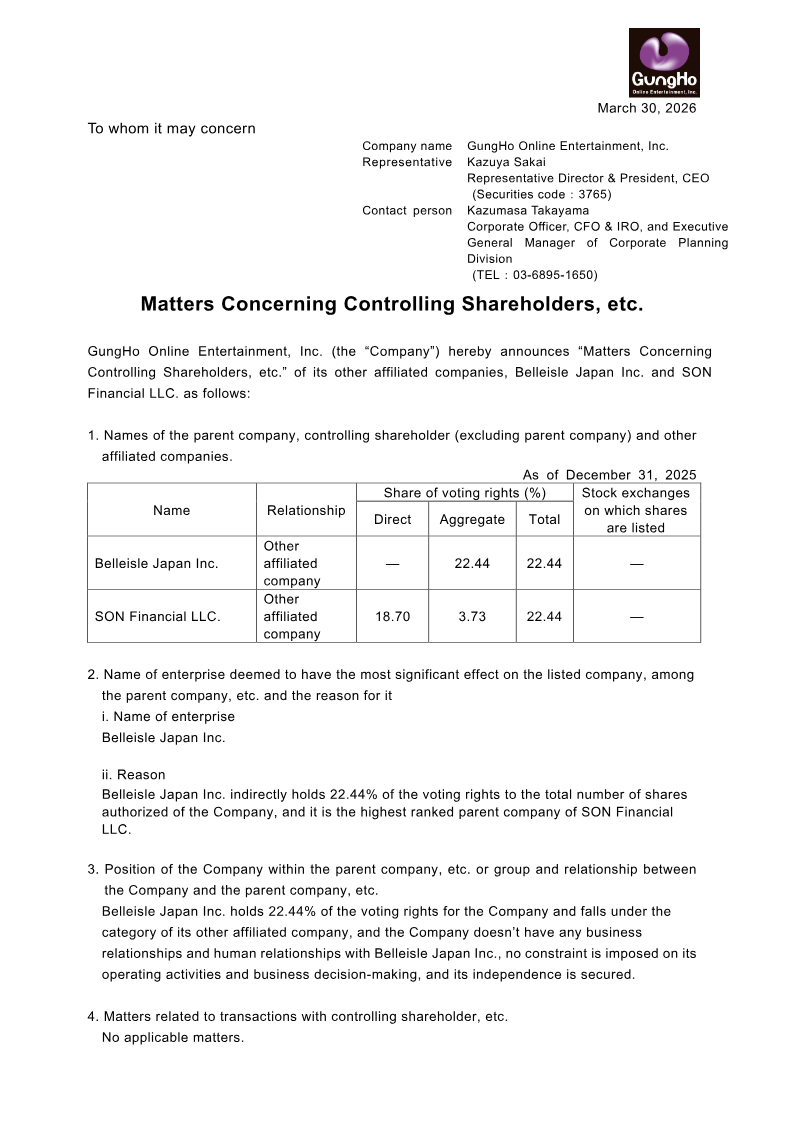

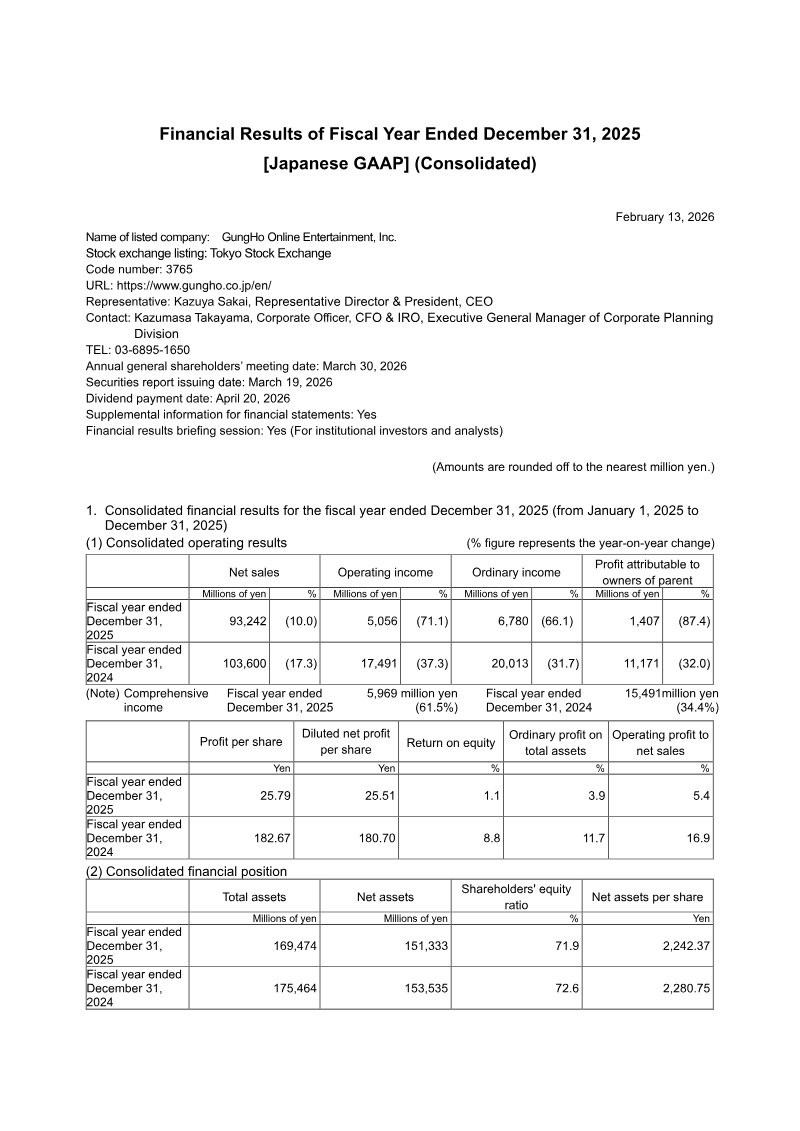

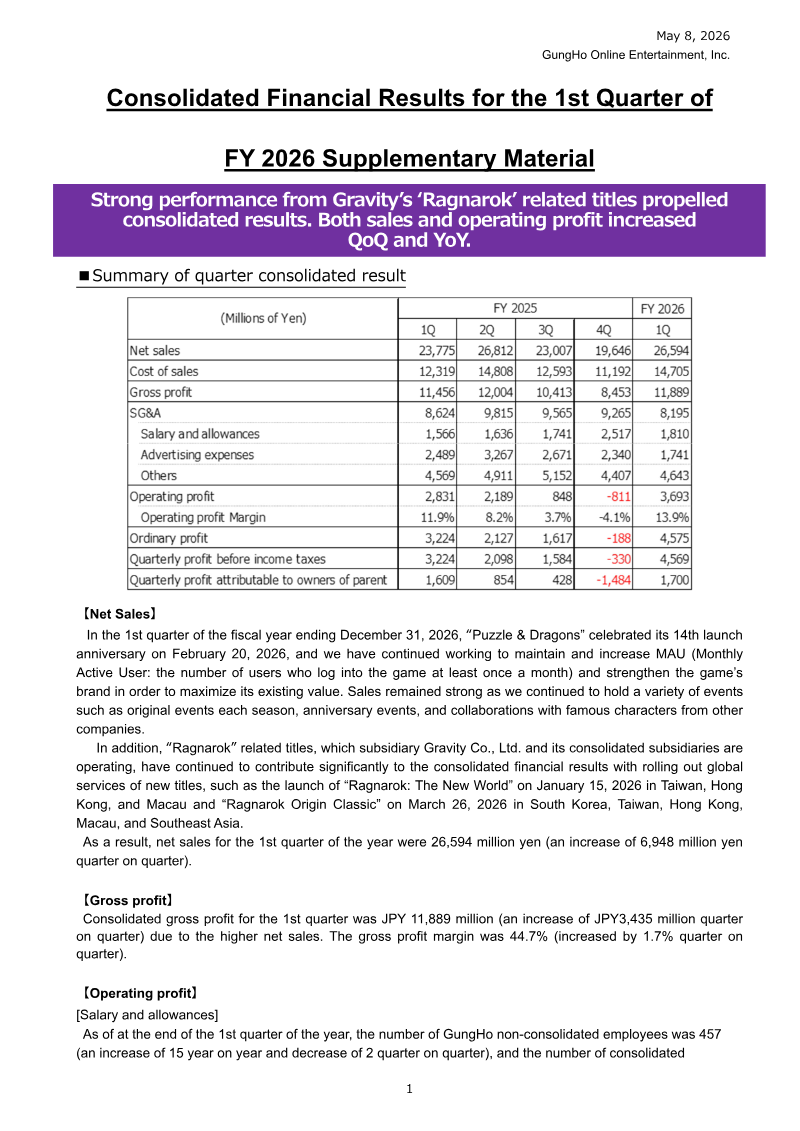

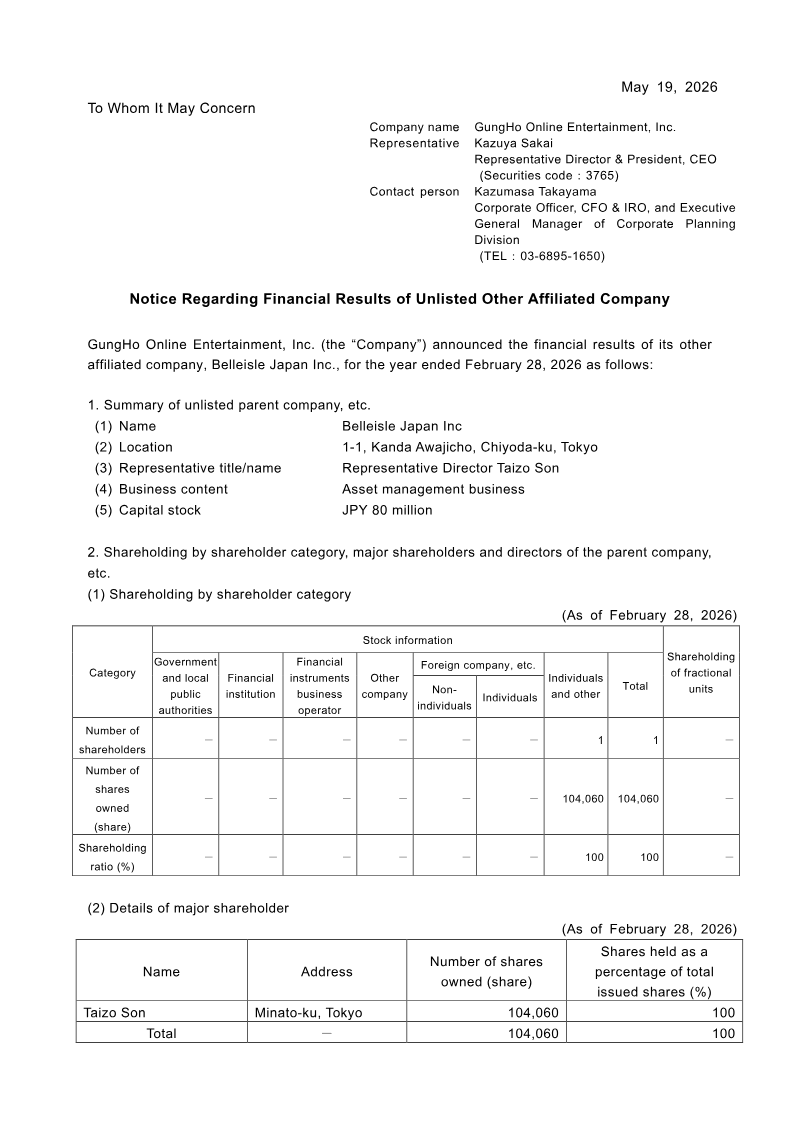

Matters Concerning Controlling Shareholders, etc.

1 pages~2 min full read

GungHo Online Entertainment, Inc. maintains a corporate structure involving two primary affiliated entities, Belleisle Japan Inc. and SON Financial LLC, as of December 31, 2025. Belleisle Japan Inc. serves as the most significant entity, holding an aggregate 22.44% of the company’s voting rights. This position is reinforced by its status as the parent company of SON Financial LLC, which also holds a 22.44% aggregate interest in GungHo through a combination of direct and indirect ownership.

Despite these significant equity stakes, GungHo Online Entertainment operates with full corporate autonomy. The company reports no existing business or human resource relationships with Belleisle Japan Inc. Furthermore, there are no constraints imposed by these affiliated shareholders on the company’s operational activities or strategic decision-making processes. This separation ensures that the company maintains its independence in all management functions.

The disclosure confirms that there are no reportable transactions between GungHo Online Entertainment and these controlling shareholders. By clarifying the ownership landscape and the lack of operational interference, the company provides transparency regarding its governance and the nature of its relationship with its largest stakeholders. This summary reflects the company’s official position on its corporate structure and the preservation of its independent business operations as of the March 2026 reporting period.

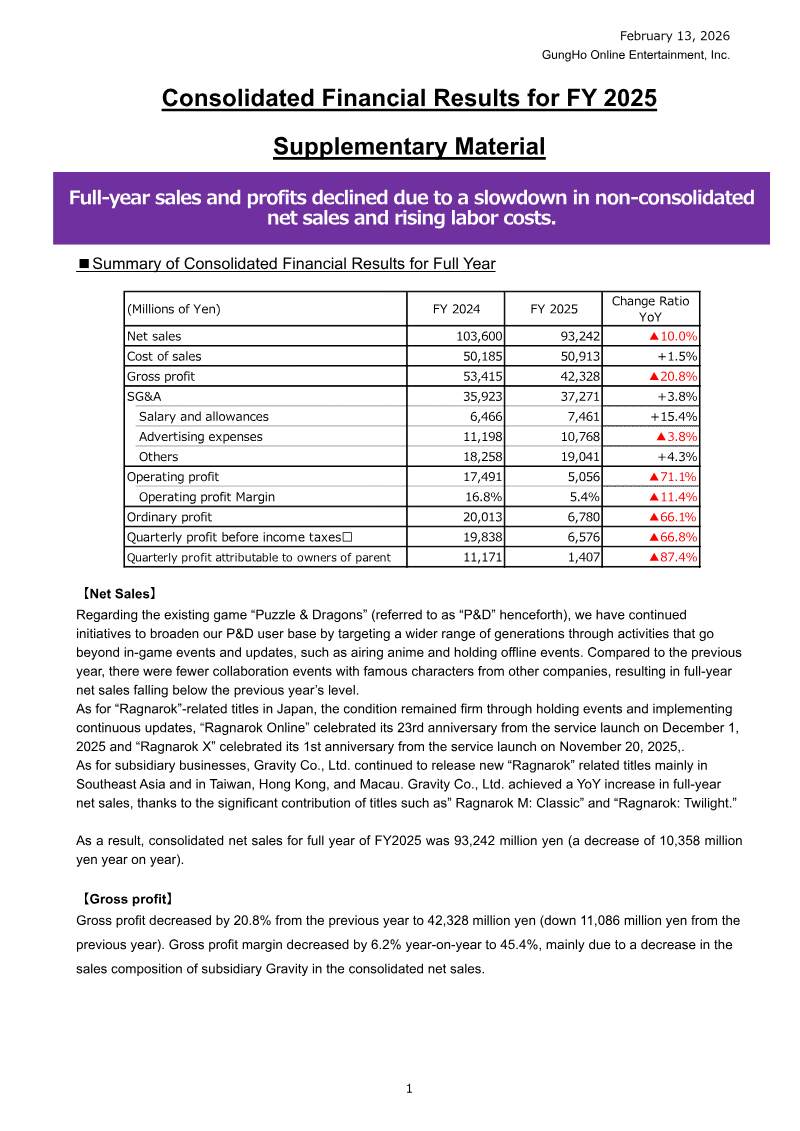

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2024

GungHo Online Entertainment

GungHo Online Entertainment

GungHo Online Entertainment

GungHo Online Entertainment

Capcom · 2026

Capcom Co. · 2026

Capcom · 2026

Sony Group Corporation · 2026

Marvelous · 2026

Square Enix · 2026

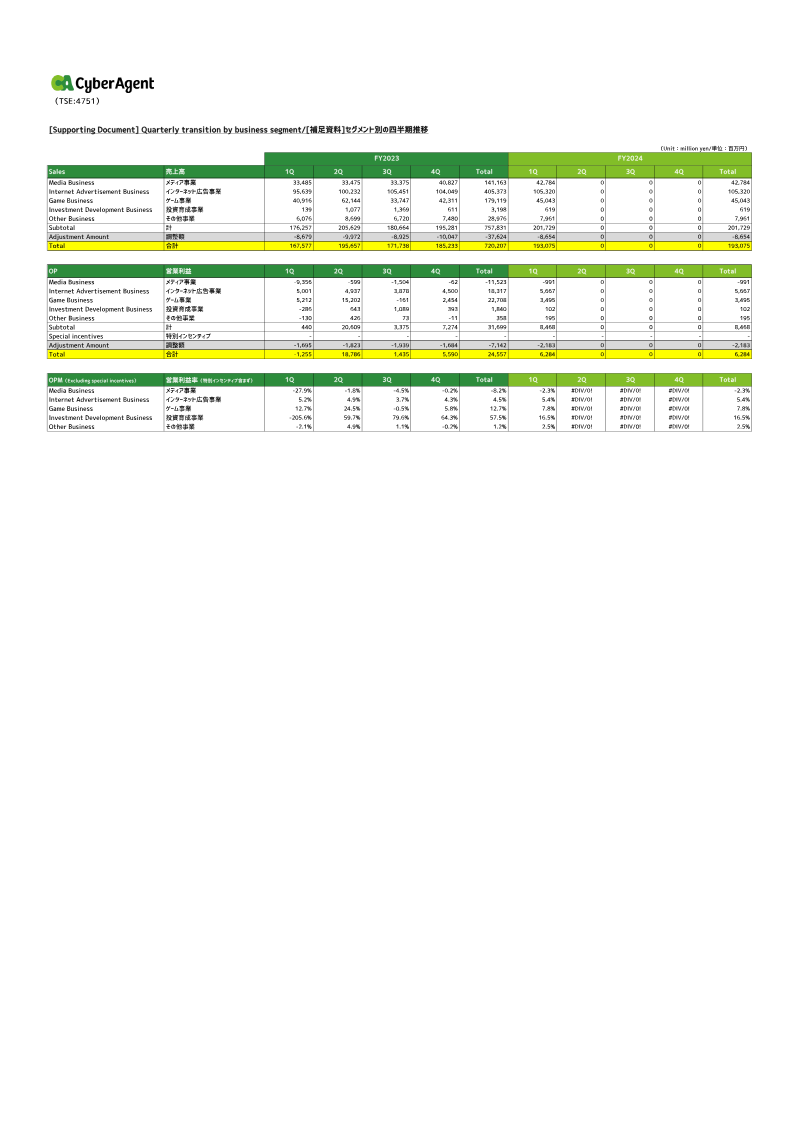

CyberAgent · 2026

Nippon Ichi Software · 2026

Square Enix · 2026

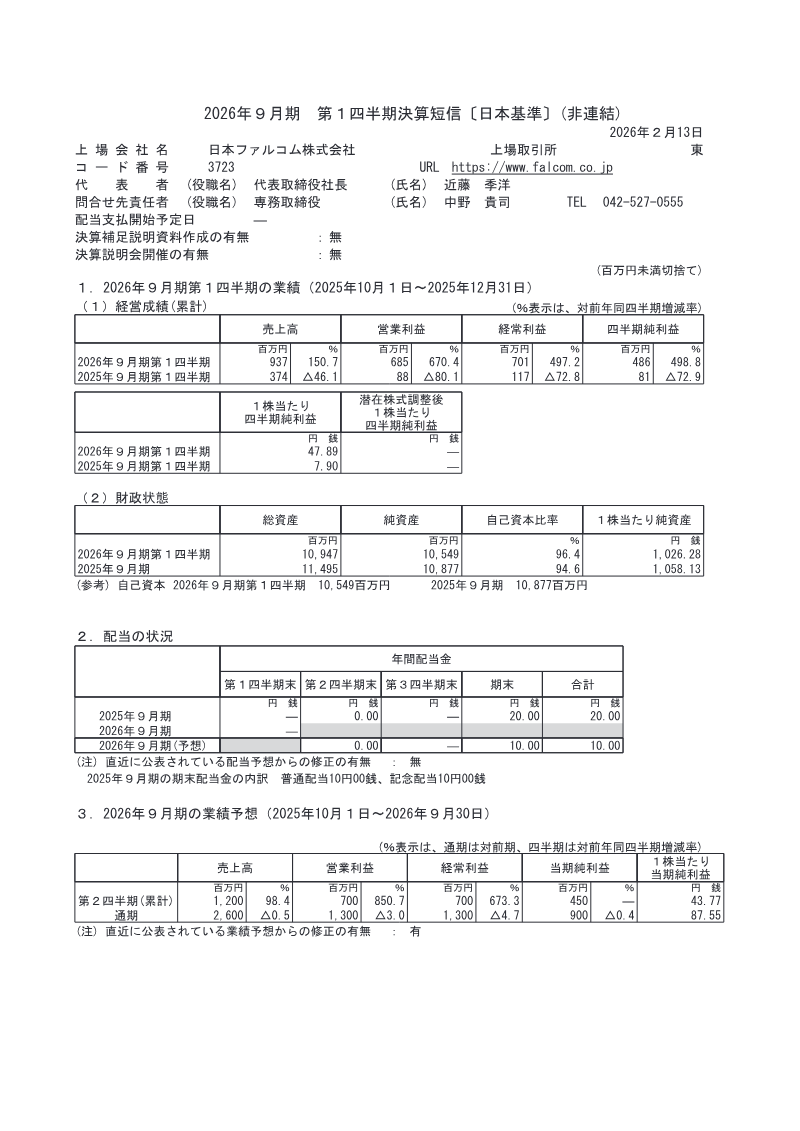

Nihon Falcom Corporation · 2026

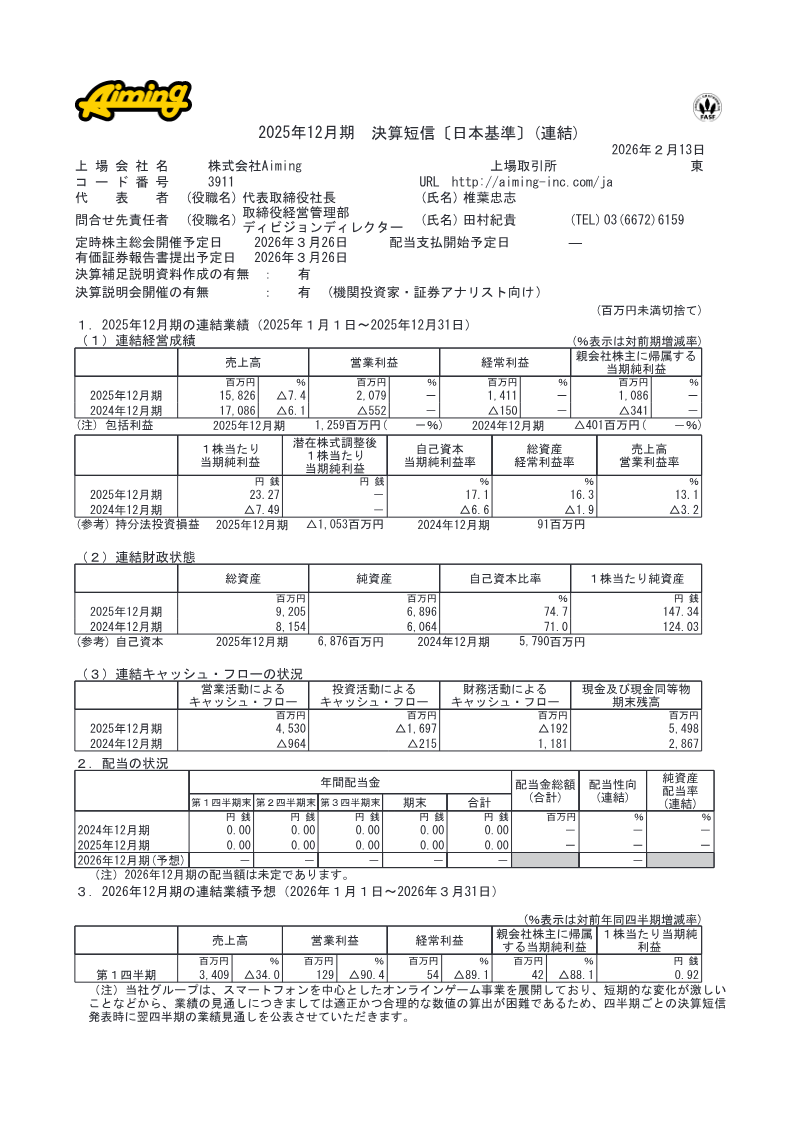

Aiming · 2026

Sega Sammy Holdings · 2026