Back to Library

Summary

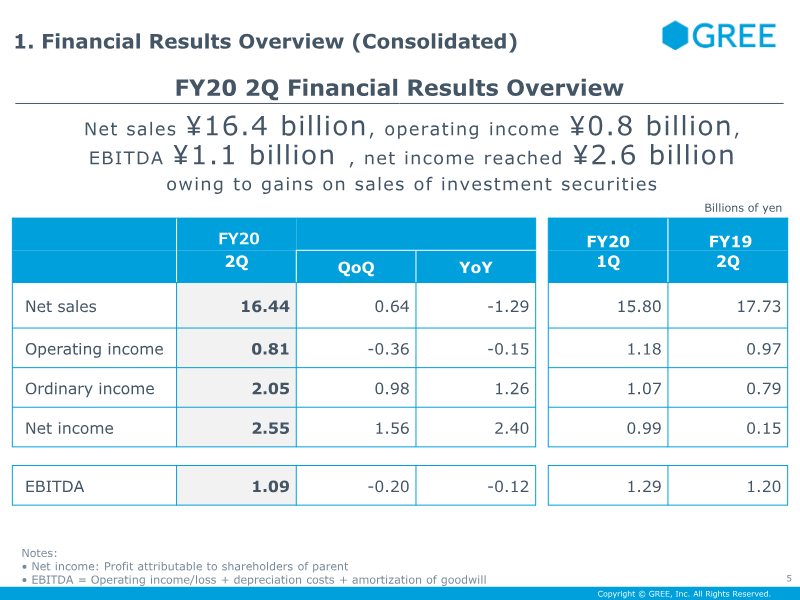

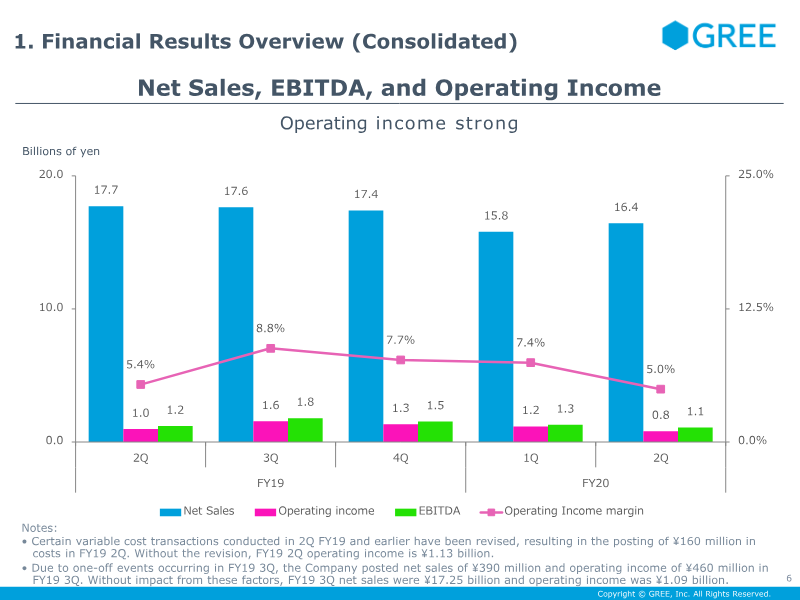

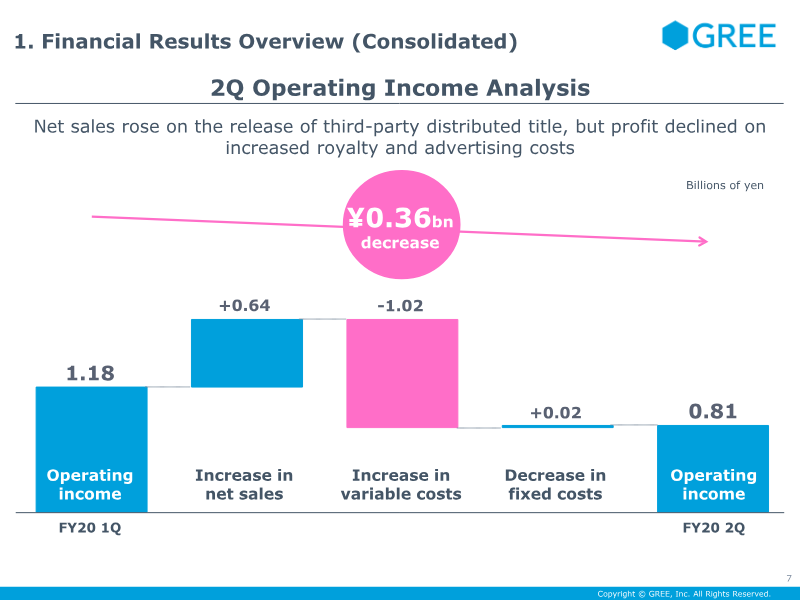

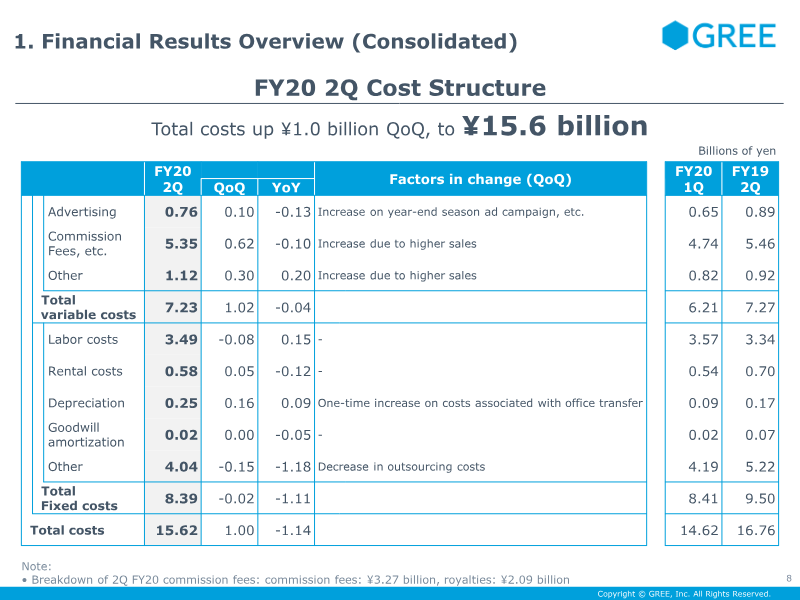

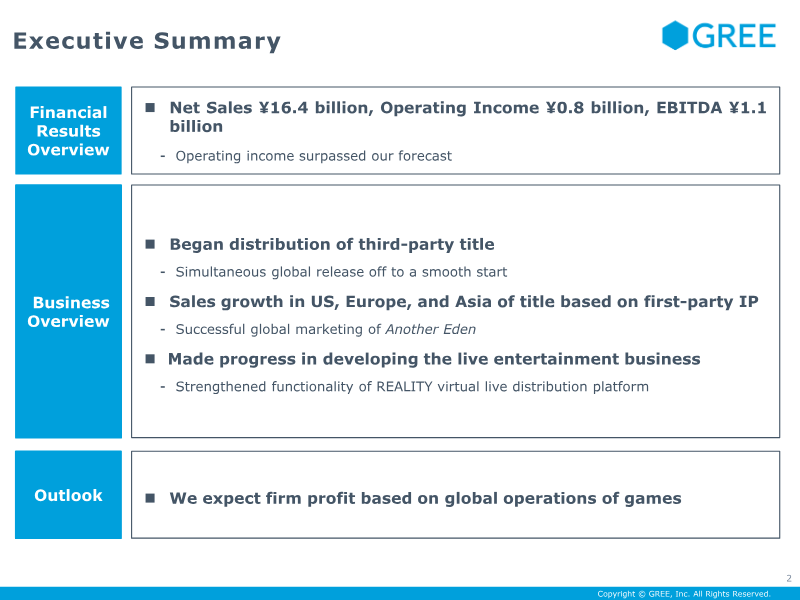

The FY2020 second‑quarter results show a net sales volume of ¥16.4 billion, up 0.64 % from the prior quarter and down 1.29 % year‑over‑year, reflecting a successful launch of a third‑party distributed title and continued growth in first‑party IP sales across the United States, Europe, and Asia. Operating income reached ¥0.81 billion, a decline of ¥0.36 billion versus the previous quarter largely due to higher royalty and advertising expenses, yet still surpassing forecast expectations. EBITDA stood at ¥1.09 billion, a modest QoQ decrease of ¥0.20 billion, while net income surged to ¥2.55 billion, driven by a ¥3.0 billion gain from investment‑security sales. Cost analysis indicates total operating costs rose by ¥1.0 billion QoQ to ¥15.62 billion, with variable costs increasing by ¥0.02 billion and fixed costs rising by ¥1.00 billion, largely attributable to elevated advertising spend during the year‑end season campaign and higher commission costs linked to increased sales. Labor costs remained stable, while depreciation and goodwill amortization were unchanged. Strategic initiatives highlighted include the simultaneous global release of a third‑party title, expansion of the REALITY virtual live‑distribution platform with low‑latency enhancements, and intensified media marketing campaigns that boosted overseas sales by 2.7× for the “Another Eden” series. The company projects firm profitability in future quarters, supported by its diversified game, live‑entertainment, and advertising businesses.

Tags

Pages

View all

Citation

Citation

Generating citation...

Similar Documents

Report

FY2020 1Q Financial Results Presentation

The presentation reports fiscal year 2020 first‑quarter results for a Japanese entertainment company. Net sales reached 15.8 billion yen, operating income was 1.2 billion yen and EBITDA 1.3 billion yen, surpassing the mid‑to‑high hundred‑million yen forecast and maintaining a stable operating margin despite a quarter‑on‑quarter sales decline driven by post‑anniversary event effects and the transfer of some game titles to improve profitability. Cost controls, particularly a 1.5 billion yen reduction in advertising and outsourcing expenses, offset the sales drop and kept operating income flat. An extraordinary income from equity issuance related to a listing event contributed positively to net income. Geographically, the company expanded its flagship title “DanMachi” into 27 European markets and continued global distribution in Japan, Asia, North America, and Europe. The live‑entertainment segment launched a reality virtual platform, hosting festivals and new program formats to broaden content offerings. The advertising and media arm focused on strengthening community engagement through targeted campaigns and anime tie‑ins, while the game development pipeline aimed to release two new titles in FY 2020 and plan four to six additional releases for FY 2021. Methodologically, the figures derive from consolidated financial statements and internal cost‑tracking systems. The outlook for Q2 projects operating income around 0.5 billion yen, with increased advertising spend to activate promising titles and a continued decline in browser game revenue. The company’s investment securities, notably the Bushiroad listing, are expected to continue appreciating in value.

GREE

Report

FY2020 2Q Financial Results Presentation

The presentation reports GREE Inc.’s second‑quarter 2020 financial performance, highlighting a net sales figure of ¥16.4 billion and operating income of ¥0.8 billion, surpassing forecasts. EBITDA reached ¥1.1 billion, while net income climbed to ¥2.6 billion largely due to a ¥3.0 billion gain from the sale of investment securities. Year‑over‑year and quarter‑on‑quarter profit growth is emphasized, with operating income projected for the third quarter between ¥0.5 billion and just under ¥1.0 billion. Key business drivers include the successful launch of a third‑party distributed title in November, which boosted net sales and coin consumption. The first‑party IP “Another Eden” expanded overseas sales, achieving a 2.7‑fold increase from November to December across the United States, Europe, and Asia, supported by intensified global marketing. The live‑entertainment platform REALITY continues to grow, introducing low‑latency mode and partnering with Cluster Inc. for integrated avatar functionality. Operationally, variable costs rose due to higher commission and advertising expenses, while fixed costs remained stable except for a one‑time depreciation increase from office relocations. The investment securities portfolio maintained a book value of ¥19 billion against an assessed value of ¥36 billion, confirming strong performance. Strategically, GREE plans to release one additional title in FY20 and 4–6 new titles for FY21 onward, including collaborations with Visual Arts (Heaven Burns Red) and SYMPHOGEAR (Assault Lily: Last Bullet). Existing titles such as SINoALICE, DanMachi, SYMPHOGEAR, and Shoumetsu Toshi continue to receive fan‑community engagement campaigns. The company’s advertising and media initiatives aim to broaden user acquisition through targeted partnerships and campaigns.

GREE