Japan

Report

Financial Results for the Q3 of the Fiscal Year Ending March 2026

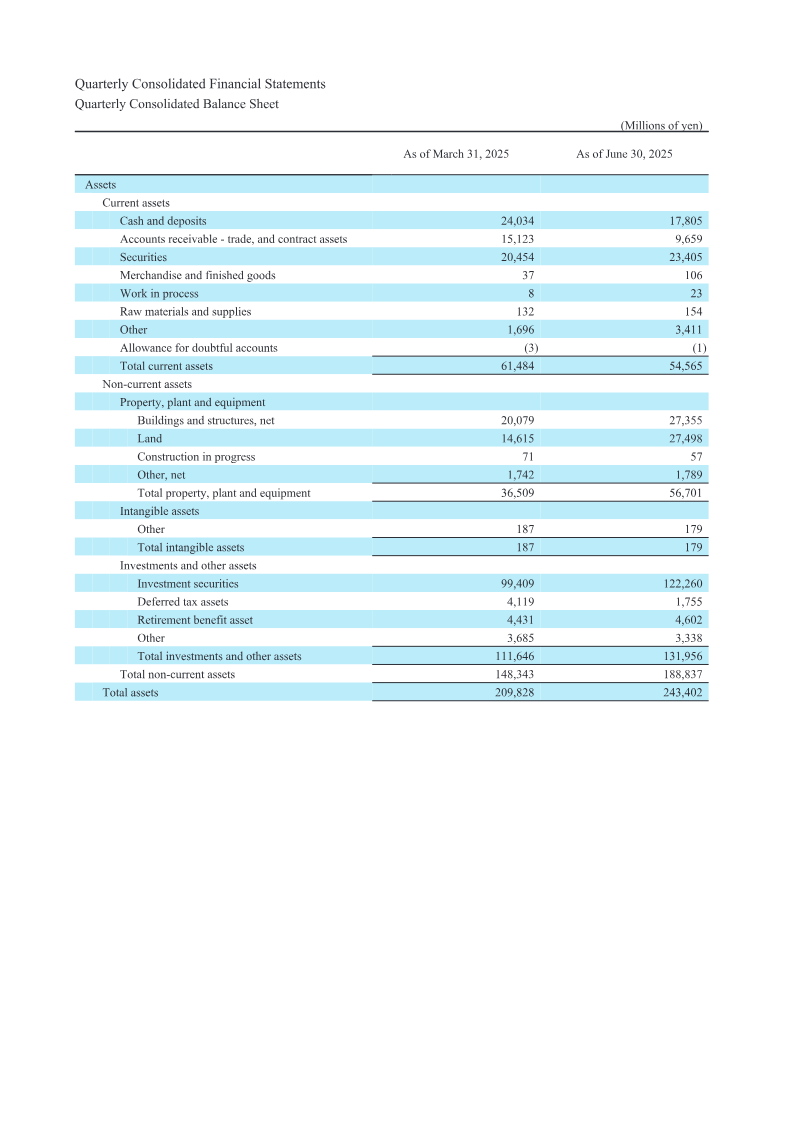

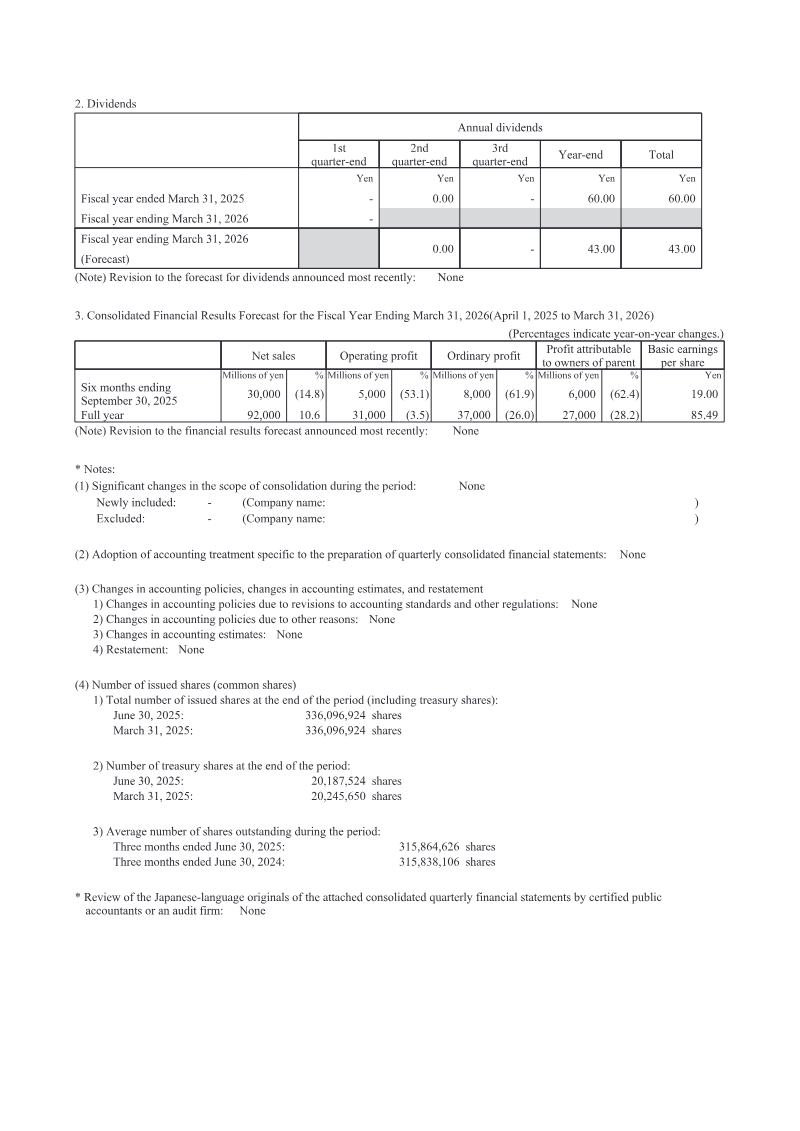

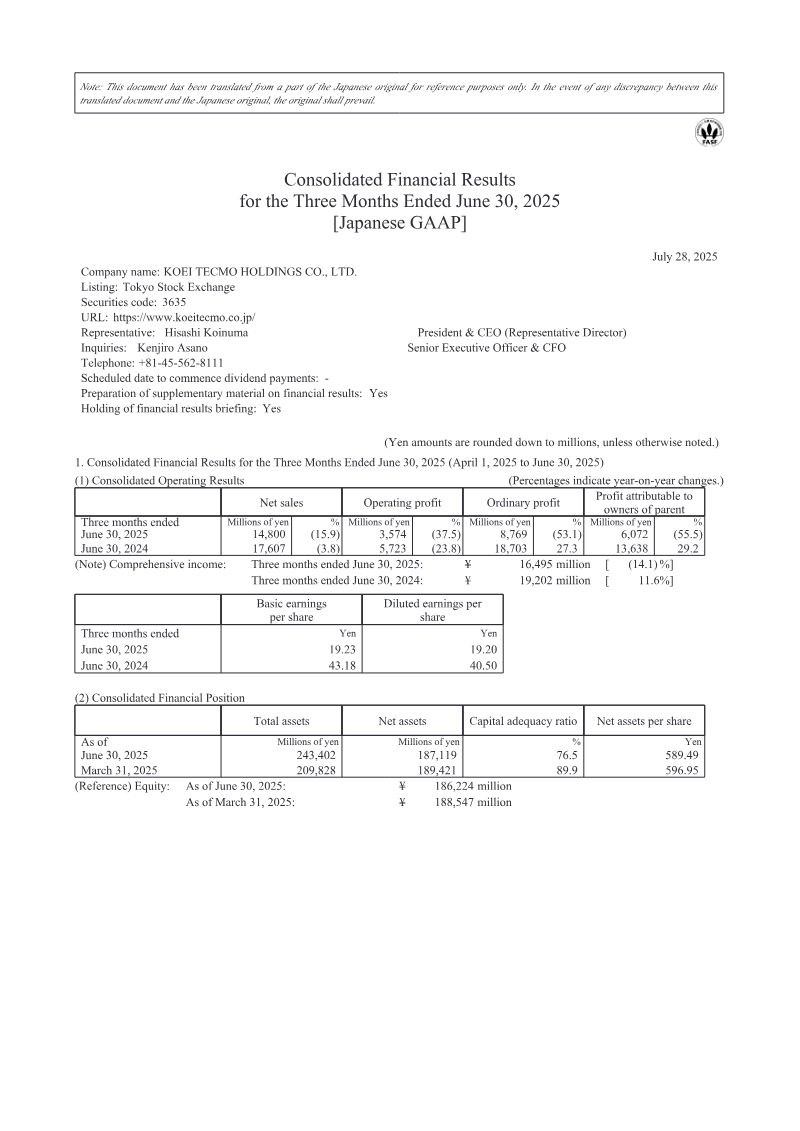

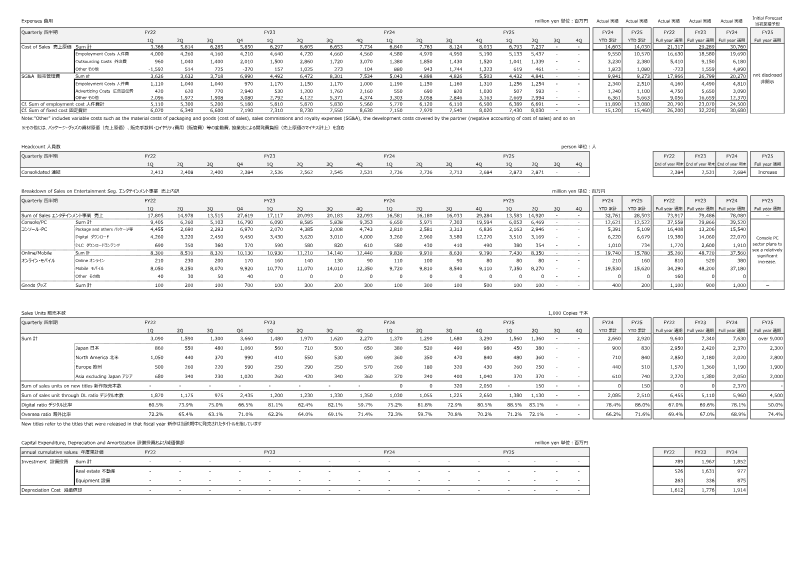

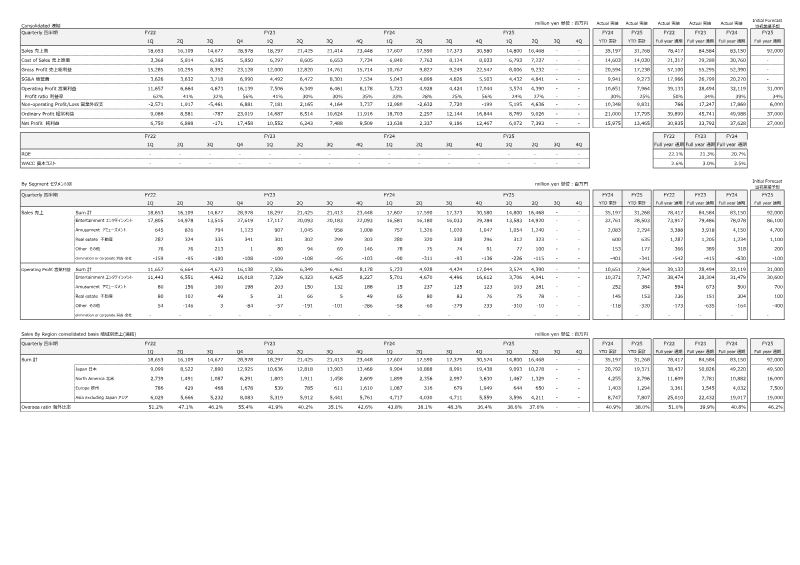

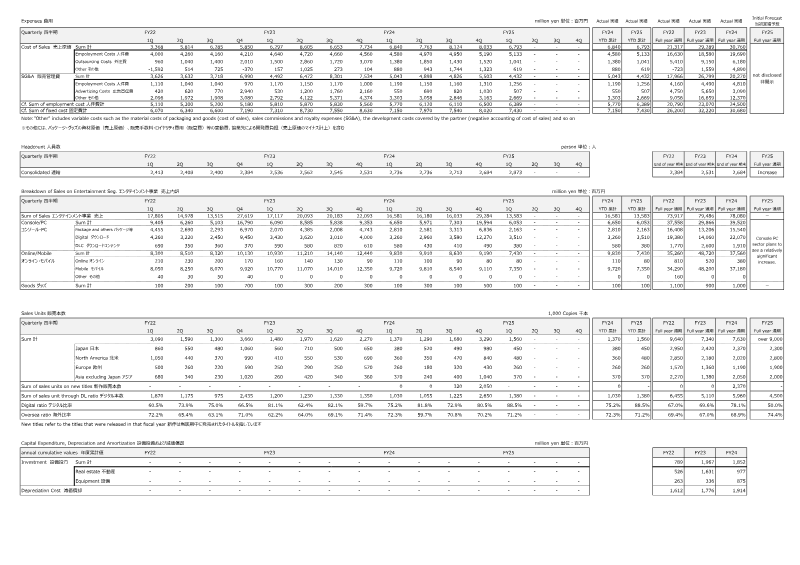

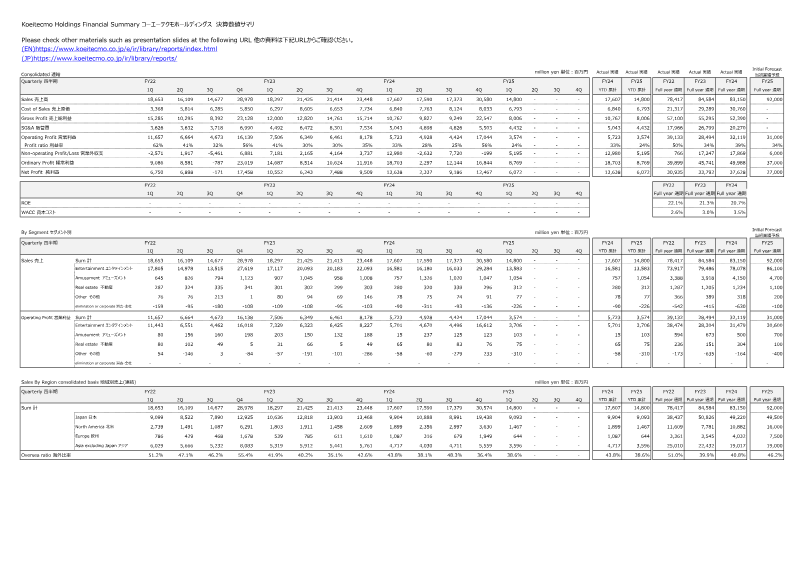

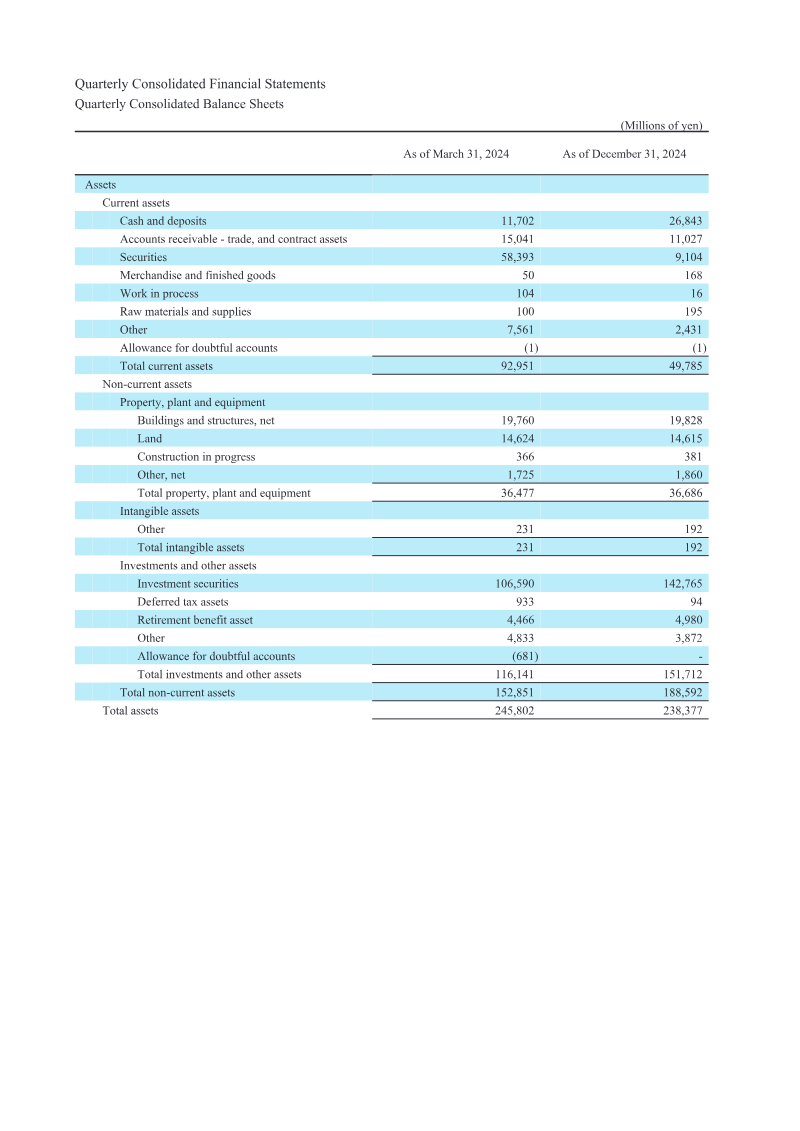

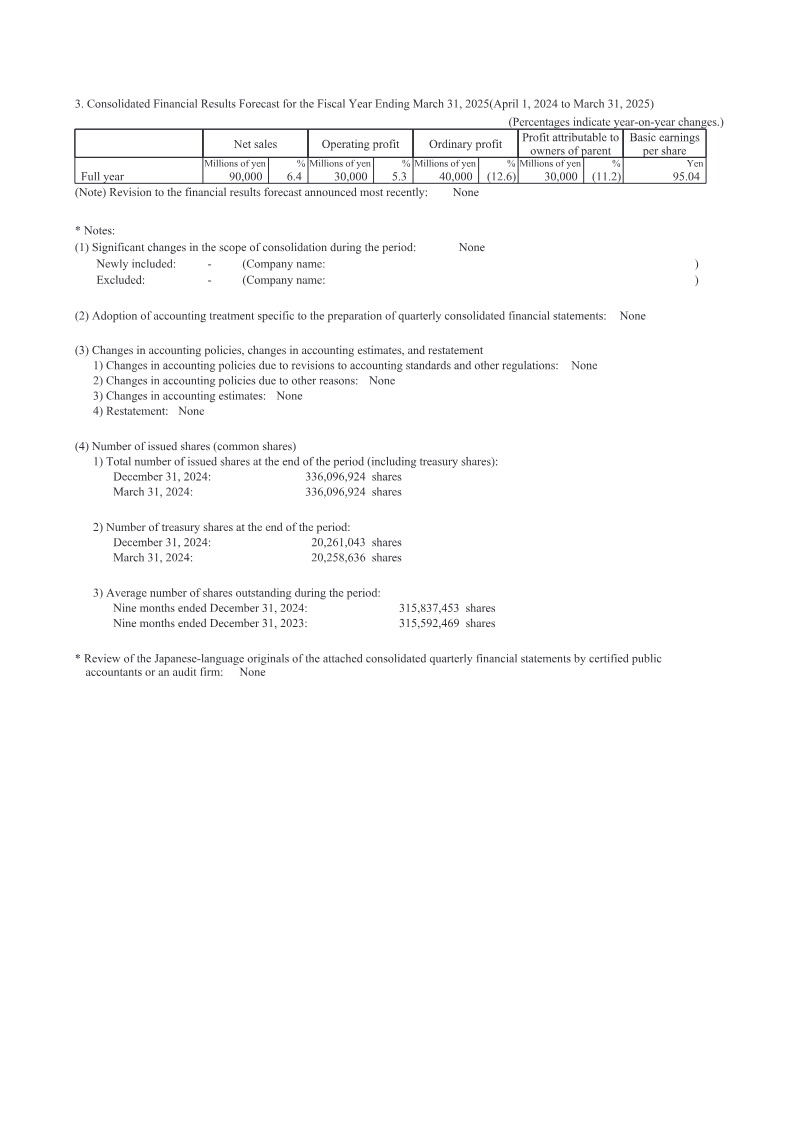

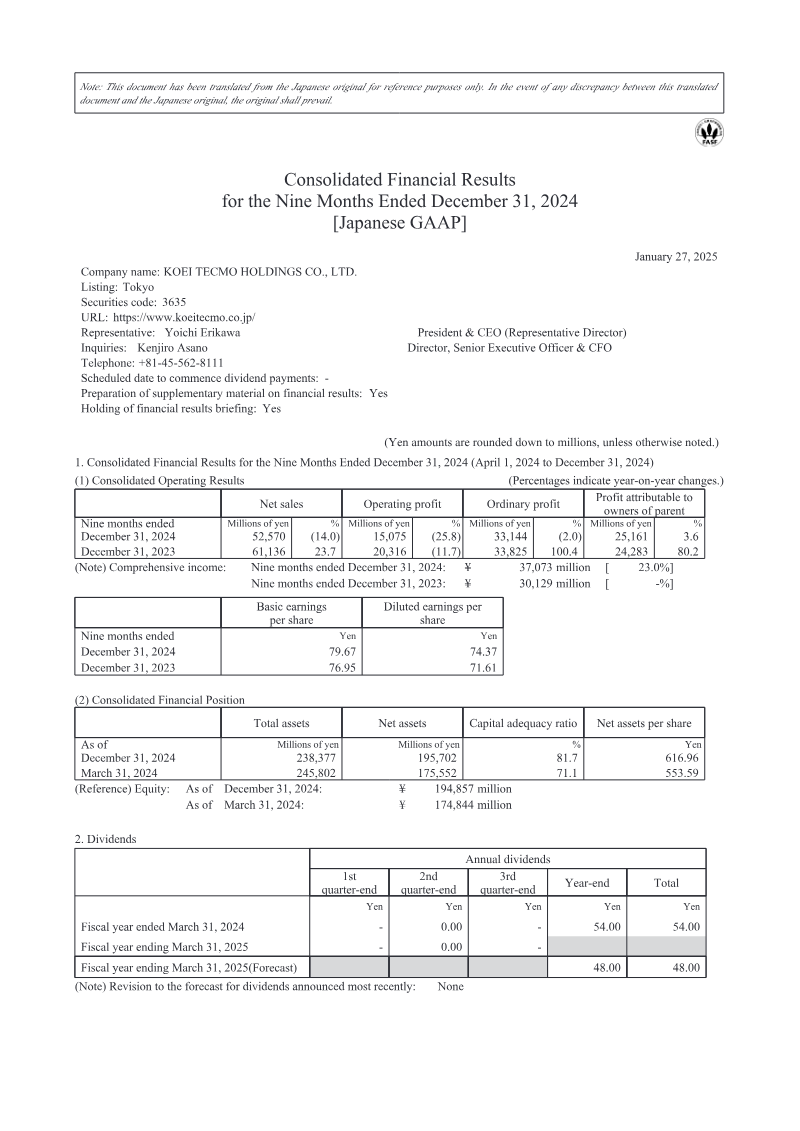

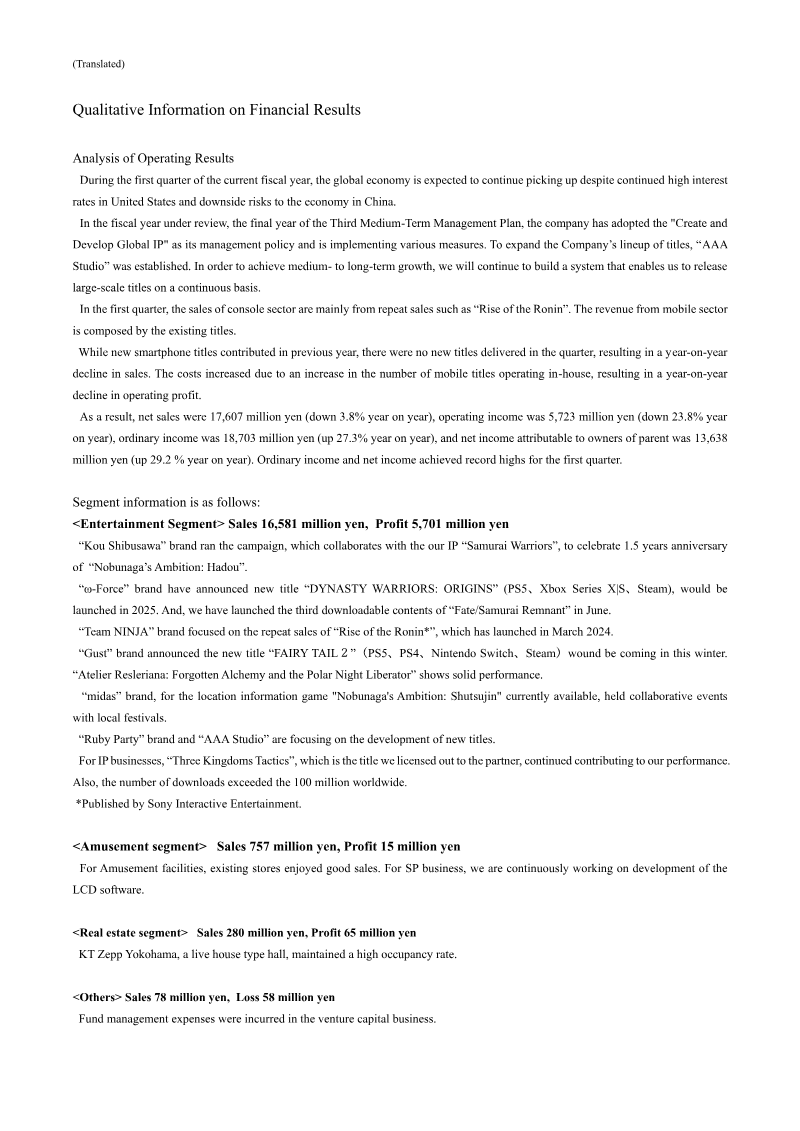

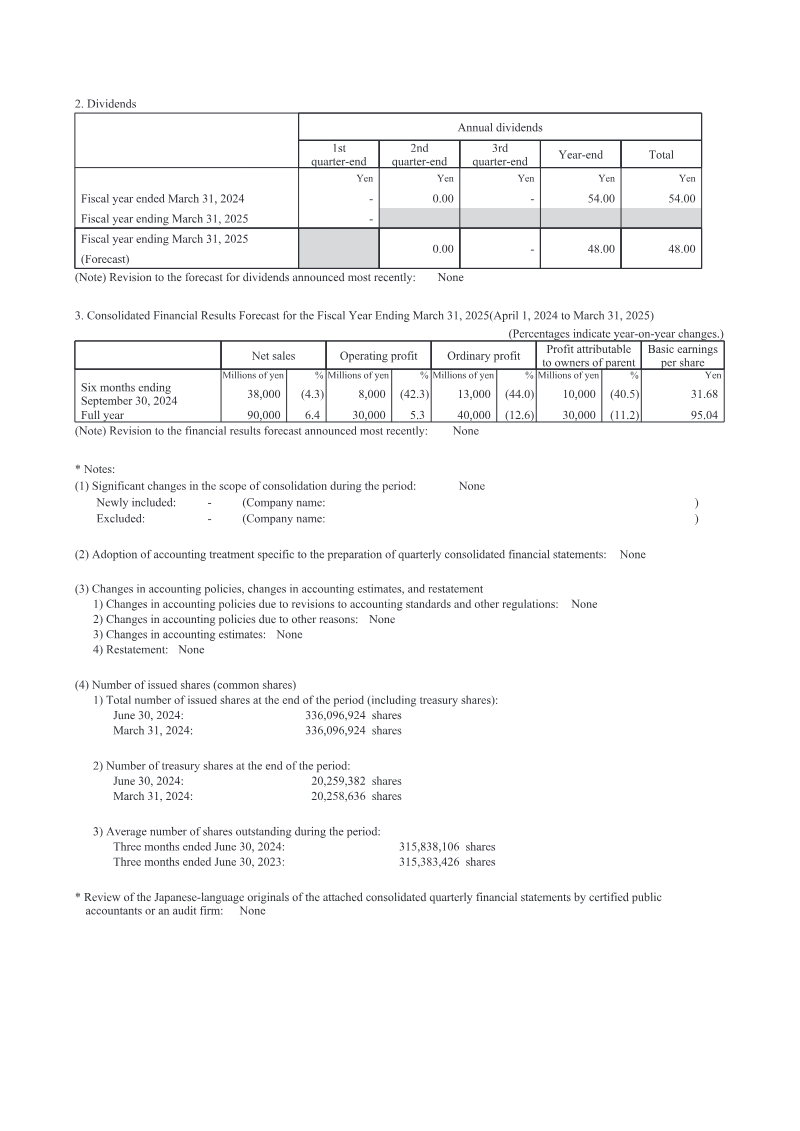

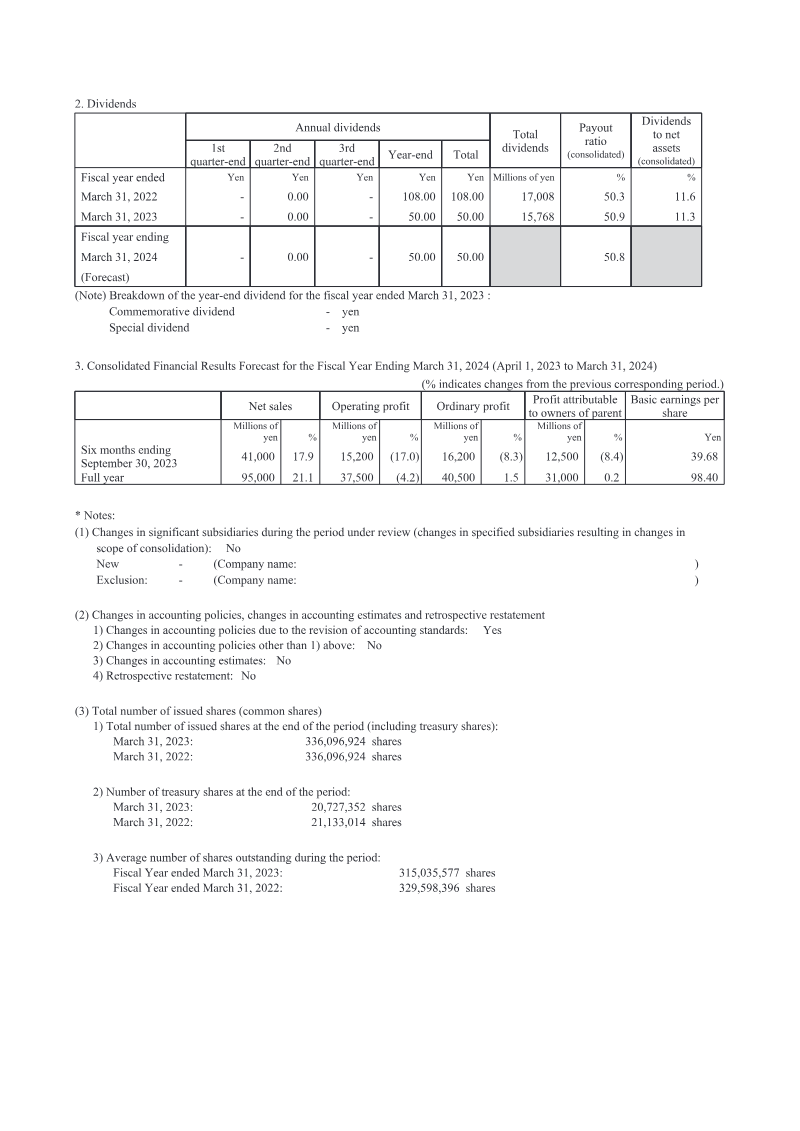

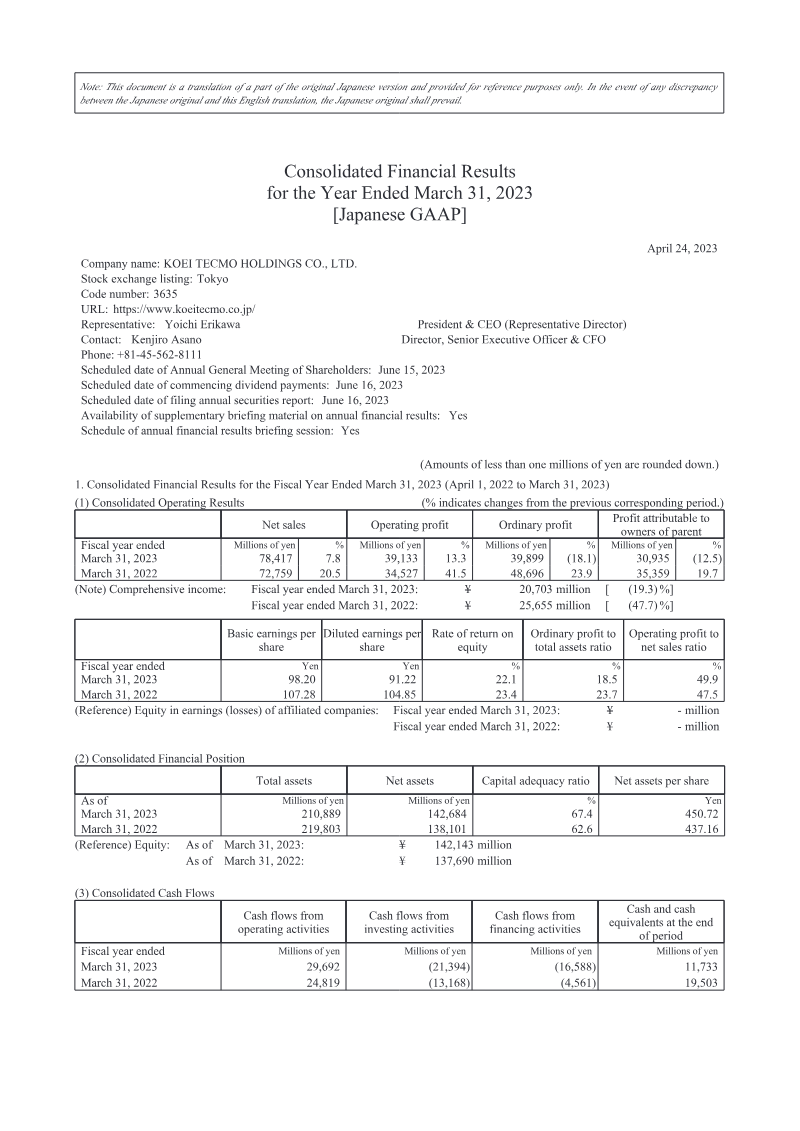

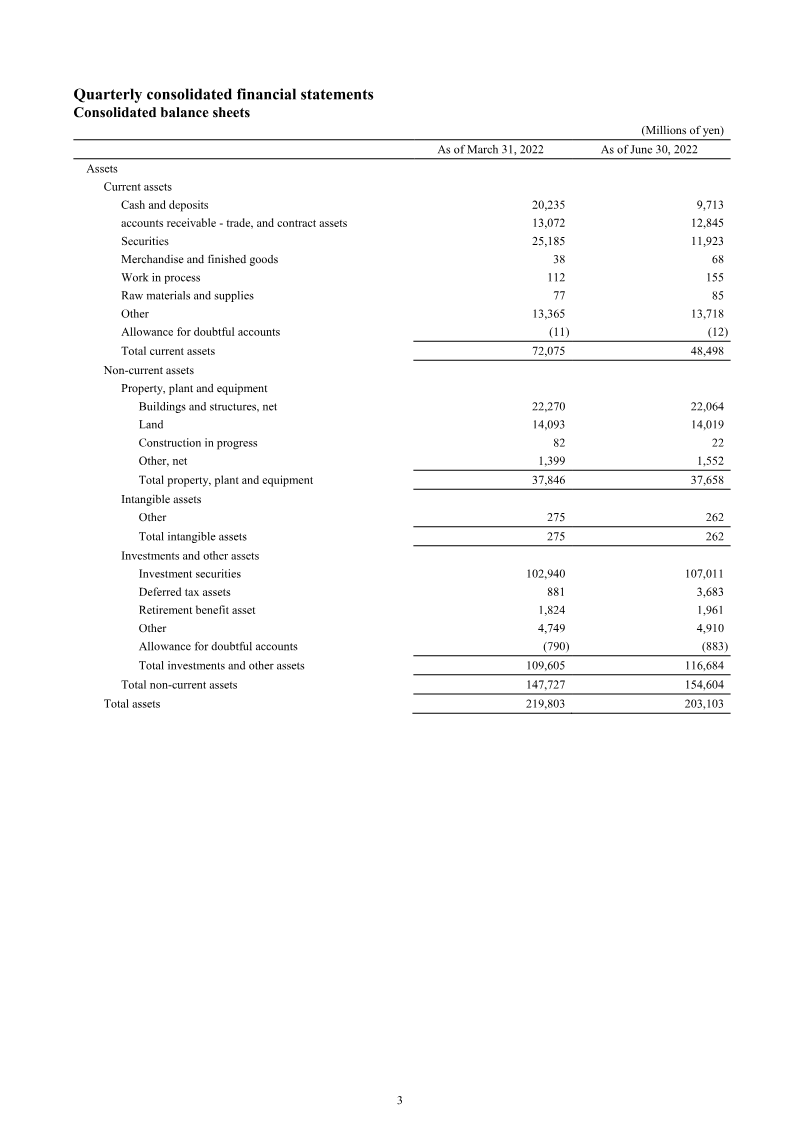

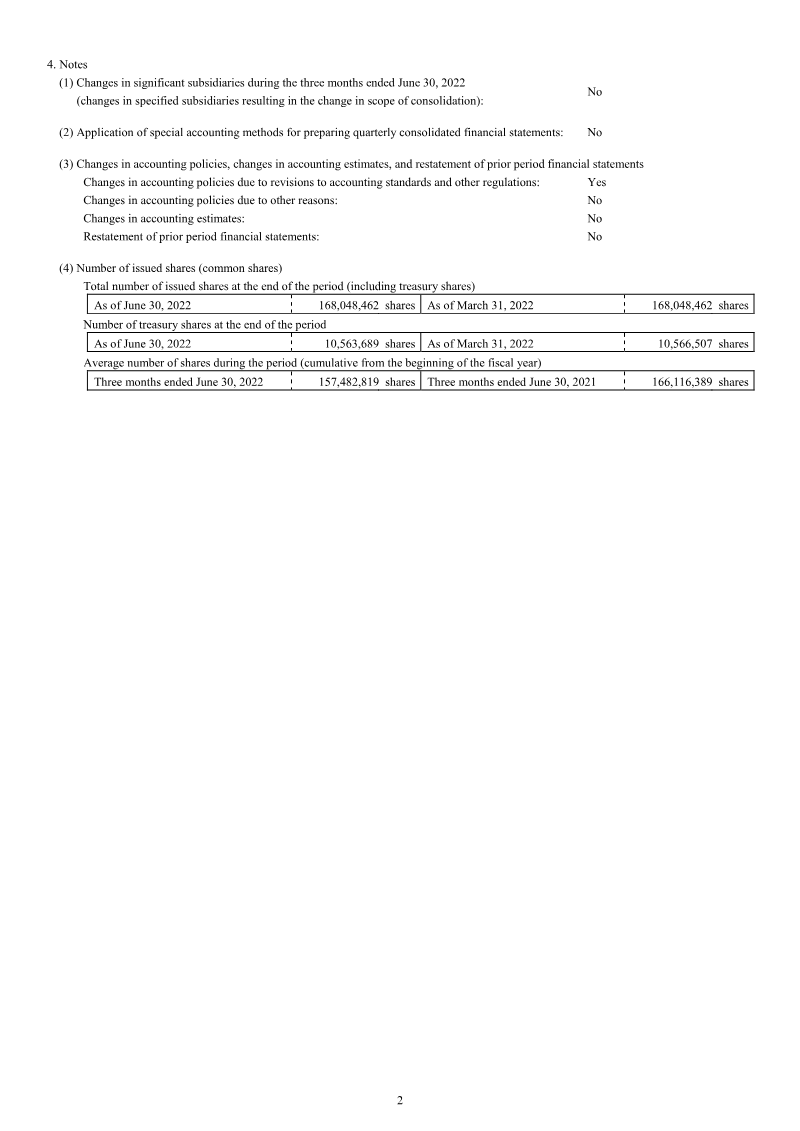

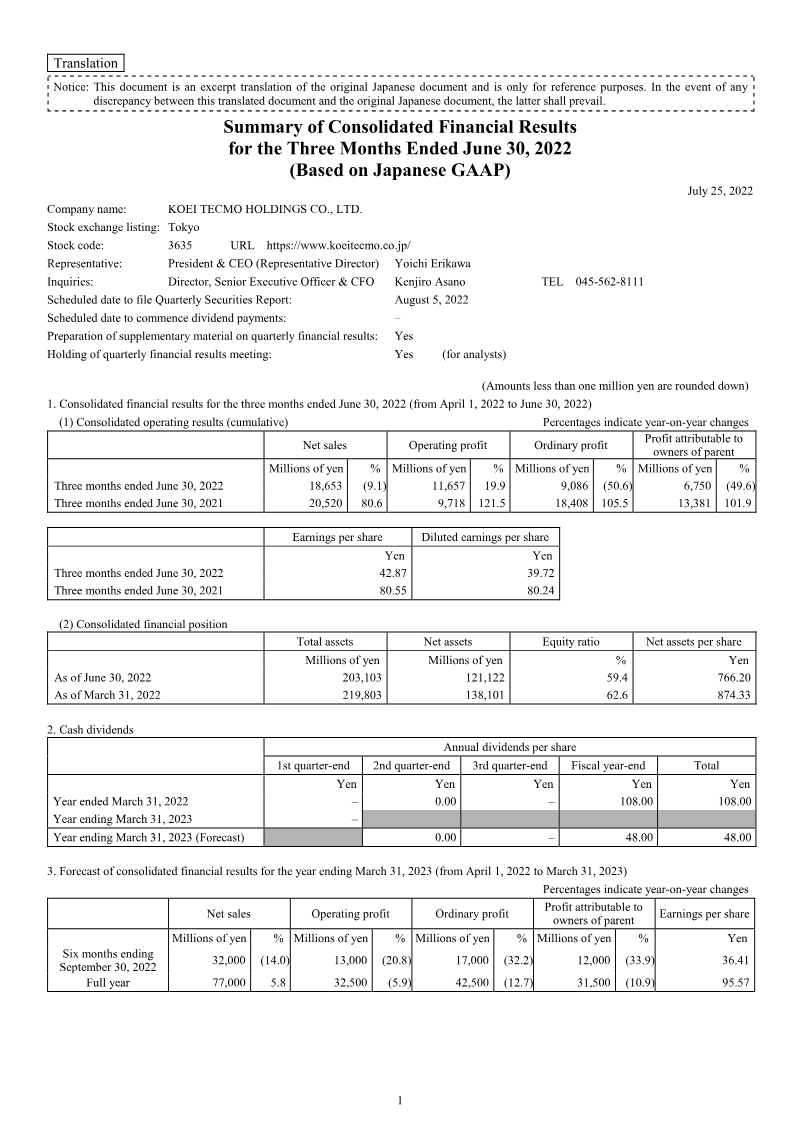

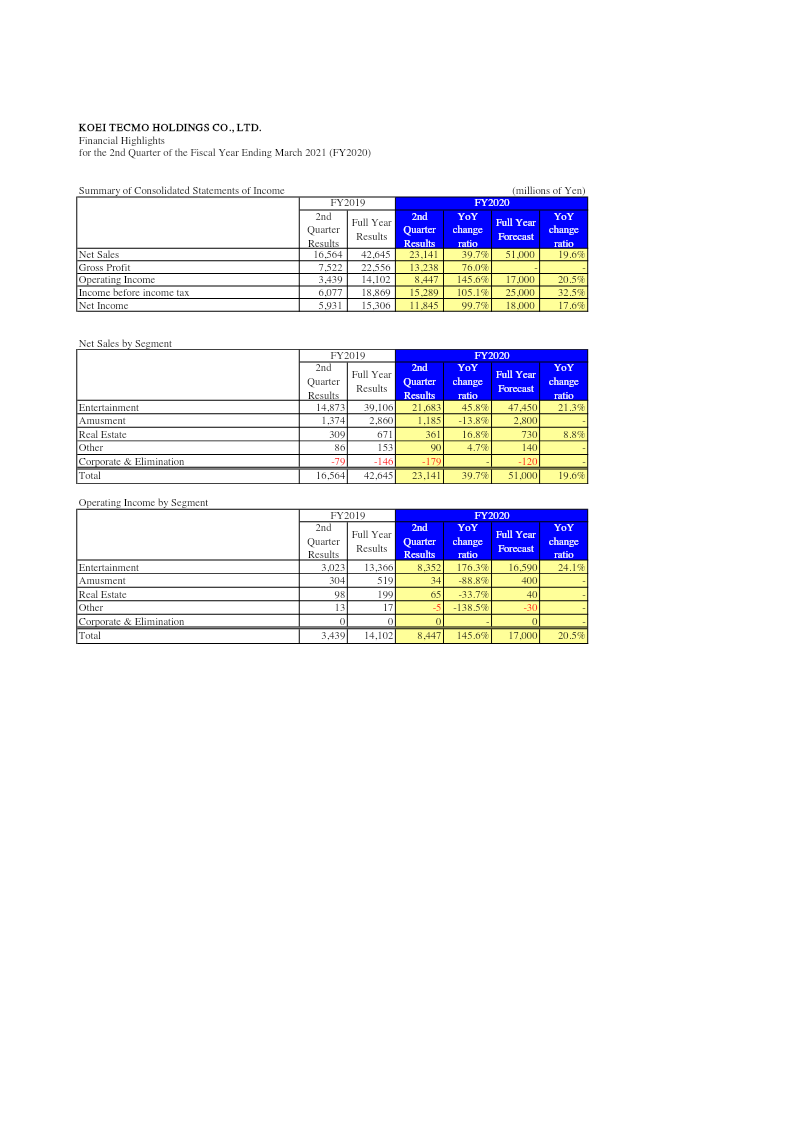

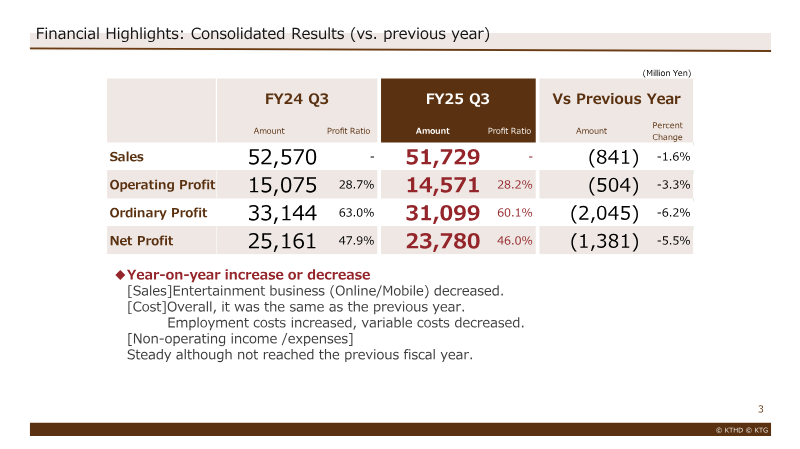

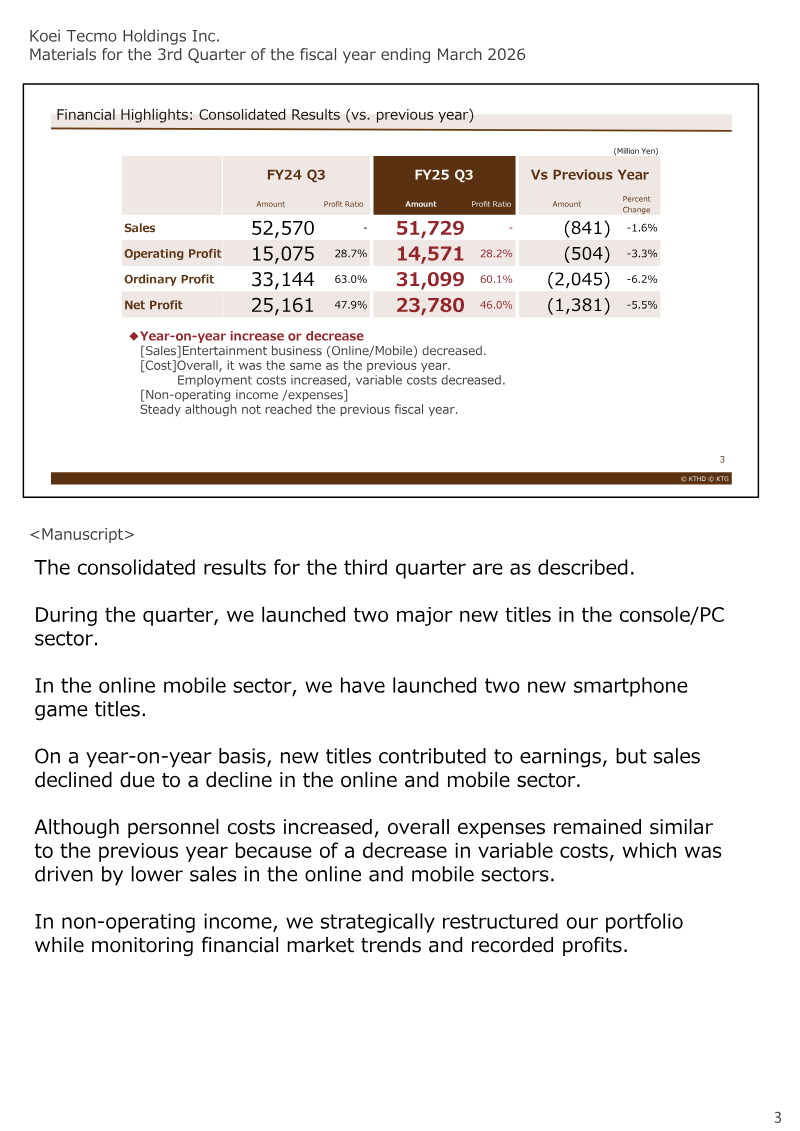

Financial results for the fiscal year ending March 2026 show a modest decline in consolidated sales, falling 1.6 % to ¥52,570 million from the previous year’s ¥51,729 million. Operating profit decreased by 3.3 % to ¥15,075 million, while ordinary and net profits fell 6.2 % and 5.5 %, respectively, reflecting a 1.6 % drop in entertainment‑business revenue and unchanged overall costs. Employment costs rose by ¥1,540 million, whereas outsourcing and advertising expenses fell slightly, keeping total cost trends flat. Segment analysis indicates a 2.5 % decline in entertainment sales, driven by weaker online/mobile performance; however, amusement‑facility revenue rose 10.8 % to ¥3,436 million, and real‑estate sales increased modestly. The company’s earnings forecast for FY25 remains unchanged: projected sales of ¥92,000 million (up 10.6 % from FY24), operating profit of ¥31,000 million (down 3.5 % from FY24), and net profit of ¥27,000 million (down 28.2 %). Dividend per share is projected at ¥43, a 28.3 % reduction from FY24. Methodology relies on consolidated financial statements and explanatory materials released via the corporate IR portal; data cover Japan‑based operations across entertainment, amusement, real estate, and other segments. The forecast assumes stable cost structures, no major temporary expenses, and an exchange rate of ¥140 per dollar. The company emphasizes a medium‑term strategy focused on expanding its title pipeline and strengthening human capital to support long‑term growth toward a top‑10 global position.

Koei Tecmo

Report

Financial Results for the Q3: Fiscal Year Ending March 2026

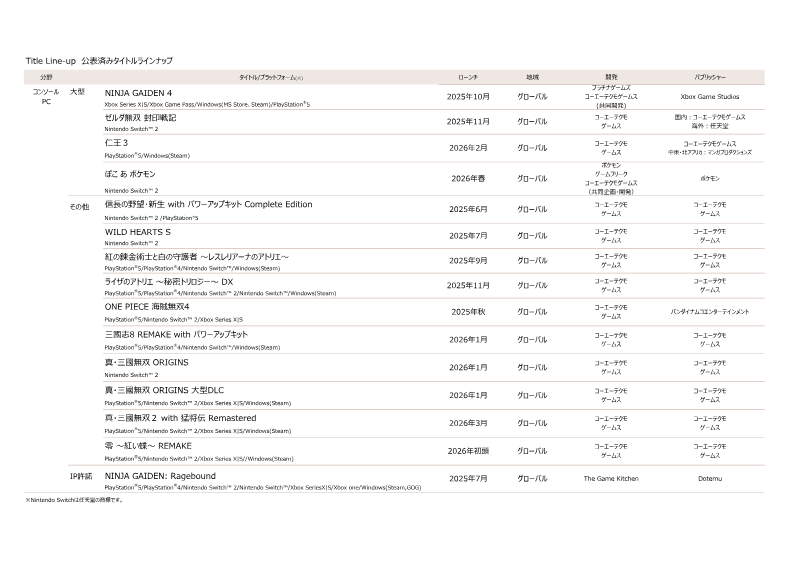

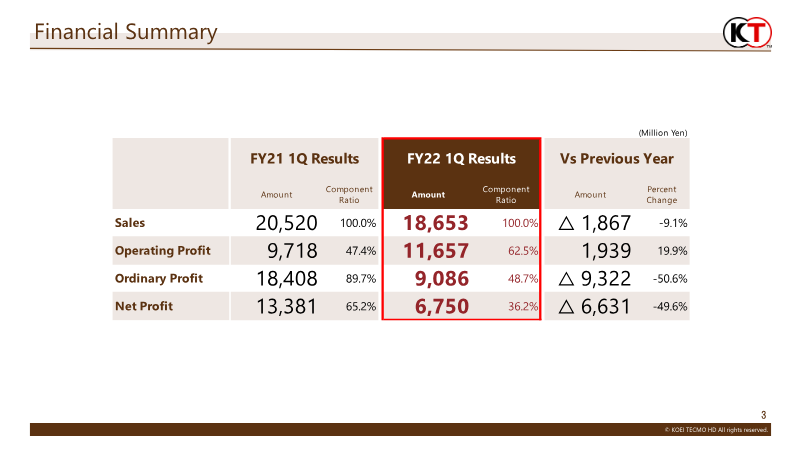

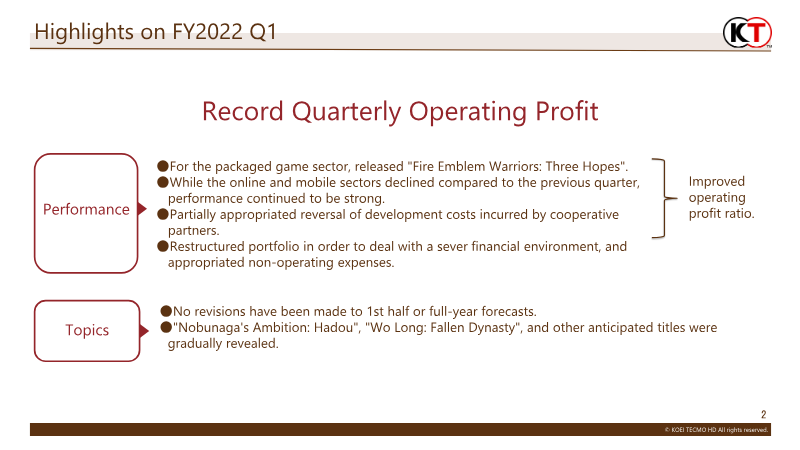

The quarterly briefing outlines KOEI TECMO HOLDINGS’ financial performance for the third quarter of fiscal 2026, highlighting a modest decline in consolidated sales to ¥52.57 billion from ¥51.73 billion, a 1.6 % year‑on‑year drop driven primarily by weaker online and mobile segments. Operating profit fell to ¥15.08 billion, a 3.3 % decline, while ordinary and net profits decreased by 6.2 % and 5.5 %, respectively, reflecting higher employment costs offset by reduced variable expenses. Segment analysis shows entertainment sales contracted by ¥1.25 billion, whereas amusement and real‑estate units posted gains of ¥333 million and ¥34 million, respectively. The company’s earnings forecast for FY25 remains unchanged, projecting sales of ¥92 billion and operating profit of ¥31 billion, with a 28.2 % drop in net profit to ¥27 billion and a dividend reduction of 28.3 % to ¥43 per share. Cost trends indicate employment expenses rising by roughly 10 % annually, while outsourcing and advertising costs are lower than the initial FY25 forecast. New console/PC titles such as “NINJA GAIDEN 4” and “Hyrule Warriors: Age of Imprisonment” contributed to a 2.3 billion yen increase in that segment, whereas online/mobile sales declined by ¥3.8 billion despite the launch of two new mobile titles. The company emphasizes a balanced pipeline strategy, combining major releases with mid‑tier and licensed IPs to stabilize revenue streams. The outlook for Q4 focuses on multiple console/PC releases, including “Nioh 3,” and continued promotion of existing mobile titles, with advertising spend expected to rise but no significant new capital expenditures anticipated.

Koei Tecmo