Back to Library

Report

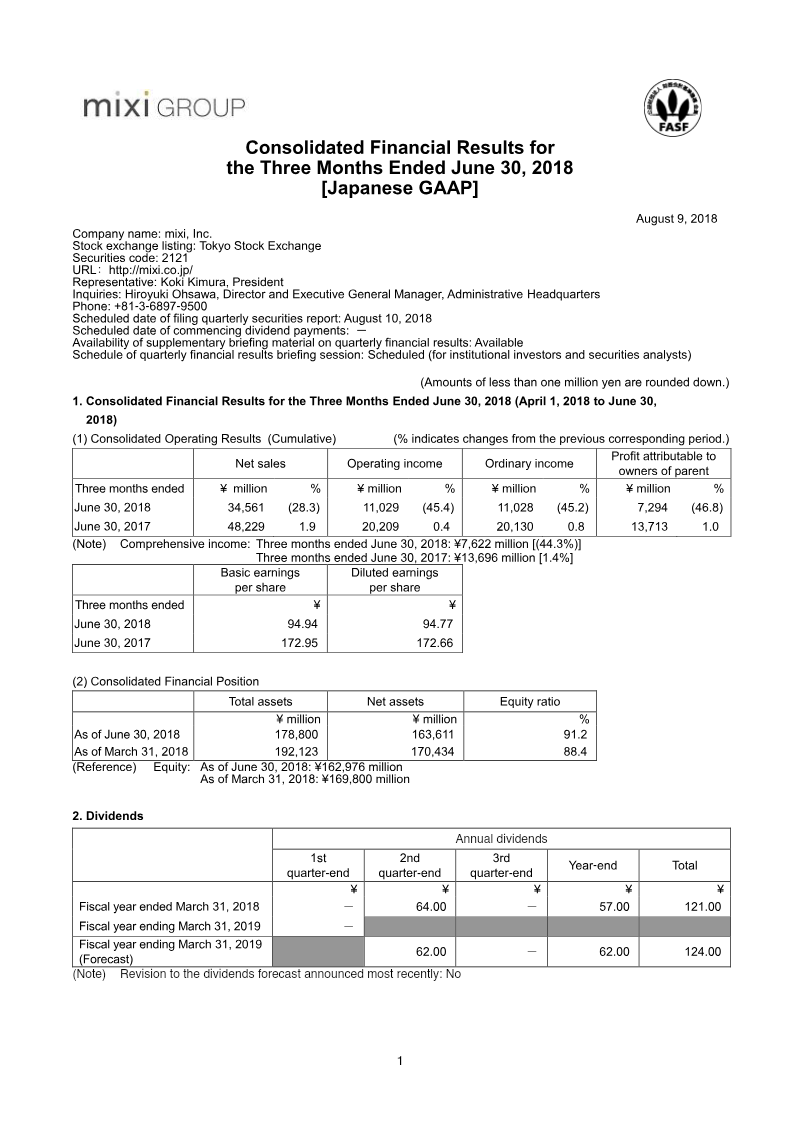

Consolidated Financial Results for the Three Months Ended June 30, 2017

By mixi

9 pages3,080 words

Summary

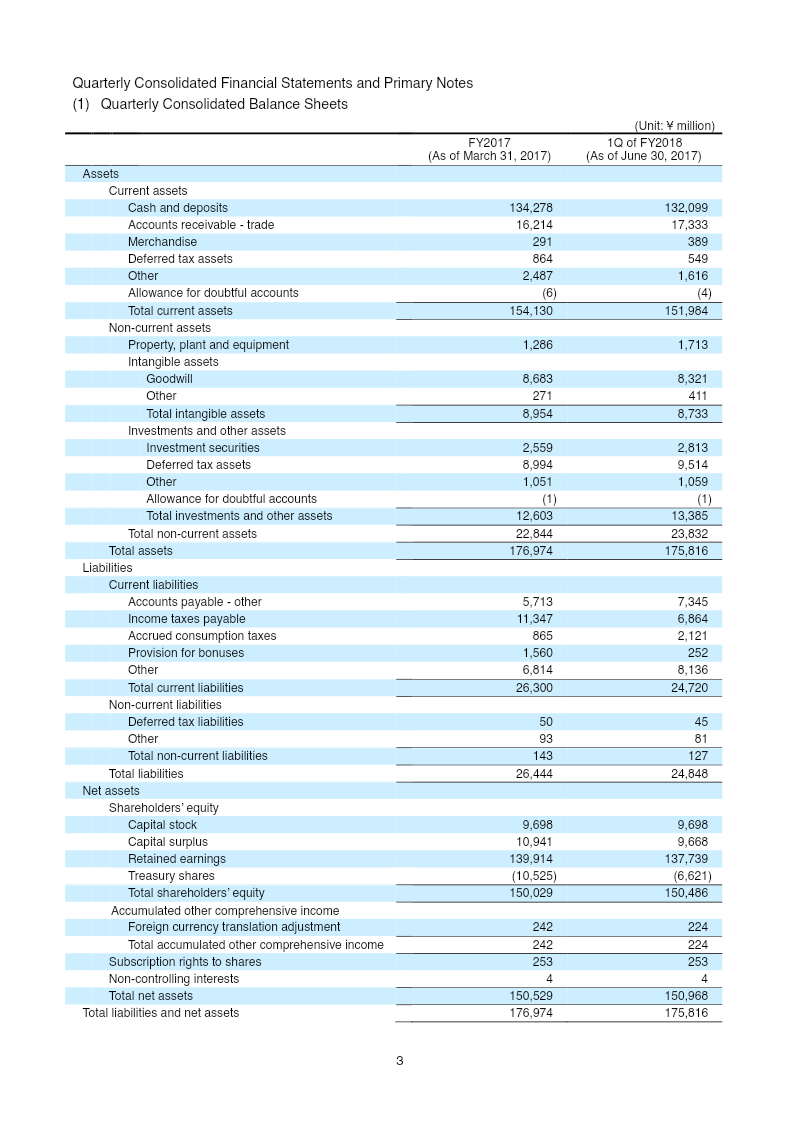

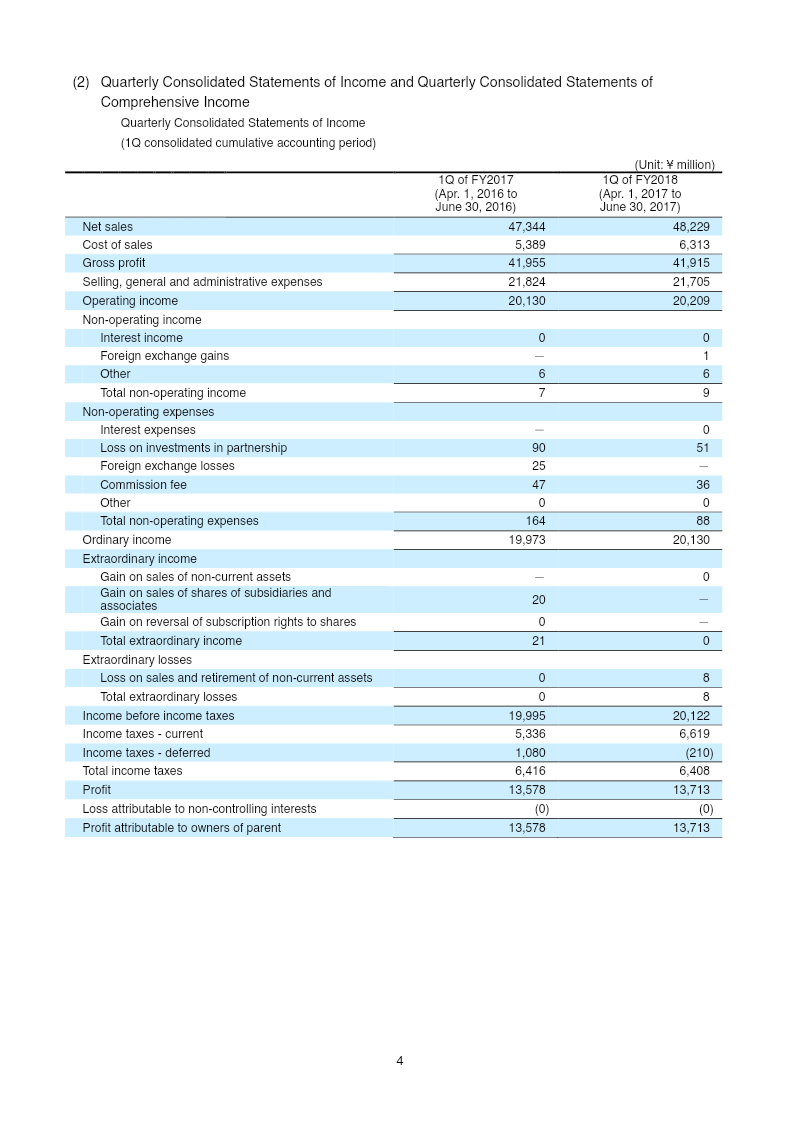

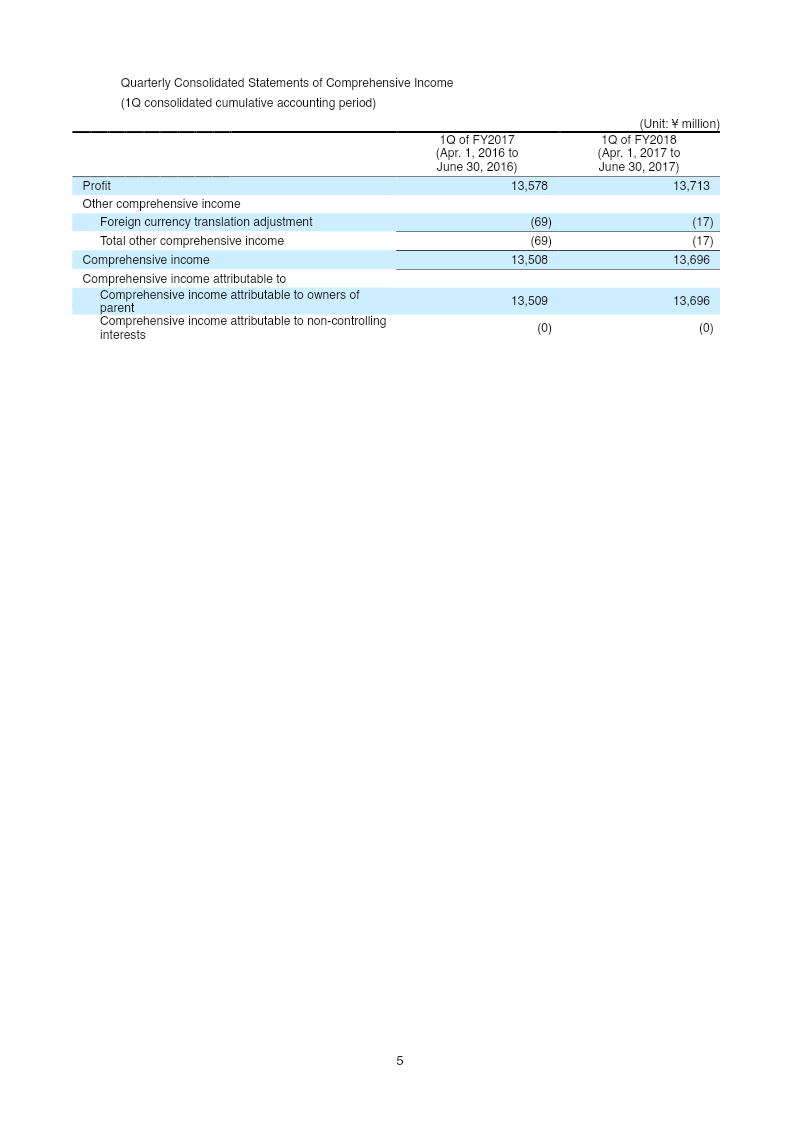

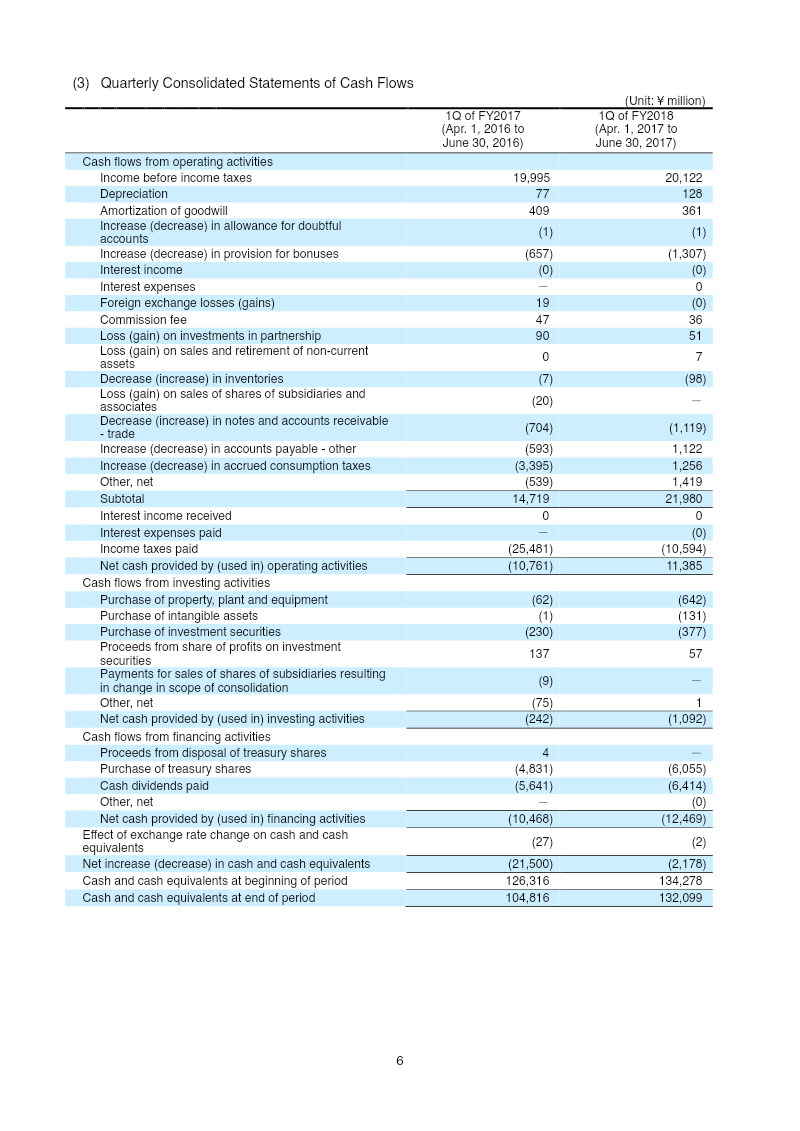

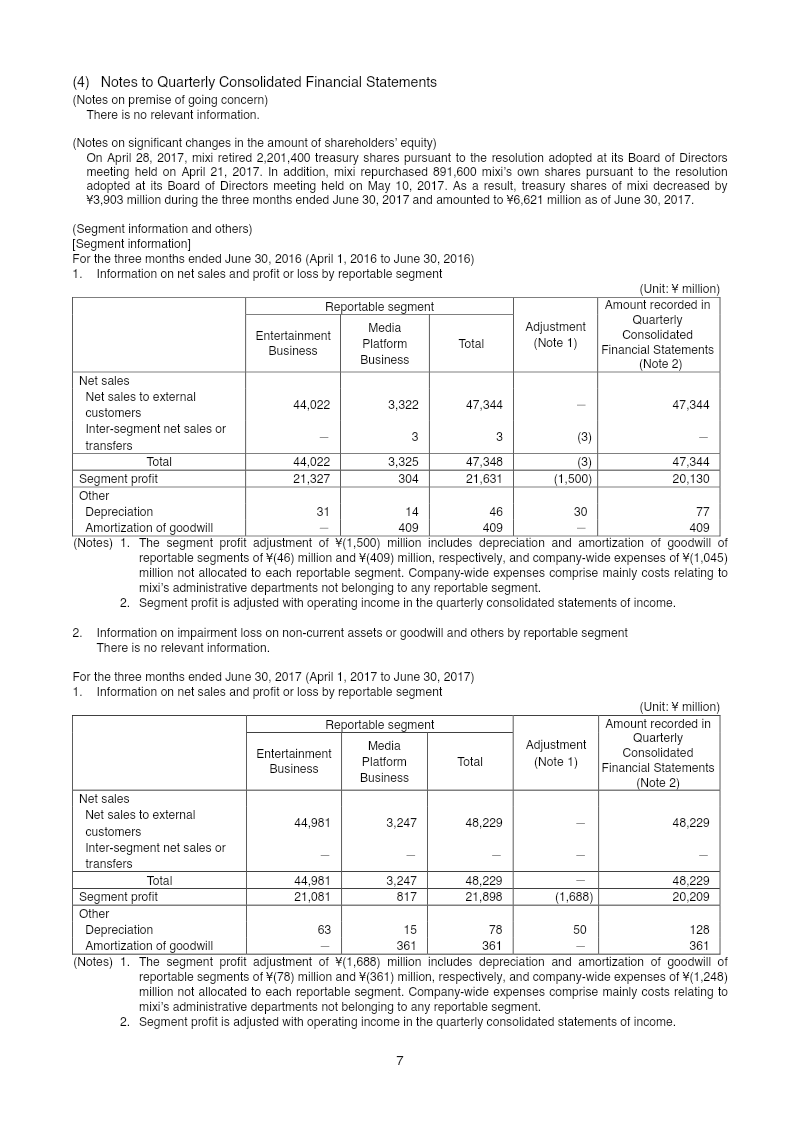

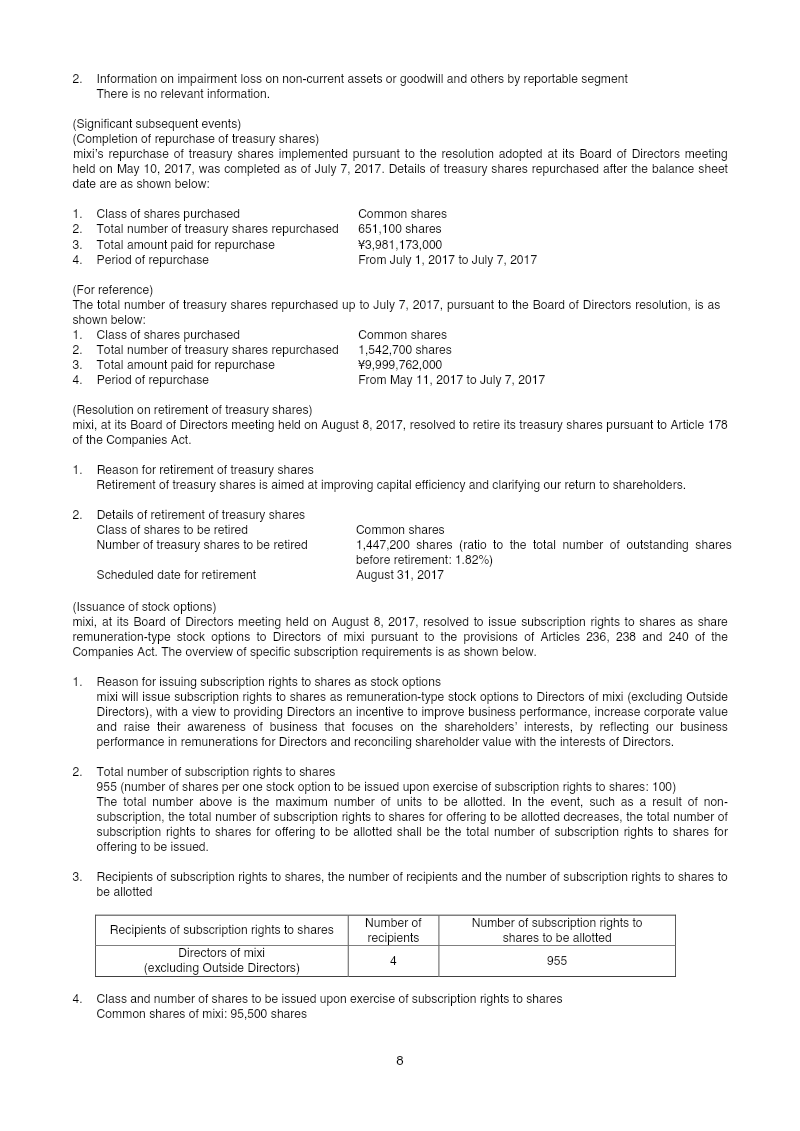

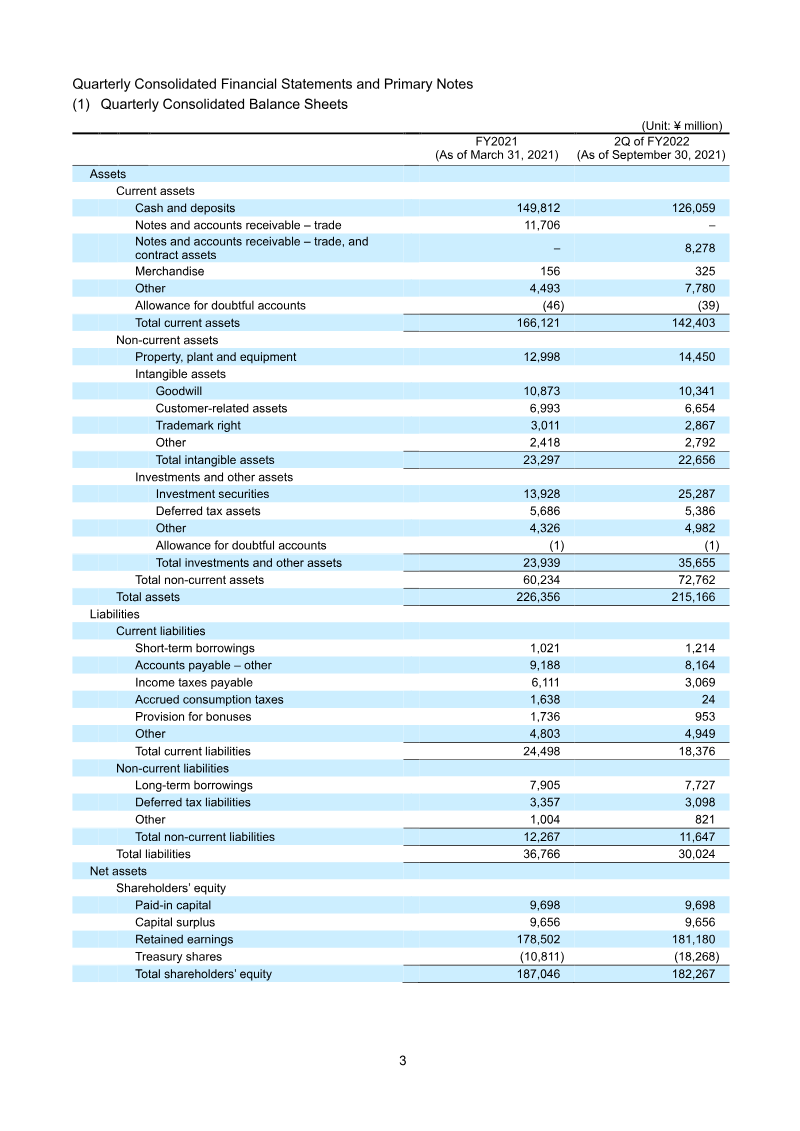

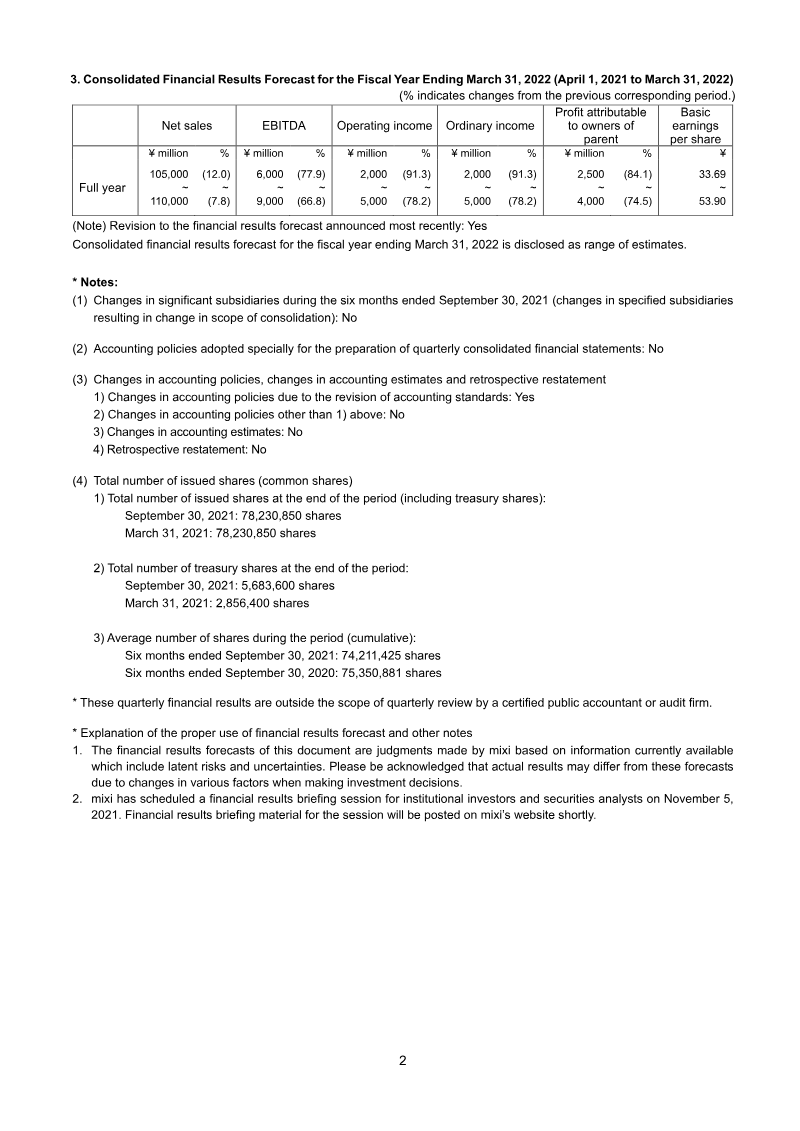

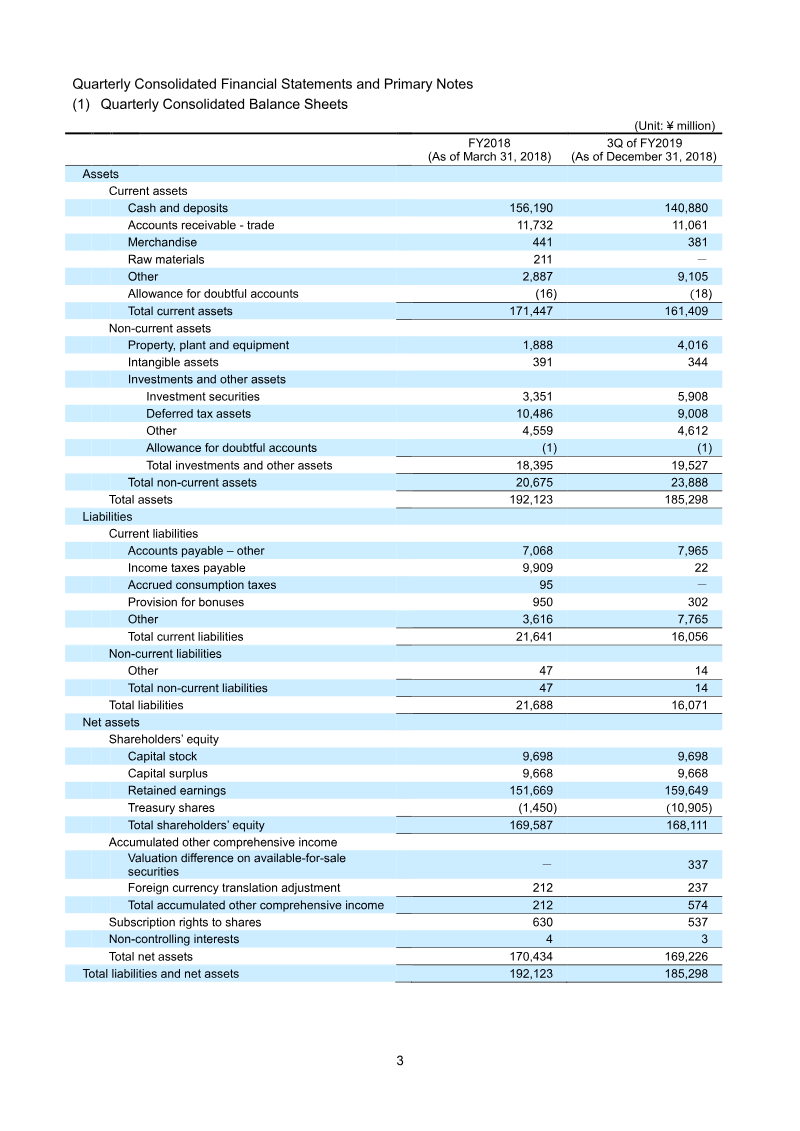

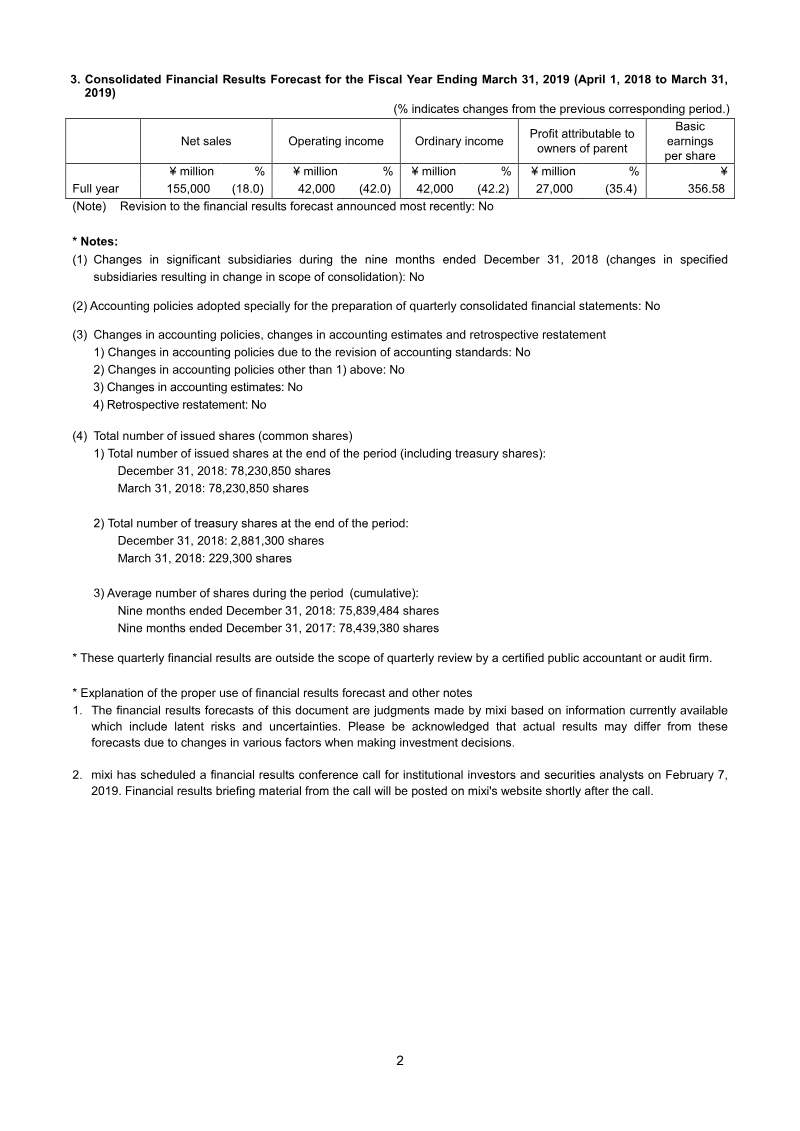

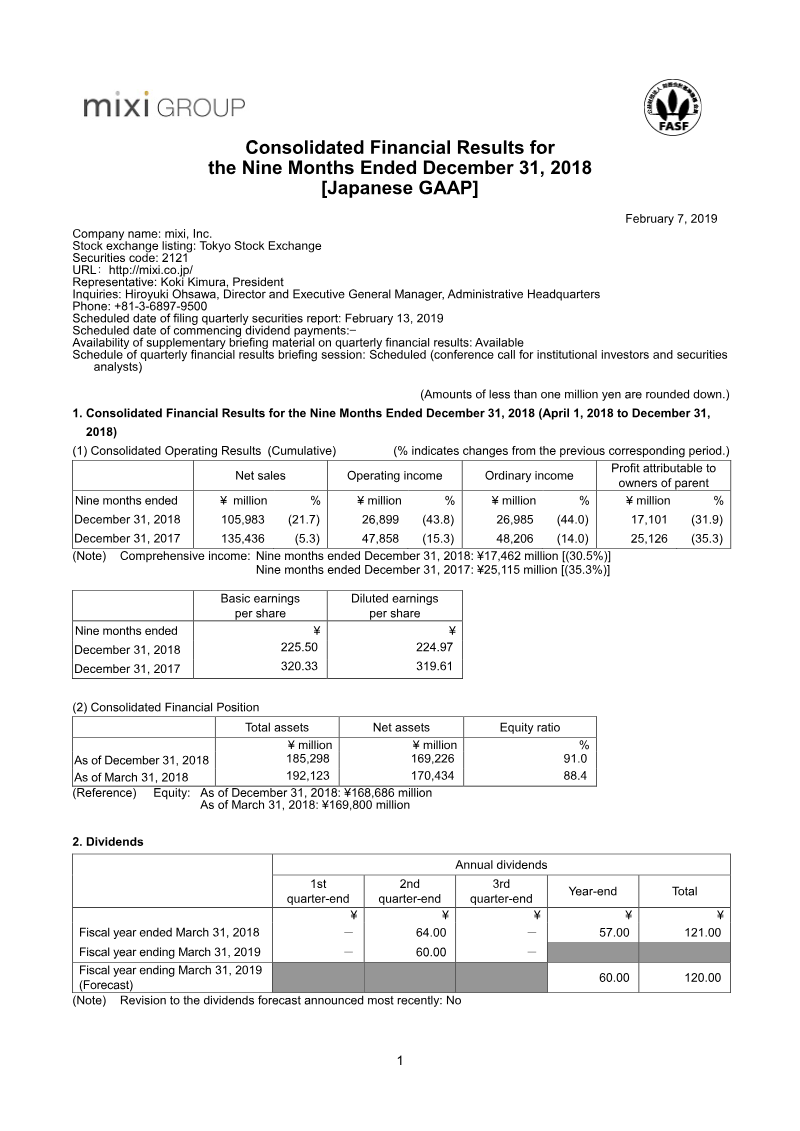

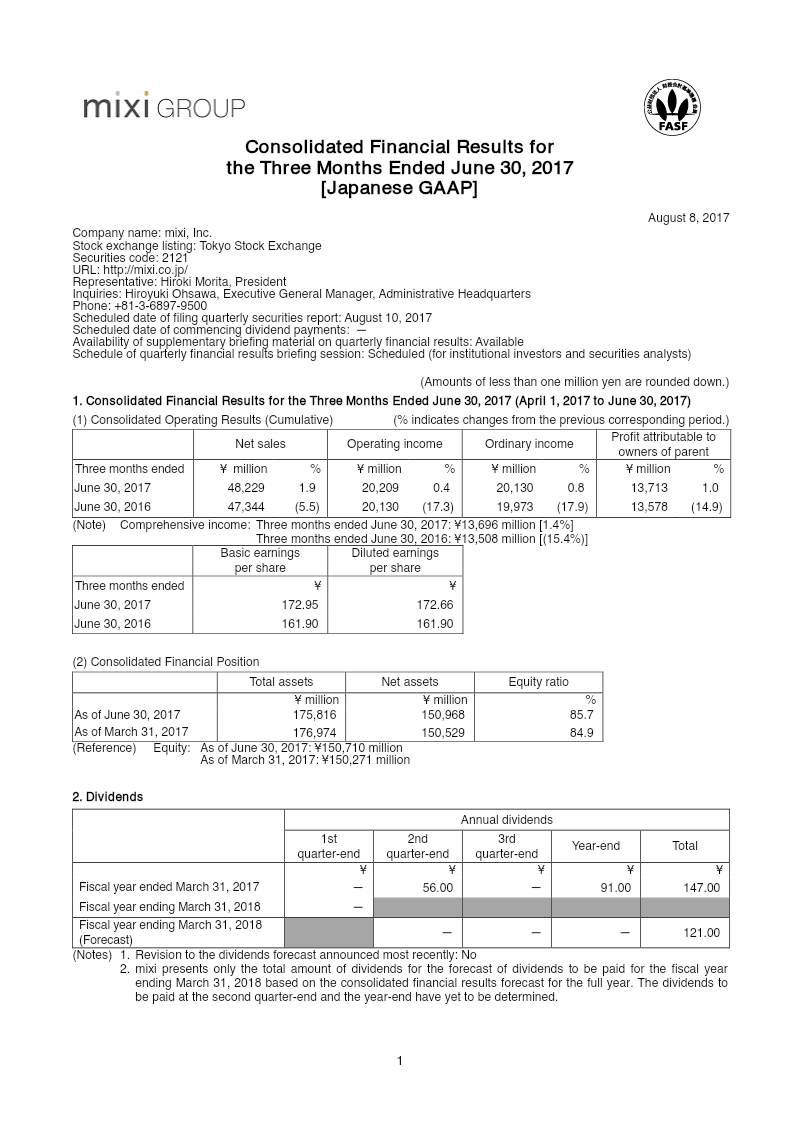

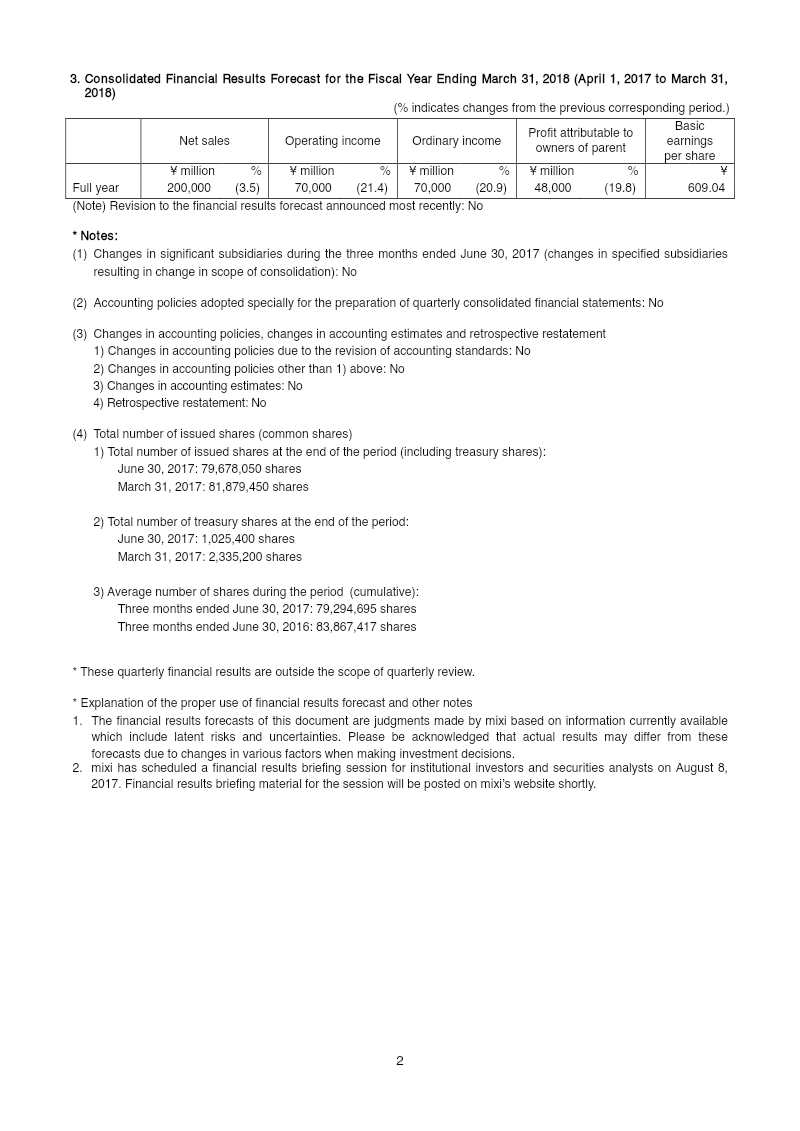

The quarterly filing presents mixi, Inc.’s consolidated financial performance for the first quarter of fiscal 2018 (April 1–June 30, 2017). Net sales rose to ¥48.2 billion from ¥47.3 billion, a 1.9 % increase, while operating income climbed to ¥20.2 billion, up 0.4 %. Ordinary income and profit attributable to owners of the parent both increased modestly, reaching ¥20.1 billion and ¥13.7 billion respectively, reflecting a 0.8 % rise in profit attributable to owners compared with the same period in 2016. Basic and diluted earnings per share improved to ¥172.95 and ¥172.66, up from ¥161.90 in the prior year. Total assets stood at ¥175.8 billion, with net assets of ¥150.9 billion and an equity ratio of 85.7 %. The balance sheet shows a slight reduction in current liabilities and an increase in cash and deposits, while treasury share holdings decreased by ¥3.9 billion due to a repurchase program completed in July 2017. The company forecasts full‑year results of ¥200 billion in sales, ¥70 billion operating income, and a profit attributable to owners of ¥48 billion, representing declines of 3.5 %, 21.4 %, and 19.8 % respectively compared with the prior year. No changes in accounting policies or significant subsidiaries were reported, and the company maintains a stable going‑concern outlook. The filing also details dividend plans for fiscal 2017 and 2018, with a total forecasted dividend of ¥121 million for the year ending March 31, 2018.

Tags

Pages

View all

Citation

Citation

Generating citation...

Similar Documents

Report

Summary of Financial Results: First Half 2017

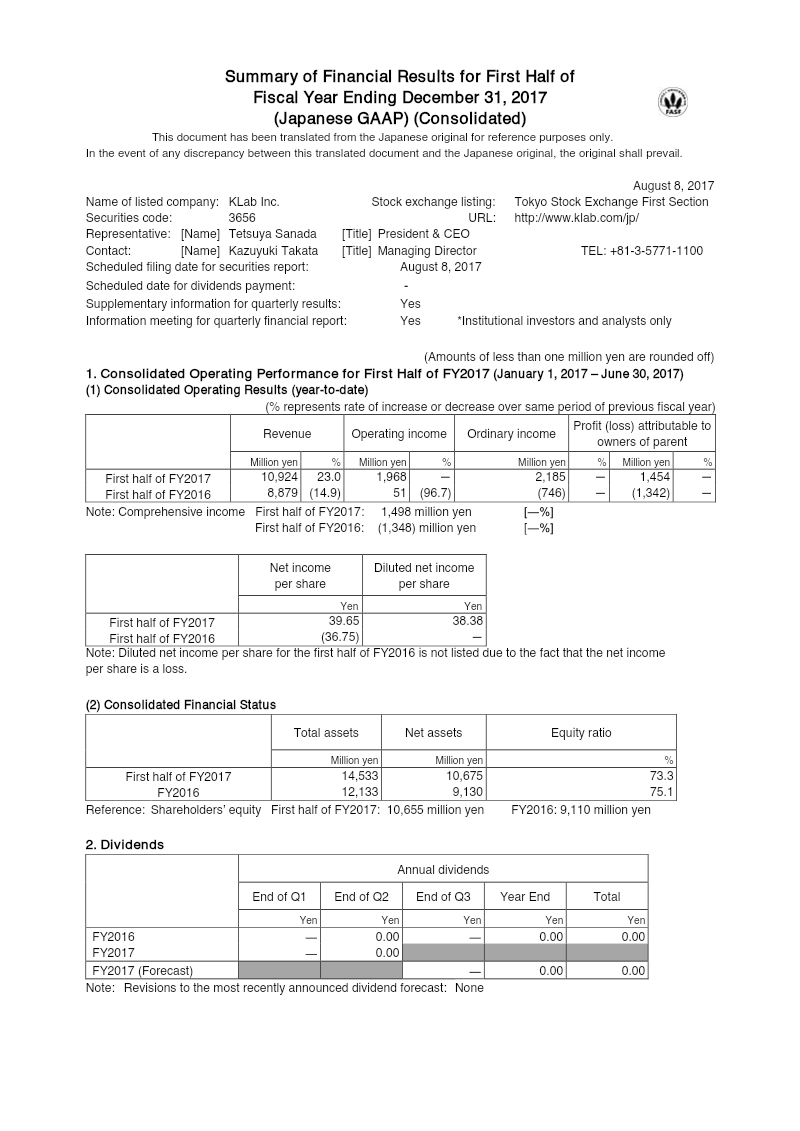

KLab Inc. reported a strong first‑half fiscal 2017 performance, with consolidated revenue rising 23 % to ¥10.92 billion compared to ¥8.88 billion in the same period of FY2016. Operating income increased markedly to ¥1.97 billion, up from a loss of ¥51 million the previous year, driven by robust sales of core mobile games and the launch of “Captain Tsubasa ~Tatakae Dream Team~” in mid‑June. Cost of sales grew modestly by 3.9 % to ¥7.02 billion, largely reflecting higher royalty and commission expenses linked to revenue growth. Selling, general and administrative costs fell 6.6 % to ¥1.93 billion due to reduced advertising and outsourcing spend, while non‑operating income of ¥217 million—primarily foreign‑exchange gains—offsets a non‑operating expense of ¥647 million, resulting in ordinary profit of ¥2.19 billion and net income attributable to owners of parent of ¥1.45 billion. Total assets reached ¥14.53 billion, up ¥2.40 billion from FY2016, with net assets increasing to ¥10.68 billion and an equity ratio of 73.3 %. The company maintained a healthy liquidity position, with current assets at ¥9.10 billion and current liabilities at ¥3.85 billion, while retained earnings grew by ¥1.54 billion. KLab revised its FY2017 forecasts upward, projecting revenue of ¥22.5–25.5 billion, operating income of ¥2.20–4.00 billion, ordinary profit of ¥2.40–4.20 billion, and net income attributable to owners of parent between ¥1.60–2.80 billion, reflecting favorable market trends and recent game releases. During the period, KLab acquired ABASEA Inc., making it a 100 % subsidiary and adding Spicemart Inc. as a sub‑subsidiary, with the acquisition cost recorded at ¥1 billion cash. This strategic move aims to enhance data‑analysis capabilities for mobile game operations and expand cross‑border market presence.

KLab

Report

FY2025 First Quarter Financial Results Briefing

The briefing presents FY2025 first‑quarter results for GREE, Inc., highlighting a net sales figure of ¥12.9 billion and an operating loss of ¥0.1 billion, largely driven by valuation losses in the Investment Business and foreign‑exchange impacts from yen appreciation. While Game and Anime, Metaverse, and DX segments exceeded forecasts—thanks to strong performance of the Chinese version of *Heaven Burns Red*, continued growth in platform and VTuber services, and solid DX profitability—the Investment Business posted a ¥0.8 billion operating loss due to crypto‑asset valuation declines and write‑downs on maturing funds. Variable costs rose from advertising spend and investment losses, whereas fixed costs remained relatively stable. Geographically, the company operates globally with significant overseas assets; the report notes a ¥1.4 billion FX loss affecting ordinary and net profit. The management plan positions Metaverse and DX as continuous‑growth businesses targeting a 120–140 % CAGR in operating profit, while Game and Anime are treated as long‑term investment assets. Medium‑term targets emphasize aggressive investment in VTuber talent and DX product development, with expectations of profitability from the VTuber segment by FY2026 and accelerated growth in DX by FY2027. Methodologically, the briefing relies on quarterly financial statements, segment‑level performance data, and investment portfolio valuations. The Investment Business’s dual GP/LP structure is explained to contextualize volatility, with an emphasis on long‑term stability despite short‑term losses. Overall, the company projects FY2025 results in line with prior forecasts but anticipates slightly lower Game and Anime sales, offset by higher operating profit from continuous‑growth segments.

GREE