FinancialNihon Falcom

Financial Results: Fiscal Year 2026 Second Quarter (Japan)

9 pages~4 min full read

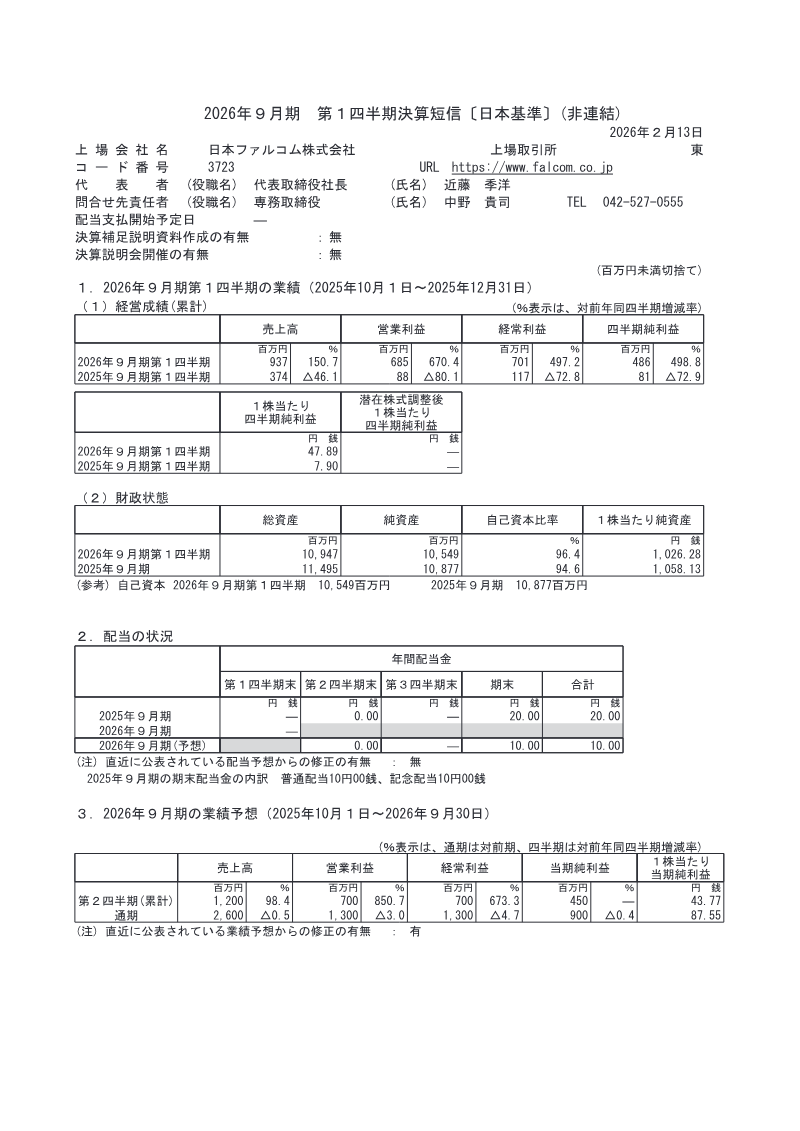

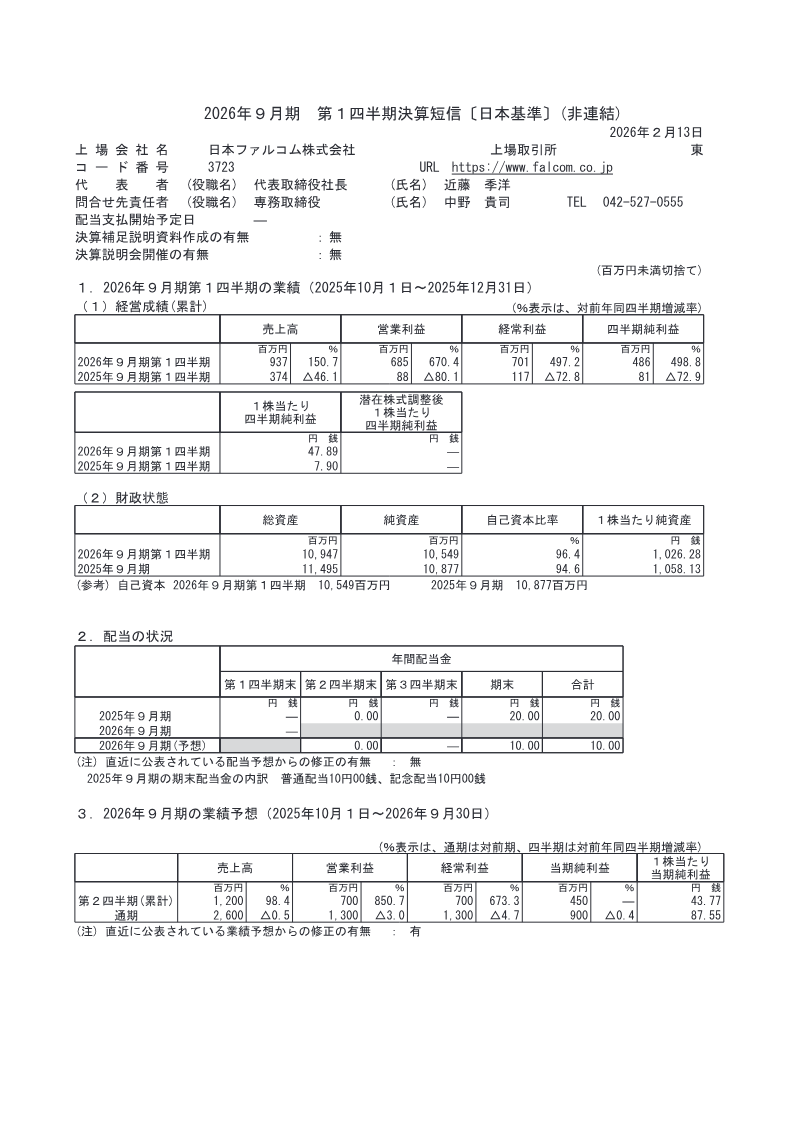

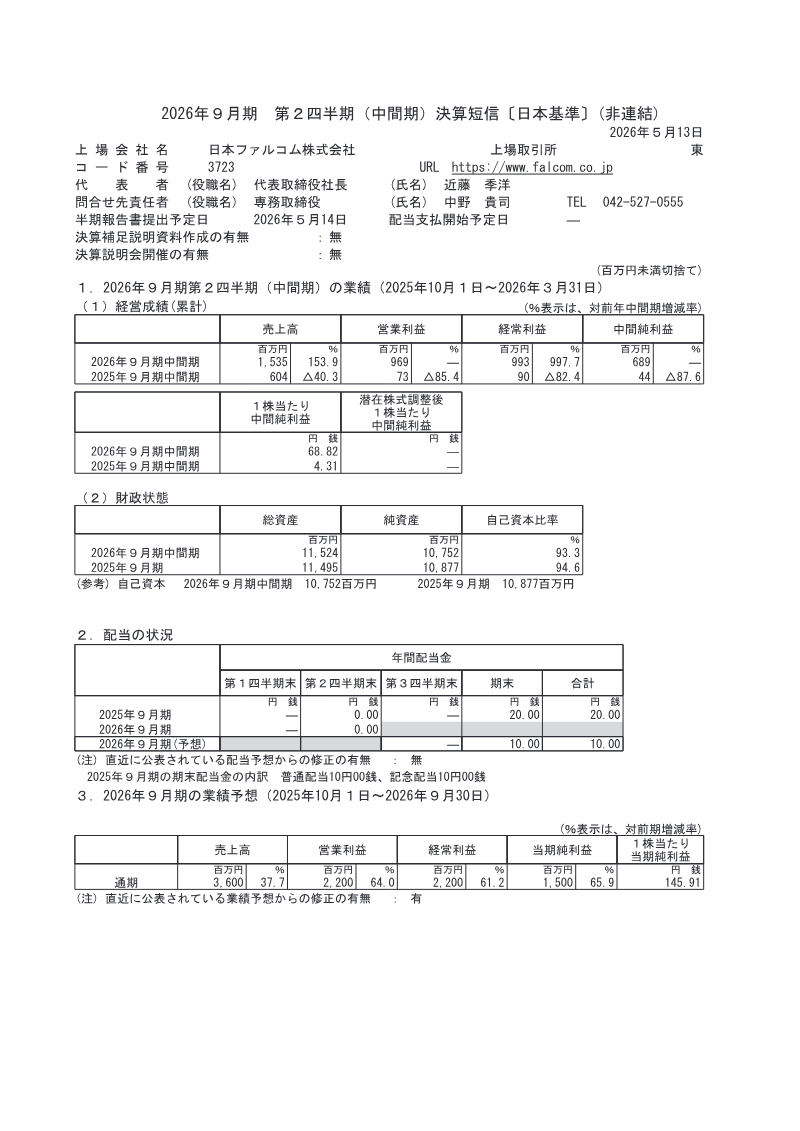

Fiscal year 2026, second‑quarter results for Falcom Corporation show a dramatic rebound from the previous quarter. Total sales rose 153.9 % to ¥1,535 million, driven by a 194.8 % increase in licensing revenue and a modest 5.5 % decline in product sales, reflecting strong performance of the “Sora no Kiseki” series and new releases across Nintendo Switch 2, PlayStation 5, Steam, and mobile platforms. Operating profit surged 1,216.4 % to ¥969 million, and ordinary profit climbed 997.7 % to ¥994 million, largely due to higher gross margins and favorable foreign‑exchange gains. Net profit for the interim period reached ¥689 million, a 1,454.3 % jump from the prior year’s quarter.

Balance‑sheet strength remained robust: total assets increased 0.3 % to ¥11,524 million, with cash and deposits up by ¥372 million. Net equity stood at ¥10,752 million, a 1.1 % decline mainly from share buybacks of ¥608 k and dividend payouts of ¥205 million. The equity ratio remained high at 93.3 %. Cash flow from operations grew to ¥1,186 million, supported by strong sales and efficient working‑capital management.

For the full fiscal year, Falcom forecasts revenue of ¥3,600 million (up 37.7 %), operating profit of ¥2,200 million (up 64.0 %), ordinary profit of ¥2,200 million (up 61.2 %), and net income of ¥1,500 million (up 65.9 %). Earnings per share are projected at ¥145.91. The company attributes the upward revision to continued momentum in its flagship titles and expanding international licensing, while noting that future results may vary with market conditions.

Nippon Ichi Software

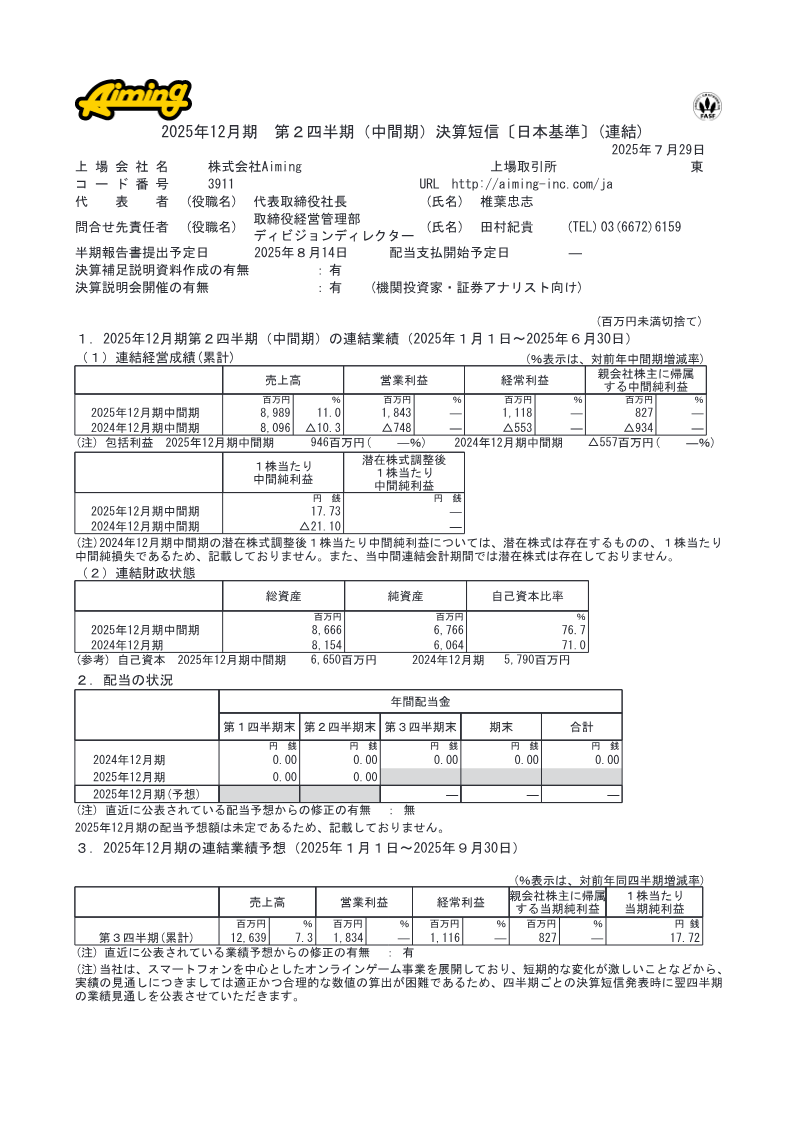

Aiming

GREE

GREE

Capcom · 2026

Capcom Co. · 2026

Capcom · 2026

Sony Group Corporation · 2026

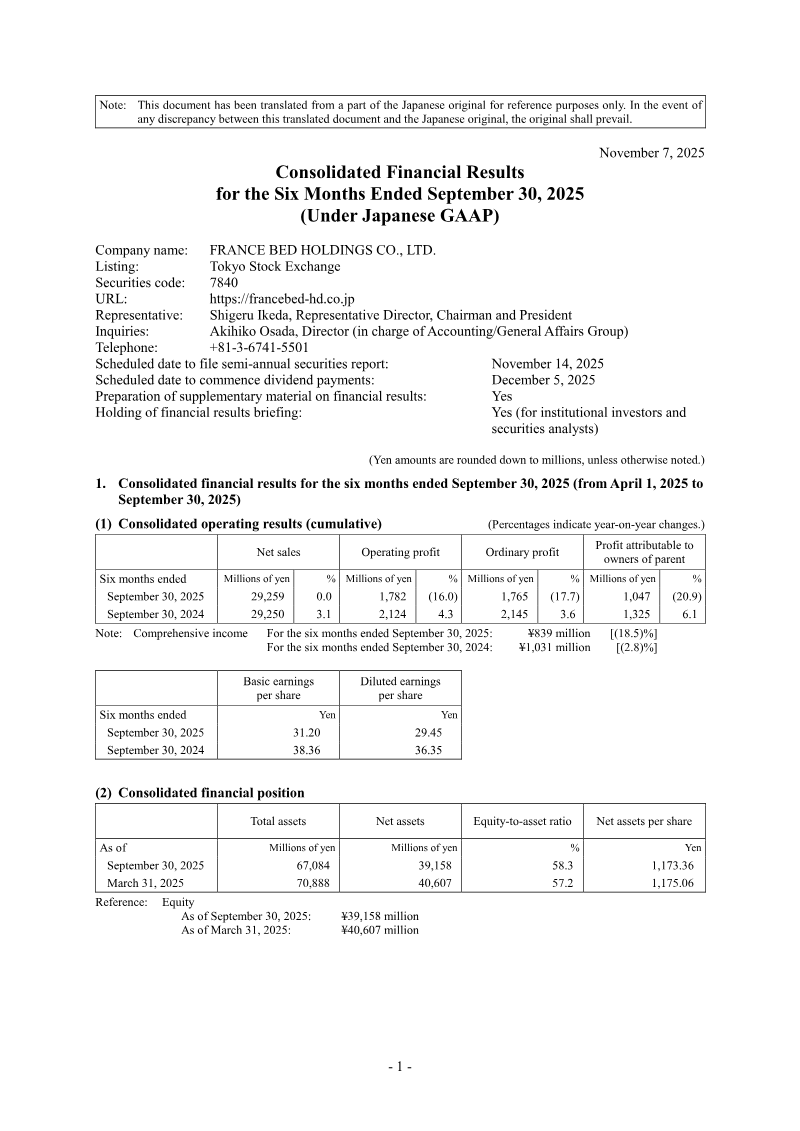

FRANCE BED HOLDINGS CO. · 2026

Marvelous · 2026

Square Enix · 2026

CyberAgent · 2026