Mobile

Report

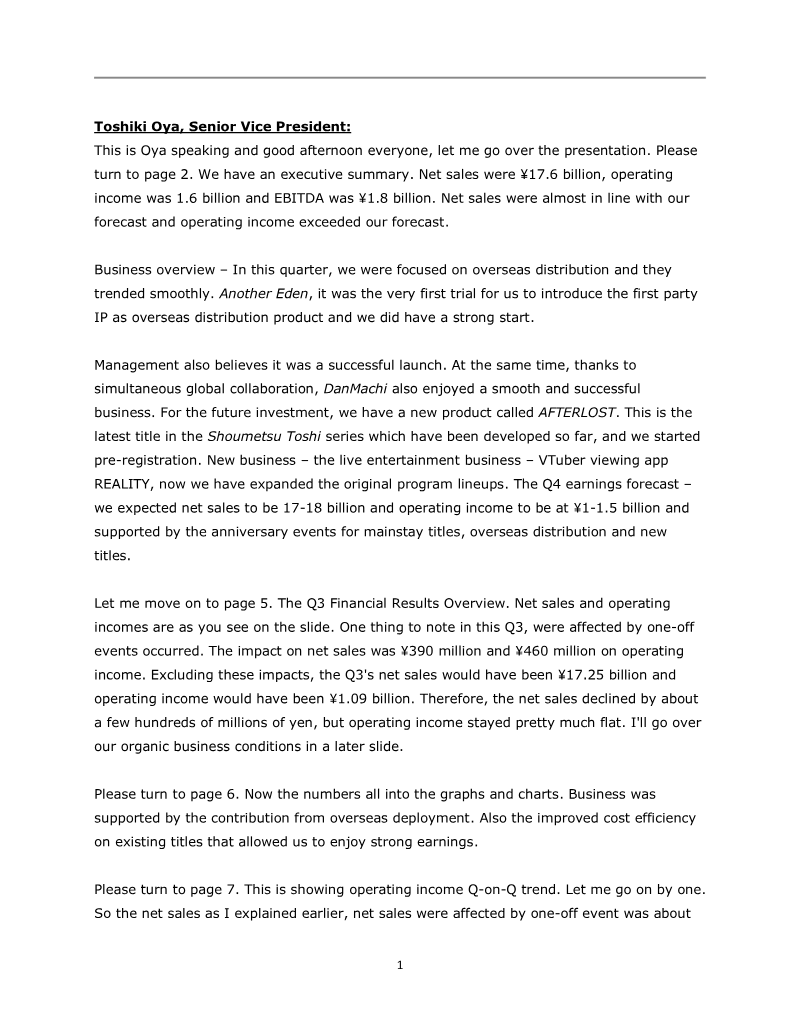

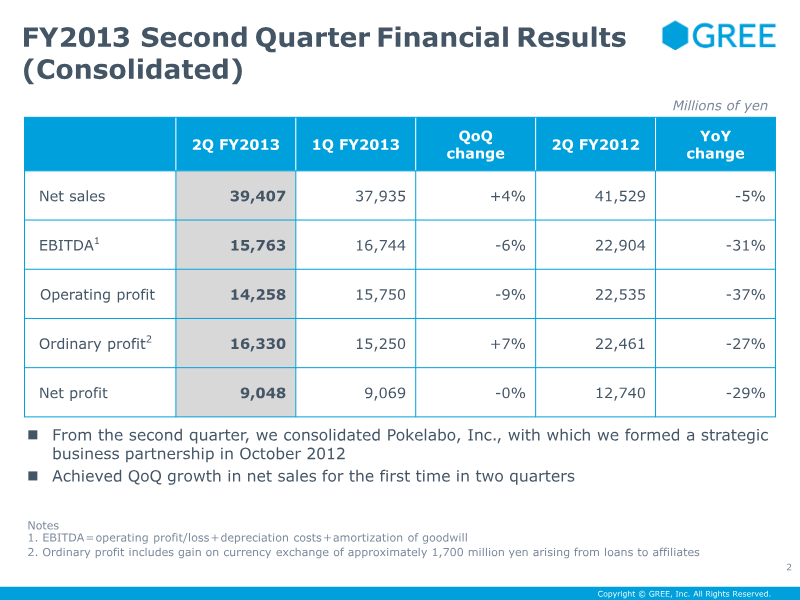

FY2013 Second Quarter Financial Results

The quarterly financial release outlines a mixed performance for FY2013 second quarter, with net sales rising 4 % QoQ to ¥39.4 billion but falling 5 % YoY, while EBITDA and operating profit declined sharply by 6 % and 9 %, respectively. Net profit remained flat QoQ at ¥9.0 billion but dropped 29 % YoY, reflecting higher costs and a one‑time currency gain. Consolidation of Pokelabo in October contributed to the QoQ sales growth, and the company noted a 35 % increase in cost of sales driven by higher labor and advertising expenses, alongside a 60 % rise in depreciation. Geographically, Japan remains the core market; coin consumption grew QoQ by 600 million coins, with strong performance in native titles such as “Driland” and IP‑based releases. Overseas coin consumption has been rising monthly since October, with new in‑house and co‑branded games expected to contribute from Q3 onward. The company plans aggressive smartphone investments in H2, targeting hit titles across new genres (MMO, FPS) and leveraging efficient marketing to balance lifetime value against cost per install. The revised FY2013 forecast reflects a downward revision of net sales to ¥170 billion (−17.9 % from prior forecast) and operating profit to ¥60 billion (−32.4 %). The outlook hinges on postponed releases in H2 and continued hiring to support smartphone growth, with anticipated increases in customer‑support and compliance costs. Overall, the report signals a strategic pivot toward diversified game genres and international expansion while managing cost pressures in a competitive mobile gaming landscape.

GREE

Report

FY2014 First Quarter Financial Results

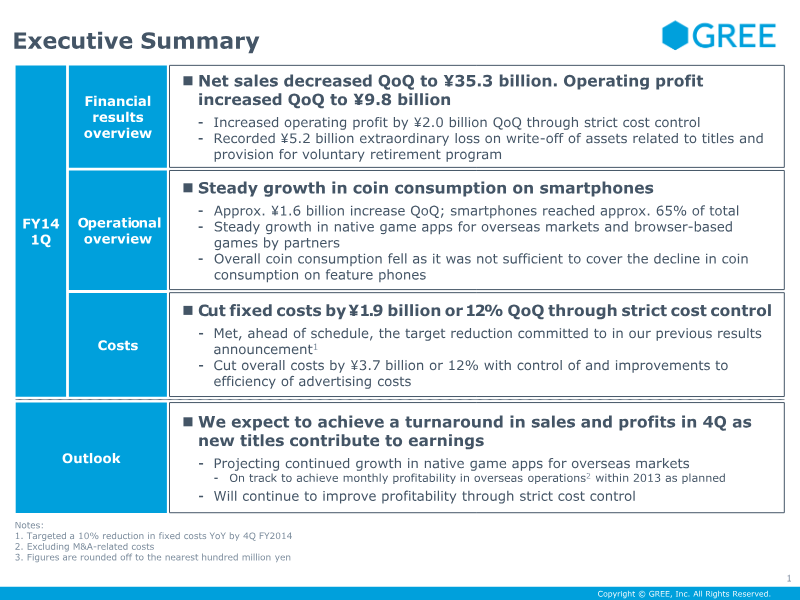

The quarterly report presents a mixed financial picture for FY2014 first quarter, with net sales declining 1.7 % QoQ to ¥35.3 billion while operating profit rose by ¥2.0 billion to ¥9.8 billion, driven largely by a ¥3.7 billion reduction in total costs and a ¥1.9 billion cut in fixed expenses. EBITDA increased to ¥11.6 billion, and the operating‑profit margin expanded by 6.6 percentage points to 27.7 %. A significant extraordinary loss of ¥5.0 billion—primarily from a ¥4.2 billion write‑off of title assets and a ¥0.6 billion voluntary retirement provision—offsets the operating gains, leaving net profit at ¥2.4 billion versus a loss of ¥0.3 billion the prior year. Operationally, coin consumption on smartphones grew by ¥1.6 billion QoQ and now accounts for roughly 65 % of total coin spend, reflecting a strategic shift from feature phones to mobile devices. The company continues to release new titles in overseas markets and Japan, targeting a turnaround in Q4 as fresh releases contribute earnings. Cost control remains a priority: advertising spend fell by ¥1.8 billion, and labor costs were trimmed through headcount reductions linked to the retirement program. Geographically, the report covers Japan and overseas operations, with a focus on native game apps in Europe and Asia. The methodology relies on consolidated financial statements, cost‑structure analysis, and coin‑consumption metrics derived from user data. Overall, the company projects a return to profitability in Q4 through disciplined cost management and accelerated title launches.

GREE