LegalKadokawa Corporation

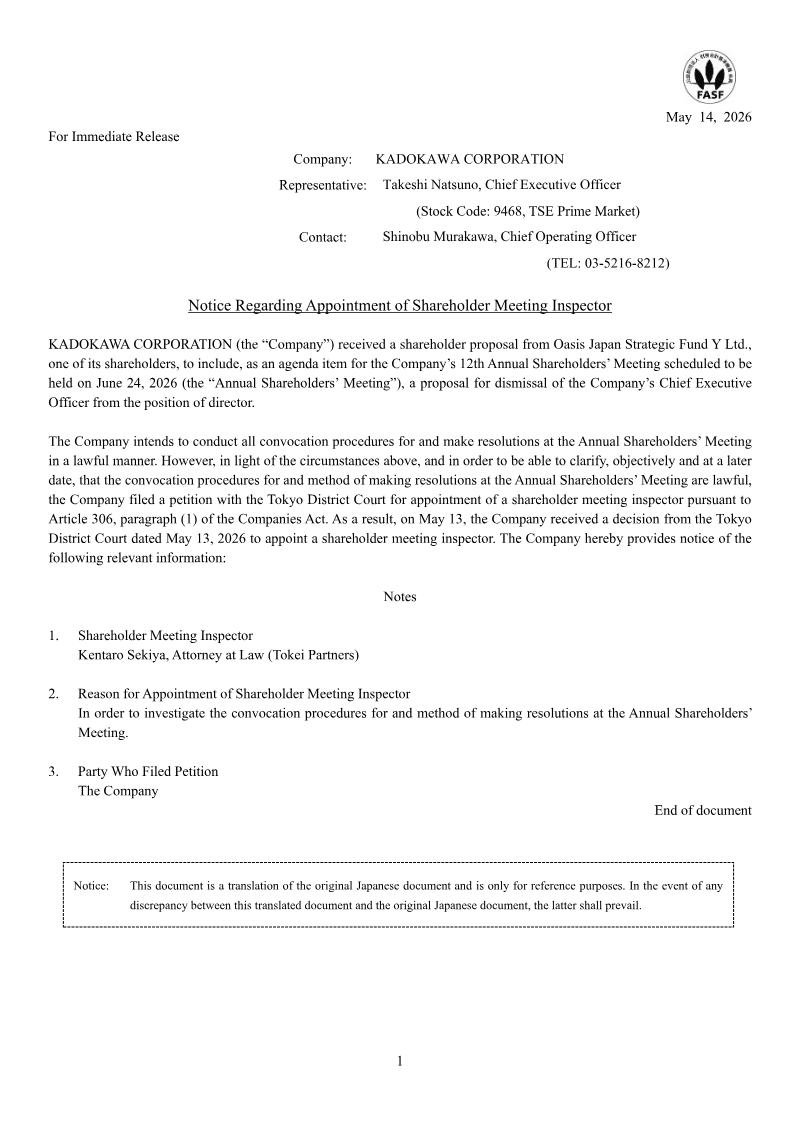

Notice Regarding Appointment of Shareholder Meeting Inspector

1 pages~2 min full read

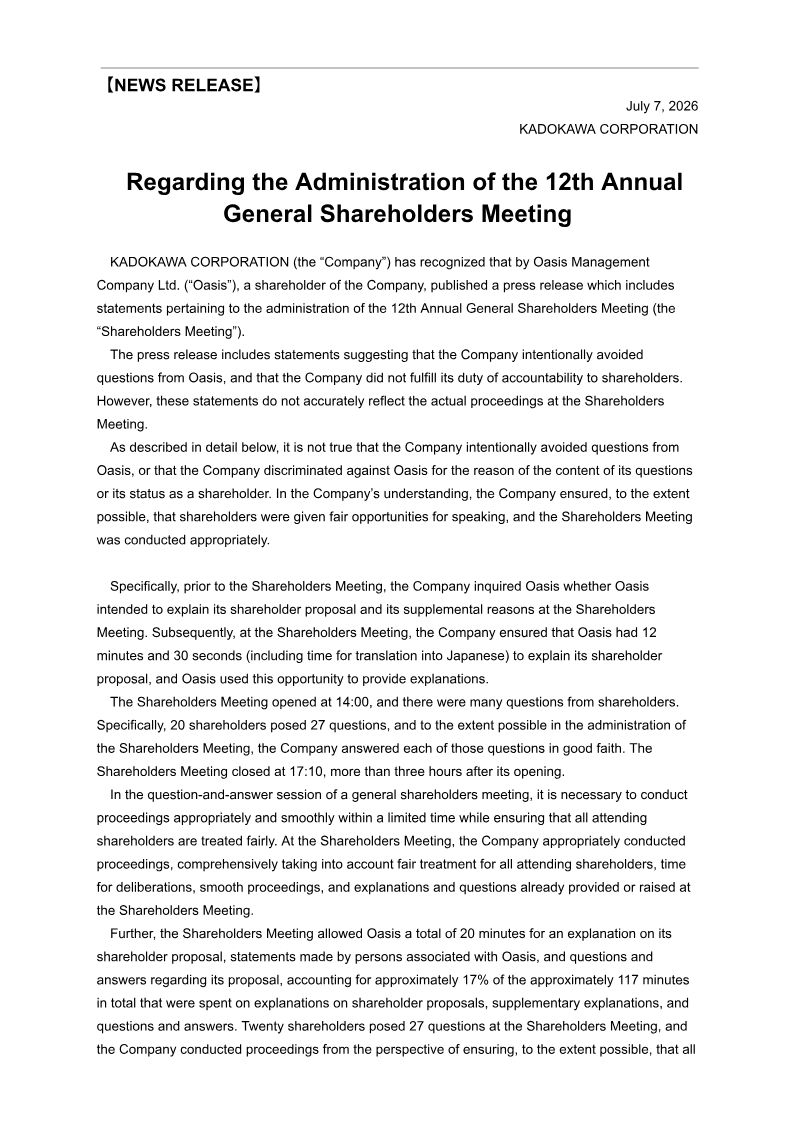

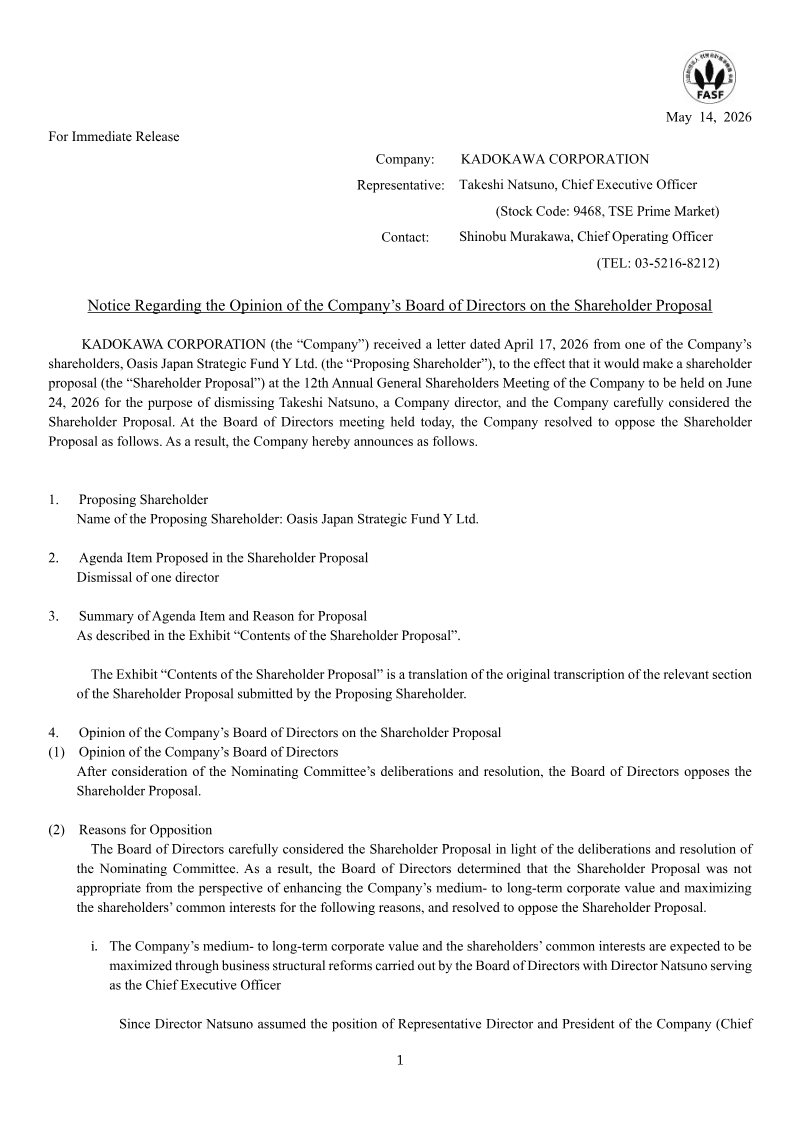

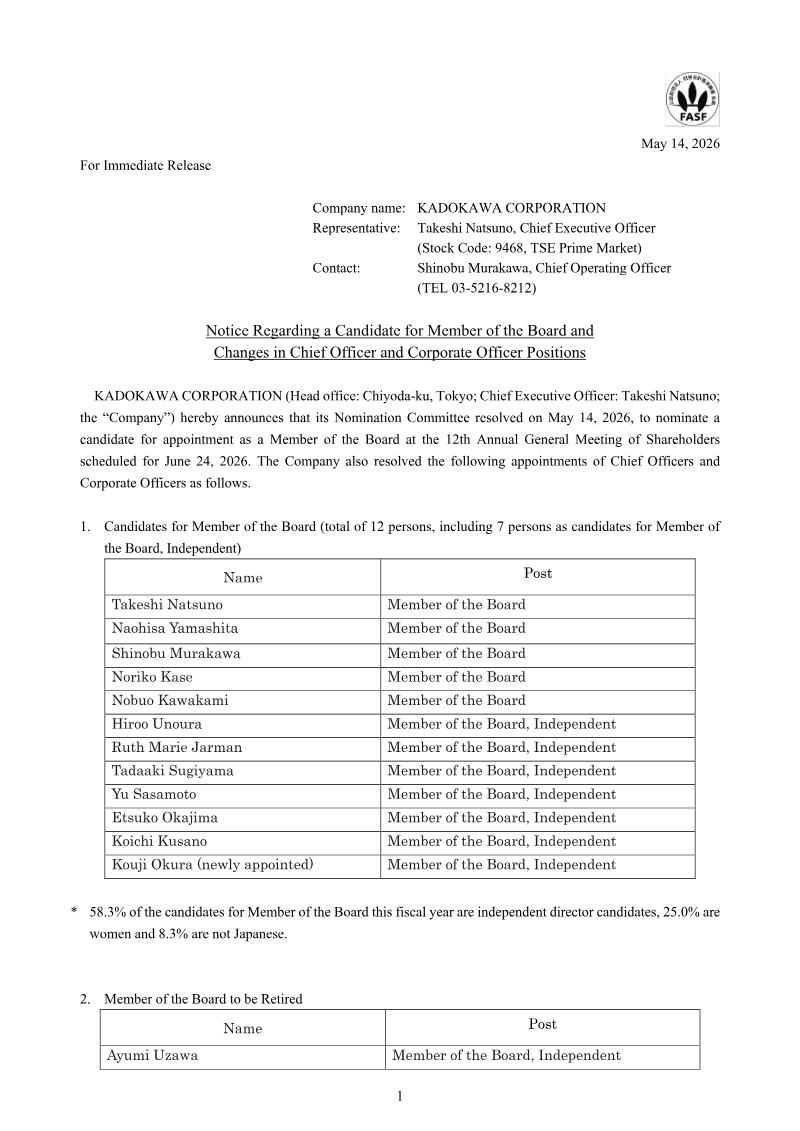

Kadokawa Corporation announced that it has secured a shareholder meeting inspector for its 12th Annual Shareholders’ Meeting scheduled on June 24, 2026. The appointment follows a shareholder proposal from Oasis Japan Strategic Fund Y Ltd., which seeks the dismissal of CEO Takeshi Natsuno from his directorial role. To ensure that all convocation procedures and resolution methods comply with legal requirements, Kadokawa petitioned the Tokyo District Court under Article 306(1) of the Companies Act. The court granted the petition on May 13, 2026, appointing Kentaro Sekiya of Tokei Partners as the inspector. The company’s rationale for this appointment is to investigate and confirm the legality of its meeting procedures, thereby safeguarding shareholder rights and maintaining corporate governance standards. The notice confirms that the inspector’s role is purely procedural, with no implication of misconduct by Kadokawa. The company remains committed to conducting the meeting in a lawful manner and will provide further updates as necessary.

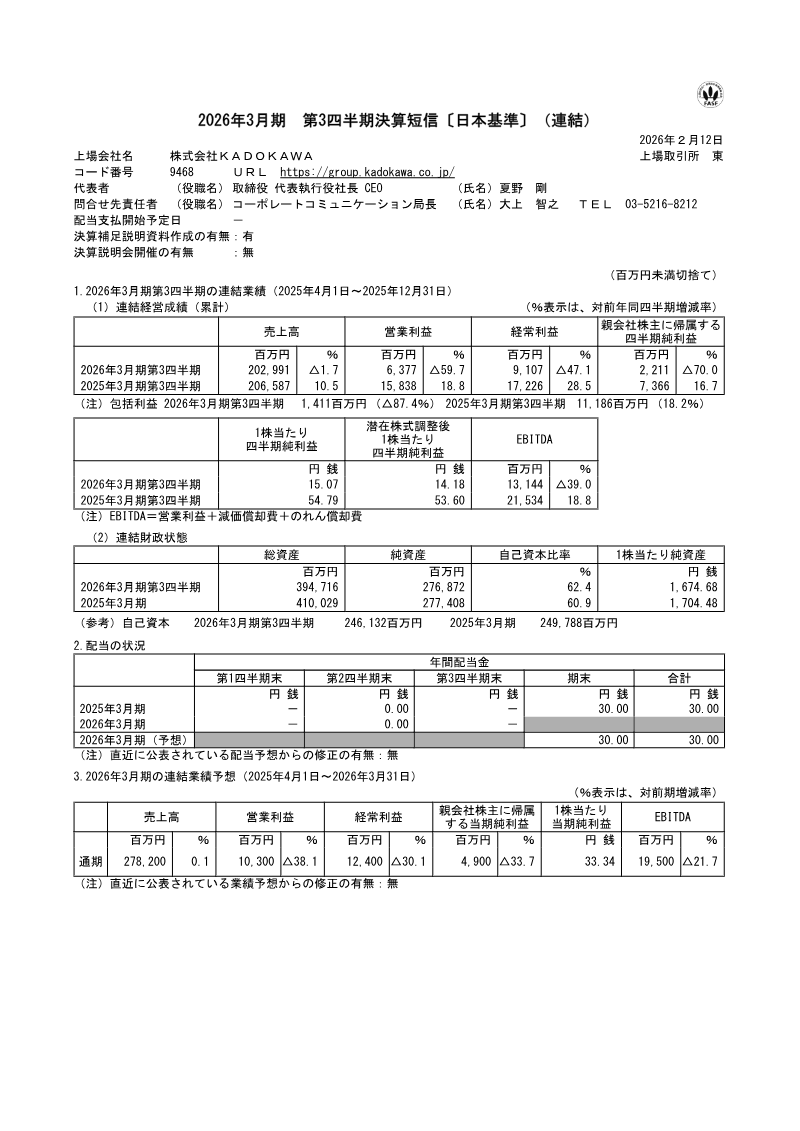

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

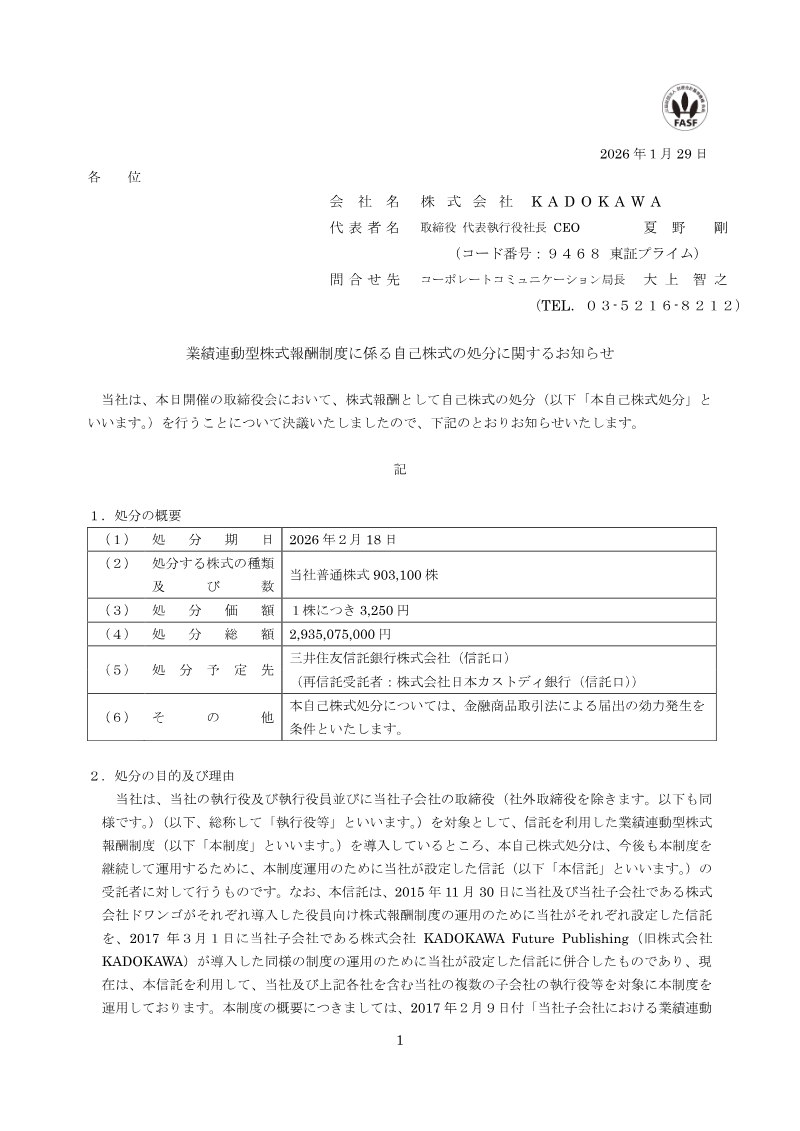

Kadokawa Corporation

Kadokawa Corporation

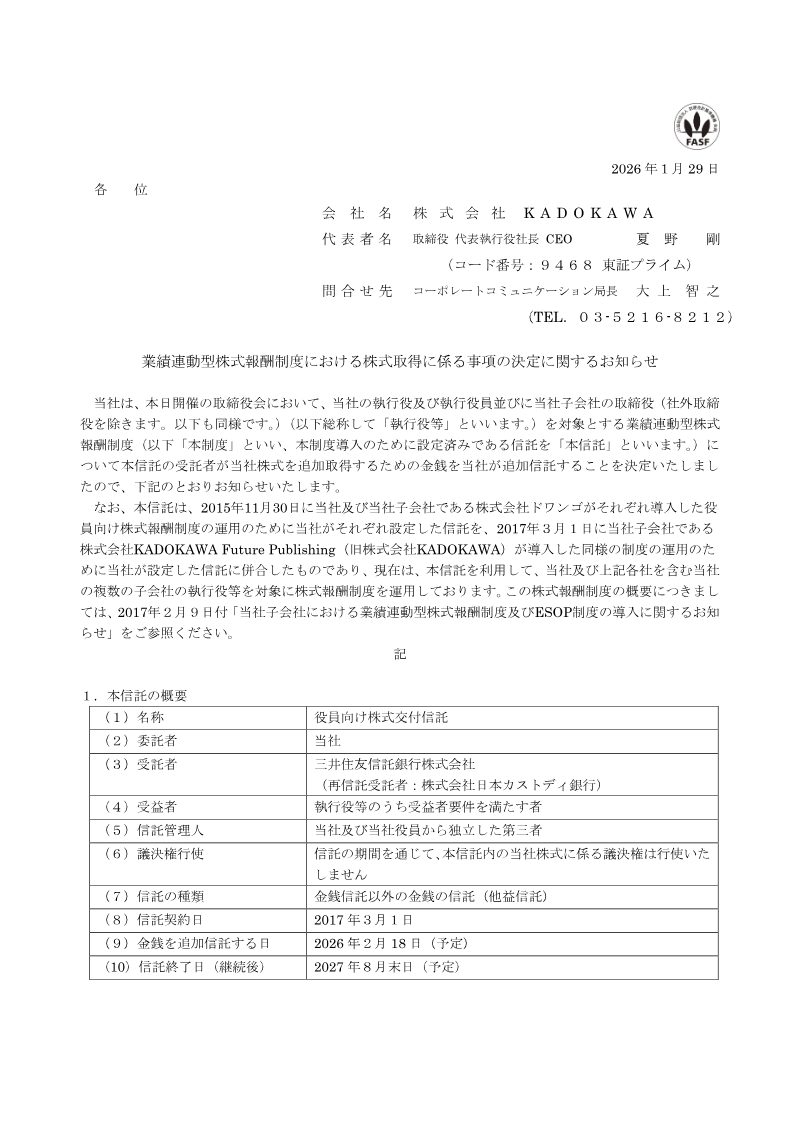

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Capcom · 2026

Capcom Co. · 2026

Capcom · 2026

Sony Group Corporation · 2026

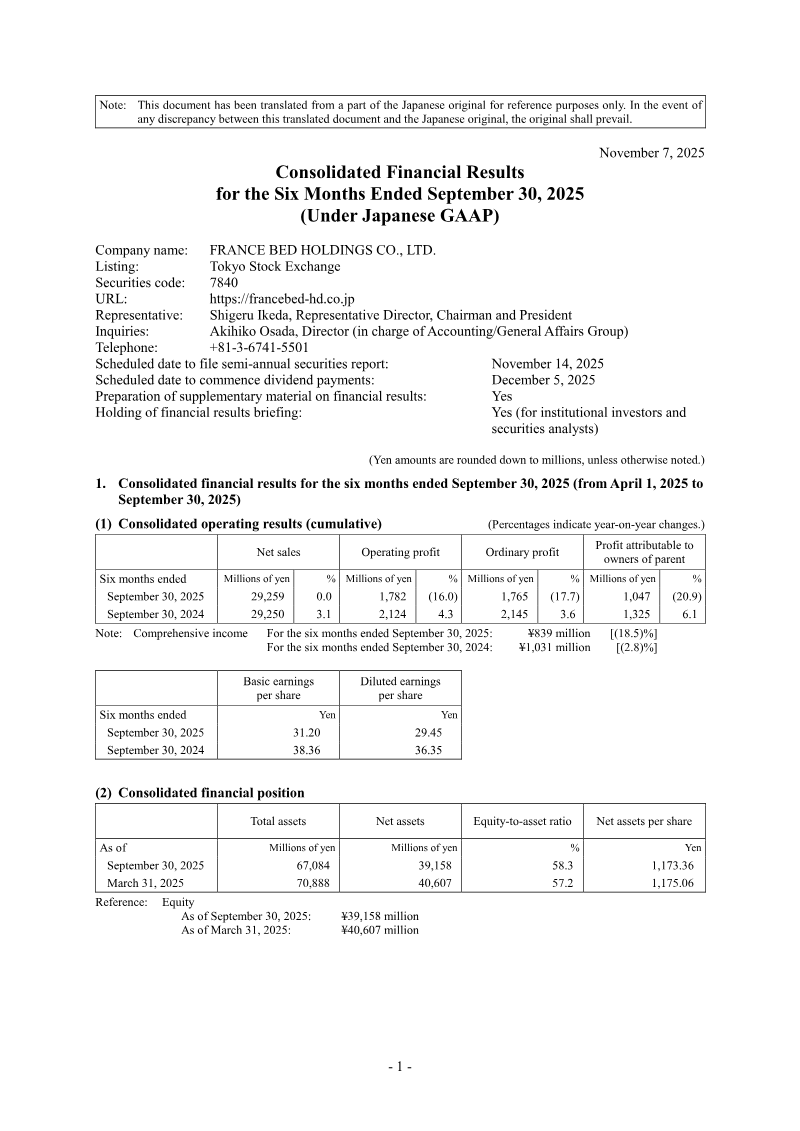

FRANCE BED HOLDINGS CO. · 2026

Square Enix · 2026

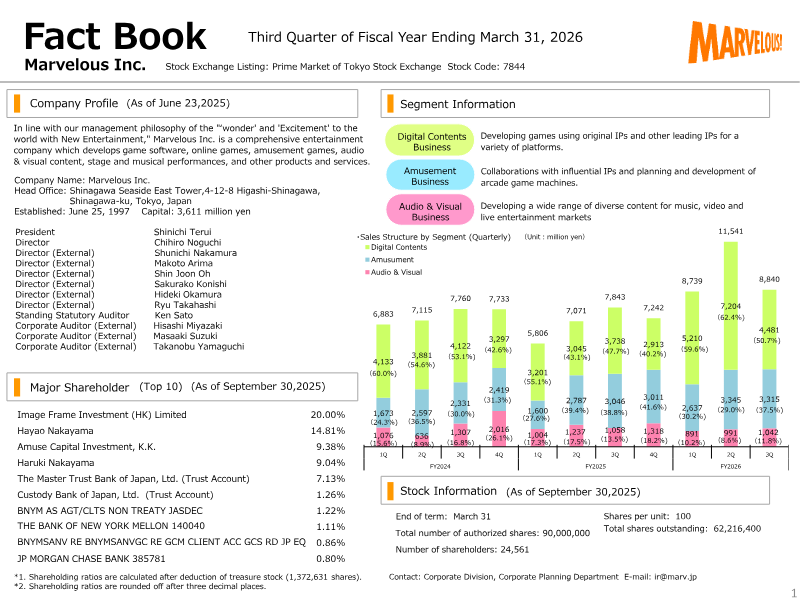

Marvelous · 2026

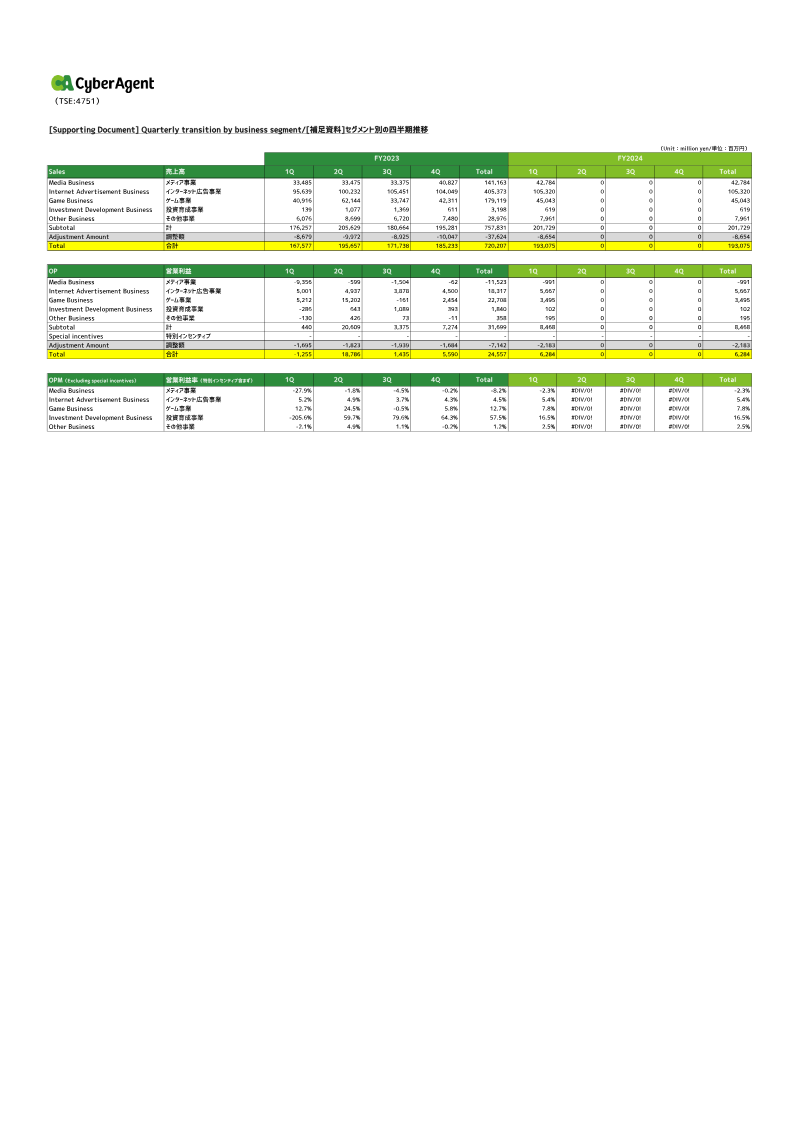

CyberAgent · 2026

Nippon Ichi Software · 2026

Square Enix · 2026

GungHo Online Entertainment · 2026

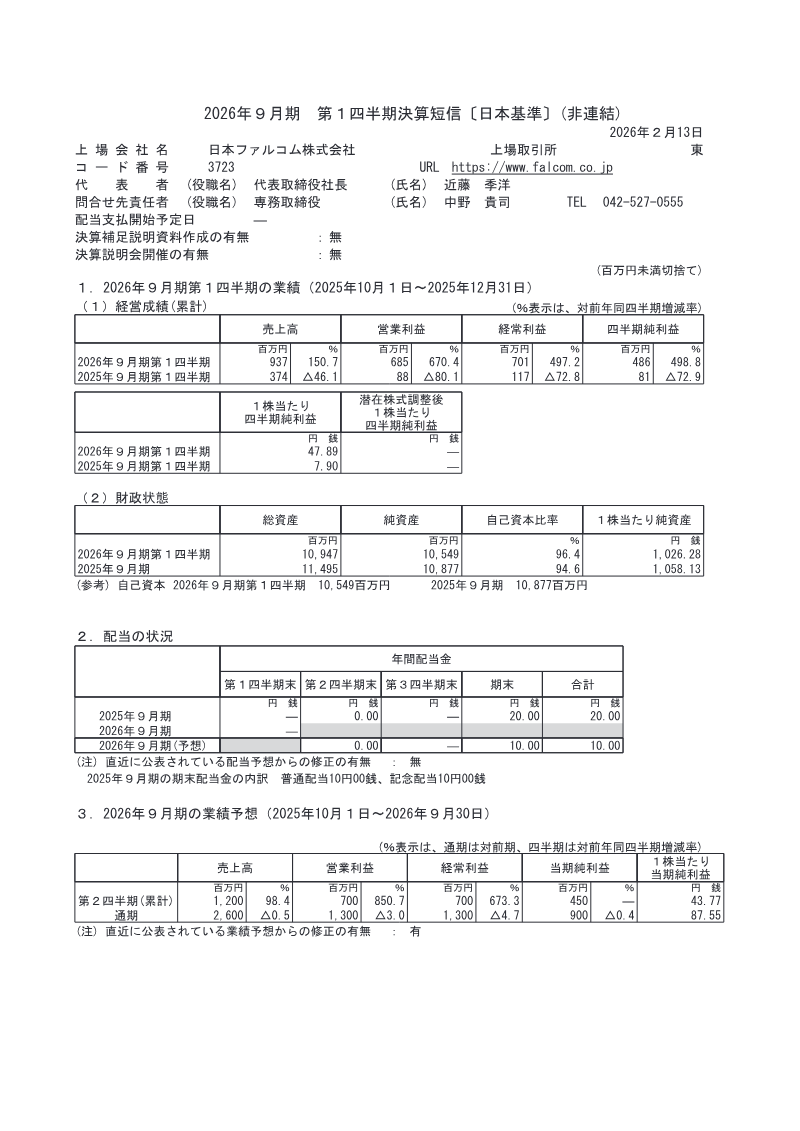

Nihon Falcom Corporation · 2026