FinancialGungHo Online Entertainment

Notice Regarding the Status of Treasury Share Acquisition: Japan

1 pages~2 min full read

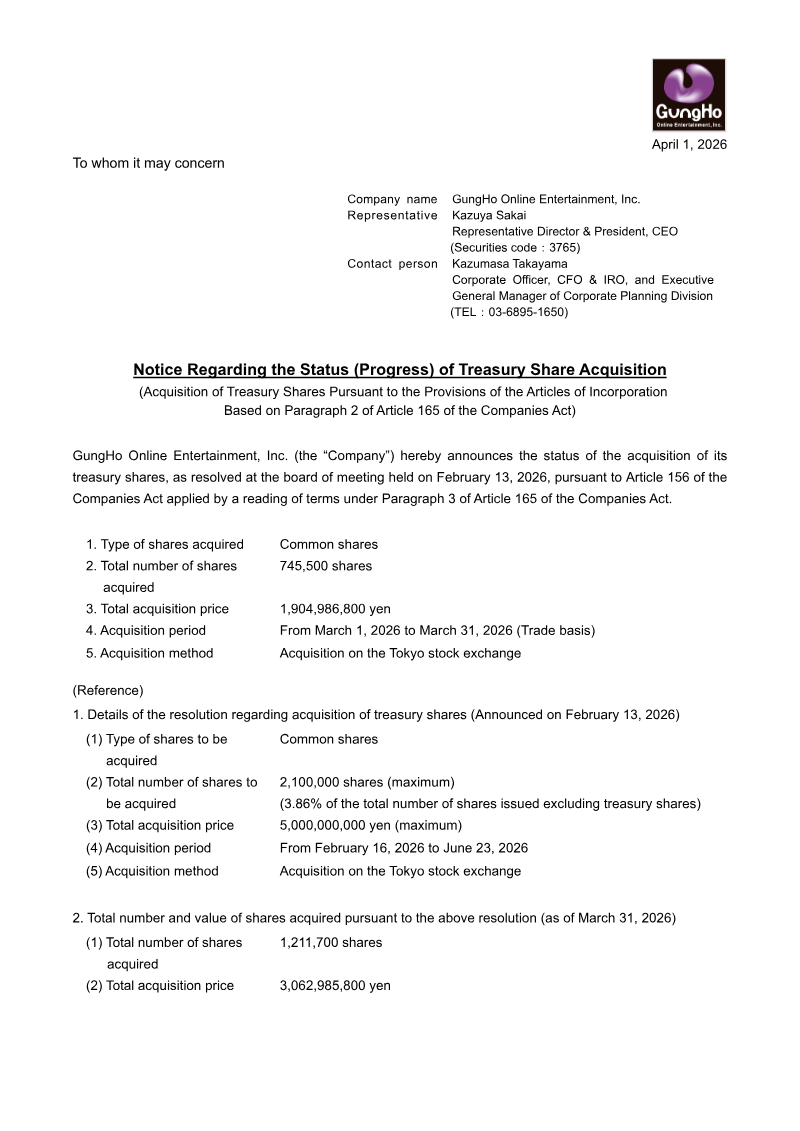

GungHo Online Entertainment, Inc. is actively executing a treasury share acquisition program to manage capital structure and enhance shareholder value. This initiative, authorized by the board of directors on February 13, 2026, operates under the provisions of the Companies Act of Japan. The program focuses exclusively on the repurchase of common shares through open-market transactions on the Tokyo Stock Exchange.

During the month of March 2026, the company acquired 745,500 common shares for a total consideration of 1,904,986,800 yen. When combined with previous activity since the program's inception on February 16, 2026, the cumulative total reaches 1,211,700 shares acquired at a total cost of 3,062,985,800 yen. These figures represent significant progress toward the board’s authorized maximums of 2,100,000 shares and 5,000,000,000 yen, respectively.

The overarching acquisition window remains open until June 23, 2026. The authorized limit of 2,100,000 shares accounts for approximately 3.86% of the total shares issued, excluding existing treasury holdings. By consistently reporting these monthly progress updates, the company maintains transparency regarding its capital allocation strategy and its commitment to the ongoing share buyback mandate within the Japanese equity market.

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2024

GungHo Online Entertainment

GungHo Online Entertainment

GungHo Online Entertainment

GungHo Online Entertainment

Capcom · 2026

Capcom Co. · 2026

Capcom · 2026

Sony Group Corporation · 2026

Marvelous · 2026

Square Enix · 2026

CyberAgent · 2026

Nippon Ichi Software · 2026

Square Enix · 2026

Nihon Falcom Corporation · 2026

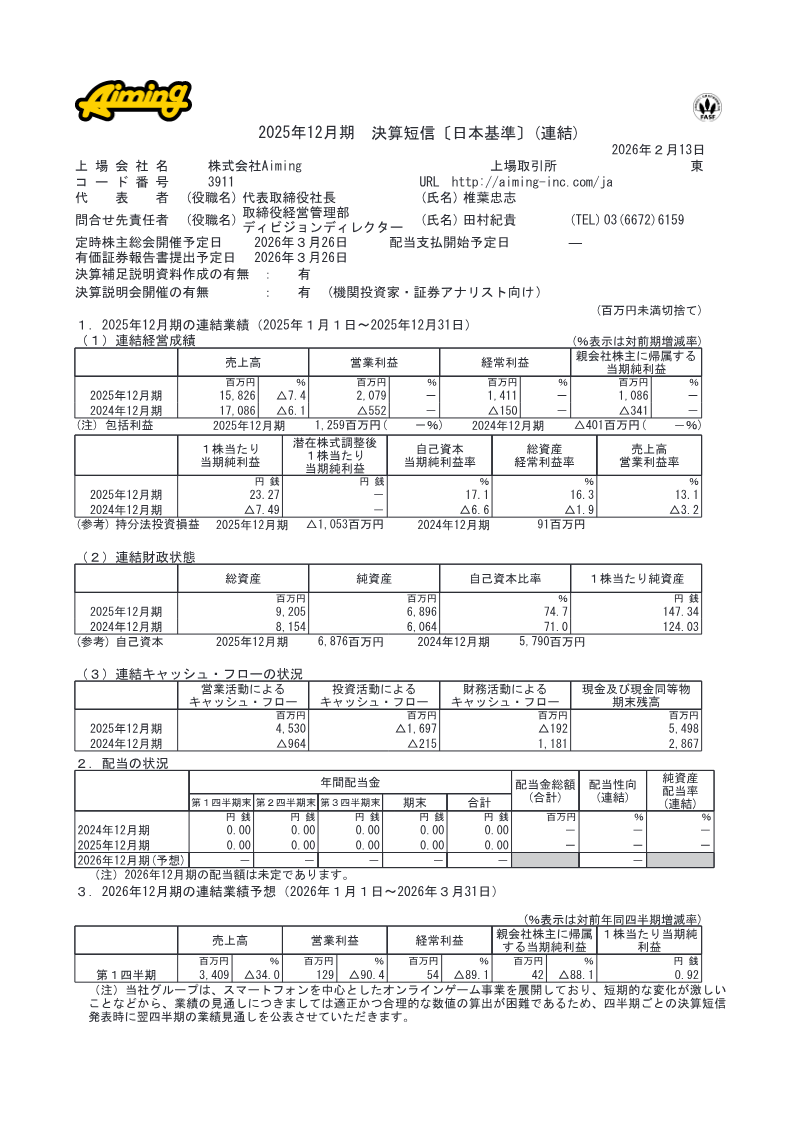

Aiming · 2026

Sega Sammy Holdings · 2026