ReportRGDA – Romanian Game Developers Association

Video Games in Romania 2023

1 Jan 20231 pages~2 min full read

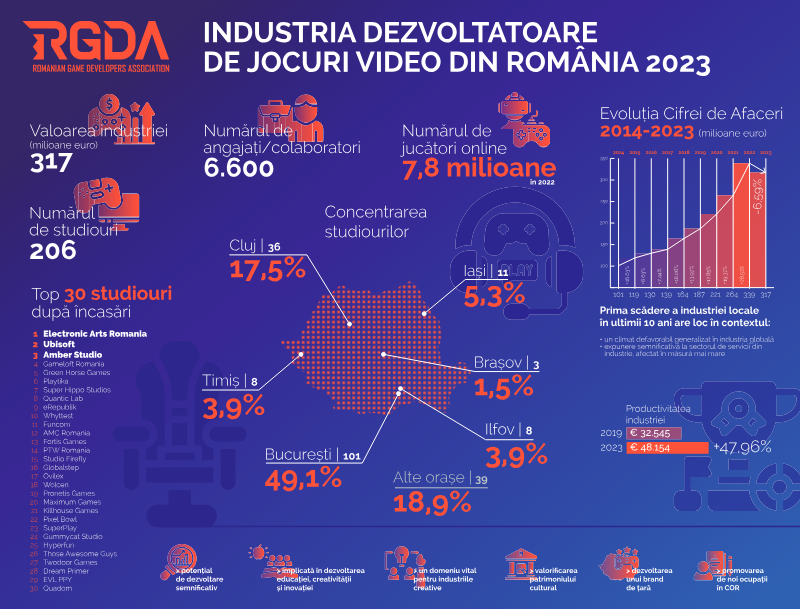

The Romanian video game industry reached a turnover of approximately €6.6 billion in 2023, supported by 350 active studios and a workforce of 6,600 employees.

The sector experienced a 6.6% contraction in 2022, marking the first decline in a decade due to an unfavorable global economic climate and service-sector volatility.

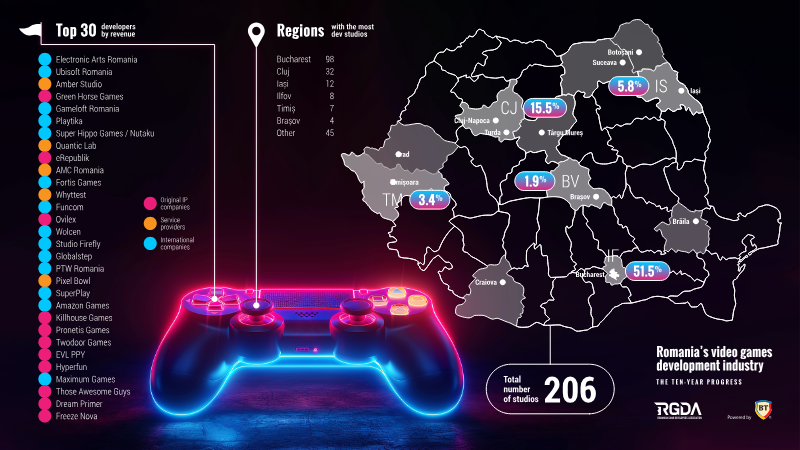

Industry activity is highly concentrated in key urban hubs, led by Cluj with 36 studios and Iași, which accounts for 17.5% of the total studio count.

The top 30 studios, including major players like Electronic Arts Romania, Ubisoft, Amber Studio Brașov, and Playtika, generate roughly 5% of the industry's total revenue.

The Romanian gaming ecosystem serves an estimated 7.8 million players through its titles and services.

Sustaining future growth will require strategic investments in educational initiatives and industry promotion to mitigate the risks posed by external market fluctuations.

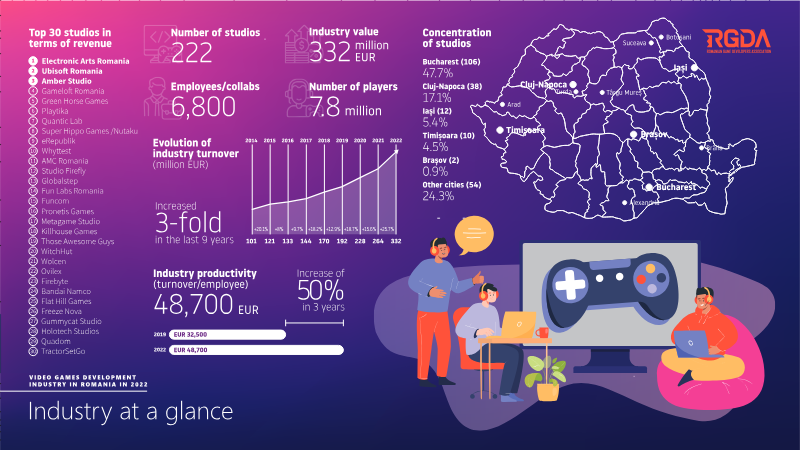

The 2023 analysis of Romania’s video‑game sector presents a comprehensive overview of its economic evolution, workforce expansion, and market concentration over the past decade. It establishes that the industry’s turnover has risen sharply, reaching approximately €6.6 billion in 2023, while the number of active studios grew to 350 and employment climbed to roughly 6 600 people. Online player participation also expanded, with an estimated 7.8 million gamers engaging with Romanian titles or services.

Growth trends are detailed year by year from 2014 to 2023, highlighting an overall upward trajectory in revenue and studio count, yet noting a first‑time contraction in 2022 of about 6.6 percent, attributed to a broadly unfavorable global climate and heightened exposure to the service‑sector dynamics that affect the industry more acutely than other creative fields. Geographic distribution shows a pronounced clustering in key urban hubs: Cluj hosts the largest concentration with 36 studios, followed by Iași, which accounts for 17.5 percent of the total, and other significant presences in Bucharest, Timișoara, and Brașov.

The report identifies the top thirty studios, which together generate roughly 5 percent of total industry revenue, and lists leading companies such as Electronic Arts Romania, Ubisoft, Amber Studio Brașov, and Playtika, among others. Their individual growth rates vary, with some recording double‑digit percentage increases, underscoring a heterogeneous performance landscape within the sector. The analysis concludes that despite recent headwinds, the Romanian video‑game ecosystem remains a vital and expanding creative economy, but it calls for reinforced educational initiatives, stronger promotion, and strategic support to sustain momentum and mitigate external risks.