Related Documents

Report

The Metaverse, Blockchain Gaming, and NFTs: Navigating the Internet’s Uncharted Waters

The metaverse represents a fundamental shift from a two-dimensional internet toward a persistent, three-dimensional social ecosystem driven by gamified virtual spaces. This evolution is currently led by "game as a platform" models, most notably Roblox, which leverages tens of millions of daily active users to host diverse commercial and social experiences. While major global brands in fashion, luxury, and finance are increasingly investing in "direct-to-avatar" economies and digital real estate to reach younger, digital-native demographics, the sector faces significant economic and technical hurdles. High developer take rates, consistent net losses among platform leaders, and networking limitations that prevent massive simultaneous user scaling remain primary obstacles to long-term growth. The integration of blockchain technology and non-fungible tokens (NFTs) has introduced new economic paradigms, such as the "Play-to-Earn" model. Although these games accounted for nearly half of all decentralized application wallet activity by late 2021, their growth is largely concentrated in emerging markets where users treat gaming as an income-generating activity. The sustainability of these ecosystems is currently challenged by high entry barriers and a prioritization of financial speculation over core gameplay quality. For the industry to mature, it must transition toward higher-quality experiences and more robust virtual economies that offer genuine utility beyond profile-picture status symbols. Mass adoption of these decentralized virtual worlds is currently constrained by technical and regulatory friction. Interoperability across different platforms remains a theoretical goal rather than a functional reality, while high transaction fees on networks like Ethereum and environmental concerns create additional barriers. Furthermore, the industry must navigate complex legal landscapes regarding digital privacy, content moderation, and the protection of intellectual property. Despite a cooling of initial market hype following a crypto correction in 2022, the long-term trajectory points toward a transmedia future where digital assets and virtual identities are central to global commerce and social interaction.

NewzooJan 2022

Report

Blockchain Industry Report: October 2022

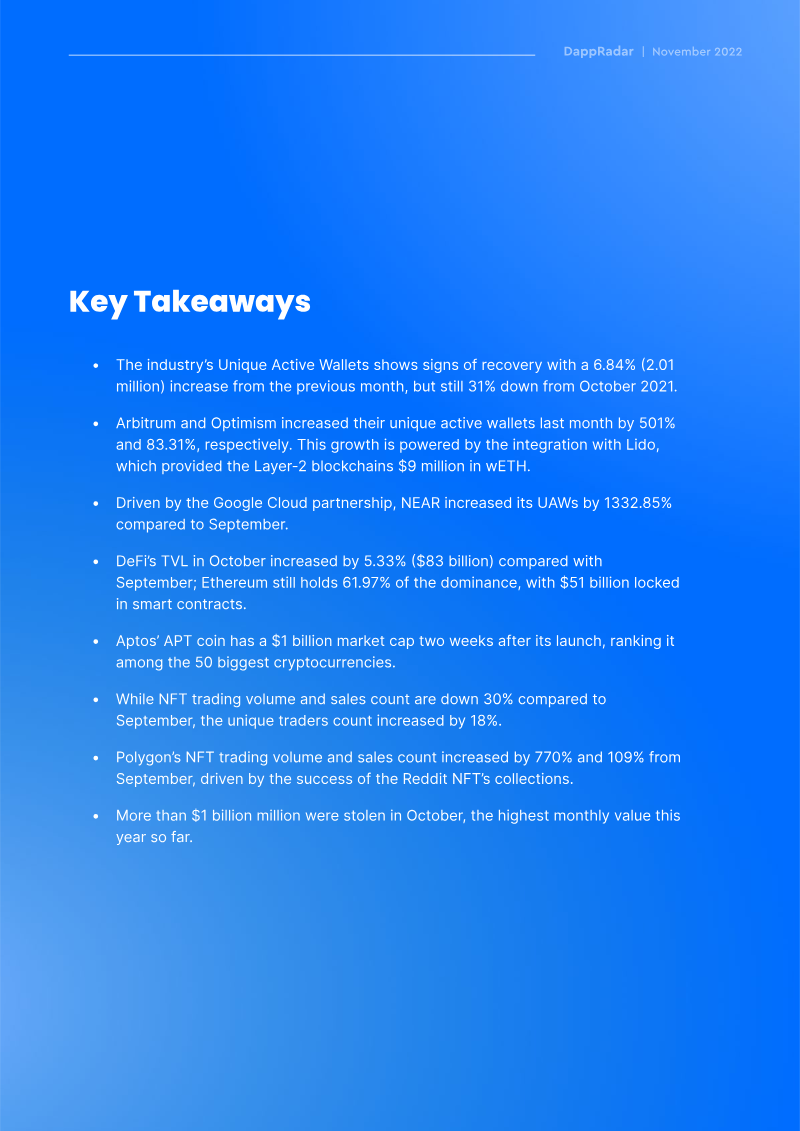

The analysis evaluates the health and dynamics of the blockchain ecosystem during October 2022, revealing a sector in transition marked by divergent growth patterns across applications, platforms, and asset classes. Overall user engagement rose, with unique active wallets for decentralized applications increasing 6.8 percent to just over two million, driven primarily by explosive adoption on Arbitrum, Optimism and a dramatic surge on NEAR following its partnership with Google Cloud. By contrast, the gaming segment and Ethereum’s core wallet base contracted, falling 2 percent and 4.5 percent respectively, underscoring a shift of activity toward emerging layer‑2 solutions. DeFi continued its rebound, with total value locked climbing 5.3 percent to $83 billion, though Ethereum retained a dominant 62 percent share of that capital. New entrants also made notable strides; the Aptos token achieved a $1 billion market capitalization within two weeks, entering the top‑50 cryptocurrencies, while Dogecoin posted the strongest price appreciation of the month at 50 percent. NFT markets displayed mixed signals: trading volume and sales declined 30 percent month‑on‑month, yet the number of unique NFT traders grew 18 percent to 1.11 million, and Polygon’s NFT volume surged 770 percent, largely propelled by Reddit‑hosted collections. Security vulnerabilities remained a critical concern, with cross‑chain bridges accounting for 82 percent of the month’s $3.57 million in exploit losses, including high‑profile attacks on Mango Markets, TempleDAO, the QANX bridge and Rabby Swap. The combined effect of rapid user migration, uneven asset performance, and persistent bridge exploits highlights both the growth potential and the systemic risk factors shaping the blockchain industry at the close of 2022.

DappRadarOct 2022

Report

2022 Blockchain Gaming Report: New Frontiers And The Path Forward

The blockchain gaming industry underwent a significant market correction in late 2022, signaling a transition from speculative "Play-to-Earn" (P2E) models toward more sustainable, gameplay-focused ecosystems. While unique active wallets stabilized at approximately one million, NFT transaction volumes fell 30% to $500 million, and major project market capitalizations plummeted by over 90%. Despite a 19% year-over-year decline in total deal value to $875 million in the third quarter, the sector saw a 2.6x increase in the number of funding deals. This shift indicates a move away from infrastructure-heavy "picks and shovels" investments toward seed-stage funding for game studios and user-friendly wallet solutions. The collapse of unsustainable economic designs has catalyzed a pivot toward "Free-to-Own" (F2O) and "Play-and-Own" (P&O) models. These frameworks prioritize fun-first gameplay and lower entry barriers by offering free initial digital assets, moving away from the yield-focused mechanics that previously dominated the space. This evolution is supported by a significant talent migration from traditional AAA and mobile gaming companies, which is professionalizing development and introducing more sophisticated tokenomics. Furthermore, the industry is expanding its reach through casual genres and the integration of established intellectual properties from major Asian studios like Square Enix and SEGA. Mass adoption efforts are increasingly focused on distribution and technical scalability. Notable milestones include the launch of blockchain titles on mainstream platforms like the Epic Games Store and the clarification of NFT guidelines within the Apple App Store. However, the industry faces ongoing challenges, including a crisis in the gaming guild model and intensifying regulatory scrutiny. As the SEC investigates major entities regarding the classification of digital assets as securities, developers are balancing innovation in on-chain mechanics and AI-driven content with the need for compliance in an increasingly complex global legal landscape.

CMC ResearchOct 2022

Report

DappRadar Blockchain Industry Report: Highlights of July 2022

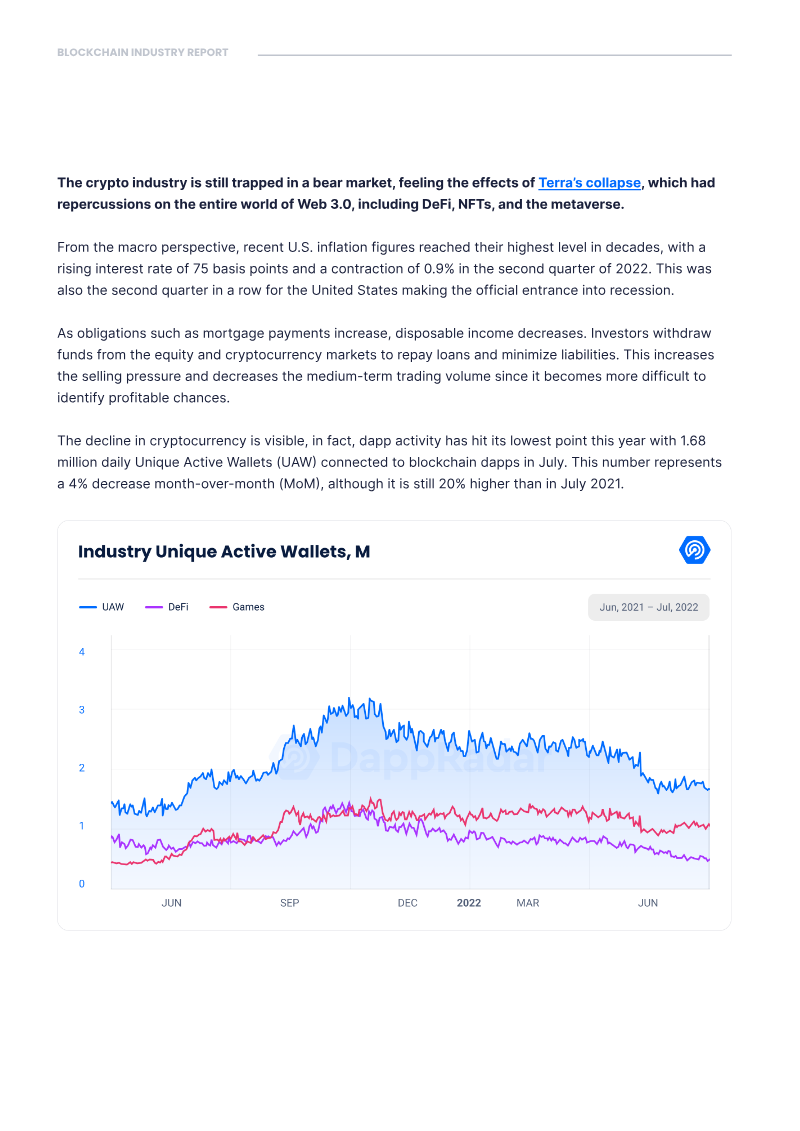

The July 2022 DappRadar Blockchain Industry Report analyzes the state of the decentralized application ecosystem during a significant market downturn. The findings indicate that while the broader crypto industry remains trapped in a bear market influenced by the collapse of Terra and macroeconomic pressures like U.S. inflation, specific sectors—most notably blockchain gaming—demonstrate remarkable resilience. The report covers global trends across decentralized finance (DeFi), non-fungible tokens (NFTs), and gaming, utilizing data on Unique Active Wallets (UAW) and Total Value Locked (TVL) to measure health and engagement. Data shows that dapp activity reached a yearly low in July with 1.68 million daily UAW, a 4% decrease from June. DeFi was the hardest-hit segment, with UAW dropping below 500,000 for the first time since early 2021. Despite this, DeFi TVL saw a 22% recovery during the month, rising to $82.3 billion, led by growth on Ethereum, BNB Chain, and Tron. The report also highlights the continued "crypto contagion" following the Celsius Network bankruptcy filing, which has increased calls for international regulatory frameworks like the EU’s MiCA. The NFT market experienced a contraction, with monthly trading volume failing to reach $1 billion for the first time in over a year. Market dynamics are shifting as OpenSea’s dominance fell from 84% in May to 58.6% in July, facing increased competition from new entrants like the GameStop and Nickelodeon marketplaces. Conversely, the gaming sector emerged as a primary industry driver, accounting for nearly 60% of all dapp usage. With nearly 1 million daily UAW, blockchain games grew 8% month-over-month, suggesting that immersive mechanics and venture capital interest are insulating the segment from the prevailing "crypto winter."

DappRadarJul 2022