Report

Estudio Videojuegos y Adultos 2015: España

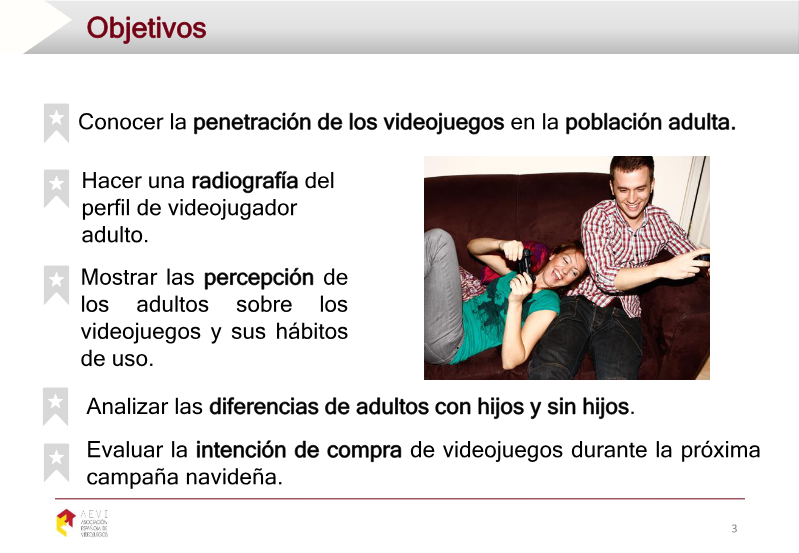

The study aimed to gauge the penetration of video games among Spanish adults, map the demographic profile of adult gamers, explore attitudes and usage habits, compare adults with and without children, and assess purchase intentions for the 2015 holiday season. Conducted nationwide in November 2015, it surveyed 1,000 individuals aged 18 and over via telephone CATI interviews, yielding a margin of error of ±3.09 percent. Overall, 38.9 percent of Spanish adults reported playing video games, while 61.1 percent did not. Play rates were highest among 18‑ to 29‑year‑olds, with three‑quarters engaging in gaming, and remained substantial for the 30‑44 age group at 54.3 percent. Men were more active than women (45.3 percent versus 32.8 percent), though women with children showed a higher participation rate (36.9 percent) than those without (30.1 percent), whereas the opposite pattern held for men. About 46.9 percent of gamers were occasional (at least monthly) and 41.5 percent habitual (weekly or daily), with habitual players being 60 percent male. Among habitual parents, 83.1 percent had children under nine, and 64.9 percent believed gaming strengthened parent‑child bonds, especially younger parents. Education correlated with gaming intensity: 63.7 percent of habitual players held secondary or university qualifications. Consoles remained the dominant platform (61.1 percent), favored by men (66.2 percent), while women preferred smartphones (57.6 percent). Approximately 36.2

AEVIDec 2015

Report

Padres y Videojuegos Hoy: España 2014

The research investigates contemporary Spanish parental attitudes toward video gaming, focusing on usage patterns, perceived competence, and consumer behavior during the 2014 holiday season. It reveals that a substantial majority—84 %—of parents actively play video games and consider themselves technologically equal to or more knowledgeable than their children. This confidence translates into a notable educational dimension, with 40 % of parents employing games as learning tools for their offspring. Family interaction emerges as a key driver, as more than half of the surveyed parents have maintained or increased their gaming time after becoming parents, citing shared play as a primary motivator. Economic analysis shows a modest decline in overall holiday spending on games compared with the previous year; however, parents who identify as gamers intend to allocate higher expenditures than non‑gamer parents. Video games rank as the most coveted Christmas gift for half of the children surveyed, with a particular preference for physical console titles. Overall, the findings underscore a robust integration of gaming within Spanish households, highlighting parental confidence, educational utilization, and sustained consumer demand despite slight seasonal spending fluctuations. The study’s scope encompasses Spanish families during the December 2014 period, offering insight into parental influence on market dynamics across both digital and physical gaming segments.

AEVIDec 2014

Report

Dossier de Prensa: España 2014

AEVI was created in 2014 to replace aDeSe and to serve as the unified voice of Spain’s video‑game ecosystem, encompassing publishers, developers, distributors and related agents. Its core mission is to promote domestic industry growth, attract investment, defend intellectual‑property rights and foster a sustainable, responsible market that highlights the sector’s cultural and innovative value. The association now gathers companies that control more than 90 % of the national distribution market, including major global publishers such as Activision‑Blizzard, Nintendo, Sony, Electronic Arts, Ubisoft and Microsoft Iberia, as well as the first development member, Novarama. Industry data indicate that Spain ranks among the top five European and top ten global gaming markets, with 19 million players across all platforms. In 2013 total consumer spending reached €762 million—software €401 million, hardware €275 million and accessories €86 million—despite a 7 % decline in physical sales that nevertheless halved the previous years’ downturn. Adult participation stands at 24 % while 62 % of minors play regularly. Regulatory focus centers on the PEGI self‑rating system, introduced in 2003, and on pending legislative reforms to the Penal Code and Intellectual‑Property Law aimed at curbing piracy, which cost the sector €284 million in 2013 and, if eliminated, could generate roughly 26 600 new jobs. AEVI also promotes major events, notably the second edition of Madrid Games Week in October 2014, positioning the capital as a key venue on the international exhibition circuit and providing a forum for industry debate.

AEVIJan 2014

Report

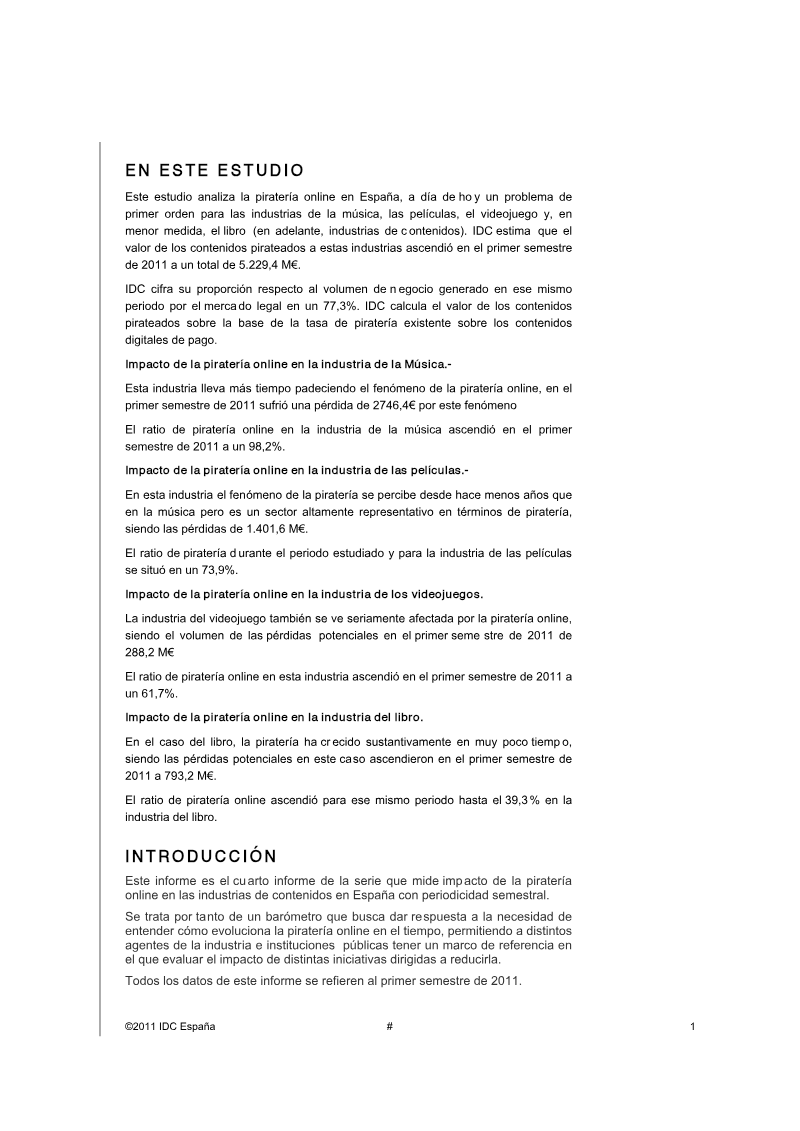

Observatorio de Piratería y Hábitos de Consumo de Contenidos Digitales: Primer Semestre de 2011

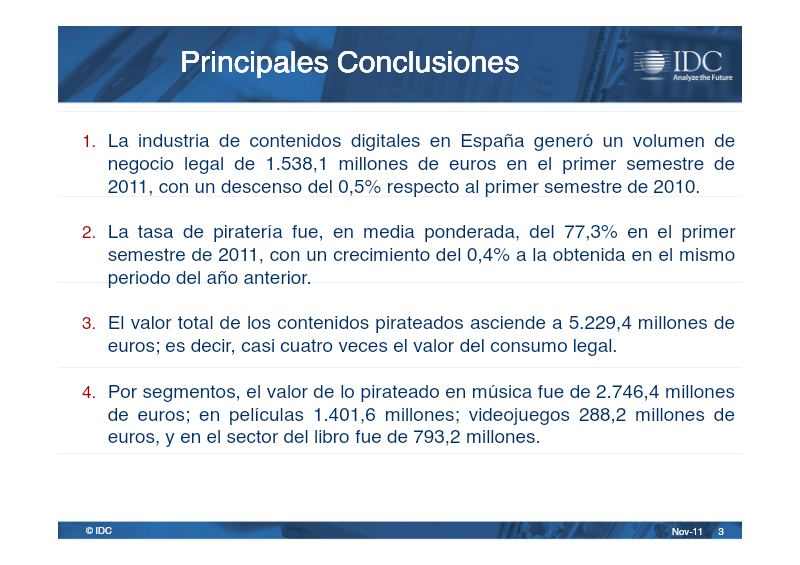

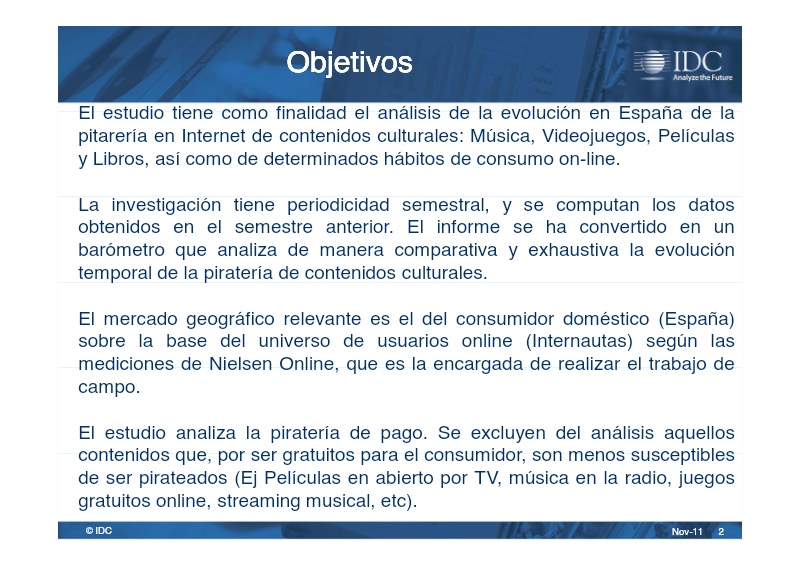

The study evaluates the evolution of online piracy of paid cultural digital content in Spain, focusing on music, video games, films and books during the first half of 2011 and comparing the results with the same period in 2010. By measuring the gap between legal consumption and unauthorized copying, it aims to quantify the scale of the illicit market and track changes in user behavior. Legal sales of digital content generated €1.538 billion, a modest 0.5 % decline from the previous year. The weighted average piracy rate rose to 77.3 %, up 0.4 % year‑on‑year, implying that pirated consumption was valued at €5.229 billion—almost four times the legal market size. Segment‑specific losses were most pronounced in music (€2.746 billion), followed by films (€1.402 billion), books (€0.793 billion) and video games (€0.288 billion). Overall, the legal market base for the analysis stood at €1.561 billion, reflecting a 1.4 % contraction. The research covers the domestic Spanish consumer market, limited to online users aged 16 to 55, and excludes content that is freely available (e.g., broadcast TV, radio, free‑to‑play games, streaming services). Data were collected through a semi‑annual online survey of 3,000 respondents drawn from a panel of 72,000, with quotas ensuring representation by gender and autonomous community. The sample provides a 95 % confidence level with a 1.8 % margin of error, and the online user universe is defined by Nielsen Online measurements. Findings highlight a persistent and growing piracy problem despite a slight dip in legal sales, suggesting significant untapped potential for a legitimate market if effective anti‑piracy measures and alternative business models are introduced.

International Data CorporationNov 2011

Report

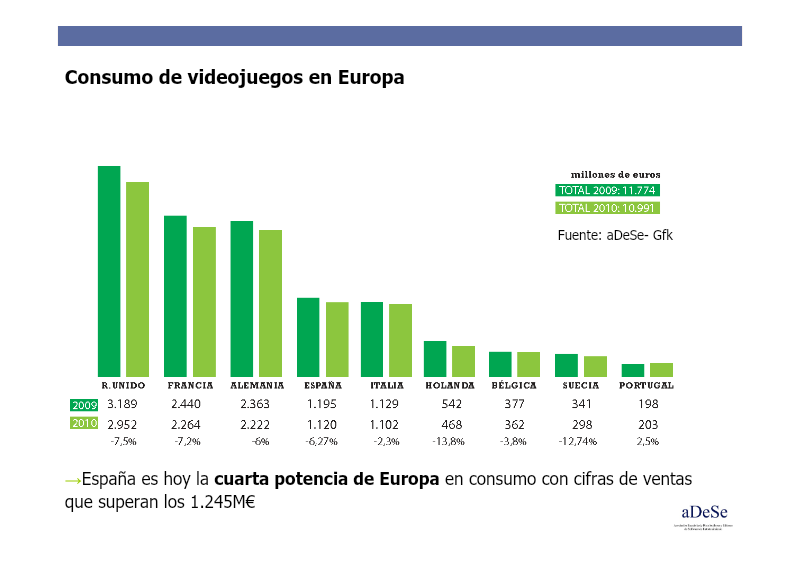

El Videojugador Español: Perfil, Hábitos e Inquietudes de Nuestros Gamers

The study commissioned by the Spanish Association of Distributors and Publishers of Entertainment Software aims to map the profile, habits and concerns of Spanish video‑game players as of 2011, positioning Spain within the broader European market. Spain ranks as the fourth largest European video‑game market, with sales exceeding €1.245 billion in 2010, while the continent records a 25.4 % adult gaming penetration (79.2 million regular players). In Spain, 24 % of adults play regularly, and the most active segment is aged 7‑34, representing 45.3 % of the population. The typical gamer is 32 years old, with women accounting for 40 % of players over 15 years. Over half are married or cohabiting, and 43 % devote between one and five hours per week to gaming. Lifestyle data show that 70 % of gamers frequently engage in outdoor activities such as walking, café visits or restaurant meals, while 61 % exercise regularly. Health awareness is high: 57 % prioritize nutritious food, and 75 % actively practice environmental stewardship through recycling and energy‑saving habits. Values analysis reveals a predominance of hedonistic (≈25 %) and authentic (≈19 %) orientations, followed by social‑rational and aspirational profiles (each around 15 %). Expectations for the next decade are strong: 90 % foresee gaming becoming a universal pastime, with 55‑88 % anticipating virtual‑reality immersion, multisensory experiences and a shift toward educational, medical and professional applications. The research draws on GfK Emer Ad Hoc surveys conducted across Europe in 2009‑2010, combining sales figures, penetration rates and attitudinal questionnaires to deliver a comprehensive portrait of Spanish gamers.

AEVISept 2011

Report

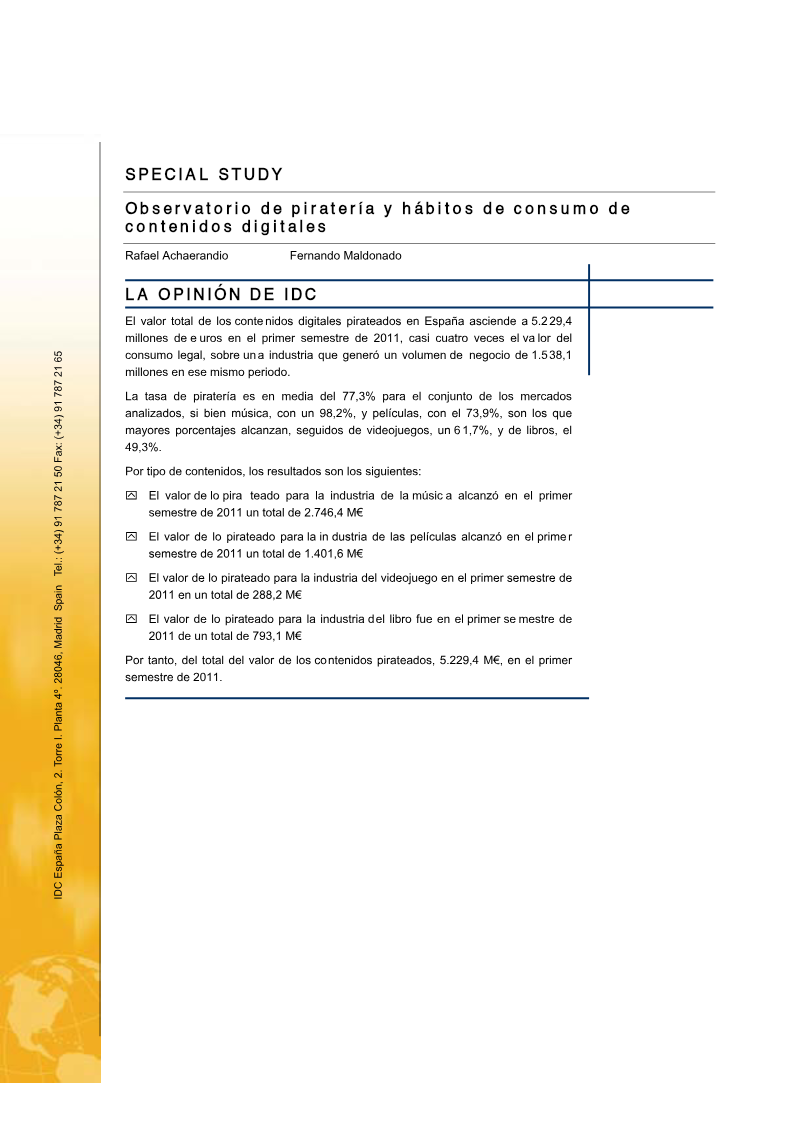

Observatorio de Piratería y Hábitos de Consumo de Contenidos Digitales: España

The study quantifies the scale of digital‑content piracy in Spain during the first half of 2011 and demonstrates that illicit consumption far exceeds legitimate market activity. Pirated material was valued at €5.23 billion, representing roughly 77 % of the legal turnover of €1.54 billion and approaching four times the revenue generated by lawful sales. The incidence of piracy varies markedly across sectors: music reaches a 98.2 % piracy rate amounting to €2.75 billion, films register 73.9 % (€1.40 billion), and video games show 61.7 % of their market value being pirated, with books trailing behind the other categories. The analysis draws on a statistically representative online panel of 3,000 Spanish adults aged 16‑55, balanced by gender (49 % men, 51 % women) and regional distribution. The sample achieves a ±1.8 % margin of error at the 95 % confidence level, with weighting and bias‑correction procedures applied through iterative proportional fitting and adjustments for demographic, capture‑probability, and source‑selection effects. Recruitment employed a multi‑partner random‑digit‑dialing telephone approach, and participants were incentivised to ensure high engagement, providing a robust foundation for assessing consumption and piracy behaviours. Survey instruments captured device penetration, the split between peer‑to‑peer and direct‑download mechanisms, and detailed recall of download and streaming volumes for music, film, video‑games and books on a quarterly or bi‑weekly basis. Findings reveal pervasive use of both P2P networks and direct‑download sites, underscoring the breadth of illegal access across multiple device types. The high piracy ratios, especially in music and film, suggest that traditional revenue models are being undermined, prompting a need for revised industry strategies, stronger enforcement, and alternative distribution frameworks to align consumer habits with sustainable market growth.

IDC EspañaJan 2011

Report

El Futuro del Videojuego: Informe de Resultados (España)

The study set out to explore how Spanish video‑game players envision the medium’s evolution, focusing on genre development, social dimensions, technological advances, and the role of online and mobile gaming. It surveyed internet users aged 14‑44 who play at least once a month, using a quota‑based online questionnaire administered to a nationally representative sample of 332 respondents, with a 95 % confidence level and a 5.2 % margin of error. The sample reflects the regional distribution of Spain and is balanced by gender and three age brackets. Findings show that gaming is as routine as sport or social outings, with 56 % of participants engaging in video games several times a week. Men play more frequently than women (65 % versus 42 % regular play). A striking 90 % anticipate that by 2020 gaming will be ubiquitous across all ages, including grandparents, and 78 % expect it to become highly social, with solitary play becoming rare. Nearly nine out of ten respondents believe most games will be rendered in 3D and that conventional controllers will be replaced by motion‑detecting devices, while older players (35‑44) express the strongest confidence in full‑immersion virtual reality. The most appealing VR scenarios involve traveling to fantastical locations and learning new skills, interests that are especially pronounced among women, whereas men favor sports‑oriented experiences. Respondents also foresee extensive non‑gaming uses for VR, such as surgical simulation, virtual real‑estate tours, e‑commerce, and education from primary to university levels. Regarding online play, 72 % predict increased activity, with men leaning toward competitive environments and women toward social interaction. Parallel trends include a rise in home‑based cinema, social‑media use, and overall digital entertainment.

ADeSeJun 2010

Report

Informe de Resultados: Cómo se proyecta el videojuego del futuro

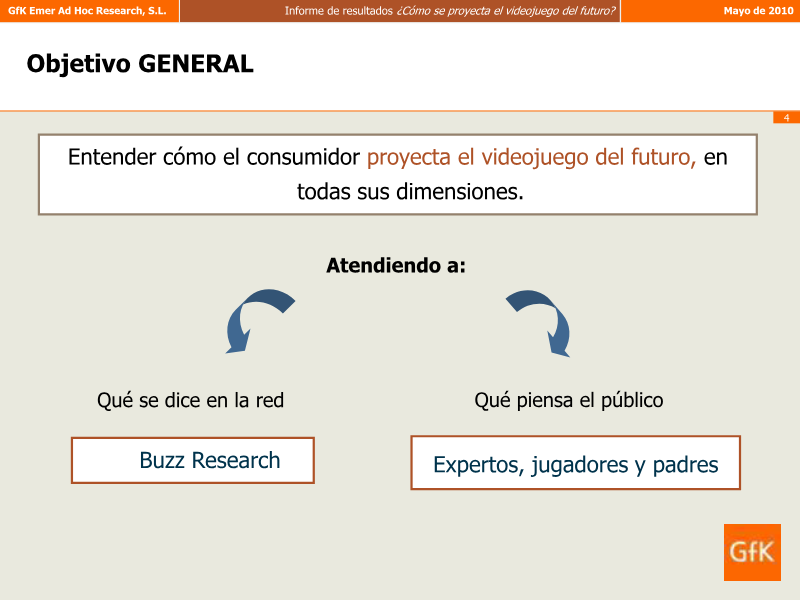

The study, conducted in May 2010, projects the evolution of video‑games through the 2020‑25 horizon, arguing that immersive virtual‑reality experiences will become the dominant technological driver of the sector. By analysing current player demographics, consumption habits and emerging distribution channels, the research maps how the industry will restructure its business models while preserving the fundamental motivations and genre preferences that have long defined gaming. Present‑day online play is still largely the domain of “hardcore” gamers, yet a significant share of moderately hardcore users—53 %—report connection latency as a primary pain point. This dissatisfaction is expected to accelerate the shift toward higher‑bandwidth, low‑latency networks that can support the projected surge in immersive content. The forecast anticipates that roughly 68 % of all game sales will be conducted through virtual stores or server‑based platforms, eliminating the need for physical distribution. Future revenue streams are projected to diversify across several complementary models: periodic free expansions, low‑cost add‑ons priced around three euros, flat‑rate monthly subscriptions that may be tied to specific devices, micro‑transactions, and ad‑supported versions. Despite these commercial innovations, core genres, narrative settings and player motivations are predicted to remain largely stable, with the home environment continuing to serve as the principal venue for play, albeit increasingly complemented by mobile and cloud‑based access points. Overall, the analysis underscores a transition toward fully digital acquisition and consumption, driven by advances in immersive technology and network infrastructure, while the cultural and experiential foundations of gaming persist across the coming decade.

AEVIMay 2010

Report

¿Cómo Se Proyecta el Videojuego del Futuro?: España

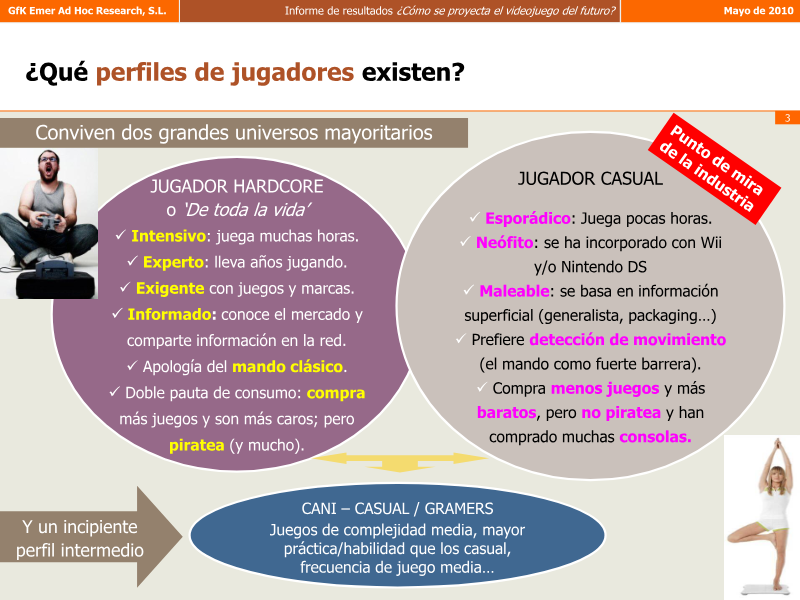

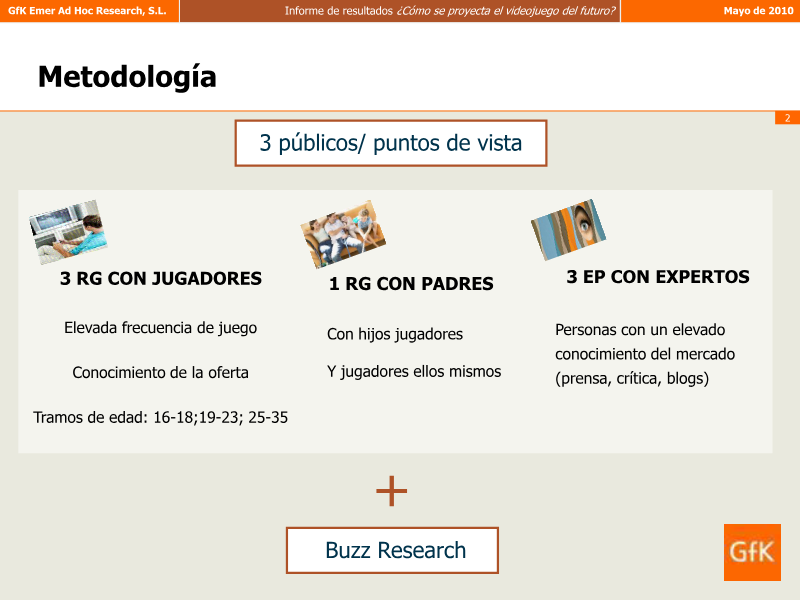

The study commissioned by ADESE explores how video games are expected to evolve, focusing on technological, social and market dynamics and projecting scenarios up to 2025. It seeks to understand current player behaviours, perceived barriers to online play, and the aspirations of different user segments for future gaming experiences. Research combined three perspectives—regular gamers, industry experts and parents—through focus groups organized by Buzz Research. Participants were grouped by age (16‑18, 19‑23 and 25‑35) and by playing profile, distinguishing hardcore players, casual players and an emerging “Cani” segment that blends moderate skill with regular play. Findings reveal that hardcore gamers dominate online activity but still rely heavily on offline play, while casual players show limited interest in online modes due to slow connections, language obstacles, trust issues and unfamiliar payment models. Parents mirror casual attitudes, valuing online interaction mainly for its social companionship. Projected developments for the medium term (around 2015) include cloud‑based distribution, motion‑sensing controls, high‑definition 3D graphics and AI‑driven personalization, with an emphasis on cross‑device compatibility. Long‑term visions (2020‑2025) anticipate immersive virtual‑reality environments, multisensory holographic interfaces, voice‑controlled menus and highly customizable controllers, suggesting a shift toward fully online ecosystems and digital‑only delivery. Experts anticipate that 100 % of future games will be online, driven by anti‑piracy incentives, streamlined matchmaking, enhanced security and ubiquitous broadband. Beyond entertainment, respondents agree that gaming technology will expand into education, senior‑care, professional training and therapeutic applications, leveraging interactive simulations for language learning, psychomotor skill development, conflict resolution and cognitive rehabilitation. The overall outlook combines cautious optimism about technological breakthroughs with recognition of current infrastructural and cultural hurdles that must be addressed for widespread adoption.

AEVIJan 2010

Report

Estudio aDeSe 2009: Usos y Hábitos de los Videojugadores Españoles

The November 2009 aDeSe study set out to map the usage patterns and habits of video‑game players across Spain, providing a statistically robust portrait of the market for stakeholders seeking to understand consumer behavior. A nationally representative sample of 4,254 residents aged fifteen and older was surveyed, delivering results with a ±1.5 % margin of error at the 95 % confidence level. The research encompassed all Spanish households, capturing data on technology ownership, demographic characteristics, and geographic distribution of gamers. Findings reveal that personal computers remain the dominant platform, with 58 % of households reporting PC ownership, while 35 % possess a dedicated video‑gaming console. This indicates a strong convergence between general computing and interactive entertainment within Spanish homes. The demographic profile shows that the majority of active gamers reside in municipalities ranging from ten thousand to fifty thousand inhabitants, a segment that accounts for 26 % of the gaming population, underscoring the importance of medium‑sized towns as key hubs of gaming activity. Overall, the study highlights a mature gaming ecosystem in Spain, characterized by widespread access to PC hardware and a substantial, though smaller, console base. The concentration of players in mid‑size municipalities suggests that market strategies should consider regional nuances, while the high penetration of computing devices points to opportunities for cross‑platform content and services.

AEVINov 2009

Report

Hábitos e Iniciación a los Videojuegos en Mayores de 35 Años: Diciembre de 2008

I’m ready to synthesize the material, but I need the remaining section summaries to produce a complete, accurate overview. Could you please provide the rest of the section-by-section information?

AEVIDec 2008