings Financial Summary: FY2024 3Q

Koei Tecmo reported a net loss of ¥171 million for FY2024 Q3, a significant reversal from the ¥6,898 million profit recorded in the previous quarter.

Consolidated sales fell 25.4% year-over-year to ¥14,677 million, while operating profit contracted to ¥4,673 million from ¥6,664 million in Q2.

Ordinary profit turned negative at ¥(787) million, primarily driven by a substantial non-operating loss of ¥5,461 million.

Market Analysis

Investment

Japan

+1

Koei Tecmo

Report

4 pages

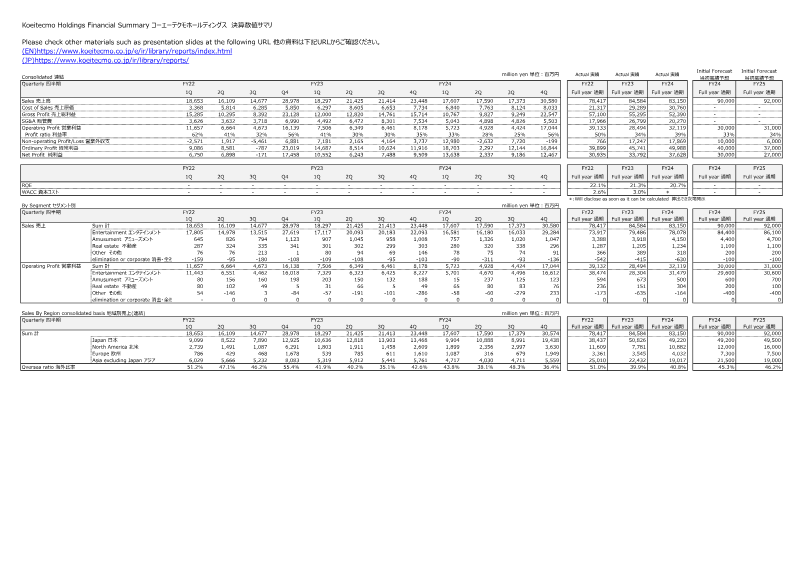

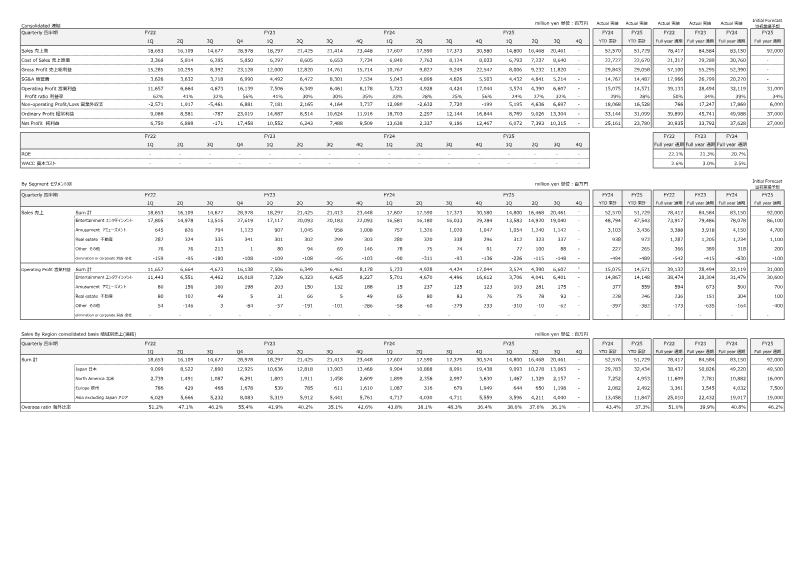

FY2024 Annual Data Appendix

Koei Tecmo's Entertainment division remains the primary revenue driver, contributing ¥73,917 million in FY24 and accounting for 94% of total company sales.

Gross profit margins experienced a significant contraction, falling from 62% in FY22 Q1 to 25% in FY24 Q4 due to rising costs of sales and SG&A expenses.

Overseas markets are increasingly critical to the company's performance, with international revenue reaching 55.4% of total sales in FY24 Q4.

Market Analysis

Investment

Japan

+1

Koei Tecmo

Report

6 pages

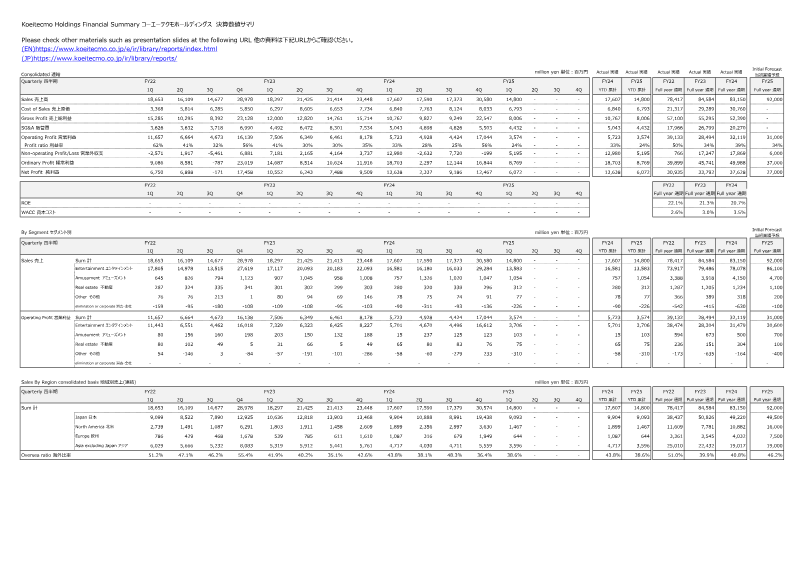

FY2025 1st Quarter Data Appendix: Koei Tecmo

Koei Tecmo reported Q1 2025 sales of ¥21.4 billion, a significant increase from ¥18.7 billion in Q1 2024, driven by 20% growth in the Entertainment segment and 30% growth in the Amusement division.

Operating profit reached ¥11.7 billion, supported by an improved gross margin of 82%, up from 78% in the previous year.

Overseas markets now account for 51% of total revenue, surpassing domestic Japan revenue (49%) for the first time compared to 46% in the prior year.

Market Analysis

Investment

Japan

+1

Koei Tecmo

Report

6 pages

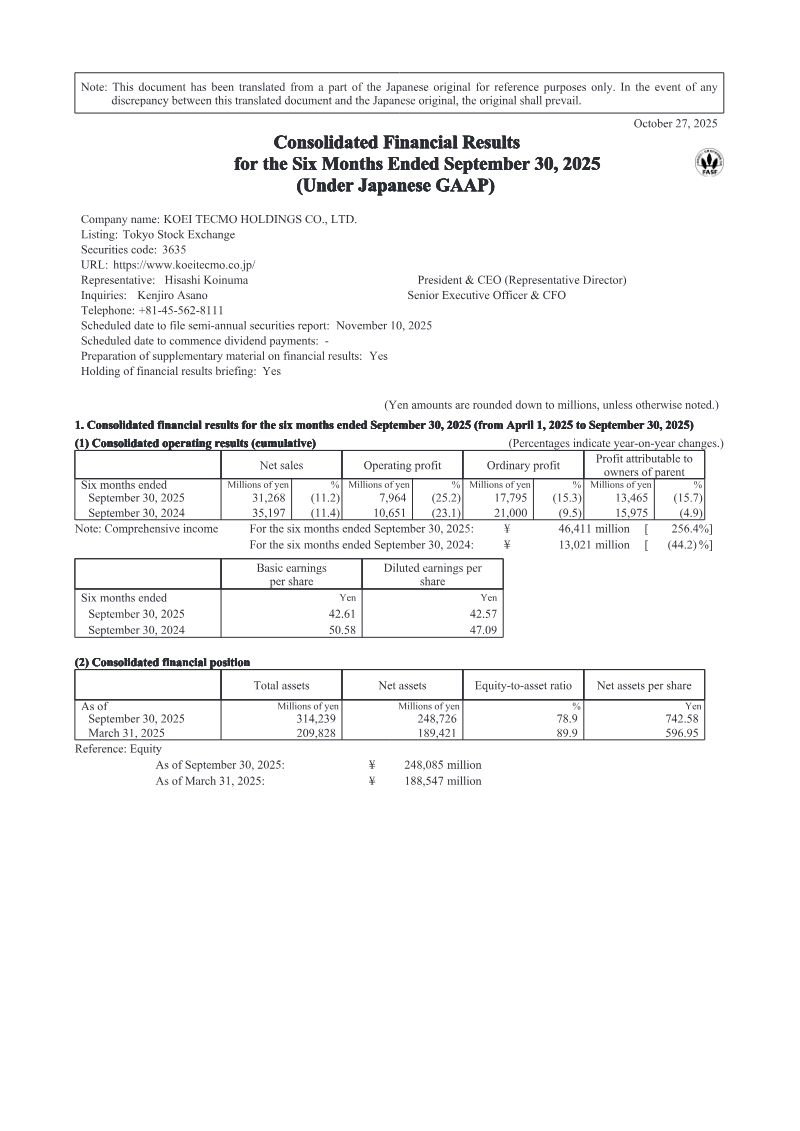

Financial Highlights: 2nd Quarter FY2025

Koei Tecmo Holdings experienced a decline in core operating performance for the first half of FY2025, with net sales falling 11.2% YoY to ¥31,268 million and operating profit dropping 25.2% to ¥7,964 million.

Comprehensive income surged 256.4% to ¥46,411 million, primarily driven by significant gains from investment securities and derivatives compared to a loss in the same period last year.

Profitability margins tightened during the six-month period ending September 30, with the operating margin decreasing from 30.6% to 25.4% and net income attributable to the parent falling 15.7% to ¥13,465 million.

Market Analysis

Investment

Japan

+1

Koei Tecmo

Report

6 pages

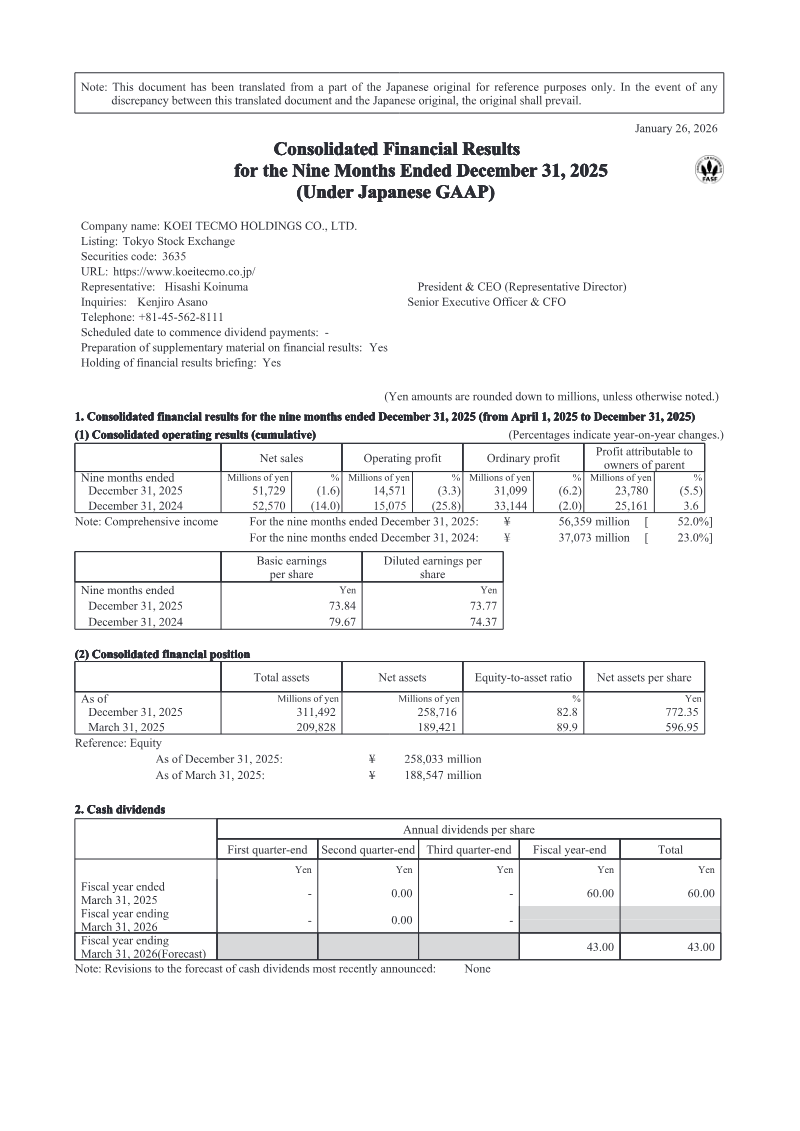

FY2025 Third Quarter Financial Highlights: Japan

Koei Tecmo Holdings reported a 1.6% decline in net sales to ¥51,729 million and a 3.3% drop in operating profit to ¥14,571 million for the nine months ended December 31, 2025.

Comprehensive income surged 52.0% year-on-year to ¥56,359 million, primarily fueled by non-operating gains from interest income and foreign exchange fluctuations.

Total assets grew significantly to ¥311,492 million by December 31, 2025, up from ¥209,828 million at the start of the fiscal year, driven by increases in investment securities and property, plant, and equipment.

Market Analysis

Investment

Japan

+2

Koei Tecmo

Report

8 pages

Consolidated Financial Data: FY2025 3rd Quarter

Operating profit declined 15.5% YoY to ¥17,044 million in Q3 FY25, primarily due to rising SG&A and cost of sales within the entertainment segment.

Total sales grew 5.4% YoY to ¥30,580 million, though this figure remains below the ¥28,978 million recorded in Q3 FY22.

Overseas revenue grew to 51.0% of total sales in FY25, up from 46.2% in FY24, signaling a successful strategic shift toward international market penetration.

Market Analysis

Investment

Japan

+1

Koei Tecmo

Report

2 pages

Summary of Main Q&A: FY2018 Second Quarter GREE Results Briefing

GREE is expanding beyond its mobile-centric foundation by entering the console market, starting with the release of 'Fishing Star' on the Nintendo Switch.

The 'Fishing Star' console title will utilize a single-purchase download model without in-game microtransactions, marking a departure from the company's typical mobile monetization.

GREE is building a multiplatform, multiregional development system designed to support simultaneous mobile and console releases for both domestic and international markets.

Market Analysis

Game Publishing

Monetization

+2

GREE

Report

2 pages

Summary of Q&A: FY2016 4Q GREE Results Briefing

GREE plans to launch eight native games in FY2017, targeting a release cadence of two titles per quarter.

Operating margins for Q1 FY2017 are expected to remain below 20% due to upfront investments in game operations and North American expansion, with a return to higher margins contingent on new title performance.

The company defines 'hit titles' as games that achieve top-ten rankings within the App Store games category.

Market Analysis

Investment

Advertising

+1

GREE

Report

2 pages

Summary of Main Questions and Answers: FY2017 1Q GREE Results Briefing

GREE is prioritizing the RPG genre to drive FY2017 growth, citing its market dominance in Japan, resilience to trends, and internal development efficiencies.

The company expects a ¥1.0 billion decline in operating income for Q2 due to strategic investments in advertising, rental costs, and goodwill amortization.

Key RPG titles in the development pipeline include Senki Zesshou SYMPHOGEAR XD Unlimited, Rara-MAGI, Another Eden, and A Farewell to Arms.

Market Analysis

Monetization

Mobile

+2

GREE

Report

3 pages

Summary of Questions and Answers: FY2017 2Q GREE Results Briefing

GREE expects Q3 operating income to decline due to increased fixed costs associated with a pipeline of seven new game releases scheduled for the second half of the fiscal year.

The company is shifting operations for select titles to Vietnam and improving marketing efficiency to stabilize coin-consumption revenue within its game segment.

New business ventures in virtual reality and video advertising are targeted to reach profitability by FY2019.

Market Analysis

Game Development

Monetization

+3

GREE

Report

2 pages

Summary of Main Questions and Answers at the FY2017 3Q GREE Results Briefing

GREE is prioritizing development efficiency by reusing game engines to shorten production timelines and reduce overall costs.

The company is shifting toward high-fidelity mobile gaming, aiming to replicate console-quality experiences on smartphones to drive long-term user loyalty.

GREE has increased its content readiness, with new titles now launching with two to three months of pre-prepared content.

Market Analysis

Game Development

Game Engines

+2

GREE

Report

3 pages

Summary of Main Questions and Answers at the FY2018 First Quarter GREE Results Briefing

GREE’s Q1 FY2018 revenue growth was driven by increased commission fees from partner titles that leverage strong intellectual property.

Key titles driving robust coin consumption in Q1 included 'Another Eden: The Cat Who Goes Beyond Time', 'SINoALICE', 'Senki Zesshou SYMPHOGEAR XD Unlimited', and 'Is It Wrong to Try to Pick Up Girls in a Dungeon: Memoria Freeze'.

The company expects a temporary decline in native game sales as it transitions to larger support teams, enhanced content, and more aggressive promotional activities to drive future growth.

Market Analysis

Monetization

Marketing

+3

GREE

Report

5 pages

FY2018 2Q Result Presentation

GREE reported FY2018 Q2 net sales of ¥19.5 billion and operating income of ¥2.3 billion, both exceeding internal targets.

The company is pivoting toward console gaming, with 'The Fishing Star' confirmed for Nintendo Switch and a global release currently in development.

While year-on-year growth was positive, quarterly sales moderated by approximately 10 percentage points due to reduced advertising spend and lower commission fees.

Market Analysis

Game Publishing

Mobile

+2

GREE

Report

4 pages

Summary of Main Questions and Answers at the FY2018 Third Quarter GREE Results Briefing: Japan

GREE is investing ¥10 billion into the VTuber market, with ¥4 billion allocated to creator support and ¥6 billion dedicated to advertising.

The company is leveraging its 3D rendering expertise to create synergies between VTuber content and VR technology to improve character interaction.

GREE’s international strategy focuses on a simultaneous or near-simultaneous global release schedule for Japanese IPs, exemplified by the North American launch of 'Is It Wrong to Try to Pick Up Girls in a Dungeon: Memoria Freese'.

Market Analysis

Investment

Game Development

+2

GREE

Report

1 pages

Summary of Main Questions and Answers at the FY2018 Fourth Quarter GREE Results Briefing

GREE’s FY2019 strategy focuses on international expansion of existing game titles and the launch of new development projects to capture emerging markets.

The company recorded a goodwill impairment in its advertising and media segment due to the underperformance of the 3 Minutes unit.

Despite the impairment, GREE maintains that its advertising and media business remains a significant revenue contributor and will continue to receive investment for further expansion.

Market Analysis

Game Publishing

Mobile

+2

GREE

Report

2 pages

Summary of main questions and answers at the FY2019 First Quarter GREE results briefing held on October 26, 2018

GREE is prioritizing international expansion by self-distributing existing titles in high-profitability markets, with China identified as a key target for upcoming operations and marketing.

The company plans to drive an earnings uptrend in the second half of FY2019 through new title releases and expanded multiplatform distribution in Japan.

GREE is diversifying its distribution channels by targeting social media gaming, specifically highlighting Facebook Messenger as a high-potential platform for new releases.

Market Analysis

Market Forecast

Game Publishing

+5

GREE

Report

1 pages

Summary of Main Questions and Answers at the FY2019 Third Quarter GREE Results Briefing

GREE projects a significant increase in net sales for the fourth quarter of fiscal 2019, with operating income expected to remain robust when excluding one-time events.

Third-quarter operating income exceeded forecasts, driven primarily by strong overseas sales performance of the title 'Another Eden'.

Profitability in the game business was bolstered by fixed-cost efficiencies that surpassed internal expectations during the third quarter.

Market Analysis

Market Forecast

Investment

+4

GREE

Report

2 pages

Summary of main supplementary explanations questions and answers at the FY2020 First Quarter GREE results briefing held on October 30, 2019

GREE projects an operating income of approximately ¥0.5 billion for the second quarter of FY2020.

First-quarter sales declined due to the conclusion of major title anniversary events and the strategic transfer of titles to improve overall profitability.

Management expects browser game revenue to continue its decline while increasing advertising spend on high-potential mobile titles.

Market Analysis

Monetization

Marketing

+3

GREE

Report

1 pages

Summary of main supplementary explanations questions and answers at the FY 2020 Second Quarter GREE results briefing held on February 3, 2020

GREE projects Q3 FY2020 operating income to range between ¥0.5 billion and just under ¥1.0 billion.

Q2 FY2020 net and ordinary income growth was driven by gains from venture capital investments and listed company holdings.

The game 'Another Eden' doubled its overseas user base following an IP collaboration with Persona 5 and optimized digital advertising.

Market Analysis

Investment

Japan

+1

GREE

Previous

1

…

5

6

7

…

12

Next