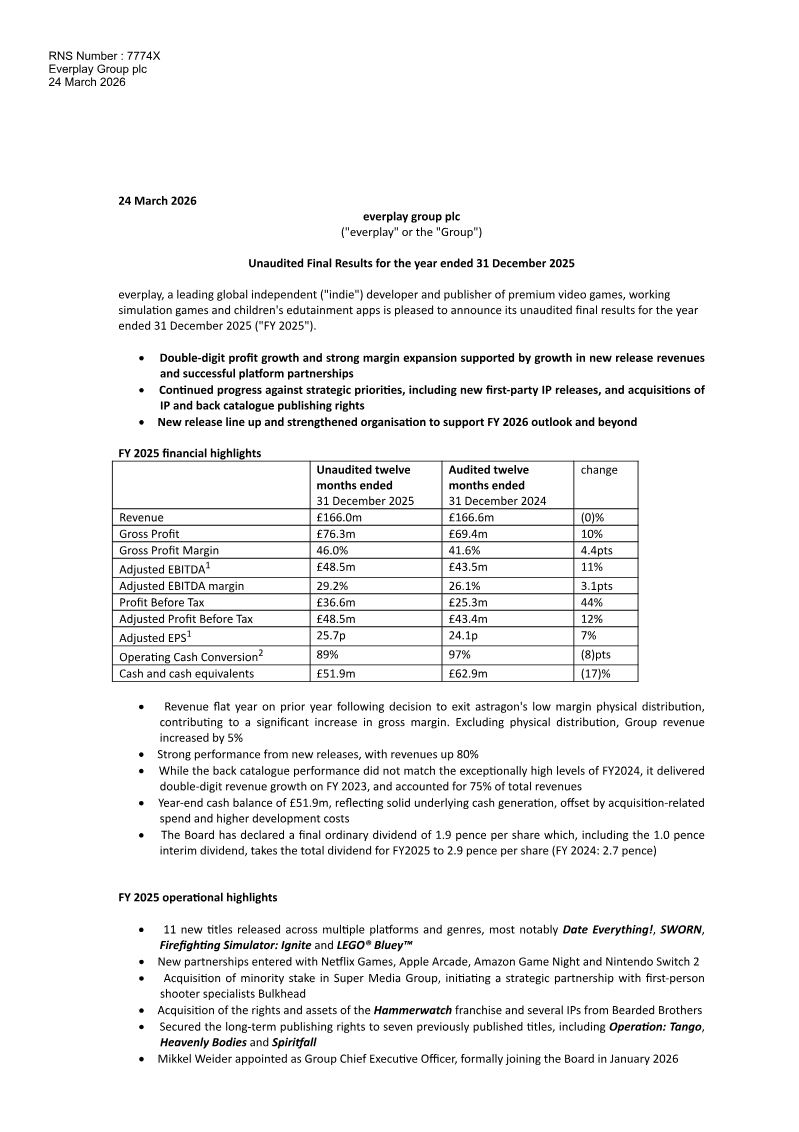

Q2 2024 saw robust activity in the digital services sector with over 350 M&A transactions totaling $7.4 billion and 880 fundraising deals raising $8.1 billion.

See it on page 3Major M&A activity was headlined by EQT’s $3.0 billion acquisition of Perficient and Cognizant’s $1.3 billion purchase of Belcan, signaling a strategic focus on digital transformation capabilities.

See it on page 5Generative AI and AI-powered technologies are identified as the primary catalysts for deal momentum, with expectations for increased M&A activity in Q3 2024.

See it on page 3Private equity remains a significant driver of market movement, exemplified by Bain Capital’s $250 million minority investment in Sikich.

See it on page 6Market demand is concentrated in technology-enabled services, specifically cloud migration, cybersecurity, business intelligence, and data analytics.

See it on page 8Corporates are increasingly utilizing inorganic growth strategies to combat technological disruption and improve operational efficiencies.

See it on page 3The quarterly Digital Services Report presents a comprehensive snapshot of the global digital services landscape for Q2 2024, focusing on mergers and acquisitions, fundraising activity, market trends, and key performance indicators across technology-enabled services. The report highlights a robust deal pipeline, with 350+ disclosed M&A transactions totaling over $7.4 billion and 880+ fundraising deals raising more than $8.1 billion, underscoring continued investor confidence despite macro‑economic uncertainty. Notable transactions include Cognizant’s $1.3 billion acquisition of Belcan, EQT’s $3.0 billion purchase of Perficient, and Virtusa’s acquisition of ITMAGINATION, illustrating a strategic shift toward digital transformation capabilities. Fundraising highlights feature Sikich’s $250 million minority investment from Bain Capital, Uniqus Consultech’s $10 million Series B led by Nexus Ventures, and Raft’s $60 million venture round from Washington Harbour.

Market analysis identifies generative AI and other AI‑powered technologies as primary catalysts for future deal momentum, with expectations of heightened M&A activity in Q3 2024 driven by pent‑up demand and abundant private equity capital. Geographic coverage spans North America, Europe, and Asia-Pacific, with a focus on technology‑enabled services such as cloud migration, cybersecurity, business intelligence, and data analytics. Methodology relies on proprietary Drake Star analysis of M&A and private placement databases, supplemented by secondary sources including Capital IQ, PitchBook, and SimilarWeb.

The report concludes that corporates increasingly pursue inorganic growth to unlock value, achieve efficiencies, and stay ahead of technological disruption. It positions digital services as a high‑growth sector poised for continued consolidation and innovation, offering investors and executives actionable insights into emerging trends and strategic opportunities.