FinancialKonami Holdings Corporation

Consolidated Financial Results: Three Months Ended June 30, 2021

19 pages~31 min full read

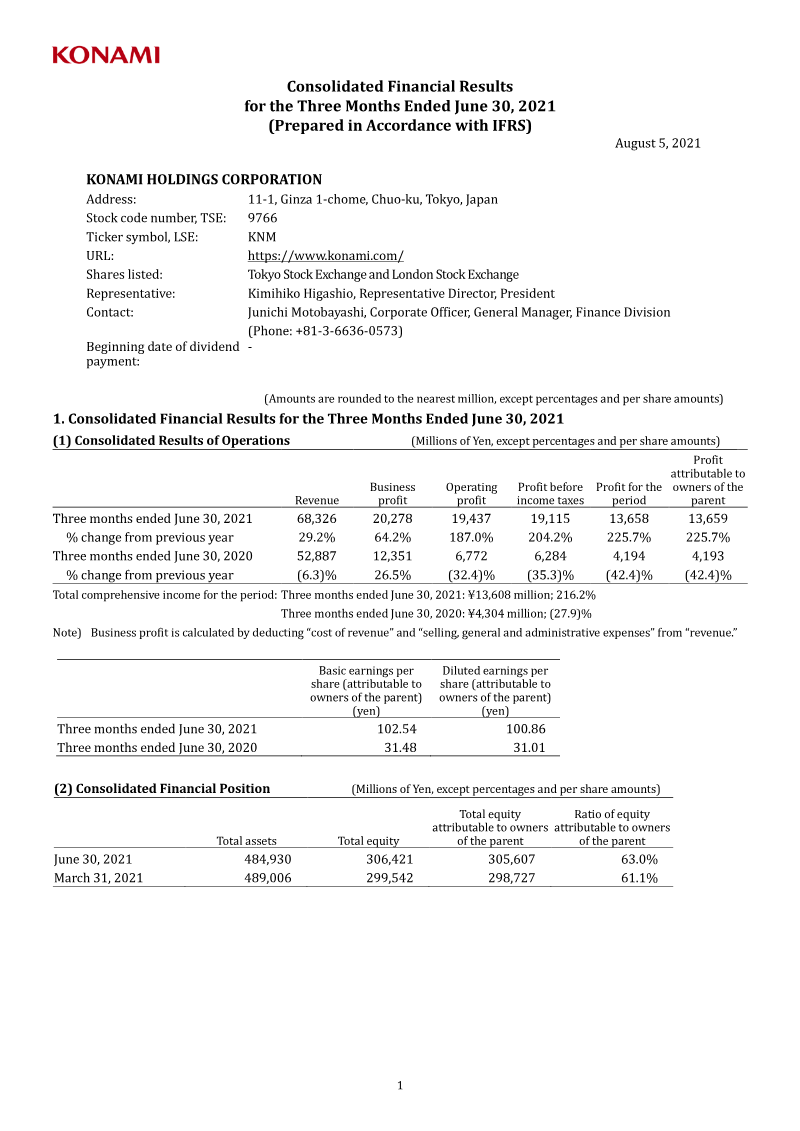

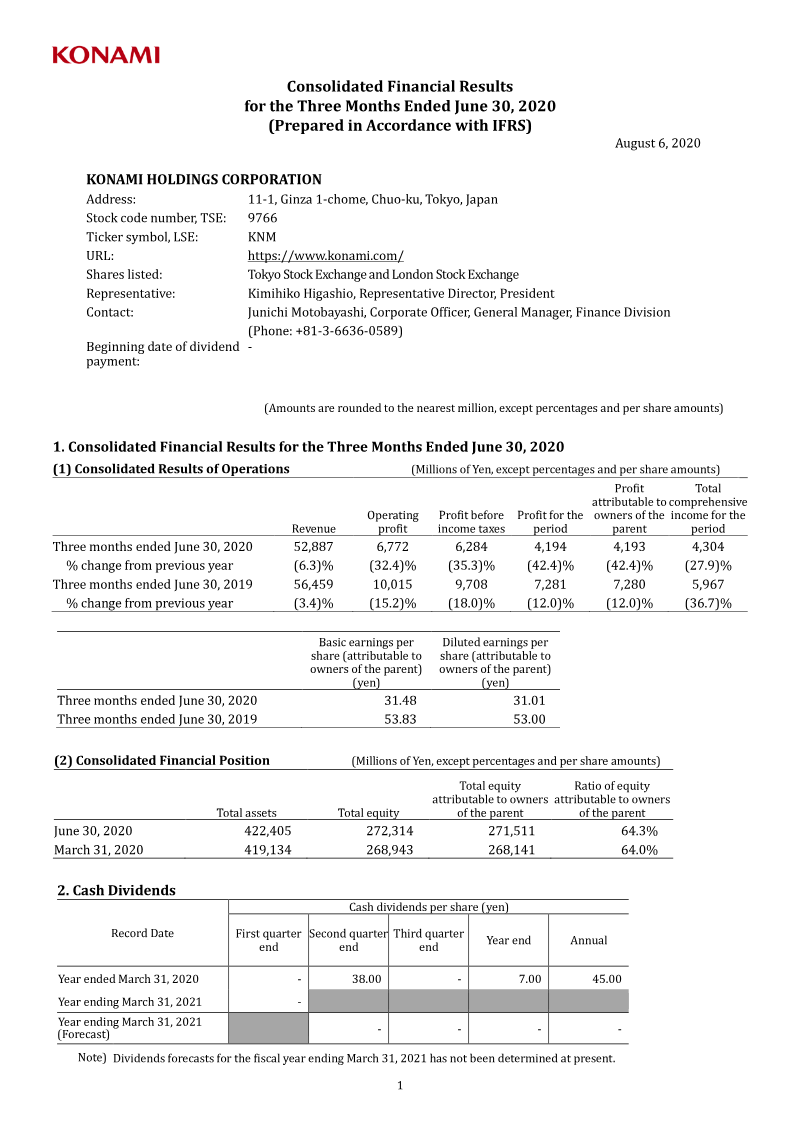

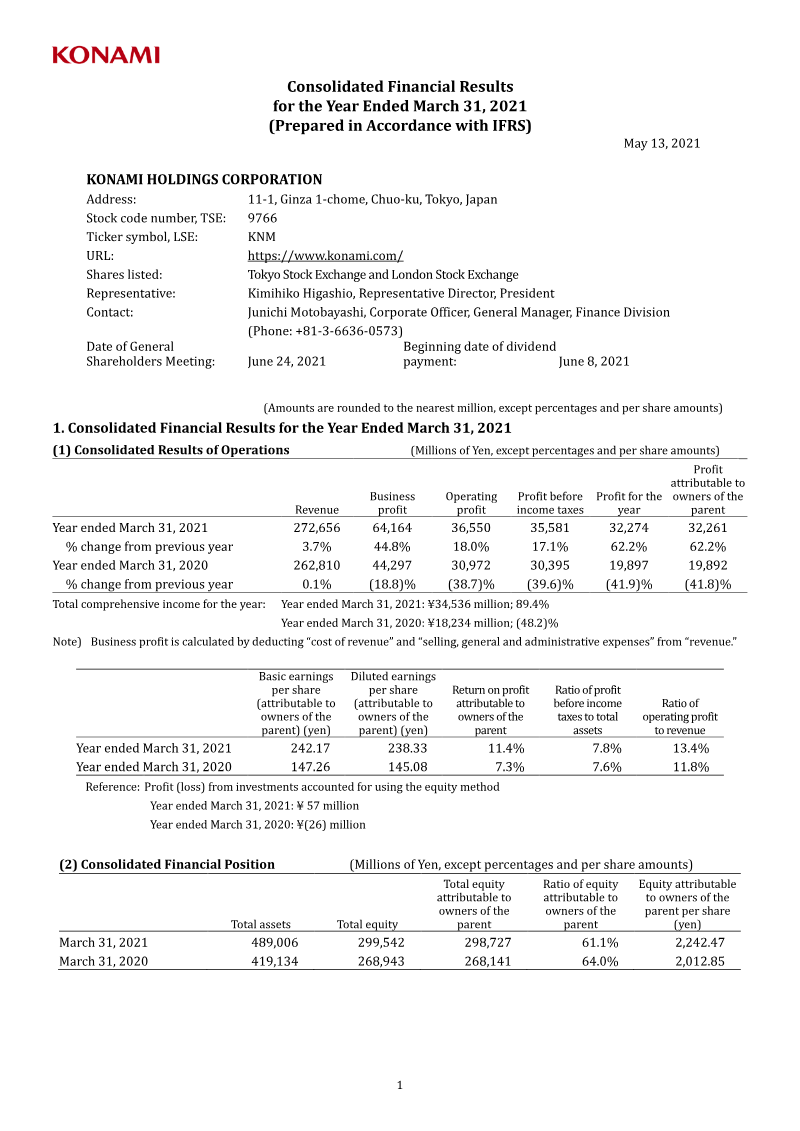

Konami Holdings Corporation achieved record-high financial results for the first quarter of the fiscal year ending March 31, 2022, signaling a robust recovery across its global operations. Consolidated revenue reached ¥68,326 million, representing a 29.2% increase compared to the same period in the previous year. Profitability saw a dramatic surge, with profit before income taxes climbing to ¥19,115 million from ¥6,284 million, while net profit rose to ¥13,658 million. This performance underscores a successful rebound from the prior year’s economic challenges, supported by a significant reduction in pandemic-related losses, which dropped from ¥5,723 million to ¥862 million.

The growth was driven by strong performance in the Digital Entertainment segment alongside a broad-based recovery in the Amusement, Gaming & Systems, and Sports divisions. These segments collectively returned to profitability, benefiting from ongoing structural cost reforms and the expansion of digital entertainment offerings and sports facility operations. By diversifying its revenue streams and optimizing operational efficiency, the organization effectively mitigated the volatility that characterized the previous fiscal period.

Despite these positive indicators, the company maintains a cautious outlook for the remainder of the fiscal year. Due to the persistent uncertainty surrounding the global trajectory of the COVID-19 pandemic, management has refrained from issuing a consolidated earnings forecast for the full fiscal year ending March 31, 2022. This conservative stance reflects a commitment to navigating potential market fluctuations while continuing to prioritize long-term stability and strategic growth across all business segments.

Konami Holdings Corporation

Konami Holdings Corporation

Konami Holdings Corporation

Konami Holdings Corporation

Konami Holdings Corporation

Sony Group Corporation · 2026

Bandai Namco · 2026

InvestGame · 2025

Square Enix · 2025

Konami · 2025

Nintendo · 2024

Bandai Namco · 2022

Bandai Namco · 2021

GREE · 2017

Bandai Namco · 2017

GREE Inc. · 2016

Bandai Namco · 2014