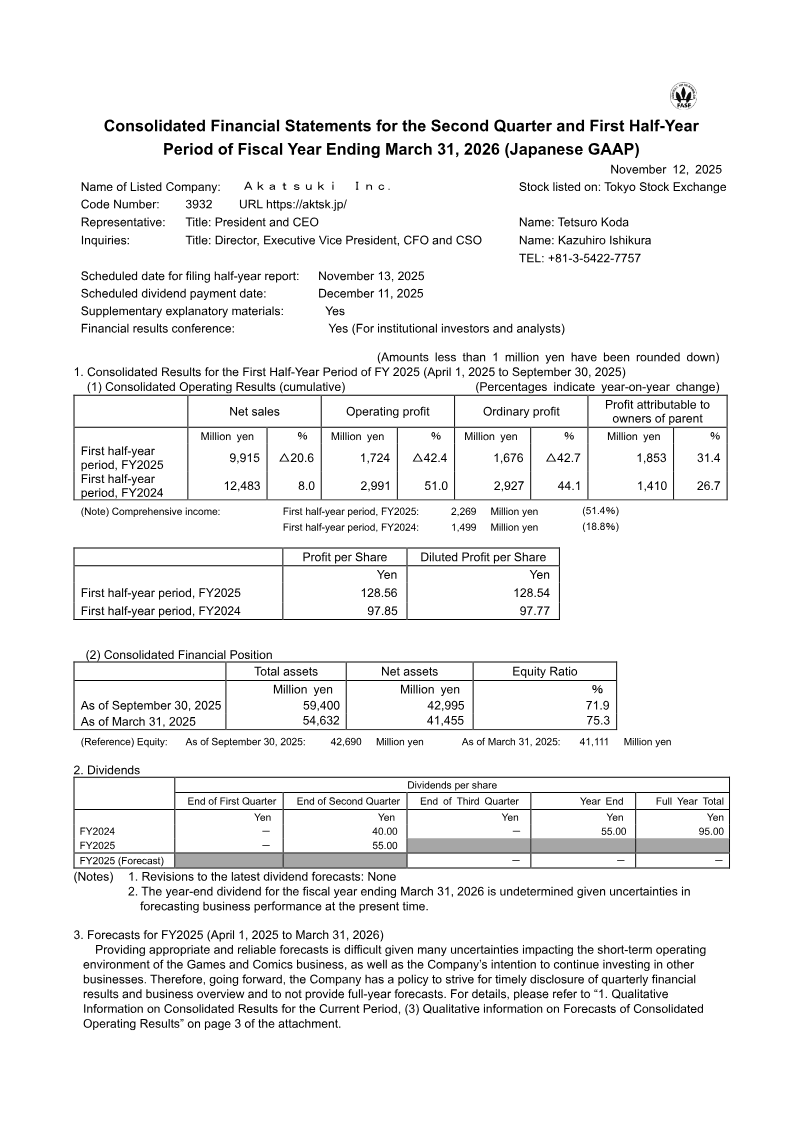

Akatsuki Inc. reports consolidated financial results for the first half of fiscal year ending March 31, 2026 (April 1–September 30, 2025). Net sales fell 20.6 % YoY to ¥9,915 million, while operating profit declined 42.4 % to ¥1,724 million; ordinary profit dropped 42.7 % to ¥1,676 million, yet net income attributable to parent rose 31.4 % to ¥1,853 million, driven by a higher comprehensive income of ¥2,269 million versus ¥1,499 million the prior year. Profit per share diluted increased from ¥97.85 to ¥128.56. Total assets grew to ¥59,400 million, with net assets rising to ¥42,995 million and equity ratio improving to 71.9 %. Cash flows from operating activities were modest at ¥369 million, while investing cash outflows of ¥5,433 million reflected significant purchases of investment securities and intangible assets. Financing activities generated net inflows of ¥1,775 million, offset by dividends paid of ¥795 million.

Segment analysis shows the Games and Comics business experienced a 23.2 % sales decline to ¥9,257 million and a 41.2 % profit drop, whereas the Entertainment and Lifestyle segment grew sales by 76.1 % to ¥649 million, achieving a 90.7 % profit increase. The Others segment recorded a sharp sales decline and continued losses.

The report notes significant consolidation changes: six new subsidiaries, including CRAYON Inc., were added; Akatsuki Fukuoka was liquidated. Goodwill increased by ¥4,316 million due to acquisitions of Natee and PAPABUBBLE JAPAN. No full‑year forecasts are provided, reflecting uncertainty in the Games and Comics market and ongoing investment plans.