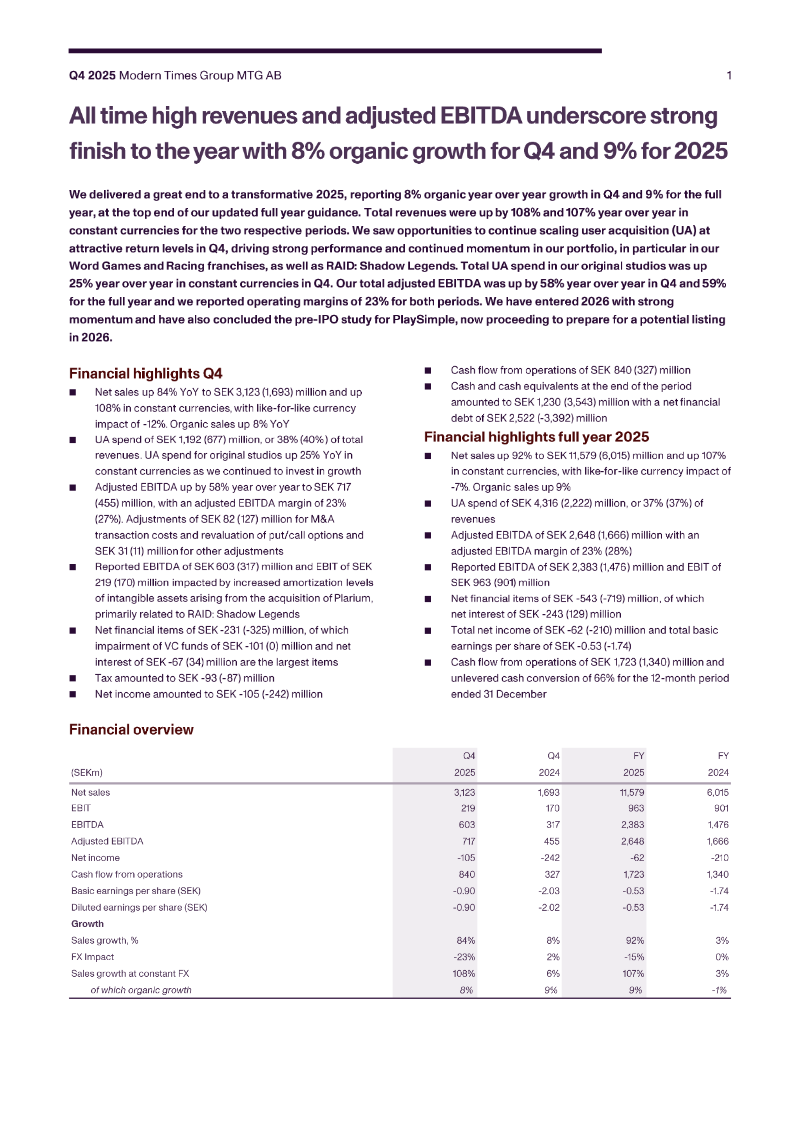

ReportMintegral

2026 Global Non‑Gaming App Trends Report

5 Apr 202633 pages~20 min full read

AI-focused applications experienced massive 2025 growth, led by Perplexity (+3,613%), ChatGPT (+1,340%), and Character AI (+918%).

See it on page 9Short Drama apps like RapidTV (+498%) and Kuku TV (+45k%) are driving explosive revenue, with North American rewarded video eCPMs for this category reaching up to 11.8x.

See it on page 26Android leads in global download volume, particularly in Utilities (79%) and Life Services (58%), while iOS captures the majority of revenue in Finance & Business (56%) and Life Services (57%).

See it on page 7User acquisition competition is intensifying, evidenced by a 50% increase in Target ROAS spending and a 57% rise in Target CPE spending, particularly within Utilities and Entertainment.

See it on page 13Cost-per-install (CPI) premiums remain high for transactional users, reaching 3x for E-Commerce on Android and 4.6x for Finance & Business on iOS.

See it on page 14In-app advertising (IAA) is the dominant monetization model for Education, Utilities, and Entertainment, with video formats outperforming banner ads by 128–165x in eCPM.

See it on page 23Market saturation is increasing as the number of apps in Life Services and Finance & Business grew by 42% and 43.5% respectively throughout 2025.

See it on page 11The report argues that non‑gaming mobile applications are experiencing accelerated growth driven by AI integration, short‑form content, and intensified user acquisition competition. Key findings show that Android dominates download volume—particularly in Utilities (79 % of installs) and Life Services (58 %)—while iOS generates a higher share of revenue, especially in Finance & Business (56 % of iOS revenue) and Life Services (57 %). In 2025, AI‑focused apps such as ChatGPT (+1,340 %) and Perplexity (+3,613 %) achieved the highest year‑over‑year download growth, and Short Drama titles like Kuku TV (+45 % k) and RapidTV (+498 %) recorded explosive revenue increases, with AI Social apps (e.g., Character AI +918 %) also driving significant monetization.

User acquisition activity expanded across all major categories, with Life Services (+42 %) and Finance & Business (+43.5 %) leading the rise in app counts. Smart bidding adoption surged, with Target ROAS spend increasing by 50 % and Target CPE spending up 57 %, particularly in Utilities and Entertainment. Cost‑per‑install (CPI) analysis revealed that E‑Commerce on Android commands a 3× premium, while Finance & Business on iOS reaches 4.6×, underscoring high competition for transactional users.

Monetization patterns shift toward in‑app advertising (IAA), dominating across Education, Utilities, and Entertainment. Video formats—rewarded and interstitial—outperform banner ads by 128–165× eCPM, with North America delivering the highest rewarded video eCPMs (up to 11.8× in Short Drama). The report covers global markets excluding Mainland China from January to December 2025, drawing on anonymized data from Mintegral and Insightrackr across 100+ key app categories.