Mobile

Report

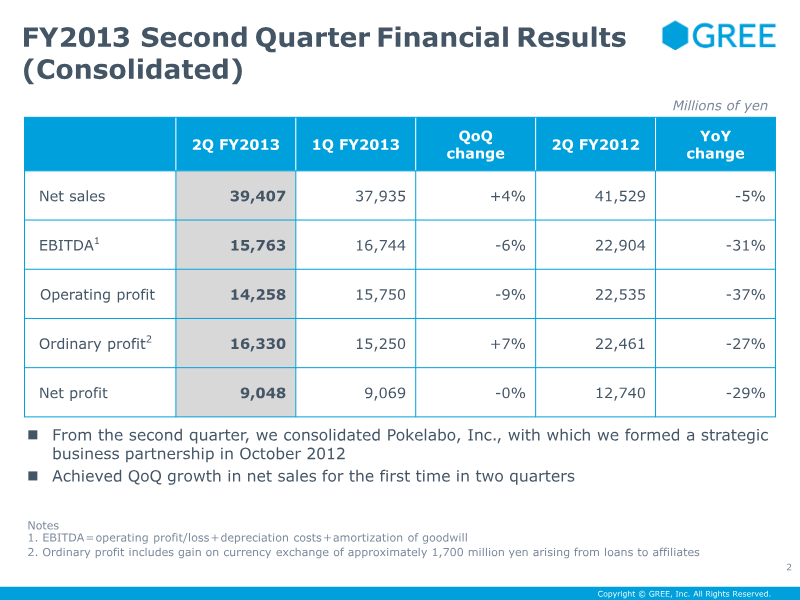

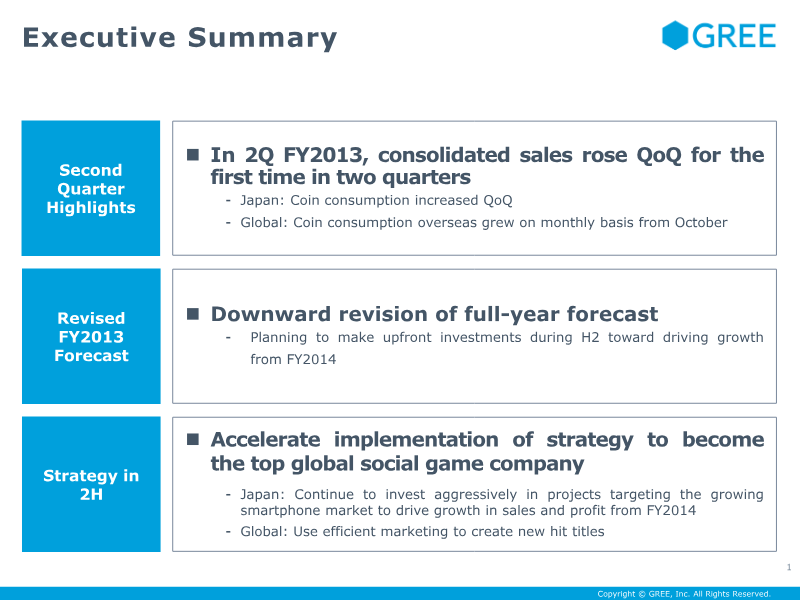

FY2013 Second Quarter Financial Results

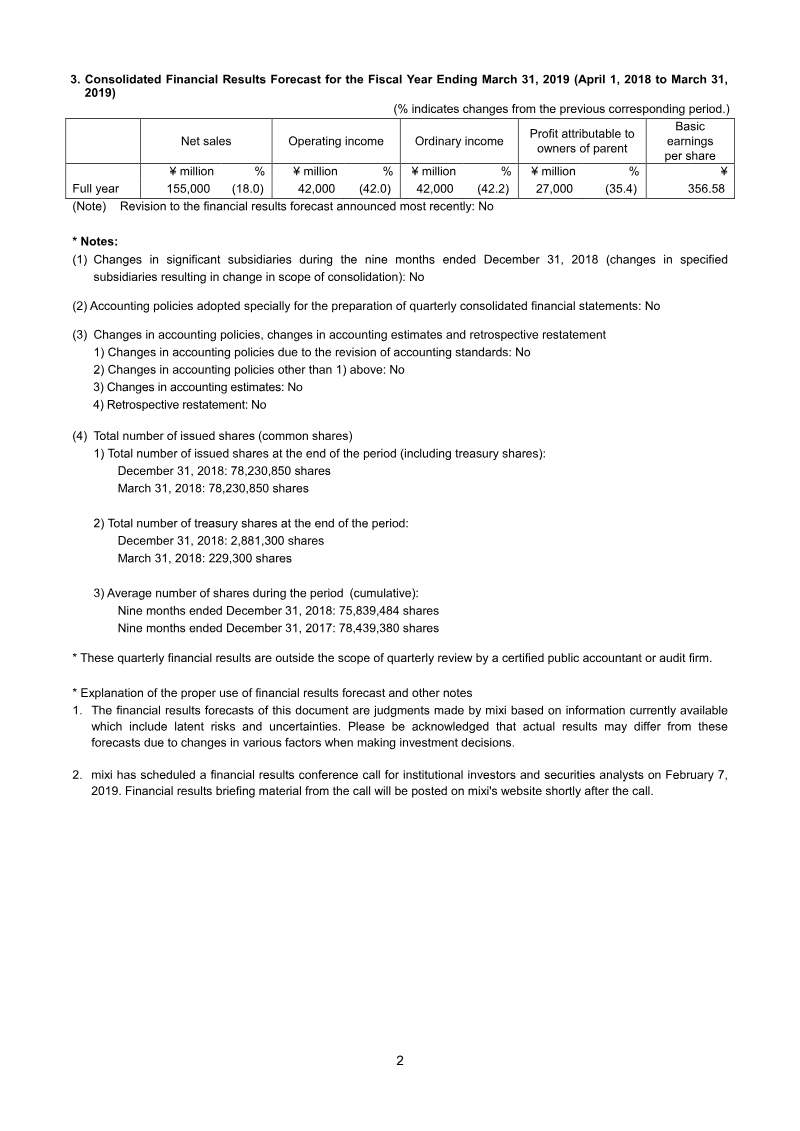

The quarterly financial release outlines a mixed performance for FY2013 second quarter, with net sales rising 4 % QoQ to ¥39.4 billion but falling 5 % YoY, while EBITDA and operating profit declined sharply by 6 % and 9 %, respectively. Net profit remained flat QoQ at ¥9.0 billion but dropped 29 % YoY, reflecting higher costs and a one‑time currency gain. Consolidation of Pokelabo in October contributed to the QoQ sales growth, and the company noted a 35 % increase in cost of sales driven by higher labor and advertising expenses, alongside a 60 % rise in depreciation. Geographically, Japan remains the core market; coin consumption grew QoQ by 600 million coins, with strong performance in native titles such as “Driland” and IP‑based releases. Overseas coin consumption has been rising monthly since October, with new in‑house and co‑branded games expected to contribute from Q3 onward. The company plans aggressive smartphone investments in H2, targeting hit titles across new genres (MMO, FPS) and leveraging efficient marketing to balance lifetime value against cost per install. The revised FY2013 forecast reflects a downward revision of net sales to ¥170 billion (−17.9 % from prior forecast) and operating profit to ¥60 billion (−32.4 %). The outlook hinges on postponed releases in H2 and continued hiring to support smartphone growth, with anticipated increases in customer‑support and compliance costs. Overall, the report signals a strategic pivot toward diversified game genres and international expansion while managing cost pressures in a competitive mobile gaming landscape.

GREE

Report

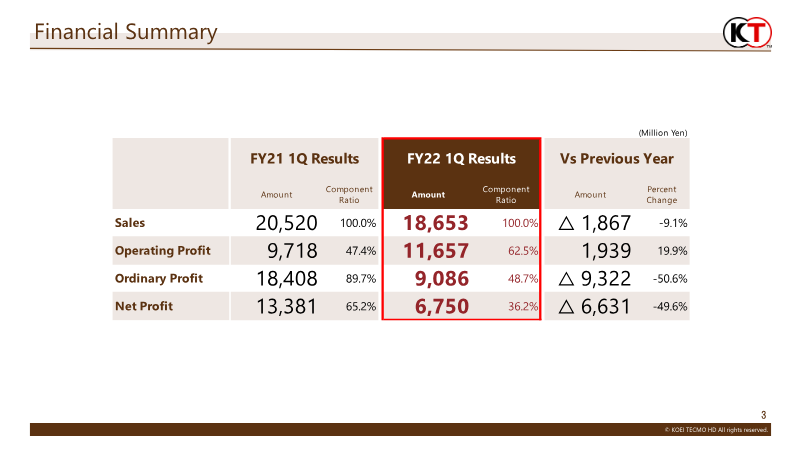

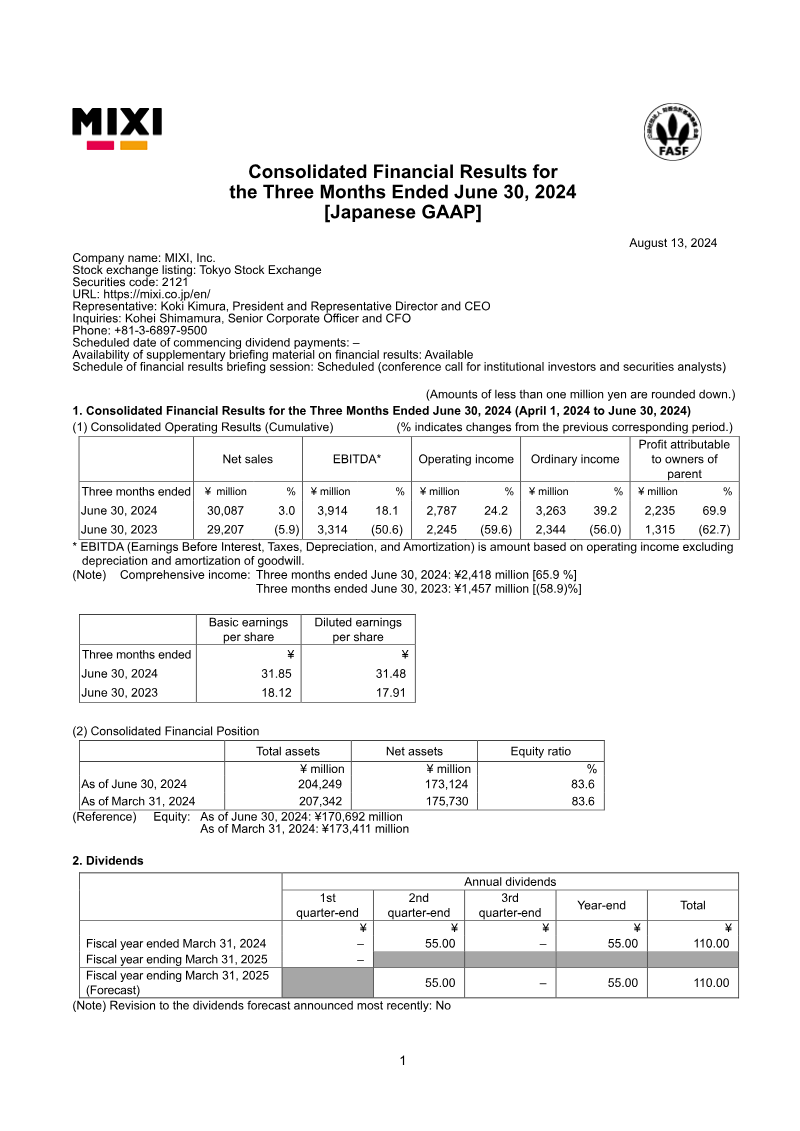

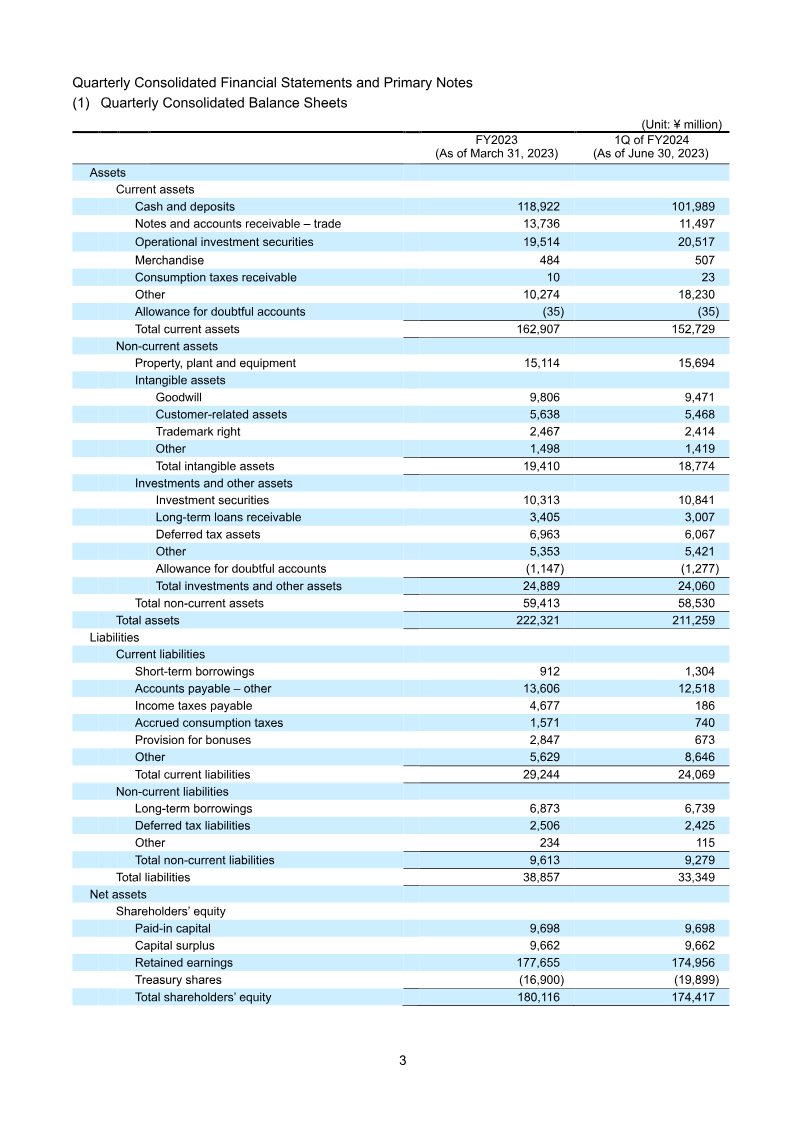

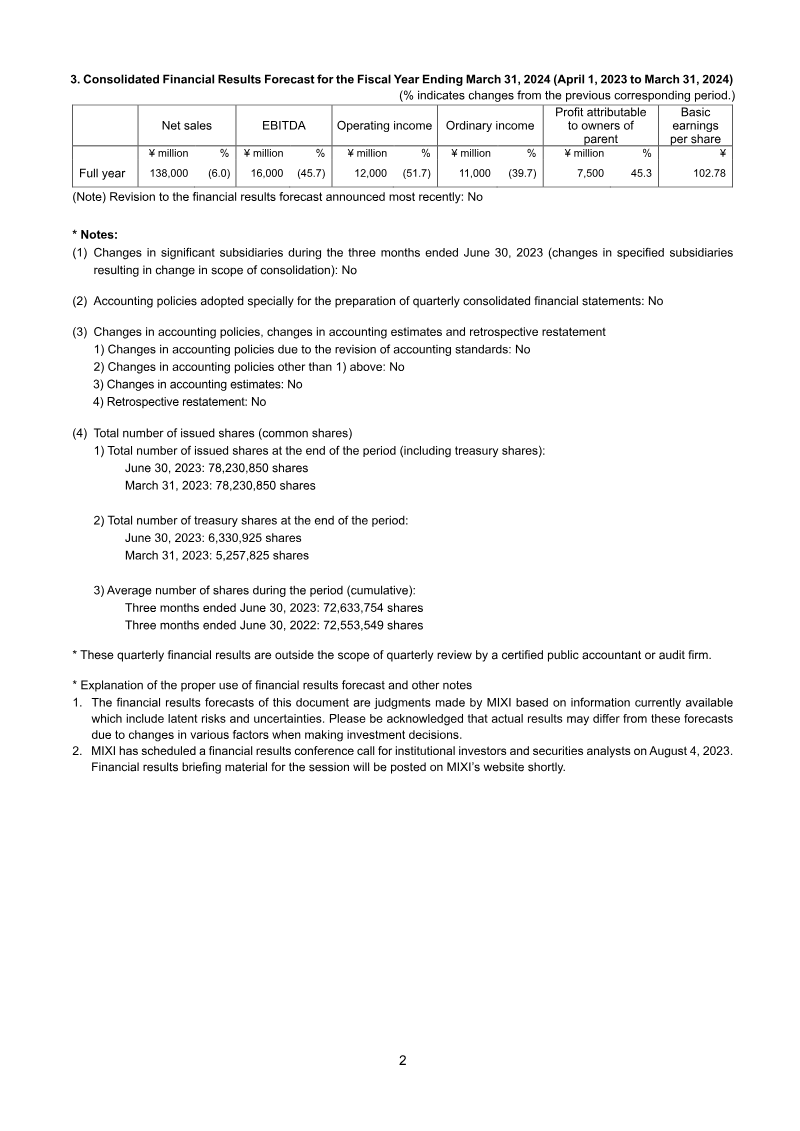

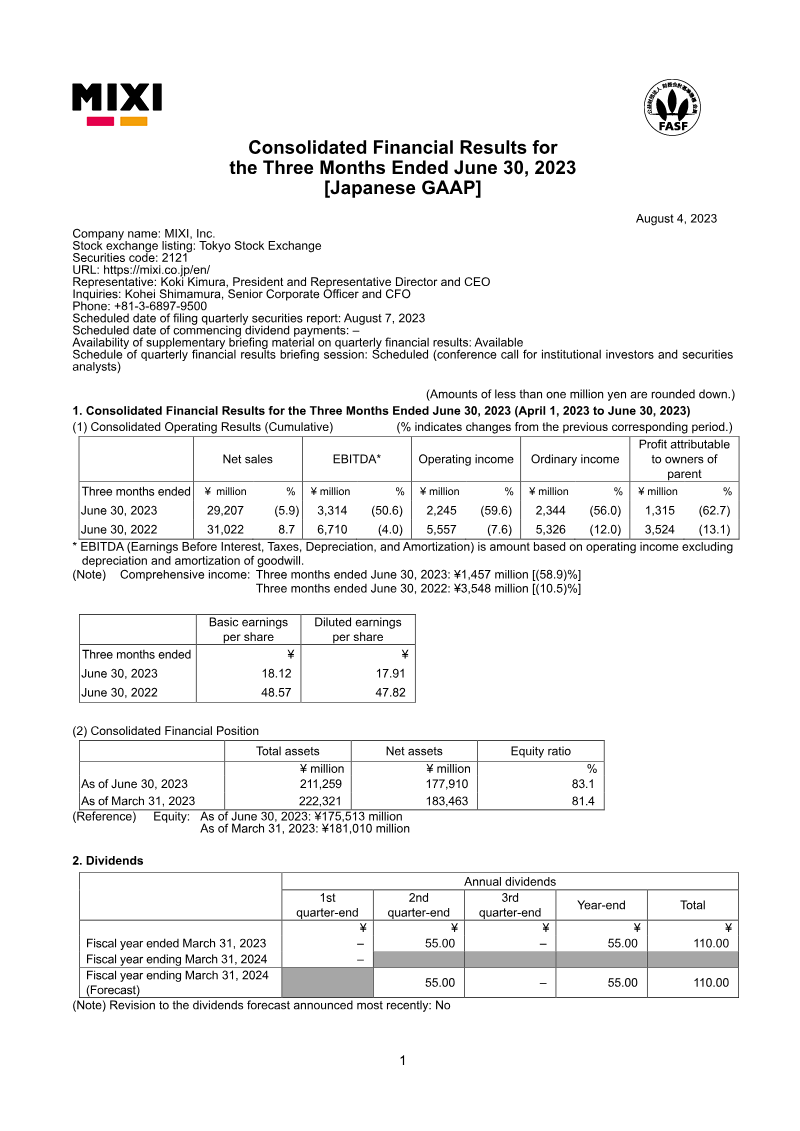

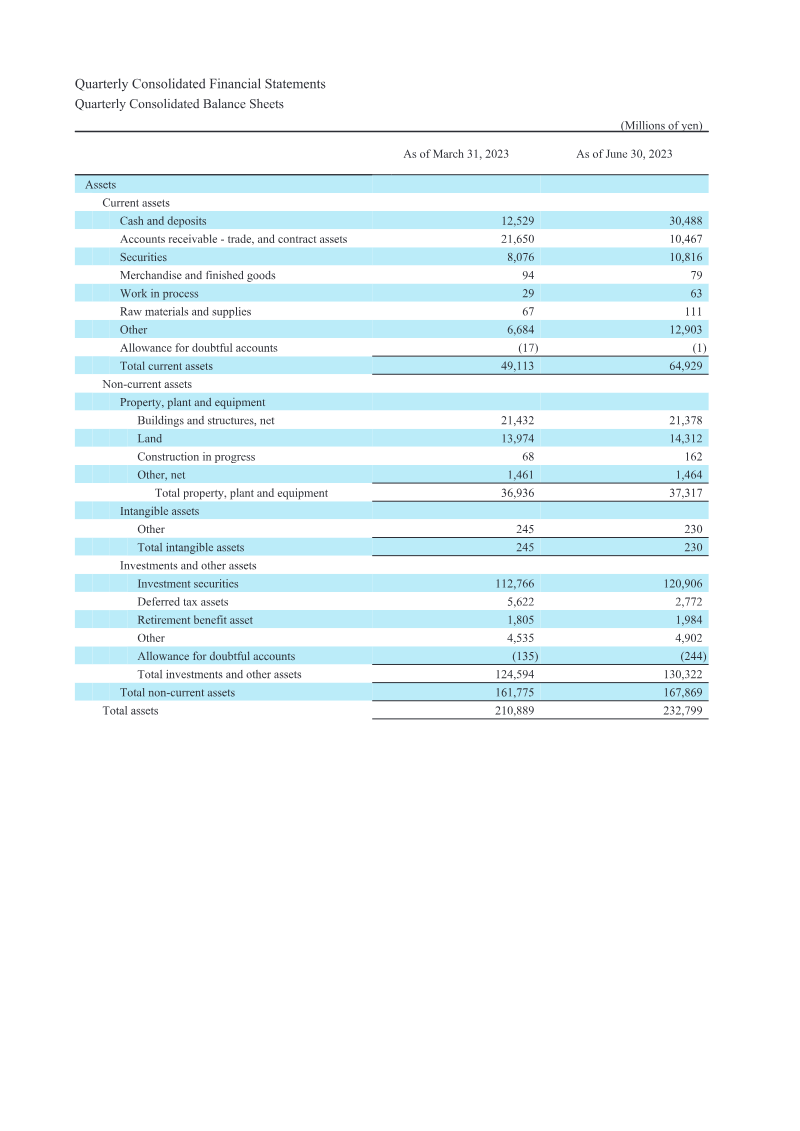

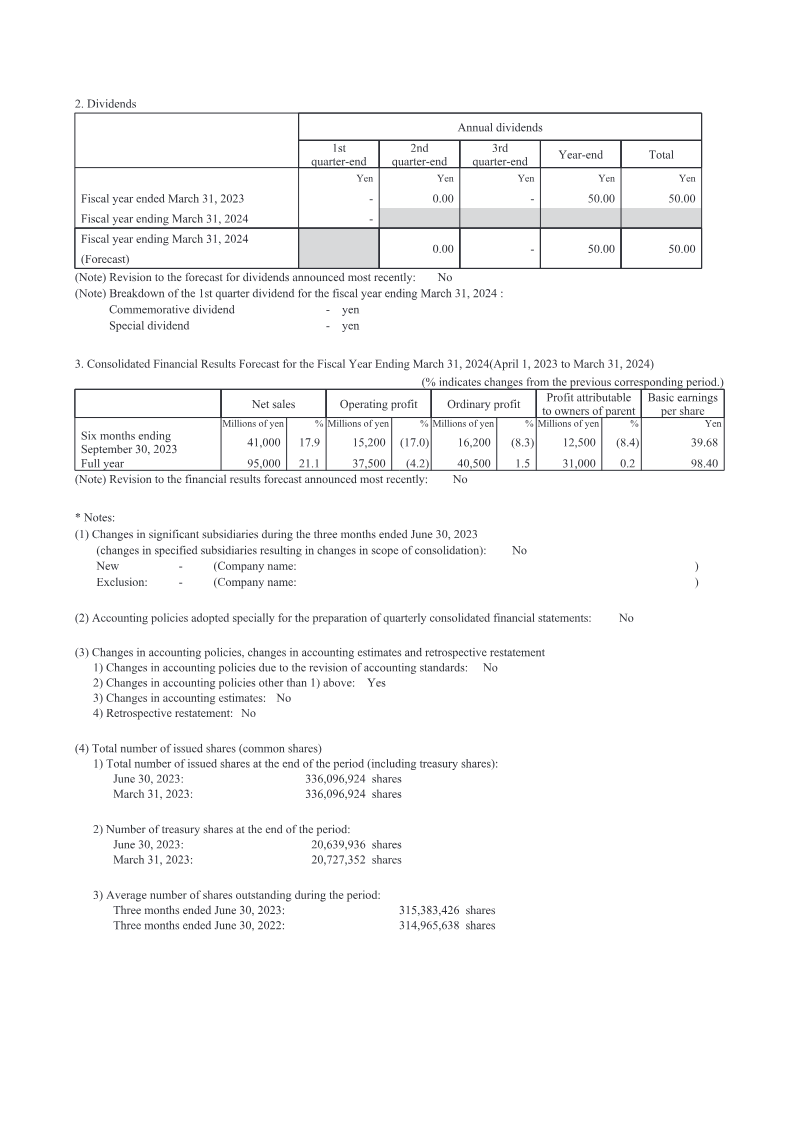

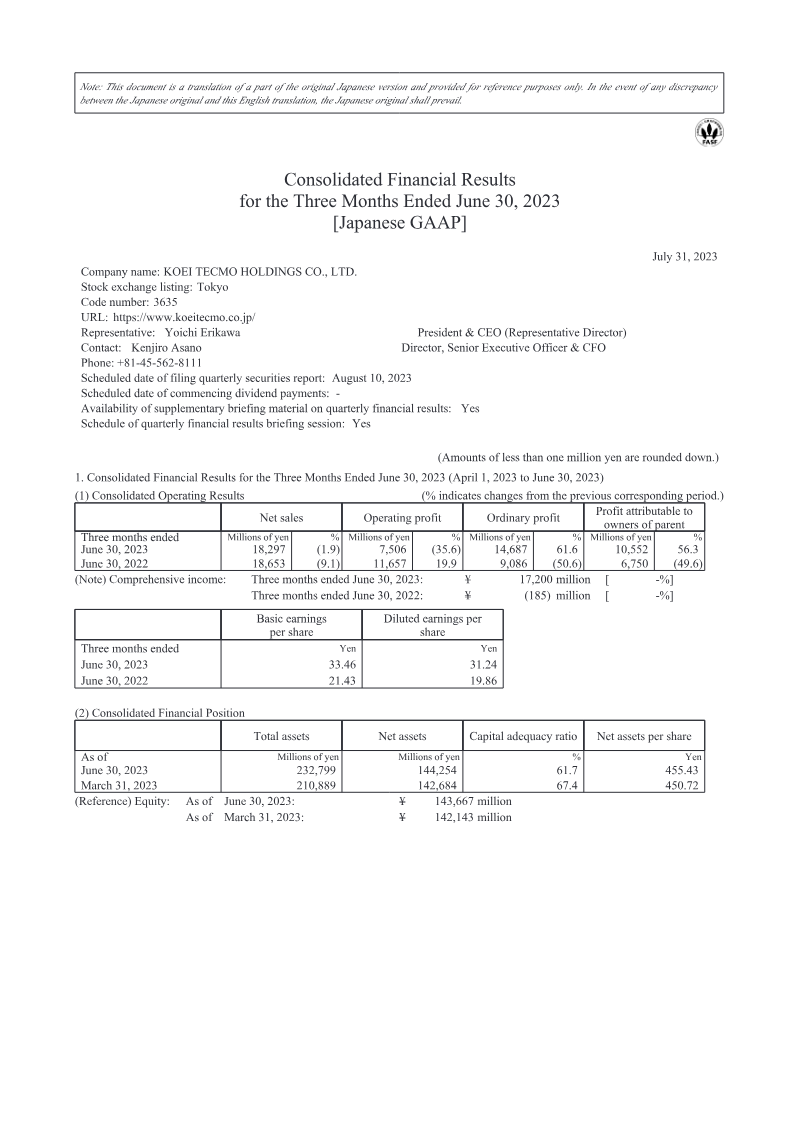

Consolidated Financial Results: Three Months Ended June 30, 2023

The quarterly consolidated financial results for the three months ended June 30, 2023 show a modest decline in net sales to ¥18.30 billion from ¥18.65 billion a year earlier, representing a 1.9 % drop. Operating profit fell sharply to ¥7.51 billion, a 35.6 % decrease from the prior year’s ¥11.66 billion, while ordinary profit contracted to ¥10.55 billion from ¥14.69 billion, a 28.5 % decline. Profit attributable to owners of the parent company decreased to ¥6.75 billion versus ¥10.55 billion, a 36.3 % reduction. Basic earnings per share fell to ¥33.46 from ¥21.43, and diluted earnings per share dropped to ¥31.24 from ¥19.86. Total assets increased to ¥232.80 billion, driven largely by higher investment securities and cash balances, while net assets rose to ¥144.25 billion, improving the capital adequacy ratio from 67.4 % to 61.7 %. Shareholders’ equity remained stable at ¥144.13 billion, with retained earnings slightly lower due to the operating loss. The company forecasts full‑year 2024 net sales at ¥95.00 billion, a 21.1 % increase over the previous year, and operating profit at ¥37.50 billion, a 4.2 % decline from the prior year’s ¥40.50 billion. Ordinary profit is projected at ¥31.00 billion, a 0.2 % rise, and earnings per share at ¥98.40. The report covers Japan‑based operations under Japanese GAAP for the fiscal year ending March 31, 2024. Methodology follows standard quarterly consolidation procedures with no changes in accounting policies or significant subsidiary adjustments during the period. The company issued 336 million shares, with an average of 315 million shares outstanding during the quarter.

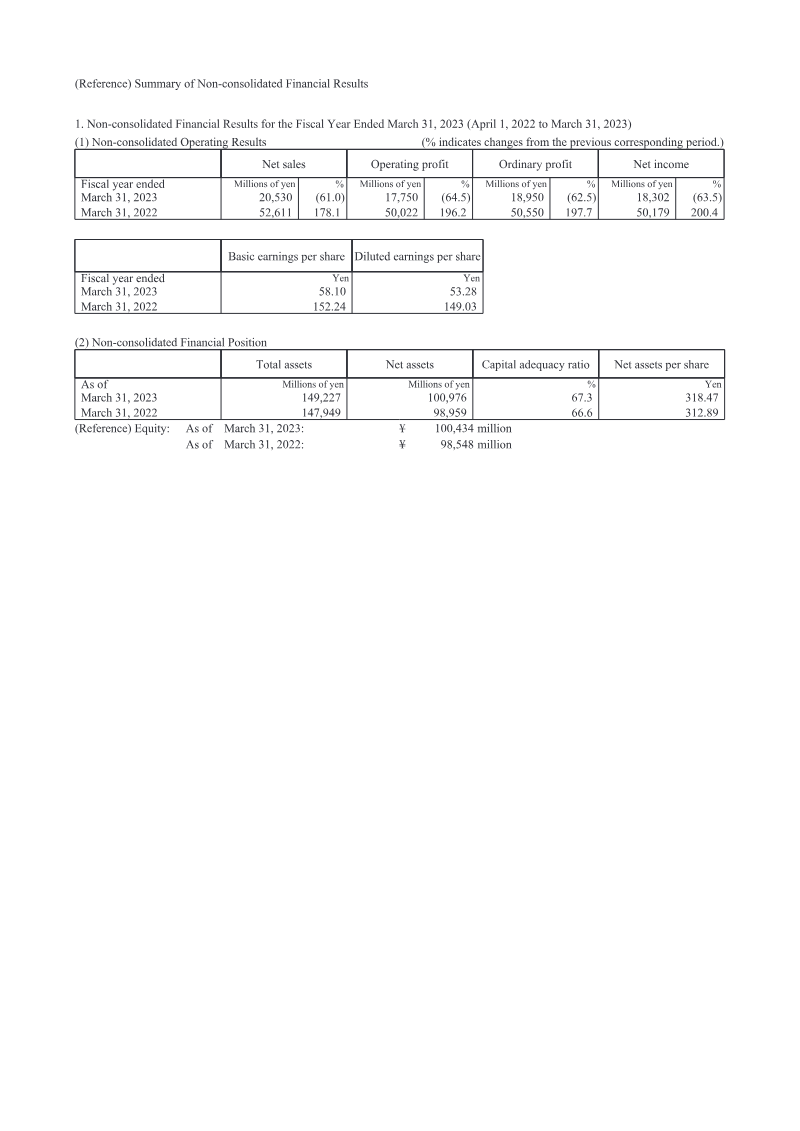

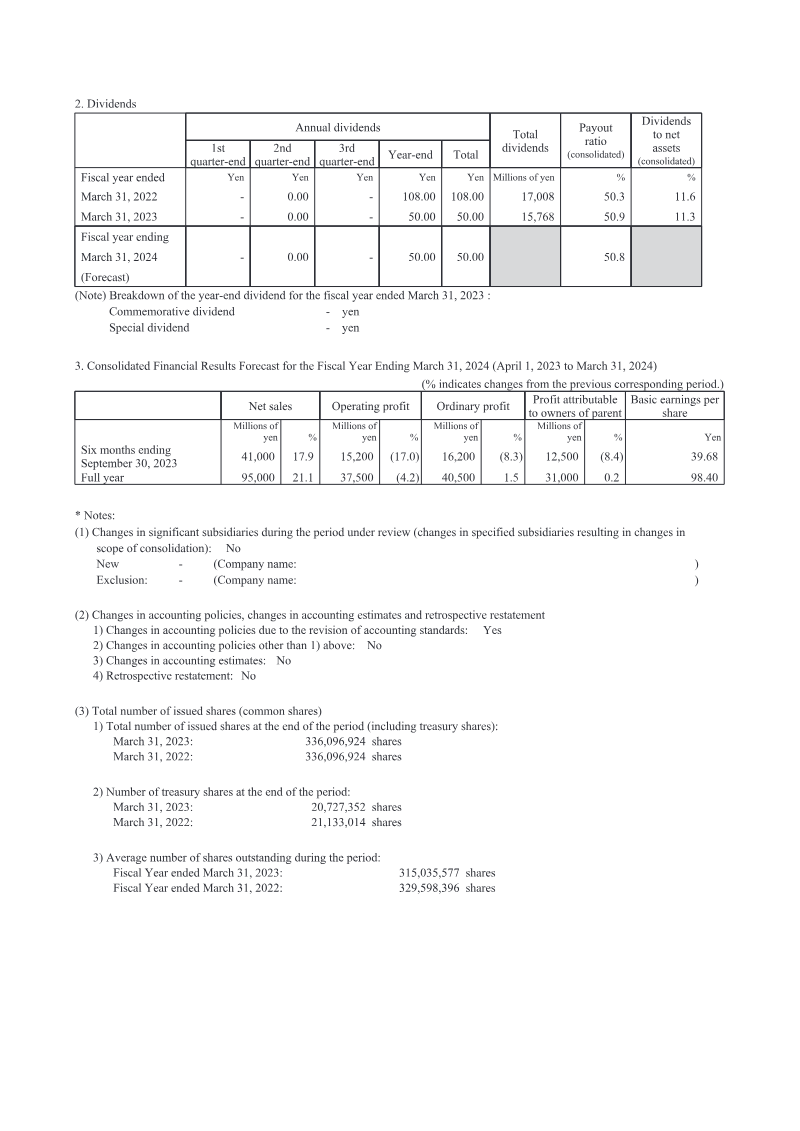

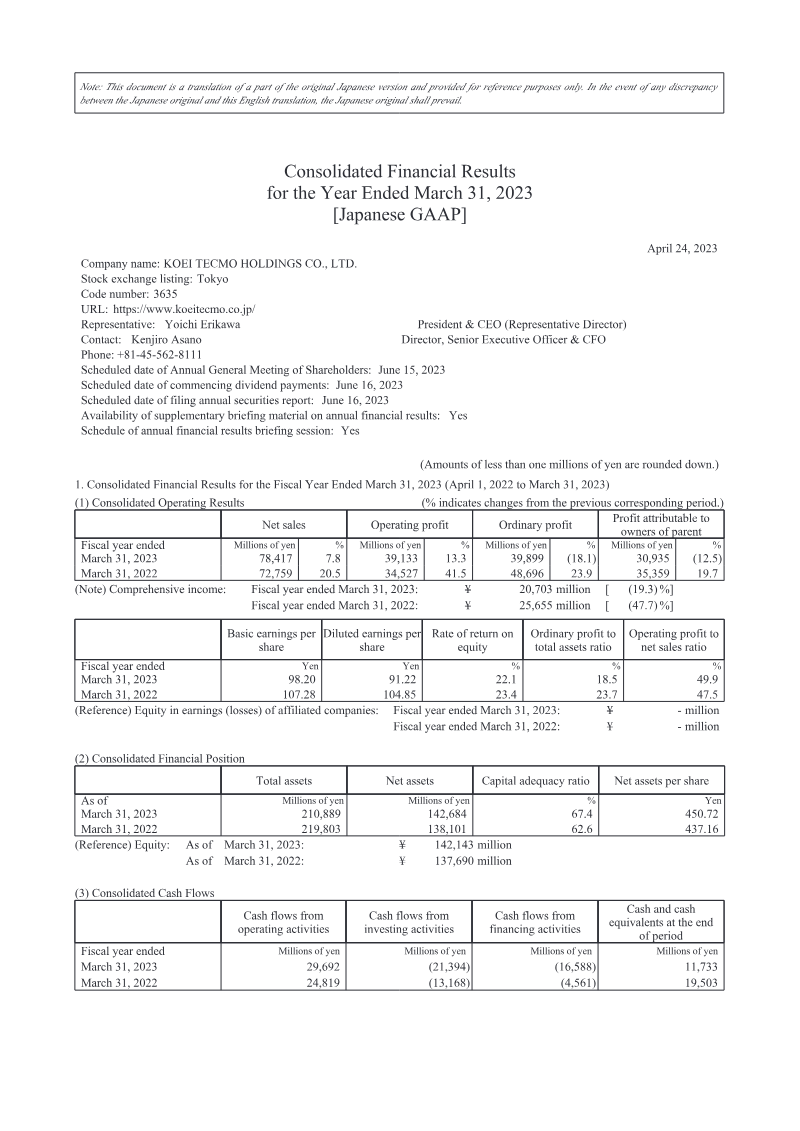

Koei Tecmo