Related Documents

Financial

Financial Results Briefing Session of Fiscal Year Ended December 31, 2025 [17,284KB]

GungHo Online Entertainment’s FY 2025 financial briefing outlines a strategic pivot from Japan‑centric mobile development toward global expansion, emphasizing action titles on consoles and PCs. The company reports a 64.1 % overseas net‑sales ratio in FY 2025, up from 47.7 % in 2019 and 56.2 % in 2020, reflecting intensified sales in North America and Europe through new releases such as “Let It Die: Inferno” on PlayStation 5, Steam, and Nintendo Switch. The launch of nine global titles in 2025, including the “Ragnarok” series and “Puzzle & Dragons,” is highlighted as a key growth driver, with the latter celebrating its 5 000‑day anniversary and hosting cross‑platform events to boost user activity. Financially, consolidated net sales fell by 1.3 % YoY to ¥125.3 billion, driven mainly by declines in mobile titles and “Ragnarok”‑related revenue under subsidiary Gravity. Operating profit contracted by 9.3 % YoY to ¥276 million, as SG&A expenses rose due to increased advertising spend and personnel costs following the full acquisition of Alim in December 2024. Non‑consolidated results remained flat, but mobile sales slipped and Gravity’s “Ragnarok” titles underperformed, contributing to the consolidated loss. The briefing covers a global geographic scope—North America, Europe, Latin America, and Asia—with a 2025 focus on launching titles in over 150 countries. Methodologically, data derive from consolidated financial statements and quarterly performance metrics, with a clear emphasis on aligning product development with international market demand.

GungHo Online Entertainment

Financial

Financial Results for the First Quarter: Fiscal Year Ending March 2022

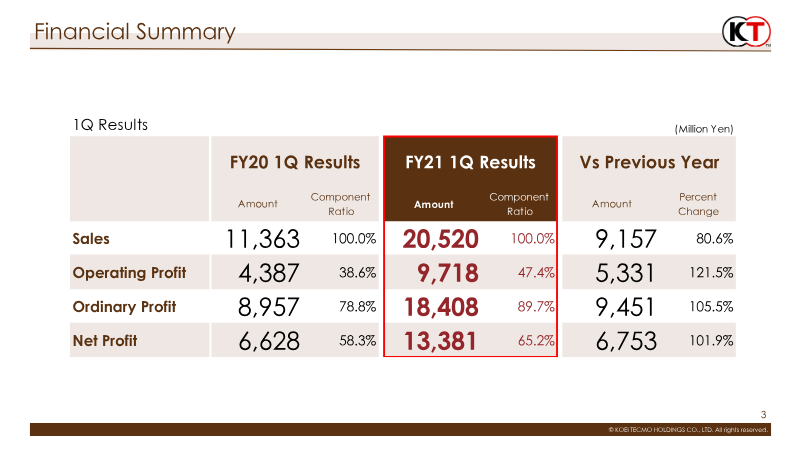

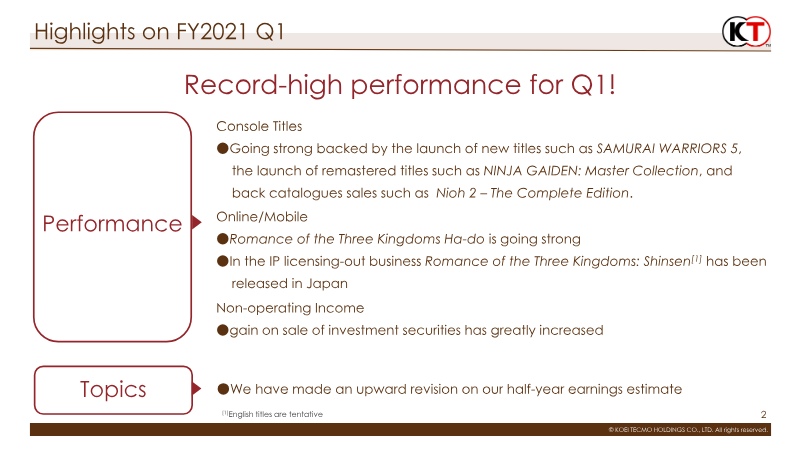

The financial overview for the first quarter of fiscal 2022 highlights a robust performance driven by new console releases and strong back‑catalogue sales. Total revenue rose 80.6 % from ¥11,363 million to ¥20,520 million, with operating profit more than doubling from ¥4,387 million to ¥9,718 million (121.5 % increase). Ordinary and net profits also surged by 105.5 % and 101.9 %, respectively, reflecting higher margins across the entertainment segment. Revenue composition shifted toward console titles, which accounted for 48.7 % of sales in the overseas market and 38.3 % domestically, supported by launches such as *Samurai Warriors 5* and remastered collections like *Ninja Gaiden: Master Collection*. Online/mobile sales grew 55.8 % in download volume, with the Romance of the Three Kingdoms series expanding into licensing‑out agreements. Non‑operating income benefited from gains on investment securities, prompting an upward revision of the half‑year earnings estimate. Geographically, Japan contributed 38.3 % of sales while overseas markets grew by 51.3 %, with North America and Europe showing mixed results—North America doubled its unit sales, whereas European units fell 26.3 %. Headcount increased by 2.5 % to 2,088 employees, and cost of goods sold rose 22.6 %, largely due to higher production for new titles. Methodologically, the report aggregates quarterly financial statements, sales data by platform and region, and download metrics from the company’s global service portfolio. The analysis underscores a strategic focus on IP licensing, back‑catalogue monetization, and digital distribution to sustain growth in the second half of fiscal 2022.

Koei Tecmo

Report

Square Enix Special Feature: Erdrick Trilogy Reimagined

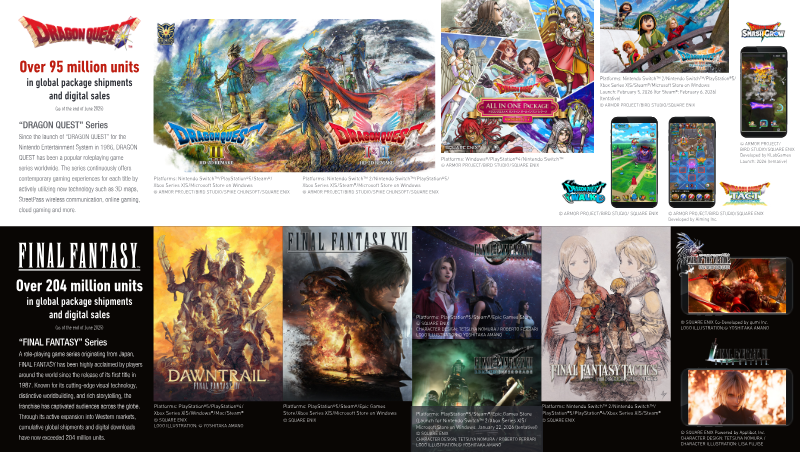

The Dragon Quest franchise continues to expand its global footprint, reaching over 95 million units in total shipments and digital sales as of June 2025. A central focus of the current release strategy is the reimagining of the foundational Erdrick Trilogy through HD-2D remakes. Dragon Quest I & II HD-2D Remake is scheduled for a February 5, 2026, launch on a wide array of platforms, including the Nintendo Switch 2, PlayStation 5, Xbox Series X|S, and PC via Steam and the Microsoft Store. This multi-platform approach reflects a broader commitment to utilizing contemporary technology to modernize classic role-playing experiences for a global audience. Beyond the core Dragon Quest series, the broader portfolio demonstrates significant market penetration across several flagship intellectual properties. The Final Fantasy franchise has surpassed 204 million units globally as of mid-2025, supported by the ongoing expansion of Final Fantasy XIV: Dawntrail and the continued rollout of Final Fantasy VII Rebirth across various ecosystems. Additionally, the Kingdom Hearts series, a collaborative effort with Disney, has achieved over 38 million units in sales, with new entries currently in development for unspecified launch windows. The strategic roadmap emphasizes cross-platform accessibility and the revitalization of legacy content. By targeting next-generation hardware like the Nintendo Switch 2 alongside established consoles and PC storefronts, there is a clear intent to maximize reach across diverse geographic markets. This strategy is complemented by a robust pipeline of mobile and niche titles, including Dragon Quest Tact and various entries in the Bravely Default and Octopath Traveler series, ensuring a steady cadence of content across the role-playing game segment through 2026.

Square EnixSept 2025

Financial

Nintendo Q1 FY2024 Financial Results (English)

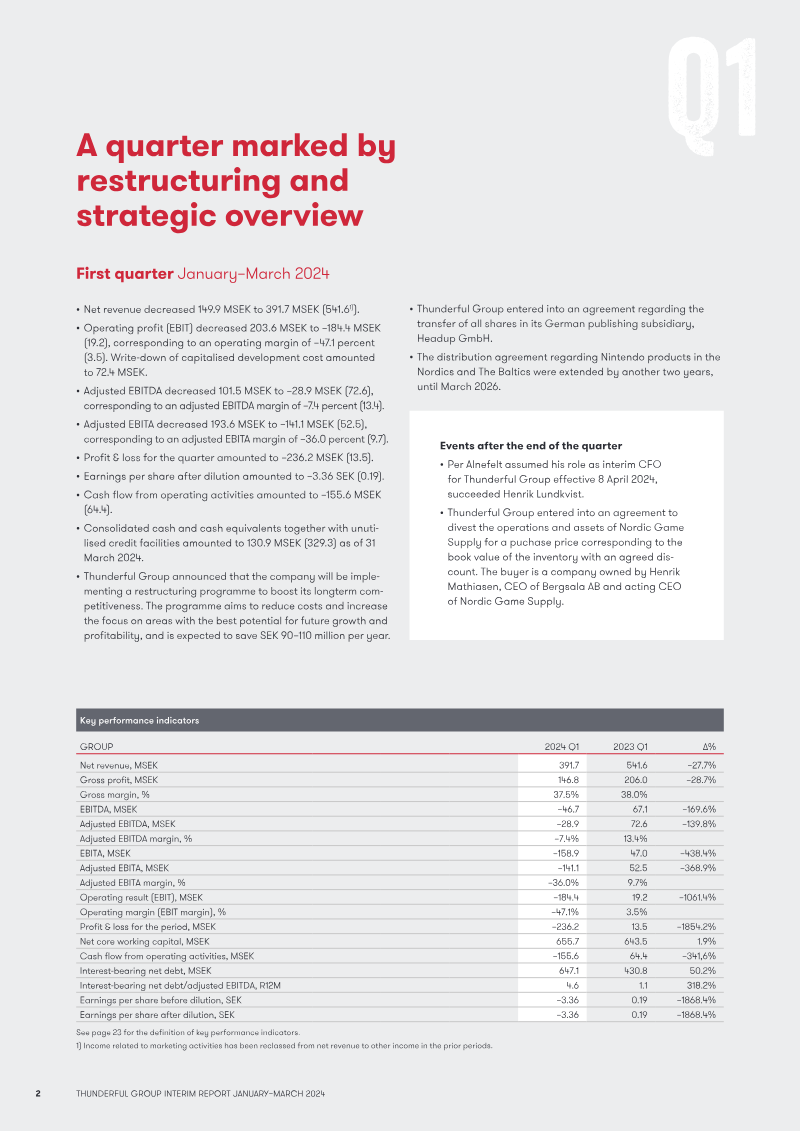

Thunderful Group’s interim report for the first quarter of 2024 details a period of significant financial decline and aggressive corporate restructuring. Net revenue fell 27.7 percent to 391.7 MSEK, while the group recorded an operating loss (EBIT) of 184.4 MSEK, a sharp reversal from the 19.2 MSEK profit reported in the same period the previous year. This downturn was driven by a 35.5 percent revenue drop in the Games segment and a 25.7 percent decrease in Distribution, largely due to weaker market demand for Nintendo Switch products and the underperformance of the internal title SteamWorld Build. To address these challenges, the group initiated a restructuring program aimed at annual cost savings of 90–110 MSEK. This process involved a 72.4 MSEK write-down of capitalized development costs following the cancellation or divestment of twelve game projects. Strategic shifts include the divestment of the German publishing subsidiary Headup GmbH and the sale of Nordic Game Supply’s assets to reduce net debt. Despite these pressures, the group successfully extended its Nintendo distribution agreement for the Nordics and Baltics through March 2026 and reported 13.9 percent growth in its Amo Toys division. The report covers the group’s global operations with a focus on European and Nordic markets for the period of January to March 2024. Financial data indicates a strained liquidity position, with cash and credit facilities dropping to 130.9 MSEK from 329.3 MSEK year-over-year. Management secured a bank waiver conditional on asset divestments and maintains that current funds are sufficient for continued operations. The overarching strategy moving forward emphasizes a simplified games portfolio, more rigorous project validation, and a balanced risk profile across internal and external development.

NintendoJan 2024