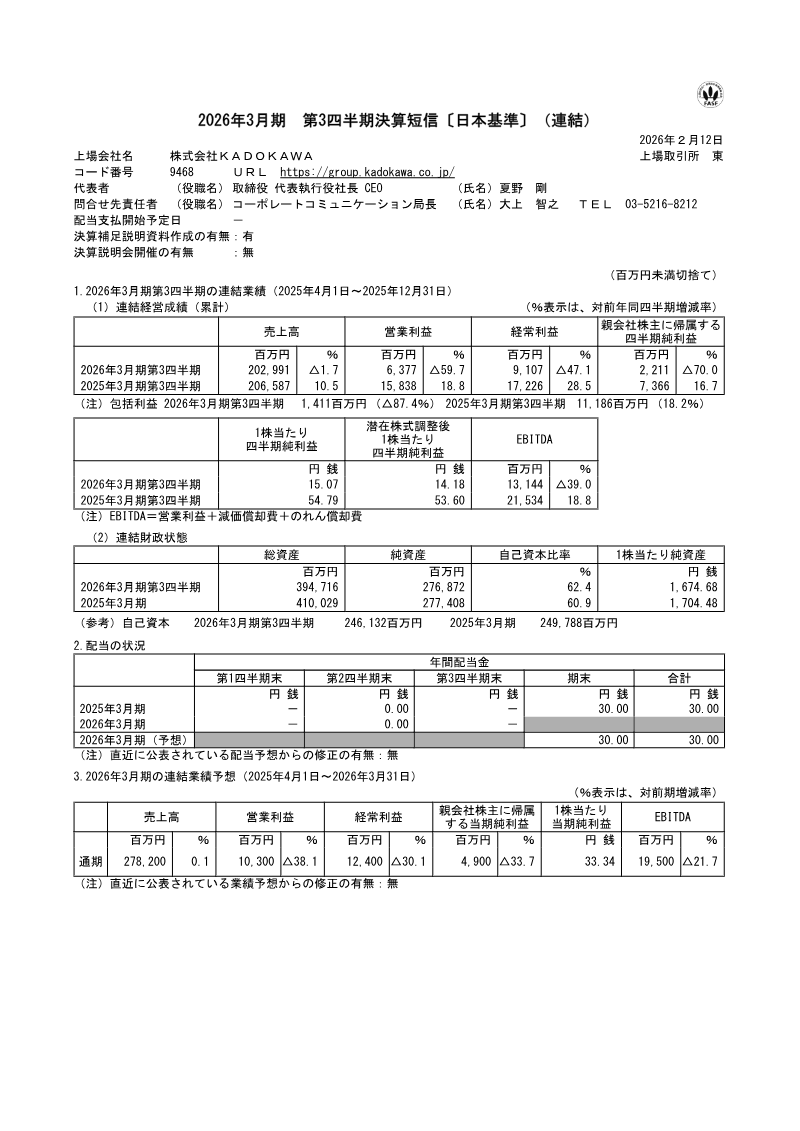

FinancialKadokawa Corporation

Kadokawa Q3 FY2026 Financial Results (Japanese GAAP)

12 Feb 202615 pages~7 min full read

Kadokawa’s operating profit plummeted 59.7% to 6.3 billion yen for the first nine months of FY2026, while net income fell 70.0% to 2.2 billion yen on net sales of 202.9 billion yen.

The Publication and IP segment experienced a 90.2% decline in operating profit, driven by rising personnel costs and a lack of major domestic hits, despite growth in U.S. and Asian markets.

The Animation and Live-Action segment shifted to an operating loss of 904 million yen due to a reliance on new, less established titles compared to the previous year's major successes.

The Game segment, anchored by FromSoftware, saw an 11.6% revenue decline as the new title 'Elden Ring Nightreign' failed to match the high revenue baseline set by the previous year's 'Elden Ring' expansion and repeat sales.

Web Services recovered from prior cyberattack impacts to post a 21.5% increase in sales, providing a rare bright spot in the company's segment performance.

Kadokawa is pursuing a 'Global Media-Mix with Technology' strategy, marked by the acquisitions of Edizioni BD in Italy and SOZO Pte. Ltd. in Singapore to bolster international IP recognition.

Despite the significant quarterly downturn, the company maintained its full-year forecast of 278.2 billion yen in net sales and 10.3 billion yen in operating profit, while confirming a 30 yen per share annual dividend.

This financial report details the consolidated results for KADOKAWA Corporation during the first nine months of the fiscal year ending March 31, 2026, covering the period from April 1, 2025, to December 31, 2025. The data reflects a challenging period for the Japanese media conglomerate, characterized by significant declines in profitability despite relatively stable net sales. Net sales reached 202.9 billion yen, a slight 1.7% decrease year-on-year, while operating profit plummeted 59.7% to 6.3 billion yen. Net income attributable to owners of the parent fell 70.0% to 2.2 billion yen.

Performance varied significantly across industry segments. The Publication and IP segment saw a 90.2% drop in operating profit due to smaller-scale domestic hits and rising personnel costs, despite growth in overseas markets like the U.S. and Asia. The Animation and Live-Action segment transitioned to an operating loss of 904 million yen, attributed to a higher ratio of new, less established titles compared to the previous year’s major hits. The Game segment, led by FromSoftware, reported an 11.6% revenue decline; while the new title Elden Ring Nightreign performed well, it could not match the high bar set by the previous year’s Elden Ring expansion and repeat sales. Conversely, the Web Services and Education/EdTech segments showed resilience, with Web Services recovering from prior cyberattack impacts to post a 21.5% increase in sales.

Strategically, the company continued its "Global Media-Mix with Technology" initiative, expanding its international footprint through the acquisition of Edizioni BD in Italy and SOZO Pte. Ltd. in Singapore. These moves aim to strengthen IP recognition and D2C capabilities in Europe and Southeast Asia. Despite the quarterly downturn, the company maintained its full-year forecast, projecting 278.2 billion yen in net sales and 10.3 billion yen in operating profit, while confirming a planned annual dividend of 30 yen per share.