Related Documents

Report

Rise of the Player-Fan: The Growing Opportunity of Mobile Esports in Asia

Mobile esports has emerged as a primary driver of player engagement and revenue across Asia, signaling a shift from traditional PC and console dominance to a mobile-first competitive landscape. The central thesis posits that Asia is the global epicenter of this evolution, fueled by a massive population of 1.5 billion gamers and a robust infrastructure of internet cafes, local streaming platforms, and increasing 5G penetration. By lowering hardware barriers to entry, mobile technology has transformed casual players into "player-fans" who both compete in and spectate high-stakes tournaments. Key data points highlight the scale of this growth, with global esports prize pools increasing 40% between 2017 and 2019 to exceed $228 million. In 2019 alone, mobile esports generated $19.5 billion in global revenue, with Asia accounting for 68% of that total. China remains the largest single market, boasting 350 million esports fans, while Southeast Asia saw a 244% increase in tournament prize values between 2018 and 2019. The COVID-19 pandemic further accelerated these trends, with gamers in Asia spending up to 75% more time playing and viewership in China doubling during lockdowns. The scope of this analysis covers major Asian markets including China, South Korea, Japan, India, and Southeast Asia, focusing on the period between 2017 and 2020. It examines industry segments ranging from hardware manufacturing and 5G infrastructure to specific game genres like MOBAs and Battle Royales. Methodology relies on primary data from Niko Partners, including consumer panels of over four million users, executive interviews, and market modeling to provide a comprehensive outlook on the region's competitive gaming trajectory.

Niko PartnersJul 2020

Report

Level Up: A Guide to Succeed in Asia’s Gaming Market

Asia has established itself as the epicenter of the global gaming industry, driven by a mobile-first population exceeding 1.5 billion players. The region’s market is characterized by the dominance of free-to-play models, which account for nearly 99% of mobile revenue and all top-grossing titles. While China and Japan lead in total revenue, Japan maintains the highest value per user with an average revenue per download of $12.84. Growth is increasingly fueled by the female demographic, which expanded to 500 million players by 2019 and contributes nearly 40% of total mobile gaming revenue. This shift necessitates more inclusive storylines and diverse development teams to capture a demographic that is currently outgrowing its male counterpart. The competitive landscape is defined by the rapid ascent of mobile esports, with Asia generating 68% of the sector's global revenue. Southeast Asia, in particular, has seen a 244% increase in tournament prize pools, signaling a transition from casual play toward complex, competitive genres like MOBAs and Battle Royales. Despite high interest, a significant gap remains between esports viewership and active participation, representing a massive untapped opportunity for developers. Success in these markets requires sophisticated monetization strategies, such as hybrid models combining gacha mechanics, battle passes, and rewarded video ads to accommodate varying income levels across the territory. Navigating the Asian market demands deep localization that extends beyond language to include cultural customs, religious sensitivities, and technical optimization for diverse hardware. While Japan and South Korea remain dominated by local developers and legacy RPG franchises, India and Southeast Asia offer high-growth potential for international titles that provide "lite" versions for accessible play. To achieve long-term engagement, developers must leverage local influencers and community-driven gameplay, ensuring that titles resonate with the specific pop culture trends and infrastructure capabilities of each unique sub-region.

NewzooJan 2020

Report

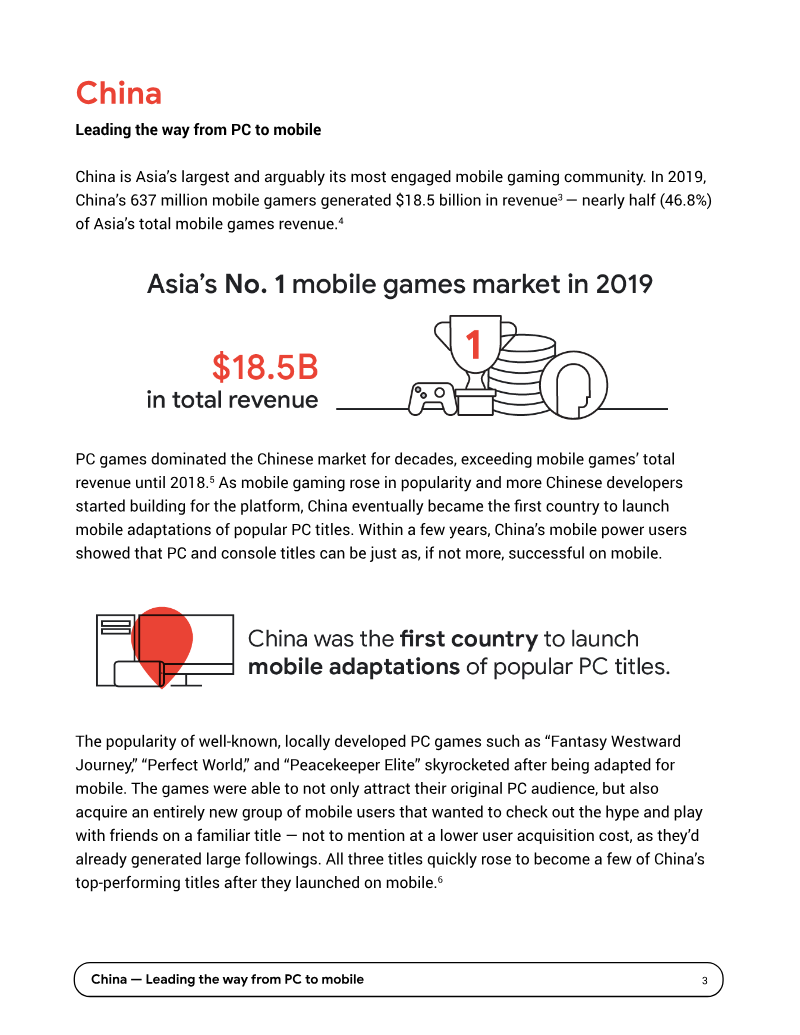

For the Win: Breaking Down the Preferences of Asia's Mobile Gamers

Asia represents the world’s most significant mobile gaming hub, housing over half of the global player base and generating the majority of the industry's mobile revenue. The primary objective of this analysis is to examine the distinct player preferences, cultural influences, and market regulations across five key regions: China, Japan, South Korea, India, and Southeast Asia. By evaluating top-grossing titles and genre shifts through the first half of 2020, the findings illustrate a broader regional transition from casual play toward complex, competitive, and socially-driven experiences. China remains the largest market, characterized by the successful migration of PC intellectual properties to mobile and a regulatory environment that necessitates domestic partnerships. In contrast, Japan’s market is defined by a deep-rooted console history and the pervasive influence of anime and manga aesthetics, with RPGs accounting for nearly half of its mobile revenue. South Korea leverages its robust 5G infrastructure and "PC bang" culture to sustain a market dominated by high-fidelity MMORPGs. Meanwhile, India and Southeast Asia emerge as high-growth regions where young populations and increasing smartphone accessibility are fueling a massive surge in mobile esports and battle royale titles. The data reveals that localization involves more than translation; it requires integrating local folklore, respecting religious customs, and optimizing for hardware constraints. For instance, "lite" versions of games are essential for market penetration in India, while community-centric features are vital for success in Southeast Asia. Across all regions, the rise of mobile esports is a dominant trend, with competitive titles increasingly displacing traditional genres in the top-grossing charts. The methodology utilizes data from Niko Partners, incorporating market models, five-year forecasts, and qualitative surveys from a panel of millions of consumers across Asia. The analysis covers the period from 2016 through June 2020, drawing on data from retailers, app markets, and interviews with industry executives to provide a comprehensive view of the mobile landscape.

Niko PartnersJan 2020

Report

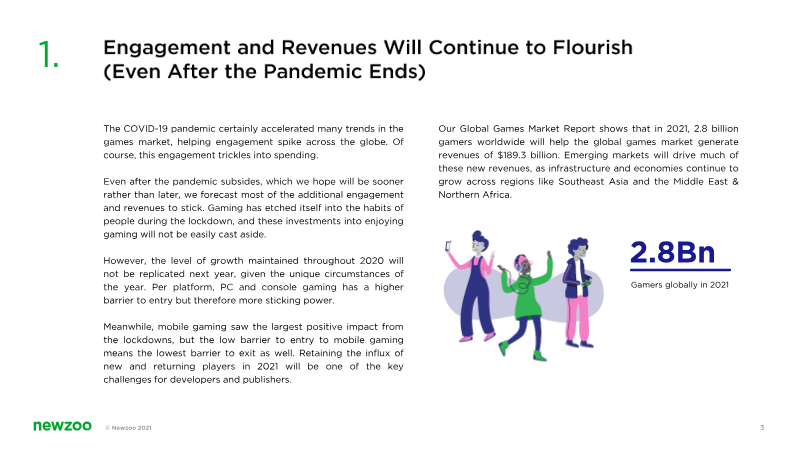

Newzoo’s Global Games Market Report 2021

This analysis explores the trajectory of the global games, esports, and mobile markets for 2021, forecasting a year of sustained engagement despite the easing of pandemic-related lockdowns. The primary thesis suggests that while the explosive growth of 2020 will normalize, gaming habits have become deeply ingrained, positioning the global market to reach 2.8 billion players and $189.3 billion in revenue. Growth is expected to be particularly robust in emerging markets such as Southeast Asia and the Middle East. Key findings highlight a significant shift toward platform agnosticism and the "metaverse." Cloud gaming is projected to surpass $1 billion in annual revenue for the first time, driven by high-fidelity experiences like Cyberpunk 2077 that bypass expensive hardware requirements. Simultaneously, games are evolving into social platforms for non-gaming events, exemplified by virtual concerts in Fortnite and Roblox. In the hardware sector, supply chain disruptions will continue to limit next-generation console availability, while AAA software delays are expected as the long-term impacts of remote development manifest. The mobile segment faces a pivotal transition due to Apple’s removal of the Identifier for Advertisers (IDFA), which is expected to disrupt traditional user acquisition and push publishers toward IP-based games and creative marketing. Despite these hurdles, 5G penetration is set to triple, with 16% of active smartphones becoming 5G-ready by year-end. Additionally, Chinese developers are increasingly exporting high-budget, immersive mobile experiences like Genshin Impact to Western markets. In the esports and streaming sectors, mobile titles are beginning to outperform traditional PC giants in viewership. Organizations are diversifying into lifestyle brands and content-creator collectives to mitigate risk. Furthermore, the industry is placing a heightened focus on social responsibility, with major stakeholders collaborating to reduce toxicity and improve diversity and inclusion in response to growing consumer demand for representative content.

NewzooJan 2021