Related Documents

Financial

AppLovin Financial Update: Q1 2026

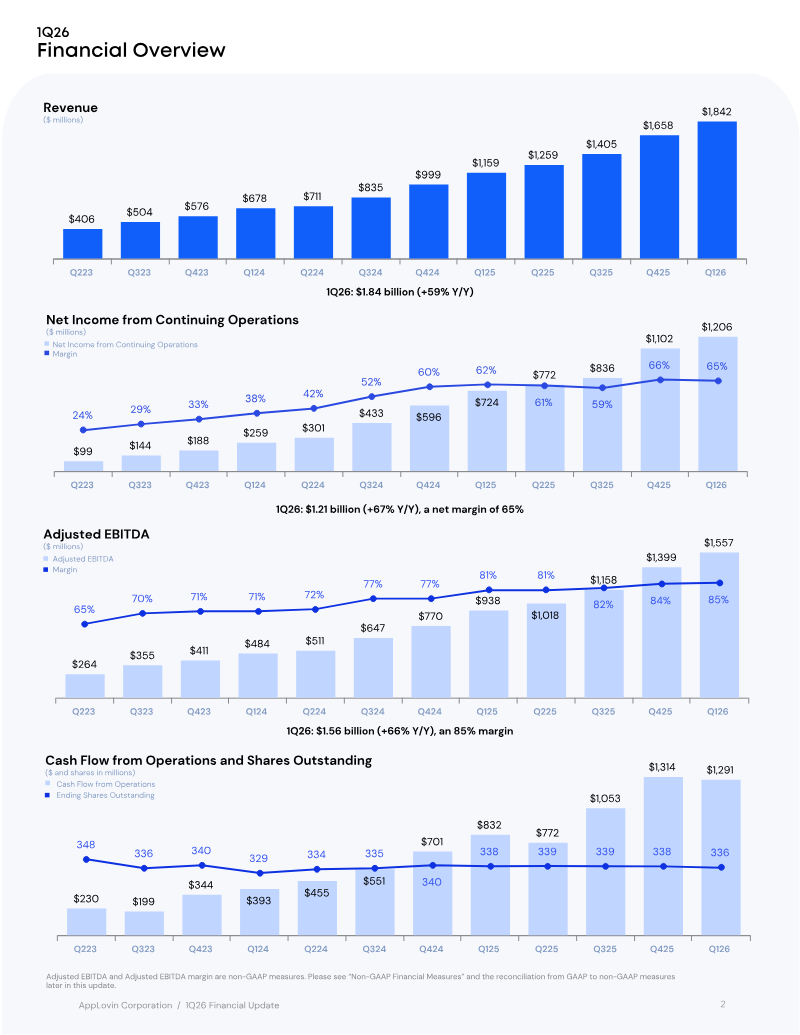

AppLovin’s Q1 2026 financial update reports a revenue of $1.842 billion, up 59% year‑over‑year, and net income from continuing operations of $1.206 billion, a 66% increase to a net margin of 65%. Adjusted EBITDA reached $1.557 billion, an 85% margin, reflecting a 66% rise from the prior year. Cash flow from operations matched Adjusted EBITDA at $1.556 billion, underscoring strong operating liquidity. Shares outstanding averaged 1.053 million, with diluted earnings per share of $3.56. The company’s balance sheet shows cash and equivalents at $2.759 billion, up from $2.487 billion, and total assets of $7.708 billion versus $7.260 billion a year earlier. Long‑term debt remained stable at $3.514 billion, while equity rose to $2.363 billion from $2.135 billion. Operating expenses grew modestly, with research and development increasing to $94 million from $56 million, while sales and marketing rose slightly to $60.8 million. Methodologically, the update presents both GAAP and non‑GAAP measures; Adjusted EBITDA is defined by excluding items such as stock‑based compensation, restructuring costs, and goodwill impairment. The reconciliation table shows cumulative Adjusted EBITDA margins climbing from 65% in Q1 2025 to 85% in Q1 2026, driven by revenue growth and controlled cost expansion. The update covers the United States market for Q1 2026, with data drawn from audited financial statements and internal reconciliations.

AppLovinMay 2026

Report

State of Gaming 2026

The 2026 State of Gaming analysis demonstrates a shifting landscape in which mobile gaming remains the largest driver of downloads—approximately 50 billion in 2025—but its growth rate is slowing. Revenue, however, continues to climb as monetization models mature and lifetime value deepens, especially within hybrid‑casual titles that now generate the most incremental income. In contrast, PC and console platforms experience record revenue growth, with Steam’s premium segment up 32 % and blockbuster releases such as Battlefield 6 capturing significant market share from incumbents. Shooter downloads on these platforms have plateaued, suggesting new titles are primarily cannibalizing existing audiences rather than expanding the category. Genre‑specific dynamics reveal that strategy games are the only mobile genre to grow in downloads, driven by 4X titles from Eastern developers. Action and shooter games dominate PC/console gains, while hyper‑casual remains the largest download engine but shows a notable lift in time spent, particularly in Tier 2 markets. Casual titles face declining day‑7 retention, indicating a stickiness challenge that could erode long‑term player value. Live‑ops and acquisition strategies have evolved toward retention‑focused events, multi‑tier season passes, and expedition‑style rewards. These mechanisms now represent the most reliable revenue drivers across competitive genres such as RPG, action, and simulation. Advertising spend remains concentrated on social channels—YouTube, Facebook/Instagram—and high‑attention formats like video, playable, and rewarded ads. Battlefield 6’s pre‑launch spend surpassed Call of Duty titles, leveraging Facebook, Reddit, and desktop display, while its post‑launch strategy pivoted to YouTube with cinematic, celebrity‑hook creatives. Geographically, the U.S. market shows a skew toward lifestyle and puzzle categories despite lower IAP shares, whereas casino titles exhibit higher spend‑to‑revenue efficiency. Overall, the industry is moving from acquisition toward deeper monetization per user, with indie shooters and simulation titles gaining traction amid intense competition in the shooter segment.

Sensor TowerApr 2026

Report

2026 Global Non‑Gaming App Trends Report

The report argues that non‑gaming mobile applications are experiencing accelerated growth driven by AI integration, short‑form content, and intensified user acquisition competition. Key findings show that Android dominates download volume—particularly in Utilities (79 % of installs) and Life Services (58 %)—while iOS generates a higher share of revenue, especially in Finance & Business (56 % of iOS revenue) and Life Services (57 %). In 2025, AI‑focused apps such as ChatGPT (+1,340 %) and Perplexity (+3,613 %) achieved the highest year‑over‑year download growth, and Short Drama titles like Kuku TV (+45 % k) and RapidTV (+498 %) recorded explosive revenue increases, with AI Social apps (e.g., Character AI +918 %) also driving significant monetization. User acquisition activity expanded across all major categories, with Life Services (+42 %) and Finance & Business (+43.5 %) leading the rise in app counts. Smart bidding adoption surged, with Target ROAS spend increasing by 50 % and Target CPE spending up 57 %, particularly in Utilities and Entertainment. Cost‑per‑install (CPI) analysis revealed that E‑Commerce on Android commands a 3× premium, while Finance & Business on iOS reaches 4.6×, underscoring high competition for transactional users. Monetization patterns shift toward in‑app advertising (IAA), dominating across Education, Utilities, and Entertainment. Video formats—rewarded and interstitial—outperform banner ads by 128–165× eCPM, with North America delivering the highest rewarded video eCPMs (up to 11.8× in Short Drama). The report covers global markets excluding Mainland China from January to December 2025, drawing on anonymized data from Mintegral and Insightrackr across 100+ key app categories.

MintegralApr 2026

Report

State of Mobile 2026

The 2026 State of Mobile report demonstrates that the global mobile ecosystem remains mature yet increasingly monetized, with 2025 in‑app purchase (IAP) revenue reaching $85.6 billion—a 21 % year‑over‑year rise that now places non‑game apps ahead of games for the first time. Generative AI and short‑form drama have become the fastest‑growing subgenres, driving double‑digit IAP growth; AI assistants such as ChatGPT alone generated $3.4 billion in 2025, while short‑drama apps captured more than ten percent of global video‑entertainment time. These categories also show a shift from acquisition to retention, with session volumes outpacing downloads and time spent tripling in AI apps. Hybrid‑casual and hyper‑casual games continue to lead revenue growth, especially in Tier 2 markets where downloads are falling but engagement is surging. Publishers targeting these segments can capture higher revenue per user, though they face tighter ad‑spend competition and a move toward high‑attention formats. In the gaming web arena, Roblox dominates with 74 % of game‑publisher site visits in 2025, underscoring the importance of product‑centric web design. Beyond entertainment, general‑shopping apps such as Temu and Amazon maintain massive download volumes, with grocery and buy‑and‑sell subgenres growing 5 % and 4 % YoY, respectively. Food & drink apps hit a record 2.4 billion downloads in 2025, driven largely by emerging markets like India and the Middle East. Mobility and sports apps also show notable shifts: Waymo’s standalone app captured 15 % of rideshare MAUs in key U.S. metros, while DFS‑style sports betting apps now command 80 % of the betting‑app MAU share, reflecting regulatory impacts and new market entrants. Overall, the report covers a global geographic scope with particular emphasis on the U.S., India, Western Europe, and emerging Tier 2 markets. It spans 2025 data with forward‑looking insights for 2026, highlighting AI’s transformative role across monetization, user engagement, and competitive dynamics in the mobile industry.

Sensor TowerApr 2026