LegalKadokawa Corporation

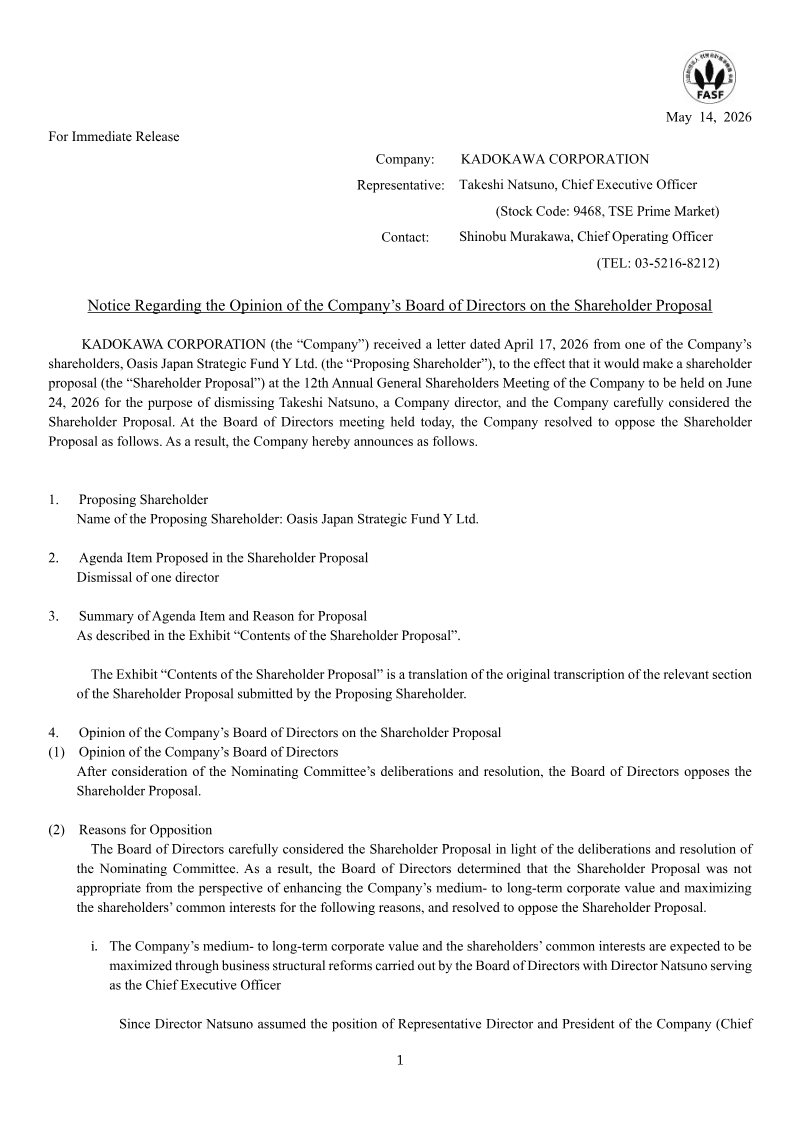

Notice Regarding the Opinion of the Company’s Board of Directors on the Shareholder Proposal

5 pages~14 min full read

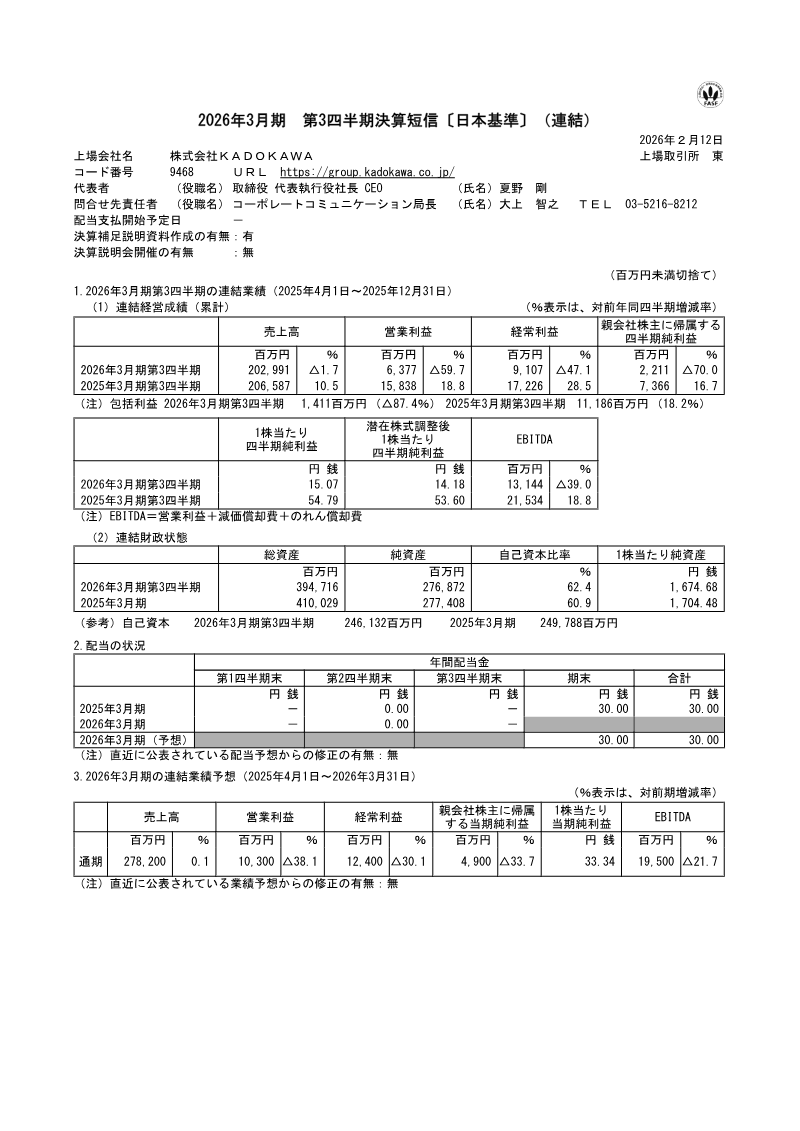

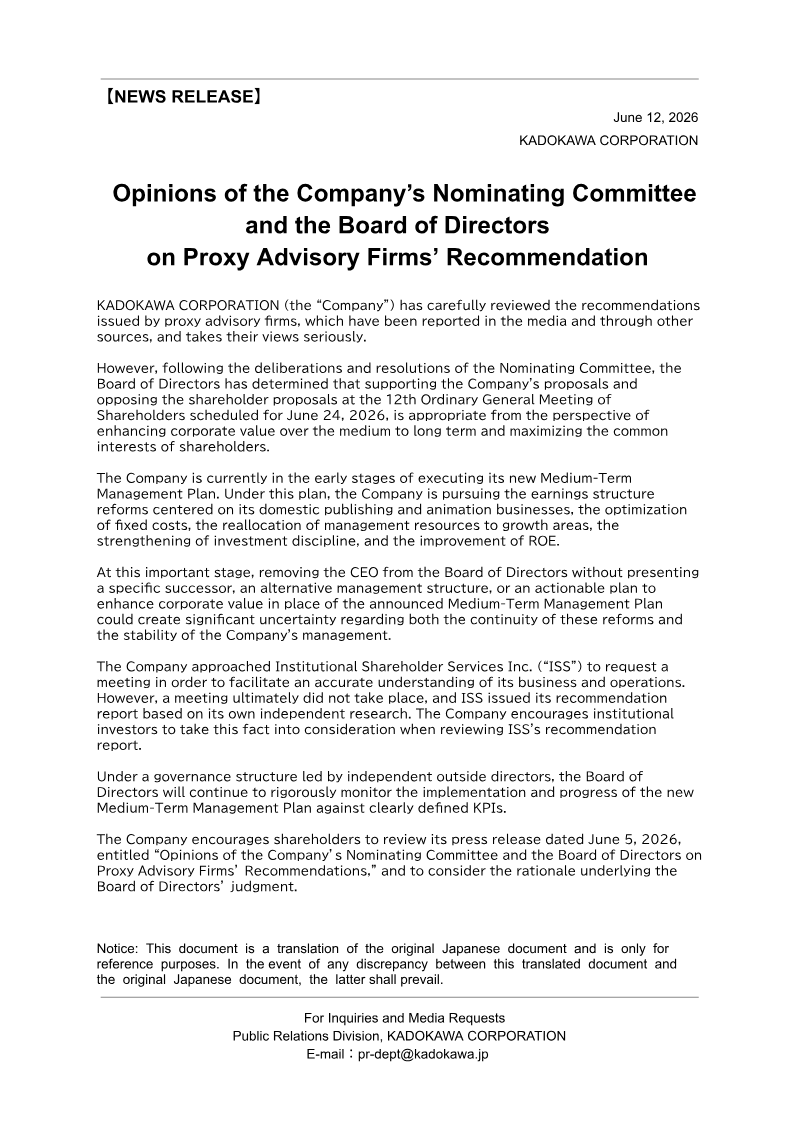

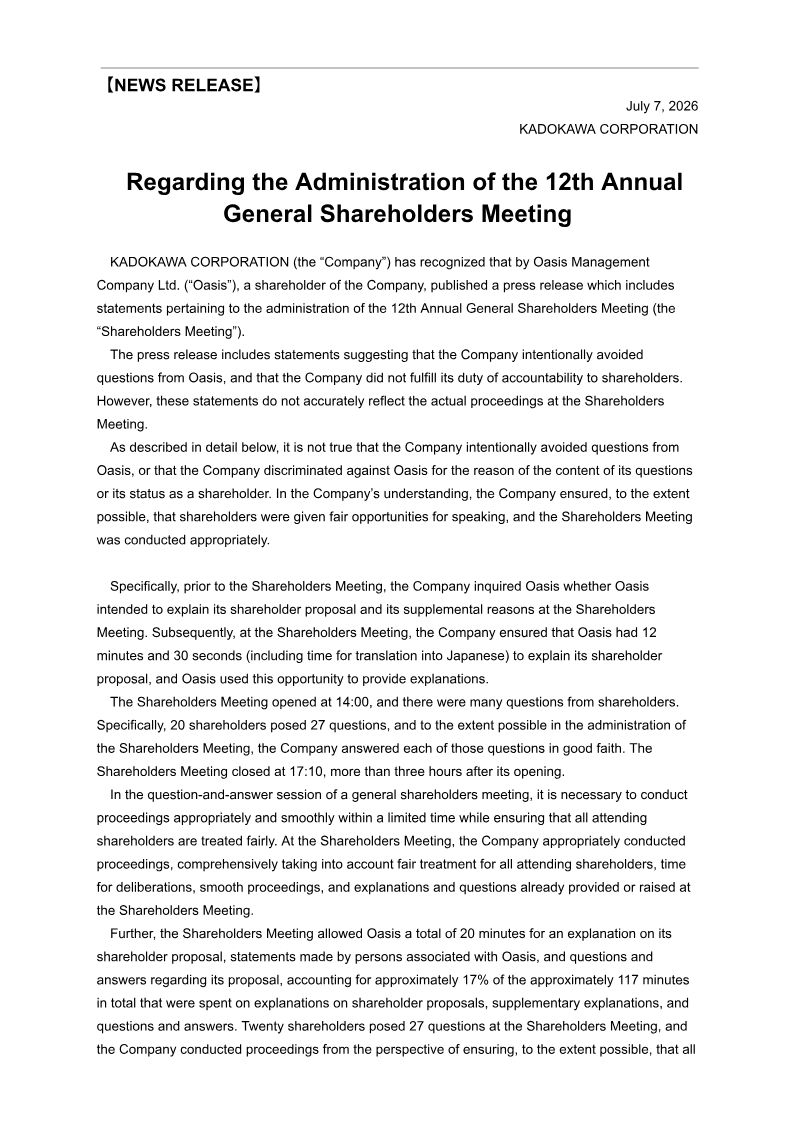

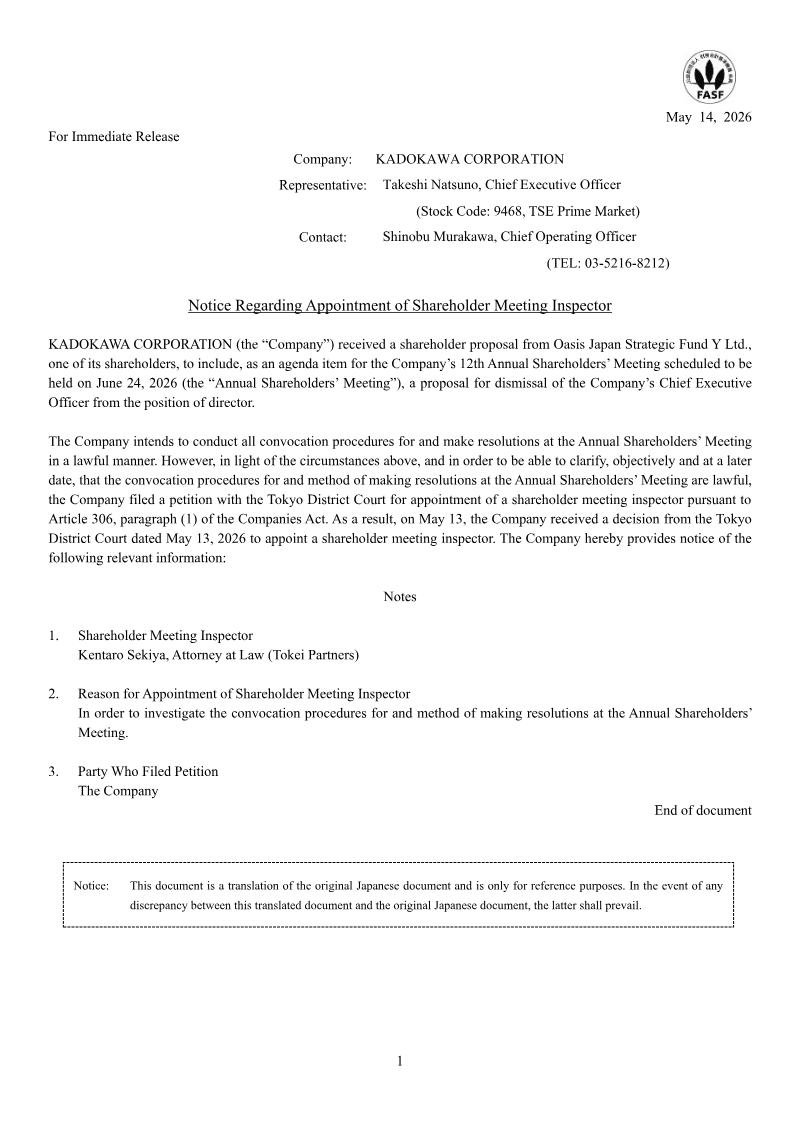

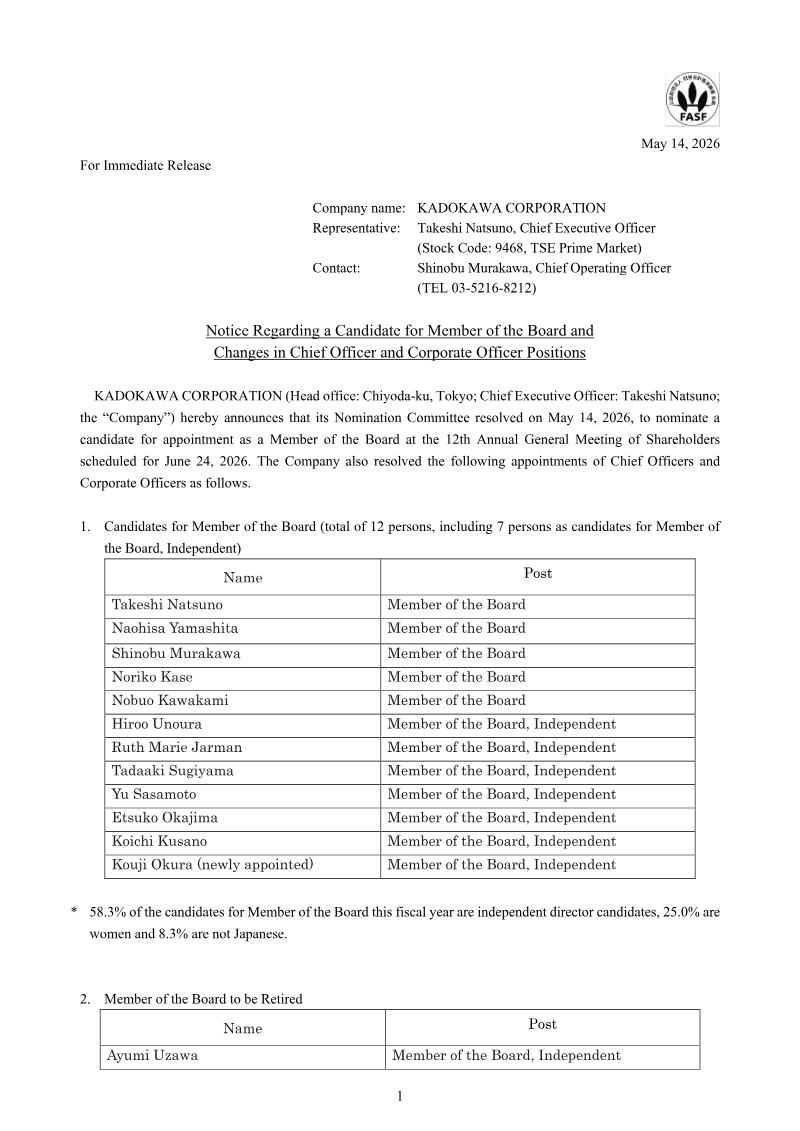

Kadokawa Corporation’s board issued a formal opposition to a shareholder proposal submitted by Oasis Japan Strategic Fund Y Ltd. The proposal, slated for the June 24, 2026 annual meeting, called for the dismissal of CEO and director Takeshi Natsuno. The board’s response, released May 14, 2026, outlines three principal arguments against the proposal. First, it asserts that Natsuno’s leadership has driven a “Global Media Mix with Technology” strategy that has expanded the company’s intellectual‑property portfolio, increased overseas sales, and set ambitious mid‑term targets (FY 2026–2031) of ¥400 billion in sales and 9.4 % ROE, positioning the company for long‑term value creation. Second, the board highlights Natsuno’s role in strengthening cyber resilience after a 2024 ransomware attack, crediting his IT‑industry experience for rapid containment and ongoing security improvements. Third, the board disputes the shareholder’s claims of mismanagement, noting that sales per editor have risen, quality controls remain stringent, and strategic decisions regarding in‑house publishing and goodwill impairments were justified within the broader restructuring plan. The board’s stance is grounded in its nominating committee’s deliberations and a broader assessment of corporate governance, concluding that dismissing Natsuno would undermine medium‑ to long‑term shareholder interests. The notice is limited to the Japanese market, covering Kadokawa’s domestic and international media operations over the fiscal years 2020–2025, and reflects a board‑level decision rather than an empirical survey.

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

GungHo Online Entertainment · 2026

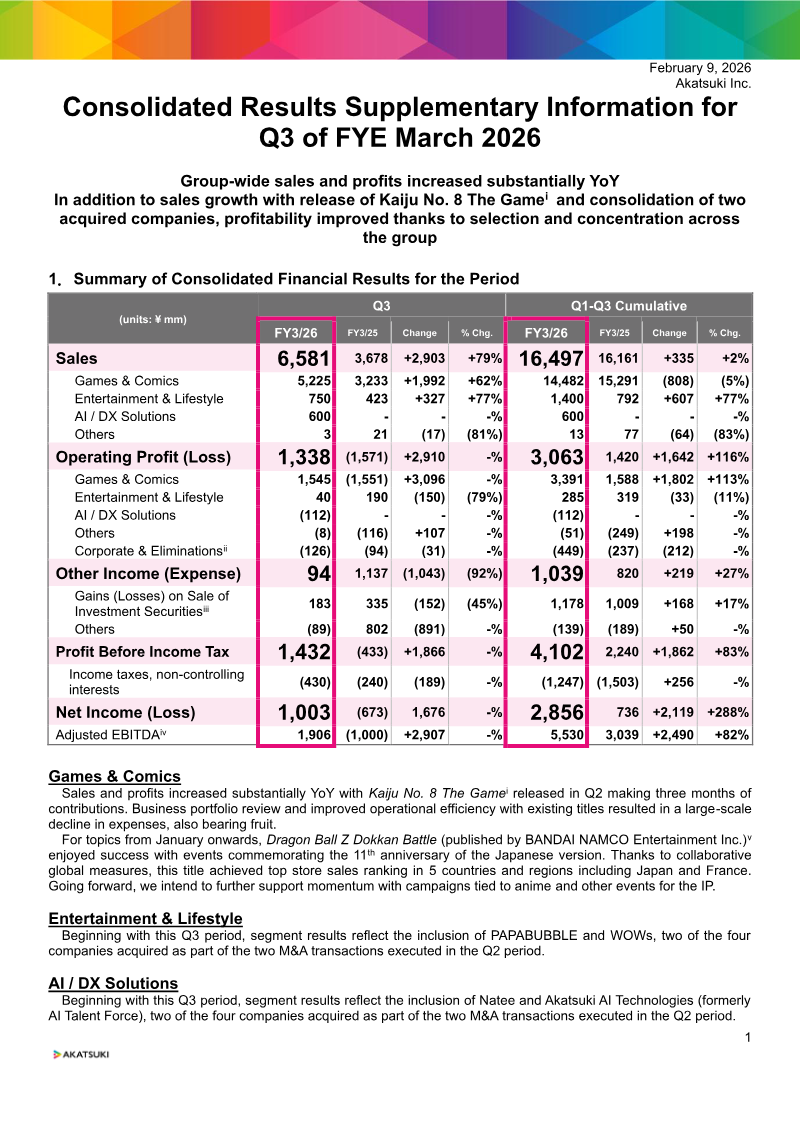

Akatsuki · 2026

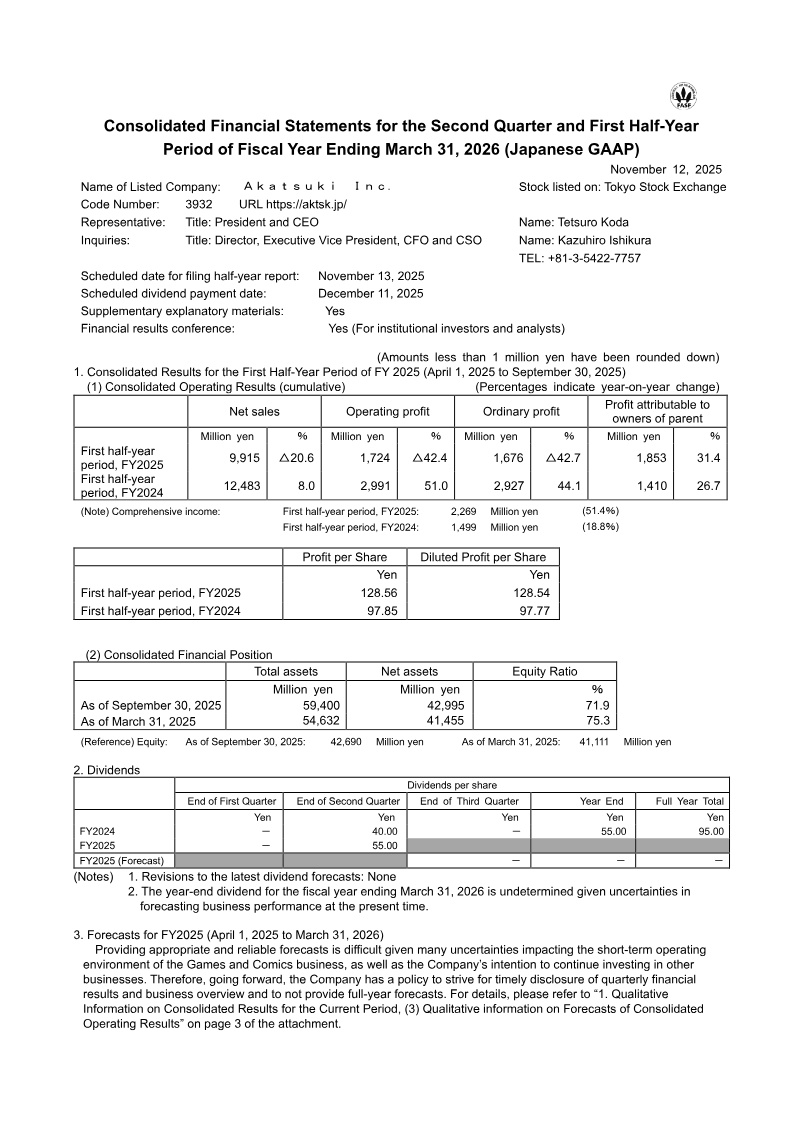

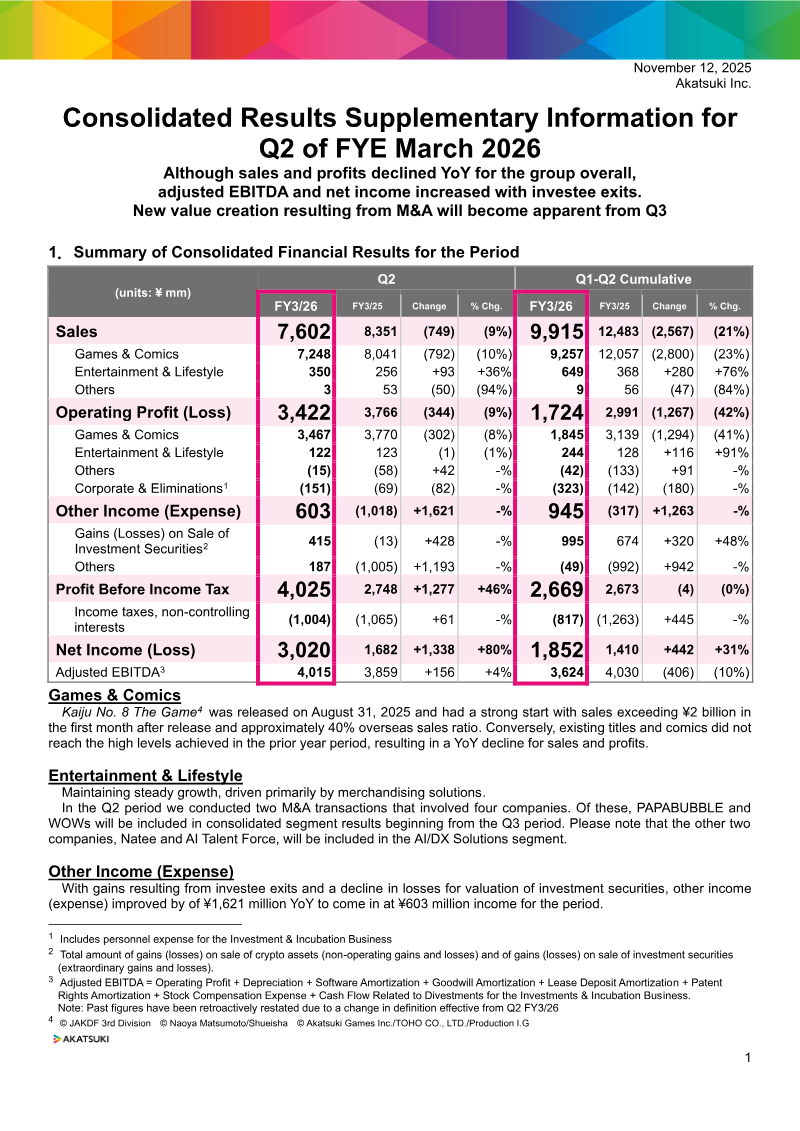

Akatsuki · 2026

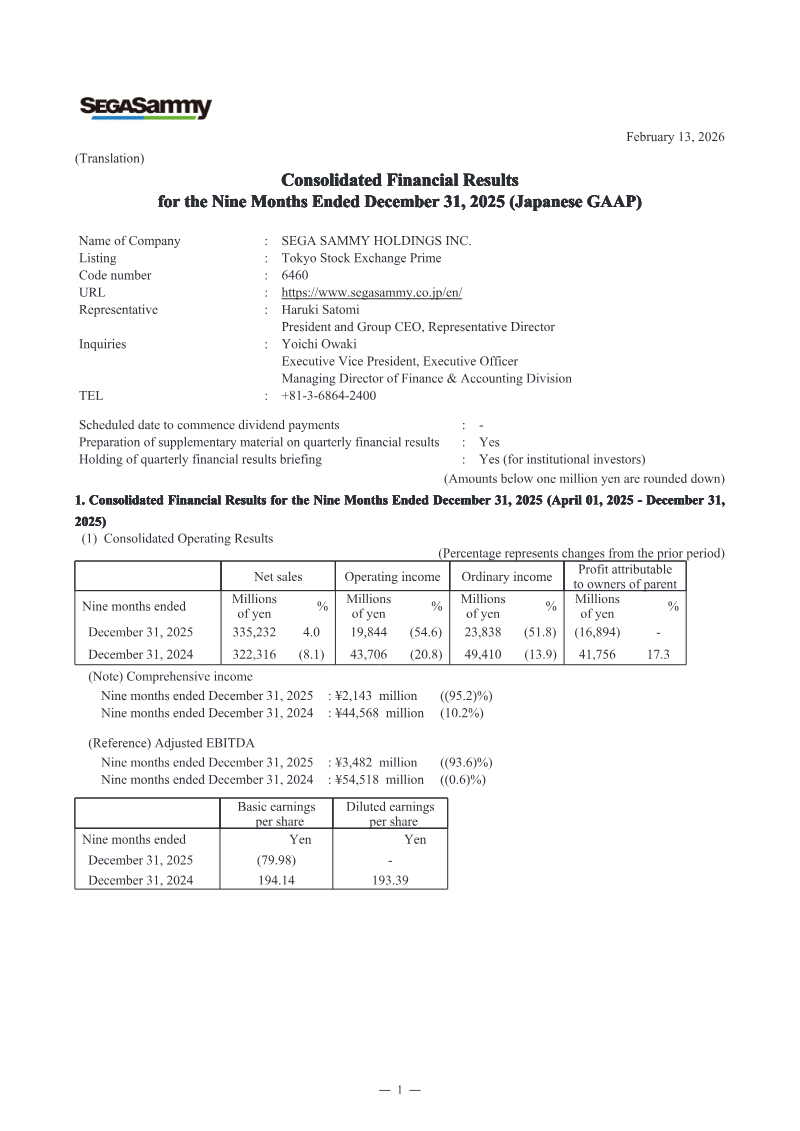

Sega Sammy Holdings · 2026

GungHo Online Entertainment · 2026

Akatsuki · 2025

Akatsuki · 2025

Akatsuki · 2025

PROEXCA · 2025

CyberAgent · 2025

Koei Tecmo · 2025

Koei Tecmo · 2024