AppLovin Corporation reports a robust 2025 financial performance, driven by accelerated revenue growth and strong operating margins. Revenue for the full year reached $5.48 billion, a 70 % increase from $3.22 billion in 2024 and an 82 % year‑over‑year rise from $3.22 billion in 2023. Net income from continuing operations climbed to $3.43 billion, up 116 % from $1.59 billion in 2024 and 63 % from $1.58 billion in 2023, yielding a net margin of 63 %. Adjusted EBITDA surged to $4.51 billion, a 82 % increase from the prior year and an 87 % rise from 2023, with a margin of 82 %. Cash flow from operations grew to $1.40 billion, a 82 % increase year‑over‑year.

The company’s balance sheet strengthened markedly: cash and equivalents rose to $2.49 billion from $741 million, while total assets increased to $7.26 billion against $5.87 billion in 2024. Shareholders’ equity expanded to $2.13 billion, reflecting retained earnings growth and additional paid‑in capital. Long‑term debt remained stable at approximately $3.51 billion, and operating lease liabilities decreased.

AppLovin’s methodology for non‑GAAP measures is disclosed in detail, with Adjusted EBITDA defined as net income excluding discontinued operations, taxes, interest, and other non‑core items. The reconciliation tables show that adjustments total $1.08 billion in 2025, largely driven by stock‑based compensation and amortization.

Geographically, the report does not segment revenue or expenses; it presents consolidated figures for the United States and global operations. The time frame covers fiscal year 2025, with quarterly comparisons to 2024 and 2023. The update is unaudited but follows standard SEC filing practices, providing a comprehensive view of AppLovin’s financial trajectory and operational efficiency.

AppLovin · 2026

AppLovin · 2026

AppLovin · 2025

AppLovin · 2025

AppLovin · 2025

AppLovin · 2025

AppLovin · 2025

AppLovin · 2024

AppLovin · 2024

AppLovin · 2024

AppLovin · 2023

AppLovin · 2023

Modern Times Group · 2026

InvestGame · 2025

G5 Entertainment AB · 2024

Bandai Namco · 2021

King · 2021

HPvX Partners

Playtika Holding

Playtika Holding

Modern Times Group

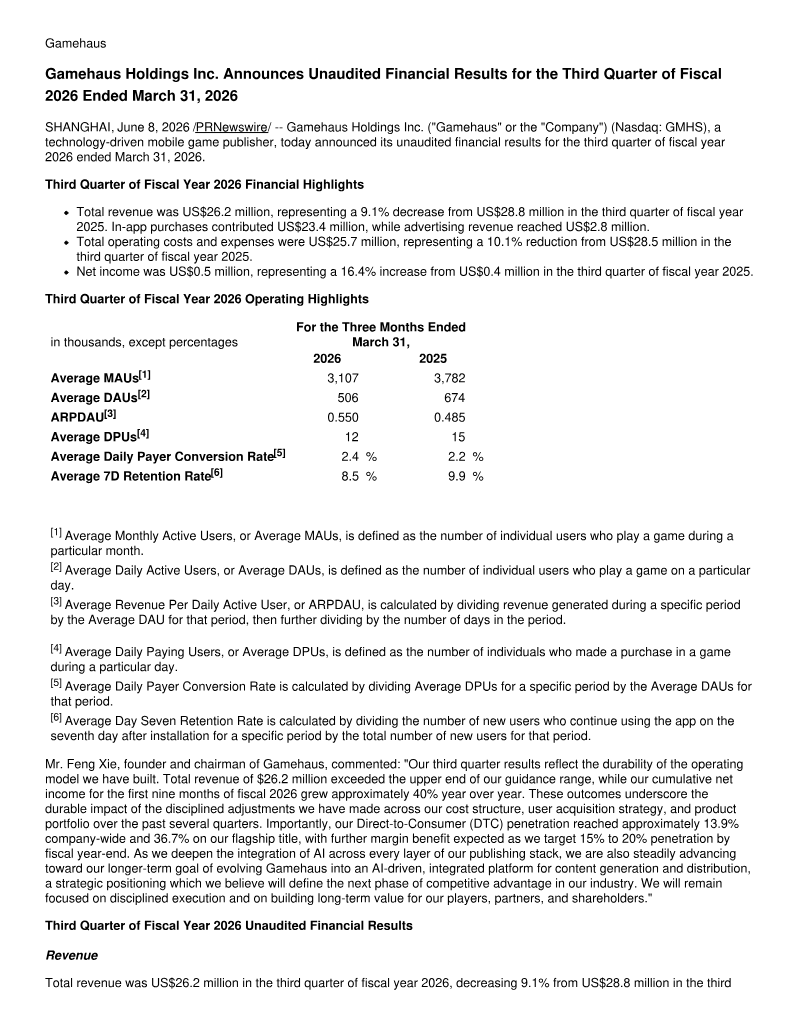

Gamehaus Holdings

Playtika Holding

Almedia · 2026