Related Documents

Report

Gamedev Salary Pulse 2026: North America, Western Europe, Nordics, Central and Eastern Europe

The game development industry is currently navigating a period of profound structural instability, characterized by widespread workforce reductions and a pervasive sense of professional anxiety. Despite the rapid integration of artificial intelligence, the primary driver of current career displacement remains studio restructuring rather than technological replacement. While the majority of the workforce remains employed in hybrid or remote roles, a significant portion of professionals are actively reassessing their career trajectories. This climate of cautious realism is reflected in market sentiment, where nearly 40 percent of industry participants anticipate further decline, leading to increased emotional fatigue and a shift in priorities toward time-based benefits, such as the four-day workweek, over traditional office perks. Geographically, the industry maintains a clear hierarchy in compensation, with North America consistently commanding the highest salary tiers across all seniority levels. In contrast, Central and Eastern Europe continue to function as the most cost-effective hubs for talent acquisition. This regional disparity underscores a broader trend of geographic diversification, as studios balance the need for specialized expertise with the economic realities of global operations. Although the workforce remains mobile, the prevalence of remote work has effectively anchored many professionals, creating a distinct divide where on-site employees demonstrate a significantly higher propensity for international relocation compared to their remote counterparts. The current landscape is defined by a maturing workforce dominated by mid-to-senior level professionals, accompanied by a concerning decline in new entrants. This demographic shift, coupled with the ongoing volatility in employment, has necessitated more flexible recruitment strategies. Studios are increasingly moving away from traditional hiring models, favoring diverse solutions that range from subscription-based flat-fee packages to comprehensive recruitment process outsourcing. As the industry continues to evolve, these data-driven benchmarks serve as a critical framework for both studios and professionals attempting to navigate the complexities of global compensation and shifting labor market dynamics.

8BitMar 2026

Report

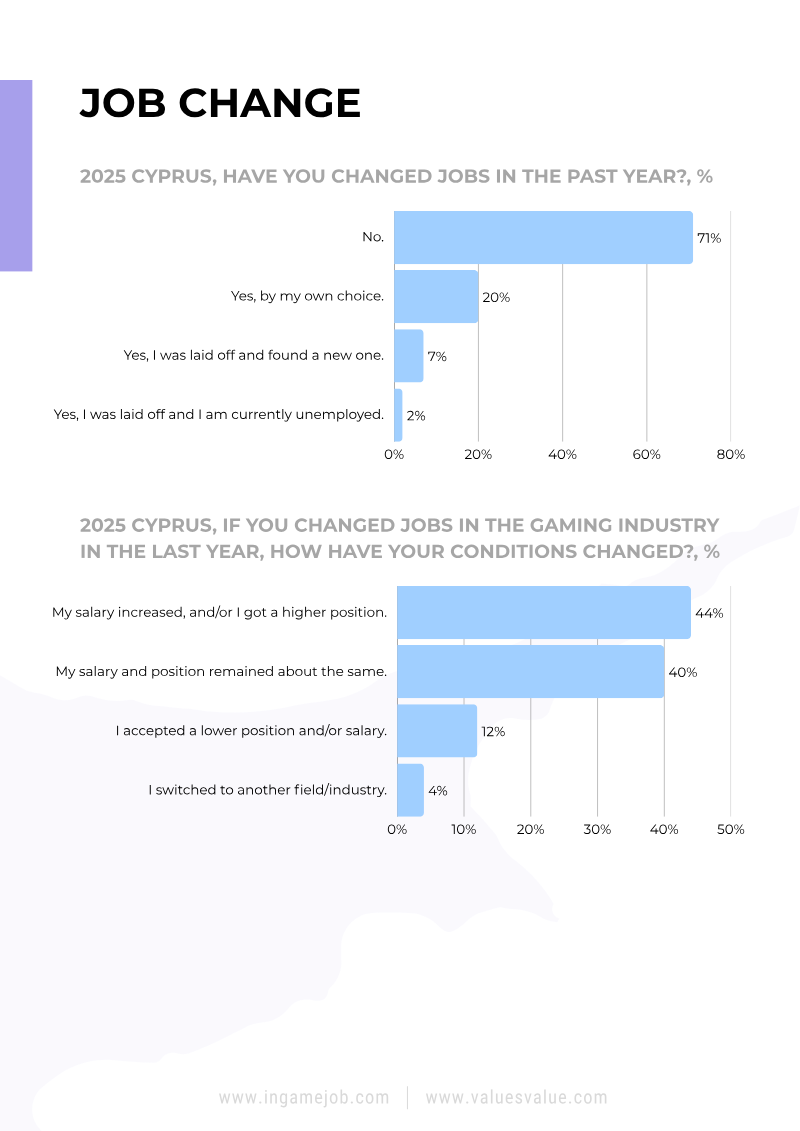

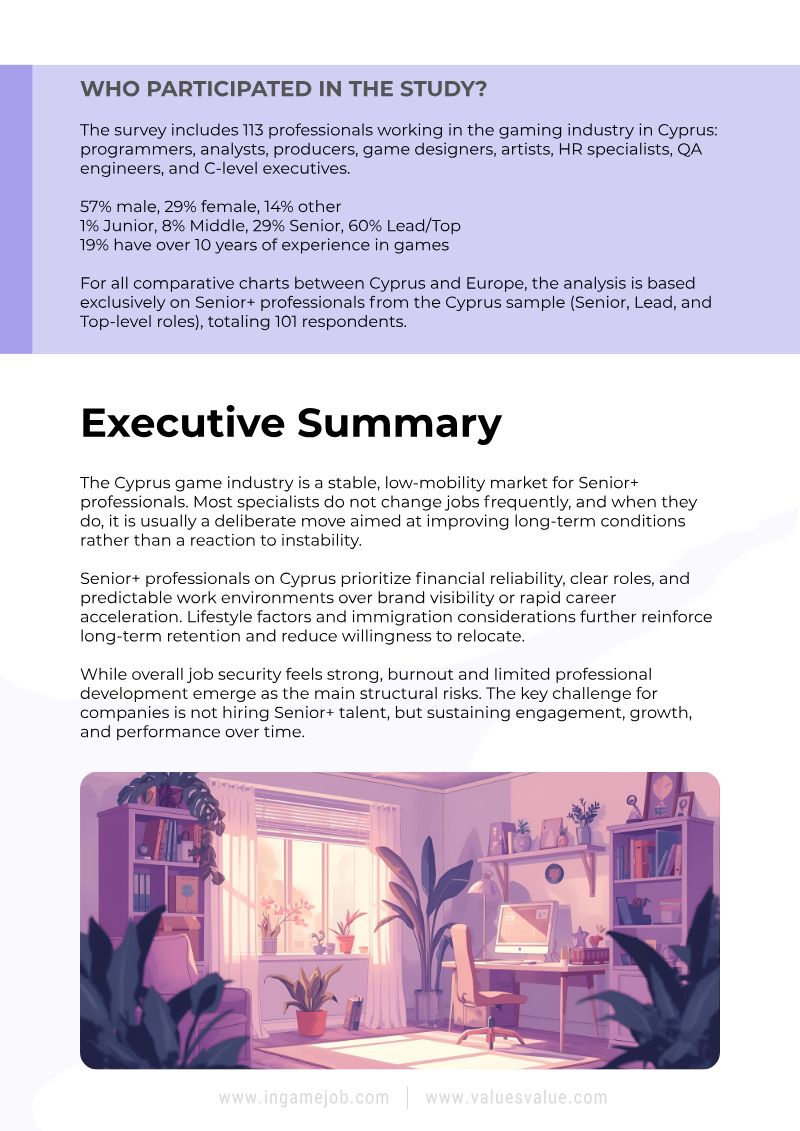

Cyprus Game Industry: Senior+ Employment Landscape 2025

SENIOR+ EMPLO Y: 113 specialists • Anonymous survey • This study is part of the Big Games Industry Employment Survey 2025. As the majority of our Cyprus-based respondents are highly experienced, this report focuses on a like-for-like comparison between Senior+ professionals in Cyprus and their counterparts across Europe.

Values ValueMar 2026

Report

The Romanian Video Games Development Industry

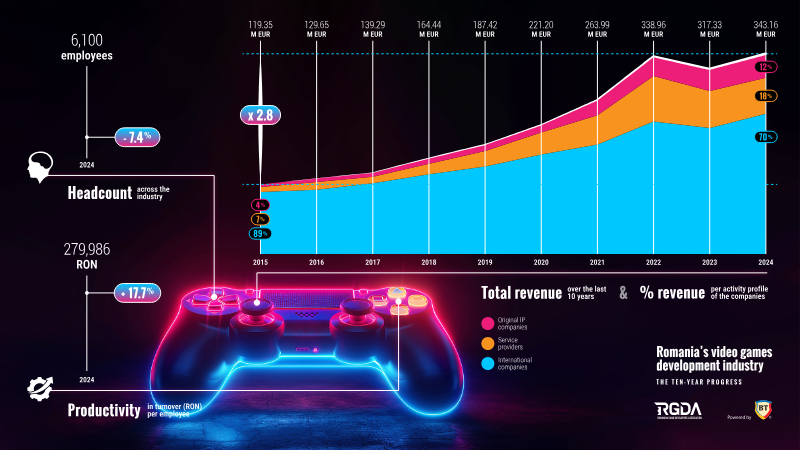

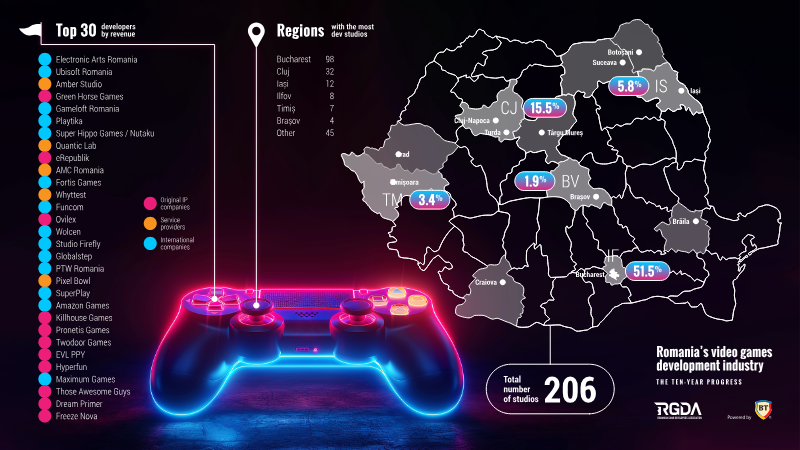

The analysis presents a comprehensive overview of Romania’s video‑game development sector, focusing on revenue performance, geographic concentration, and workforce trends over the past decade. Its central thesis is that the industry has experienced rapid expansion, with total turnover rising from roughly €119 million in 2015 to more than €340 million in 2024, while the number of active studios grew by 70 % within the same period. Revenue concentration is illustrated by a ranking of the top thirty developers, highlighting that multinational publishers such as Electronic Arts Romania (Bucharest) and Ubisoft Romania (Cluj‑Napoca) dominate the market, together accounting for a substantial share of the €340 million total. Mid‑size studios—including Amber Studio (Iași), Green Horse Games (Ilfov), and Playtika (Brașov)—contribute notable percentages, ranging from 5 % to 15 % of overall earnings. The data also maps studio locations, revealing a strong clustering in Bucharest, Cluj‑Napoca, Iași, and Brașov, with emerging hubs in Timișoara, Turda, and Arad. Workforce figures show headcount increasing from 279,986 employees in 2015 to a projected 343,160 in 2024, reflecting a 12 % annual growth rate in personnel. Productivity, measured as turnover per employee, rose by 7.4 % over the ten‑year span, indicating that revenue gains are not solely driven by hiring but also by higher efficiency. Service‑oriented companies and international providers together represent 51.5 % of the sector, underscoring the importance of outsourcing and cross‑border collaborations. The scope encompasses the entire Romanian market, covering all development, publishing, and service activities from 2015 through 2024. Figures appear to be compiled from company‑reported revenues, employee registers, and regional studio counts, suggesting a mixed methodology of financial reporting and industry surveys. Overall, the evidence points to a robust, diversifying ecosystem that is increasingly integrated with the global video‑game supply chain.

RGDA – Romanian Game Developers AssociationJan 2025

Report

Big Games Industry Employment Survey 2025: Salaries, Compensation Trends and State of the Games Sector in Europe

The European games industry entered 2025 in a state of significant distress, characterized by widespread layoffs, stagnant wages, and a sharp decline in employee well-being. Approximately 26% of professionals across the continent experienced layoffs, with junior-level talent bearing the brunt of the instability as 39% exited the sector entirely. This contraction has shifted the labor market from a growth-oriented environment to one focused on cost optimization. Consequently, employee engagement scores have plummeted, and over half of the workforce reports suffering from professional burnout. Financial stability has replaced company mission as the primary motivator for 87% of workers, many of whom are now accepting inferior contract terms or pay cuts to remain employed. Compensation trends reveal a deepening divide based on geography, seniority, and specialization. While median salaries remain highest in the Fighting and MMO genres, reaching up to €90,000 in the EU and UK, a persistent gender pay gap continues to affect technical and C-level roles. Programmers have seen a downward trend in compensation due to increased competition and the rapid integration of artificial intelligence. AI adoption has surged, with over 60% of professionals now using these tools regularly, particularly in analytics and management. However, creative fields like art and quality assurance remain more resistant to AI integration, even as these specific roles face the highest risks of unemployment and long-term job searches. Workplace culture is currently defined by a regression in structured support and a rise in management inefficiency. The number of companies lacking dedicated diversity and inclusion specialists has increased to 67%, while nearly one-third of developers report stagnant professional growth. Although remote flexibility remains a high priority, the shift toward pragmatic relocation suggests that workers are increasingly making career decisions based on cost-of-living calculations rather than traditional ambition. This environment of instability has doubled the rate of long-term unemployment, leaving the European games industry with a workforce that is increasingly disillusioned and prioritized toward survival over innovation.

InGameJob & Values ValueJan 2025