Related Documents

Report

Match3 Genre Snapshot: US iOS (May 2021)

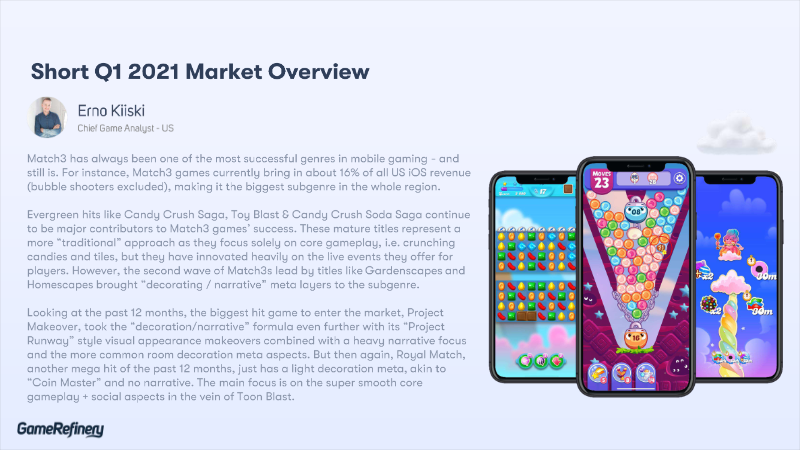

The Match3 subgenre represents the largest individual segment of the US iOS mobile gaming market, accounting for approximately 16% of total market revenue as of May 2021. While the category has long been dominated by established titles that have maintained chart positions for years, recent market shifts indicate a move away from traditional swapping mechanics. Notably, none of the new Match3 titles entering the top 500 grossing rankings over the last 18 months utilize standard swapping gameplay, signaling a diversification in core mechanics and the rising importance of meta-layers. Meta-elements, particularly those focused on decoration and customization, have become essential components for modern success in the genre. Successful megahits like Royal Match and Project Makeover demonstrate the effectiveness of combining core puzzle gameplay with deep progression systems and sophisticated monetization strategies. Data indicates that recurring live events, special event rewards, and limited-time in-app purchase offers have the highest impact on revenue. Furthermore, social features such as guild mechanics and "send/ask help" systems are increasingly vital for driving engagement and retention. Player motivation analysis, based on a survey of over 7,000 mobile gamers across English-speaking Western markets, reveals distinct psychological drivers within the genre. While "Thinking and Solving" remains the primary driver for traditional titles like Candy Crush Saga, newer successful entries increasingly lean into "Customization and Decoration" and "Role-playing and Emotions." This shift reflects a broader industry trend where loss aversion mechanics and social competition are leveraged to enhance the player experience and maximize lifetime value in a highly competitive landscape.

GameRefineryMay 2021

Report

Strategy Genre Snapshot 2021

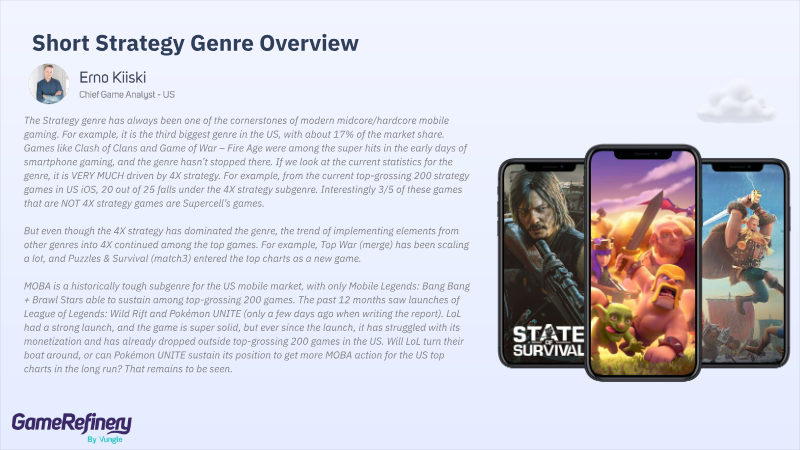

The strategy genre remains a cornerstone of the mobile gaming market, currently ranking as the third-largest genre in the United States on iOS with a 17% revenue market share. The landscape is heavily dominated by the 4X strategy subgenre, which accounts for 20 of the top 25 grossing strategy titles. While the market is crowded with aging titles, recent growth is driven by genre-blending, where developers integrate mechanics from other categories—such as merge, match-3, or RPG elements—to broaden player appeal. Market analysis reveals that 4X strategy games rely on three primary pillars: long-term power progression through permanent boosts and deep economies, complex live operations featuring recurring events, and robust social frameworks centered on competition and collaboration. High-performing examples include State of Survival, which reached the top of the 4X subgenre through massive IP collaborations, and Top War, which successfully scaled using merge mechanics. Conversely, the MOBA subgenre continues to face challenges in the U.S. market; despite a strong launch, League of Legends: Wild Rift struggled to maintain its top-grossing position, leaving the subgenre's future performance to newer entries like Pokémon UNITE. Player motivation data, derived from a survey of over 7,000 respondents across English-speaking Western territories, indicates that strategy players are primarily driven by strategic planning, resource optimization, and social competition. Successful titles capitalize on these drivers by offering deep technology trees, competitive guild mechanics, and diverse PvP modes. While Supercell remains the only major player finding significant success outside the 4X subgenre with titles like Clash of Clans, the broader trend suggests that sustained revenue in this space requires a sophisticated mix of deep monetization loops and constant feature innovation.

GameRefineryOct 2021

Report

2023 Casual Gaming Apps Report

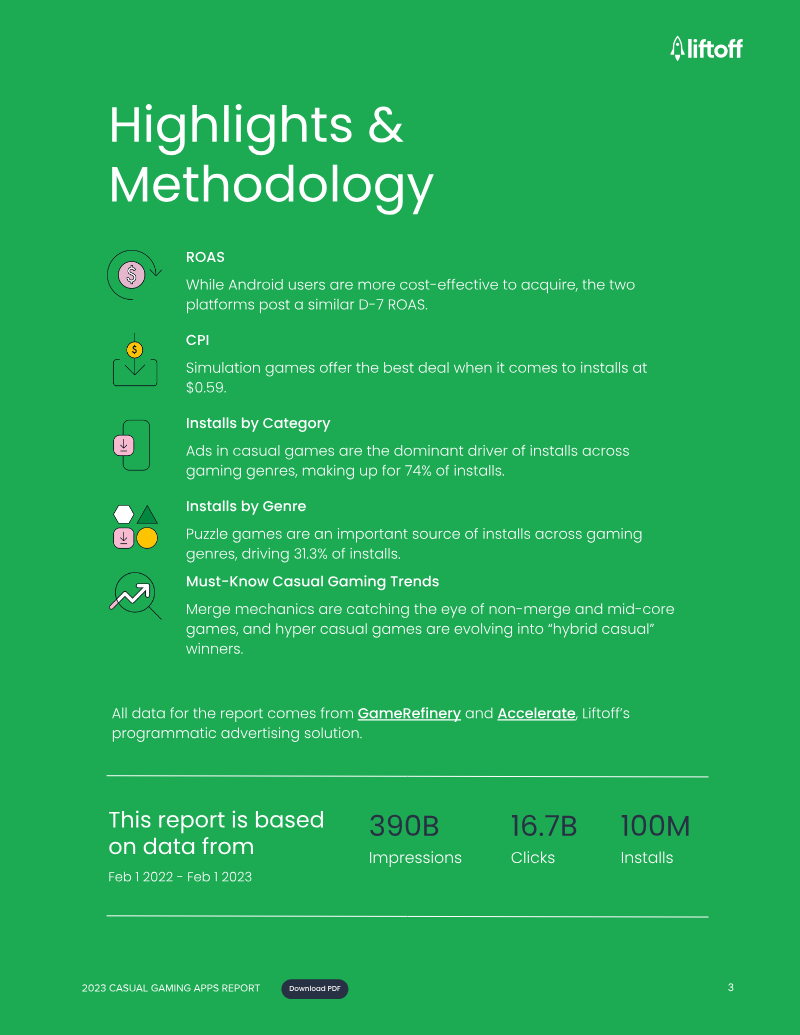

The casual gaming landscape in 2023 is defined by a strategic pivot from rapid user acquisition toward long-term profitability and sophisticated engagement models. While iOS acquisition costs significantly exceed those of Android at $2.23 compared to $0.63, both platforms achieve a comparable Day-7 return on ad spend of approximately 7.7%. North America remains the most expensive yet lucrative market, yielding an 8.1% return on ad spend despite a high $3.59 cost per install. Simulation games have emerged as a particularly efficient entry point for developers, maintaining the lowest acquisition costs at $0.59. Casual titles serve as the primary engine for the broader mobile ecosystem, driving 74% of installs across all gaming categories and nearly 75% of mid-core installs. Hyper-casual and puzzle games remain the dominant traffic sources, but the industry is increasingly embracing hybridization. This trend involves layering complex meta-elements, such as narrative progression and competitive social features, over simple core mechanics. By blending ad-based and in-app purchase monetization models, developers are successfully targeting crossover audiences and extending the lifecycle of traditionally short-lived genres. Engagement strategies now heavily rely on competitive mechanics and gameplay diversification. Approximately 90% of leading level-based titles utilize solo leaderboards, while over half incorporate team-based races, debunking the myth that casual players avoid competitive environments. Furthermore, nearly a quarter of top-grossing casual games integrate minigames, such as hidden object or board game mechanics, to refresh the user experience and lower acquisition barriers. These features collectively deepen player retention and monetization, signaling a shift toward more robust, feature-rich casual experiences that prioritize player depth over simple volume.

LiftoffJan 2023

Report

Casual Gaming Trends Snapshot Report March 2022

This analysis examines the evolving landscape of the casual mobile gaming market as of March 2022, focusing primarily on the United States iOS market. The central thesis posits that the casual sector has become increasingly competitive, forcing developers to move beyond simple core gameplay by integrating sophisticated meta-elements, hybrid mechanics, and social features to maintain chart positions and drive player retention. Key findings indicate a massive shift in the Match3 genre, where the presence of meta-elements in top-100 grossing games rose from under 10% six years ago to 70% by early 2022. Renovation and construction mechanics have emerged as the dominant trend; notably, every top-100 grossing casual game released in the two years preceding the report utilizes renovation elements. Construction features specifically appeared in 49% of top Match3 games, a significant increase from 7% in 2016. These elements are prized for providing visual progression and satisfying psychological "completionist" motivations without disrupting core game balance. The scope of the research covers the casual genre hierarchy—including subgenres like Match3, Solitaire, and Time Management—with a specific focus on top-grossing titles on the US iOS platform. Data points highlight the stability of the top three casual games between Q4 2020 and Q4 2021, while noting that newer titles like Royal Match and Project Makeover successfully captured market share by leveraging episodic design and deep customization. Methodologically, the insights are derived from the GameRefinery SaaS platform, utilizing a proprietary three-layered taxonomy (Category, Genre, Subgenre) developed with industry experts. The analysis concludes that successful casual games are increasingly adopting midcore-inspired features, such as social hangouts, competitive tournaments, and diverse minigames, to broaden their motivational appeal and create new monetization sinks in a post-IDFA marketing environment.

GameRefineryMar 2022