Related Documents

Report

2025 Global Games Market Report

The global games market is entering a period of moderate maturation, with total revenue projected to reach $188.8 billion in 2025, a 3.4% increase over the previous year. The industry now serves 3.6 billion players, reflecting a 4.4% year-over-year expansion. While mobile gaming maintains its dominance, accounting for $103.0 billion or 55% of total revenue, console gaming is poised for the strongest growth at 5.5%, reaching $45.9 billion. PC gaming remains a stable pillar with $39.9 billion in revenue. Despite the growth in player counts, average spend per payer is experiencing a slight decline, signaling a strategic pivot toward maximizing engagement and retention within saturated markets rather than relying solely on aggressive monetization. Strategic success in this environment increasingly depends on long-tail engagement and the effective management of post-launch content. Data indicates that releasing single-player titles during the second quarter yields 34% higher engagement compared to the saturated holiday season. Furthermore, simultaneous multi-platform launches significantly outperform staggered releases, and titles exiting Early Access after a six-month window demonstrate superior acquisition results. Developers are also increasingly leveraging remakes and remasters to mitigate rising development costs, while user-generated content platforms like Roblox continue to expand as foundational ecosystems for daily active users. Geographically, the market continues to diversify, with Latin America emerging as a notable growth region projected to reach $8.3 billion, driven primarily by mobile adoption. The industry’s analytical framework, which focuses on consumer spending on software and services, highlights that player attrition typically stabilizes after 12 weeks. Consequently, long-term commercial viability is now inextricably linked to aligning content updates and discounting strategies with this post-launch retention curve, ensuring that community support remains as critical as initial sales performance.

NewzooSept 2025

Report

Mobile Gaming Market Outlook 2022

The global mobile gaming landscape has entered a period of stabilization following pandemic-era surges, with quarterly downloads maintaining a steady baseline of 14 billion. Although total revenue experienced a 6% year-over-year decline to $21.2 billion in early 2022, the market remains significantly larger than its pre-pandemic state. Casual games continue to lead in volume, representing 80% of all downloads, yet Mid-Core titles remain the primary economic engine, generating 60% of total player spending. While the United States maintains its position as the leading consumer market, the Asia-Pacific region exerts increasing influence, evidenced by Taiwan’s rise to the fifth-largest global market and the region's dominance in high-monetization genres like MMORPGs and Card Battlers. Strategic advertising and intellectual property integration have become essential for navigating this competitive environment. Strategy and RPG titles are increasingly prioritizing YouTube for share of voice, while the acquisition of MoPub by AppLovin has shifted the advertising landscape for strategy games. Success in the rapidly growing Card Battler sub-genre, which earns 62% of its revenue from the APAC region, is largely driven by high-performing titles like Yu-Gi-Oh! Master Duel and the effective use of Live Ops and Season Passes. Furthermore, cross-media synergies, such as the impact of the Netflix series Arcane on game downloads, demonstrate the power of multimedia IP in driving user acquisition. The market outlook suggests a temporary correction phase with a projected return to growth by 2023. While Asian markets currently account for 80% of MMORPG revenue, Western interest is growing, as seen with the successful U.S. launch of Diablo Immortal. Similarly, the Real-Time Strategy sector is seeing a geographic shift, with China overtaking the U.S. as the top market for the sub-genre. Future expansion across these segments will likely depend on localized IP collaborations and sophisticated user acquisition strategies tailored to specific regional preferences.

Sensor TowerMay 2022

Report

Market Outlook 2022

The analysis outlines a 2022 outlook for the global mobile‑gaming market, emphasizing that quarterly installs have plateaued at roughly 14 billion after a pandemic‑driven surge, with casual titles still accounting for about 80 % of downloads. Revenue dynamics have shifted: mid‑core games now generate 60 % of total earnings, while overall mobile‑game revenue fell 7 % year‑over‑year in Q1 2022, marking the first decline since the industry’s rapid expansion. The United States remains the largest spend market, yet Asia‑Pacific regions—especially Taiwan and Brazil—exhibit the fastest growth rates. Advertising spend analysis reveals that role‑playing games dominate iOS channels, with YouTube capturing an 8.2 % share of voice and exceeding 10 % in Q2 2022; Android spend lags across all networks. Card‑battler titles emerge as the fastest‑growing sub‑genre, driven largely by Japan and China, which together account for 62 % of player spending. Yu‑Gi‑Oh! Master Duel leads launch revenue, reaching $80 million in five months and achieving a worldwide revenue per day of $20—twice that of its nearest competitor. MMORPGs hold the second‑largest spending position globally, with Diablo Immortal topping U.S. spend at $22 million in H1 2022 and maintaining a modest 10 % share of U.S. MMORPG installs. In the United States, Diablo Immortal generated over $30 million in its first six weeks and captured 3.2 % of mid‑core revenue, yet U.S. players still lag behind Asian markets where Lineage M and Odin: Valhalla Rising amassed $225–$350 million in the same period. The report underscores that U.S. MMORPG revenue represents only about 4 % of the global total, highlighting the critical need for localized market strategies in future mobile RPG releases.

Sensor TowerJan 2022

Report

Vietnam Mobile Gaming 2025: The Next Billion-Dollar Frontier in Southeast Asia

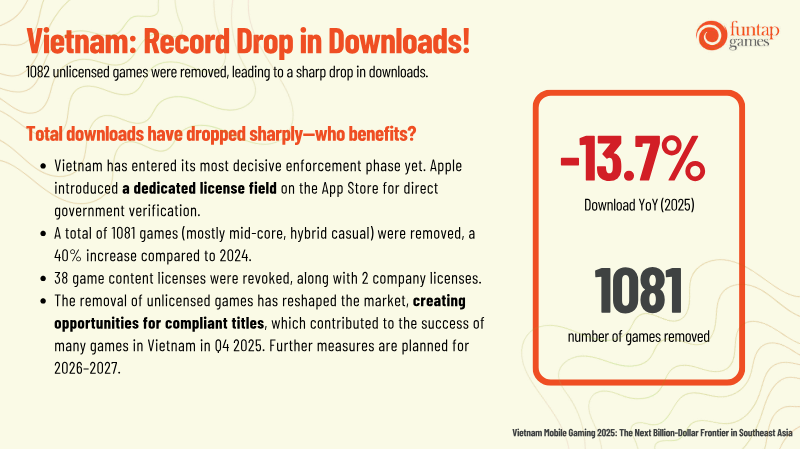

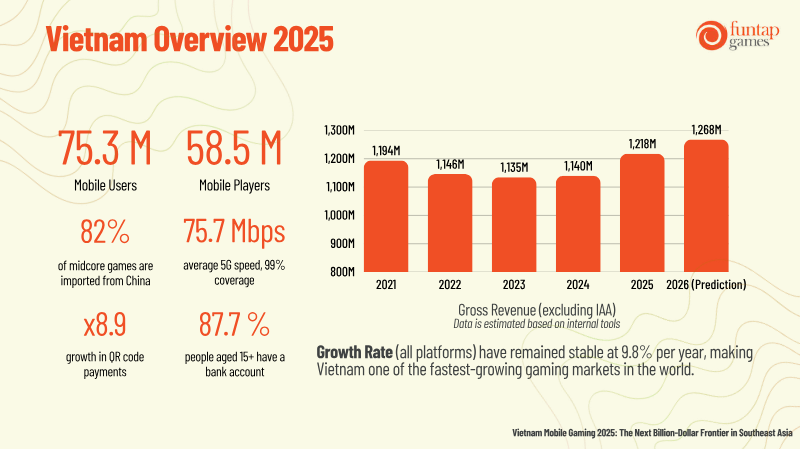

The report argues that Vietnam’s mobile gaming sector will reach a billion‑dollar valuation by 2025, driven by an expanding user base and high spending per download. In 2023, 1.1 billion mobile users and 900 million mid‑core players generated gross revenue of approximately US$1.3 billion, with a compound annual growth rate of 9.8 % across all platforms. The analysis attributes this surge to rapid mobile penetration, widespread 5G coverage (average speed 75.7 Mbps), and a growing banking‑linked payment ecosystem that facilitates in‑app purchases. A key finding is the regulatory shift that began in 2025, when Apple introduced a mandatory license field and the Vietnamese government revoked 1,081 unlicensed titles. This crackdown reduced total downloads by 13.7 % but created a more favorable environment for compliant mid‑core games, which now dominate the market. The report’s methodology involved surveying 250 representative titles with significant download volumes, measuring D1 and D7 retention, playtime, and revenue. Data were cross‑validated with internal tools and third‑party analytics to correct discrepancies common in the local market. Geographically, the study focuses on Vietnam but benchmarks against other Southeast Asian markets. It notes that while daily playtime is rising across the region, Vietnam’s revenue per download exceeds that of the Philippines by at least 28 %. The report concludes that early licensing and a focus on social, competitive, and narrative‑rich mid‑core experiences—particularly 4X strategy, MOBA, squad RPG, MMORPG, and battle royale genres—will be critical for publishers seeking sustainable growth in the Vietnamese market.

InvestGameFeb 2026