This document details the admission of tinyBuild, Inc. to the AIM market of the London Stock Exchange, with trading scheduled to commence on March 9, 2021. The offering consists of a placement of approximately 91.4 million shares at 169 pence per share, resulting in a post-admission market capitalization of approximately £340.6 million. The company is raising £28.6 million in net proceeds to fund organic growth, strategic acquisitions, and the expansion of its intellectual property portfolio.

As a global video game publisher and developer, tinyBuild employs a digital-first, "own-IP" strategy designed to create high-margin, multi-platform franchises. The company’s business model relies on a data-driven selection process for indie and AA titles, supported by influencer marketing and community engagement. With a pipeline of 23 titles for 2021–2022, the company focuses on acquiring development teams—an "acqui-hire" approach—to secure long-term assets. Financial performance has shown consistent growth, with revenue increasing from $11.9 million in 2017 to $18.5 million in the first half of 2020, supported by a transition to IFRS reporting standards.

The scope of this admission is global, though it is subject to significant regulatory constraints. Because the company is incorporated in Delaware, its shares are classified as "restricted securities" under U.S. securities laws. Consequently, the offering is subject to Regulation S Category 3 transfer restrictions, which prohibit sales to U.S. persons or within the United States without registration or an applicable exemption. Investors are cautioned that the company faces operational risks, including revenue concentration in a small number of titles, reliance on third-party distribution platforms, and the complexities of managing a global workforce. Governance is managed through a six-member Board and adherence to the QCA Code, with specific anti-takeover provisions and protective measures in place to manage the company's concentrated shareholder structure.

tinyBuild · 2026

tinyBuild · 2025

tinyBuild · 2025

tinyBuild · 2024

tinyBuild · 2024

tinyBuild · 2023

tinyBuild · 2022

tinyBuild · 2021

tinyBuild · 2021

tinyBuild · 2021

tinyBuild

tinyBuild

PCF Group · 2025

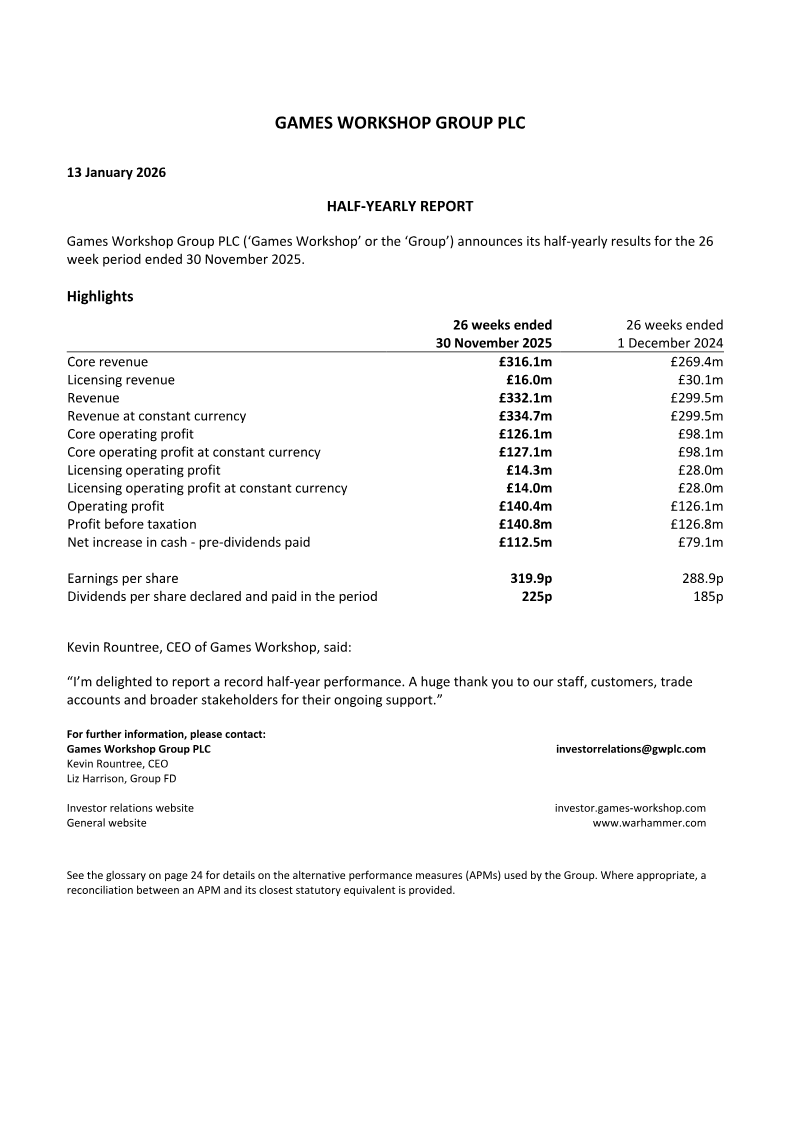

Games Workshop Group · 2025

InvestGame · 2024

Frontier Developments · 2023

PCF Group · 2021

InvestGame · 2021

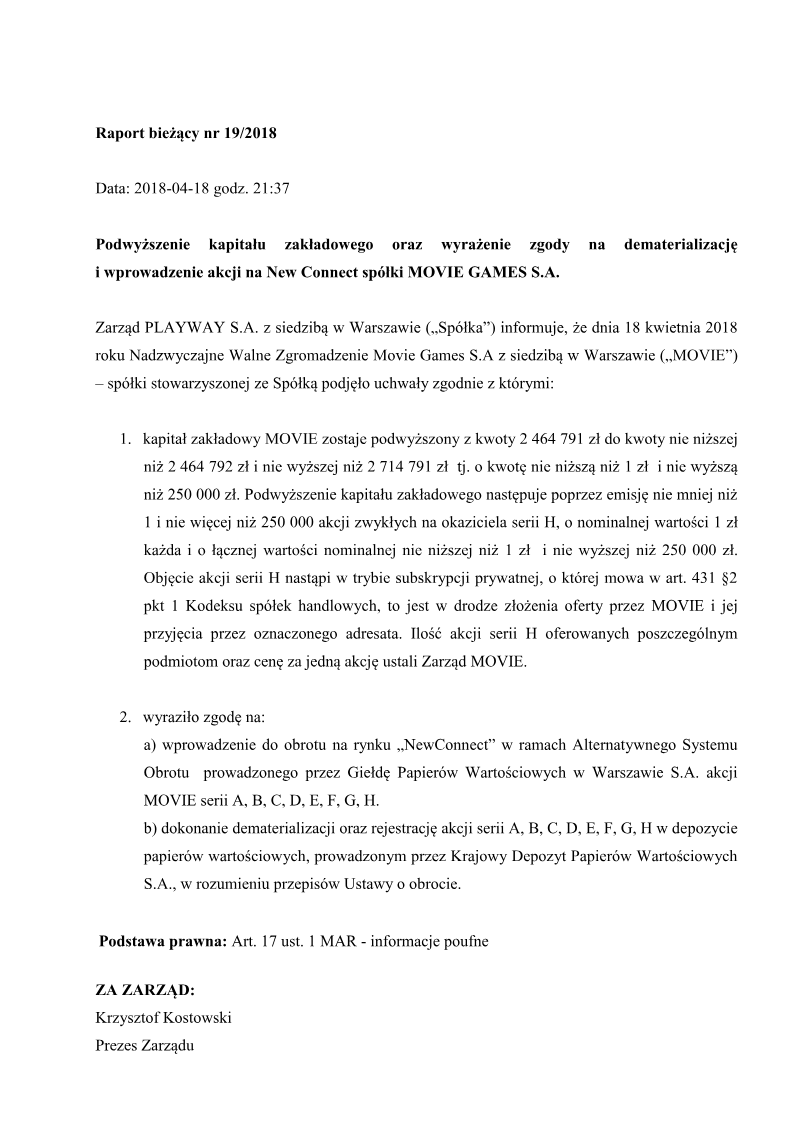

PlayWay · 2018

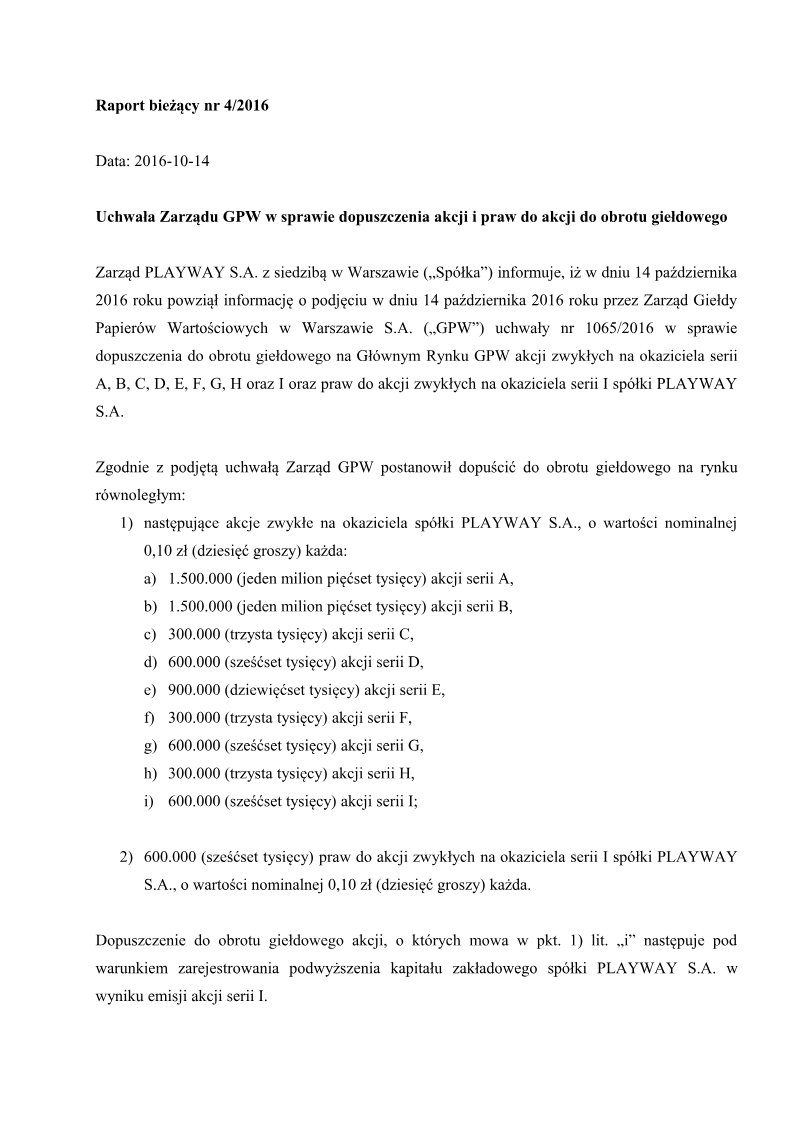

PlayWay · 2016

Games Workshop Group · 2015

PCF Group

PCF Group

Coffee Stain Group AB