LegalKadokawa Corporation

Supplementary Document of the Company’s Initiatives to Enhance Corporate Value and the Shareholder Proposal: Japan

32 pages~31 min full read

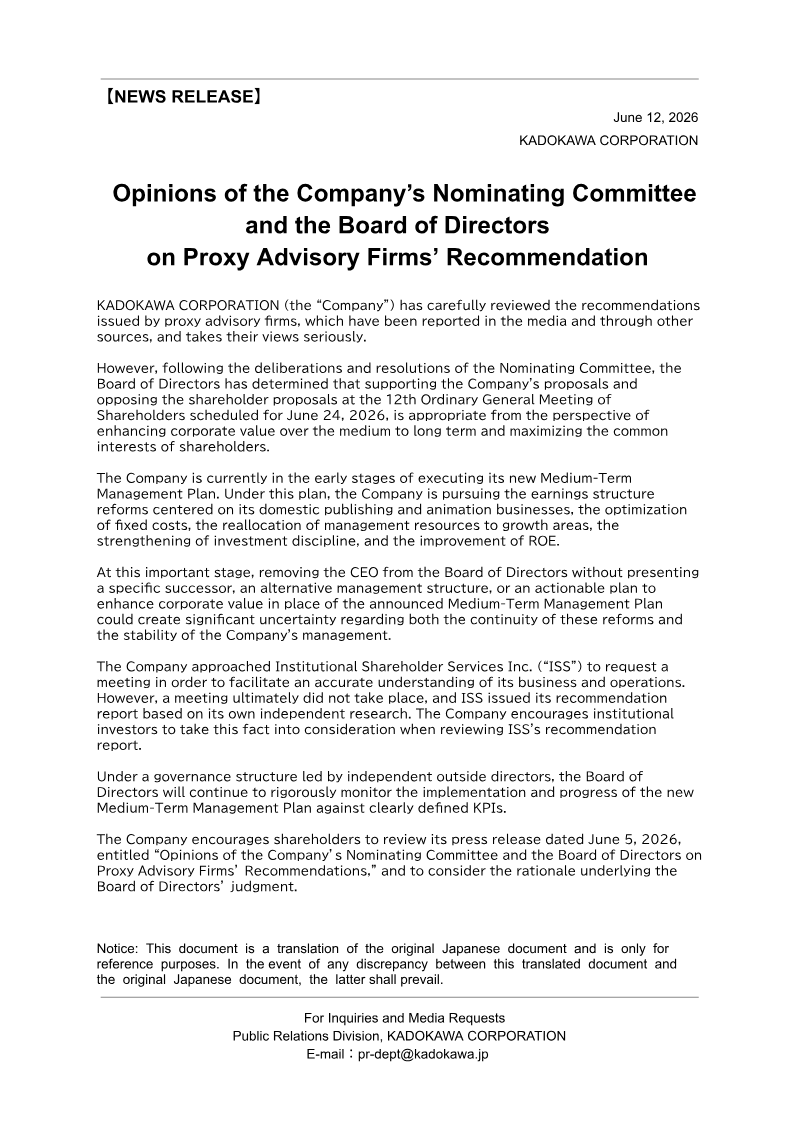

The supplementary document presents KADOKAWA’s strategic response to a shareholder proposal, outlining a six‑year Mid‑term Management Plan that replaces the previous five‑year framework. The core objective is to restore profitability and build a resilient, IP‑driven revenue base by restructuring domestic publishing and animation operations, tightening fixed costs, and investing in high‑growth intellectual property. The plan targets a 12 % return on equity (ROE) by fiscal year 2031, with an emphasis on portfolio and price‑strategy optimization in publishing, cost control in animation production, and a strategic early‑retirement program to free resources for growth.

The transformation strategy is divided into three phases: structural reform (FY2026‑27), profit growth (FY2028‑29), and expansion (FY2030‑31). During the reform phase, KADOKAWA will consolidate business units under new executive leaders and establish a cross‑business steering committee, while pruning unprofitable lines. Net sales are projected to rise from ¥325 bn in FY2026 to ¥400 bn by FY2031, and operating margins are expected to improve from 4.0 % to 9.5 %. A disciplined capital policy will aim for a 30 % payout ratio and maintain share‑buyback flexibility.

Governance measures reinforce the plan’s execution. CEO Takeshi Natsuno maintains 100 % attendance at key board, executive council, and investor meetings, while conducting regular “direct‑meeting” sessions with employees and final interviews for new hires. The board will continuously monitor KPIs—sales returns, in‑house animation production, overseas revenue, ROE, and EPS—and will adjust management structure or investment allocation if progress lags. These initiatives collectively aim to accelerate revenue restructuring, enhance capital efficiency, and sustain leadership continuity across Japan’s media‑mix industry.

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

GungHo Online Entertainment · 2026

Akatsuki · 2026

Akatsuki · 2026

Sega Sammy Holdings · 2026

GungHo Online Entertainment · 2026

Akatsuki · 2025

Akatsuki · 2025

Akatsuki · 2025

PROEXCA · 2025

CyberAgent · 2025

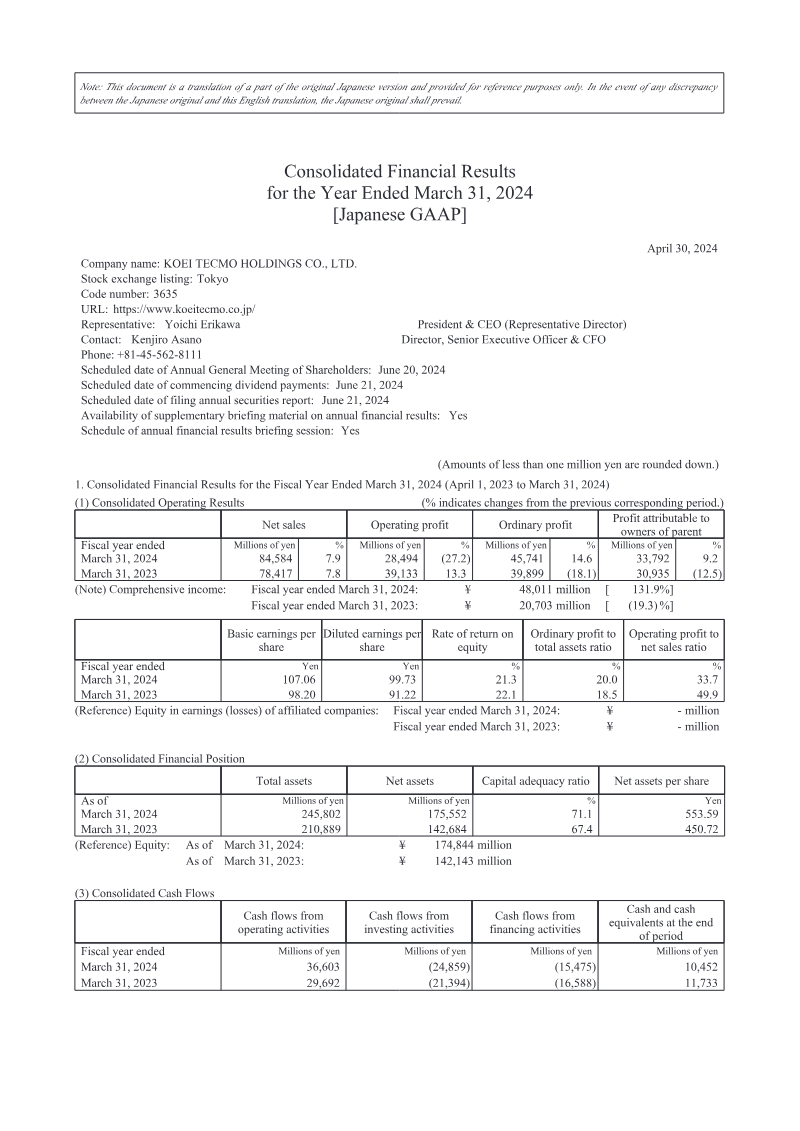

Koei Tecmo · 2025

Koei Tecmo · 2024