Related Documents

Report

Level Up: A Guide to Succeed in Asia’s Gaming Market

Asia has established itself as the epicenter of the global gaming industry, driven by a mobile-first population exceeding 1.5 billion players. The region’s market is characterized by the dominance of free-to-play models, which account for nearly 99% of mobile revenue and all top-grossing titles. While China and Japan lead in total revenue, Japan maintains the highest value per user with an average revenue per download of $12.84. Growth is increasingly fueled by the female demographic, which expanded to 500 million players by 2019 and contributes nearly 40% of total mobile gaming revenue. This shift necessitates more inclusive storylines and diverse development teams to capture a demographic that is currently outgrowing its male counterpart. The competitive landscape is defined by the rapid ascent of mobile esports, with Asia generating 68% of the sector's global revenue. Southeast Asia, in particular, has seen a 244% increase in tournament prize pools, signaling a transition from casual play toward complex, competitive genres like MOBAs and Battle Royales. Despite high interest, a significant gap remains between esports viewership and active participation, representing a massive untapped opportunity for developers. Success in these markets requires sophisticated monetization strategies, such as hybrid models combining gacha mechanics, battle passes, and rewarded video ads to accommodate varying income levels across the territory. Navigating the Asian market demands deep localization that extends beyond language to include cultural customs, religious sensitivities, and technical optimization for diverse hardware. While Japan and South Korea remain dominated by local developers and legacy RPG franchises, India and Southeast Asia offer high-growth potential for international titles that provide "lite" versions for accessible play. To achieve long-term engagement, developers must leverage local influencers and community-driven gameplay, ensuring that titles resonate with the specific pop culture trends and infrastructure capabilities of each unique sub-region.

NewzooJan 2020

Report

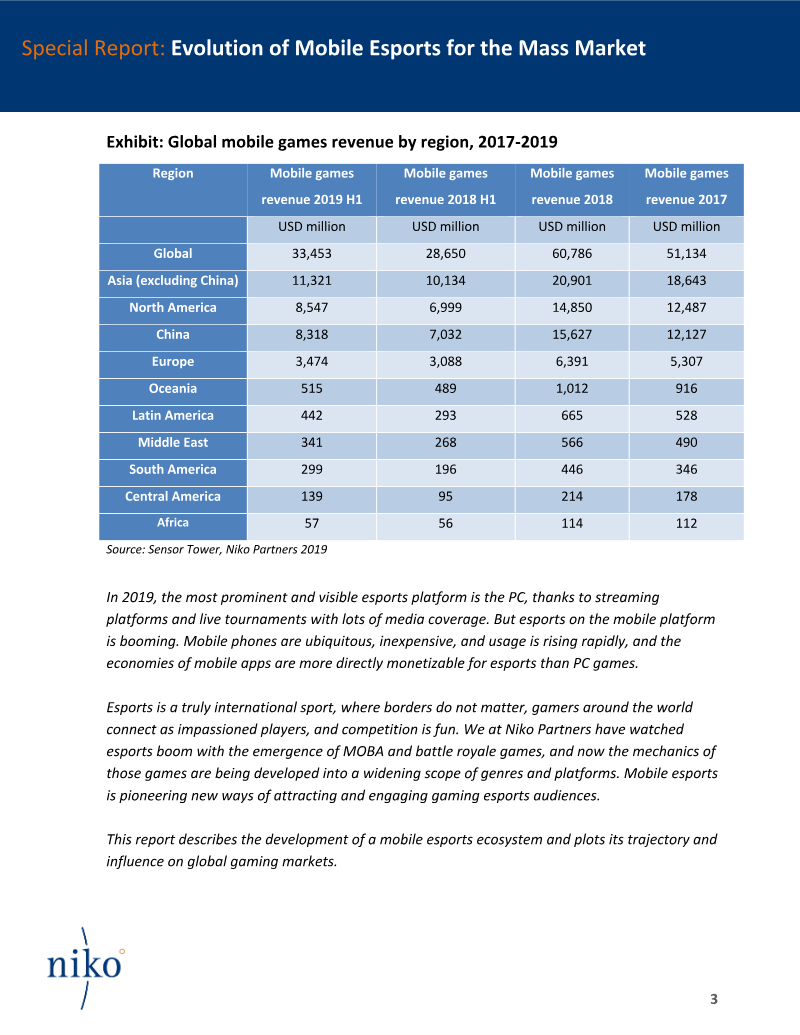

Evolution of Mobile Esports for the Mass Market

Mobile esports is positioned to become the primary catalyst for growth in the digital games industry over the next five years, leveraging a global player base of 2.53 billion that already surpasses the combined reach of PC and console gaming. In 2018, mobile esports titles generated $15.32 billion in revenue, representing over a quarter of the total mobile market. This expansion is driven by high smartphone penetration and a fundamental shift from high-profile spectator events toward a pervasive ecosystem of regional and online-only competitions. By lowering barriers to entry, the sector has successfully attracted a more diverse and gender-balanced audience than traditional competitive gaming platforms. The industry is currently transitioning from a publisher-funded marketing tool into a scalable mass-market powerhouse. While professional PC esports historically dominated revenue, mobile esports is rapidly closing the gap, fueled by sophisticated monetization strategies including media rights, sponsorships, and microtransaction-based models like season passes. Asia serves as the epicenter of this evolution, with China and Southeast Asia hosting the most concentrated markets for competitive mobile titles. Significant investments from traditional sports franchises and the expansion of media rights into mainstream cable television further signal the professionalization and maturation of the sector. Technological advancements in 5G and cloud gaming are disrupting the historical dominance of PC titles by delivering high-quality competitive experiences on accessible hardware. This technological shift, combined with strong government support in Asian markets, has led to explosive growth, exemplified by a 44.5% revenue increase in top Belt and Road markets during the first half of 2019. As industry leaders establish franchised leagues and record-breaking prize pools, the mobile esports model is proving more sustainable and participatory than its predecessors. Ultimately, the sector’s massive reach and superior monetization capabilities ensure its trajectory to overtake PC esports as the dominant global competitive gaming format.

Niko PartnersJan 2019

Report

For the Win: Breaking Down the Preferences of Asia's Mobile Gamers

Asia represents the world’s most significant mobile gaming hub, housing over half of the global player base and generating the majority of the industry's mobile revenue. The primary objective of this analysis is to examine the distinct player preferences, cultural influences, and market regulations across five key regions: China, Japan, South Korea, India, and Southeast Asia. By evaluating top-grossing titles and genre shifts through the first half of 2020, the findings illustrate a broader regional transition from casual play toward complex, competitive, and socially-driven experiences. China remains the largest market, characterized by the successful migration of PC intellectual properties to mobile and a regulatory environment that necessitates domestic partnerships. In contrast, Japan’s market is defined by a deep-rooted console history and the pervasive influence of anime and manga aesthetics, with RPGs accounting for nearly half of its mobile revenue. South Korea leverages its robust 5G infrastructure and "PC bang" culture to sustain a market dominated by high-fidelity MMORPGs. Meanwhile, India and Southeast Asia emerge as high-growth regions where young populations and increasing smartphone accessibility are fueling a massive surge in mobile esports and battle royale titles. The data reveals that localization involves more than translation; it requires integrating local folklore, respecting religious customs, and optimizing for hardware constraints. For instance, "lite" versions of games are essential for market penetration in India, while community-centric features are vital for success in Southeast Asia. Across all regions, the rise of mobile esports is a dominant trend, with competitive titles increasingly displacing traditional genres in the top-grossing charts. The methodology utilizes data from Niko Partners, incorporating market models, five-year forecasts, and qualitative surveys from a panel of millions of consumers across Asia. The analysis covers the period from 2016 through June 2020, drawing on data from retailers, app markets, and interviews with industry executives to provide a comprehensive view of the mobile landscape.

Niko PartnersJan 2020

Report

A Rising Market: Southeast Asia

Southeast Asia represents a rapidly accelerating segment of the global esports market, characterized by high growth rates in both viewership and revenue. Between 2019 and 2024, the region is projected to see a compound annual growth rate (CAGR) in audience size that significantly outpaces global averages, with year-over-year increases reaching as high as 18.2%. This expansion is driven by a mobile-first gaming culture where 82% of the online population plays mobile games and 39% of players identify mobile as their primary platform. Key markets fueling this trend include Indonesia, Vietnam, the Philippines, Thailand, Malaysia, and Singapore. The regional ecosystem is heavily influenced by mobile-centric titles, specifically Mobile Legends: Bang Bang, Garena Free Fire, and PUBG Mobile. These three games accounted for roughly half of all global esports hours watched for those titles on Twitch and YouTube Live during the first half of 2021. Revenue streams in the region mirror global trends, with sponsorship serving as the primary contributor, supported by media rights, publisher fees, and digital goods. Government intervention also plays a critical role in market maturation, with initiatives like the Youth Esports Program in the Philippines and the integration of esports into the 30th SEA Games as a medal event. Data for these findings was sourced from Newzoo’s 2021 Global Esports and Live Streaming Market Report and Consumer Insights. The methodology utilized a Major City Approach for most Southeast Asian nations to represent active internet users aged 10-50, while Singapore data covered the general online population within that age bracket. The findings conclude that improved internet infrastructure and the accessibility of mobile devices are the primary catalysts for long-term engagement and the continued attraction of non-endemic brand sponsorships to the region.

NewzooJul 2021