ReportKoei Tecmo

Financial Highlights: 3rd Quarter of the Fiscal Year Ending March 2013

2 pages~4 min full read

Key insights

7 takeaways · ~3 min read- 01

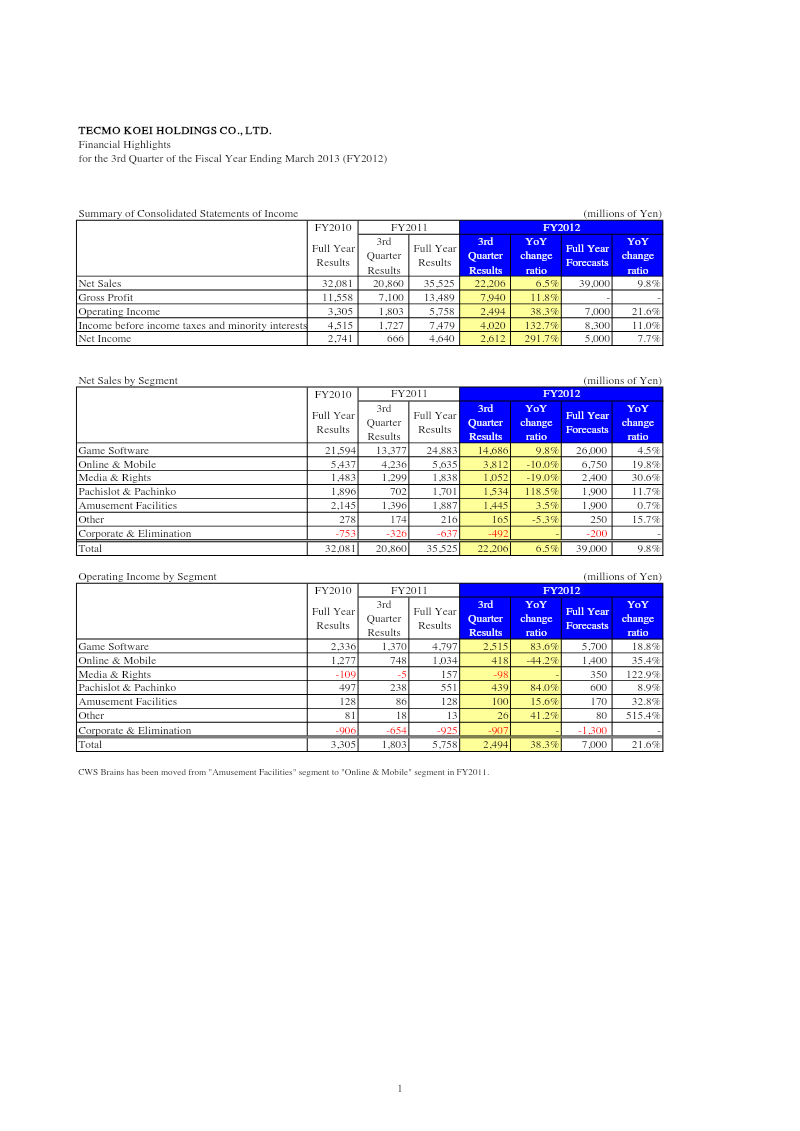

Tecmo Koei Holdings achieved a net income of ¥4,640 million for Q3 FY2012, representing a 291.7% increase over the prior year's ¥666 million.

See it on page 1 - 02

The Game Software segment was the primary driver of growth, with operating income surging 83.6% year-on-year to ¥4,797 million.

See it on page 1 - 03

Total net sales rose 6.5% to ¥35,525 million, while overall operating income climbed 38.3% to ¥5,758 million.

See it on page 1 - 04

The Online & Mobile segment saw sales increase to ¥5,635 million, but operating income dropped 44.2% to ¥1,034 million due to rising marketing expenditures.

See it on page 1 - 05

Media & Rights returned to profitability with an operating income of ¥157 million, a significant turnaround from the previous year's ¥109 million loss.

See it on page 1 - 06

Liquidity improved as current liabilities decreased from ¥9,220 million to ¥5,691 million, while shareholders' equity grew to ¥79,070 million.

See it on page 2 - 07

Pachislot & Pachinko and Amusement Facilities segments both posted gains, with operating incomes rising 84.0% to ¥551 million and 15.6% to ¥128 million, respectively.

See it on page 1