Related Documents

Report

Newzoo Trend Report 2022: An Overview and Outlook of Virtual Reality

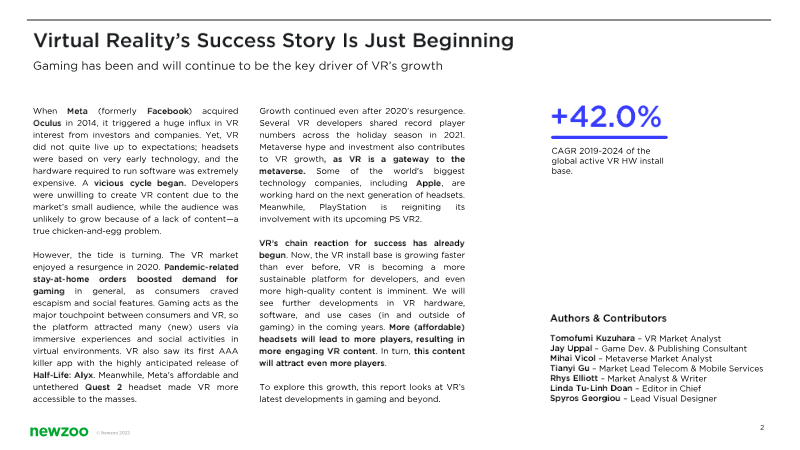

The global virtual reality market is undergoing a significant resurgence, transitioning from a niche hardware segment into a sustainable ecosystem. This evolution is primarily driven by the proliferation of affordable standalone 6DoF devices, such as the Meta Quest and Pico 4, which have lowered barriers to entry for mainstream consumers. While these standalone units may lack the raw performance of high-end PC VR setups, their accessibility has catalyzed rapid growth in the active install base. Data indicates that nearly 60% of VR gamers engage with their headsets at least once a week, signaling high retention and a shift toward consistent usage patterns. Gaming remains the primary gateway for consumer adoption, bolstered by the emergence of high-quality "killer apps" and the popularity of adventure and shooter genres. The market is also seeing a shift toward hybrid monetization models, including downloadable content and subscriptions, alongside an increase in social and fitness-oriented virtual environments. Beyond entertainment, VR technology is becoming increasingly essential for industrial applications. Powerful 3D engines like Unreal and Unity are facilitating the expansion of immersive technology into healthcare simulations, remote architectural planning, and education. The global active VR hardware install base is projected to reach 46 million units by the end of 2024, reflecting a compound annual growth rate of 42.0% since 2019. This sustained momentum is supported by continuous advancements in motion tracking and haptic feedback, as well as substantial investments from major software and hardware firms. As the technology matures, the integration of VR into both consumer lifestyles and professional workflows suggests a long-term trajectory toward widespread cross-industry utility.

NewzooJan 2022

Report

Global Games Market Report 2021: The VR & Metaverse Edition

The global games market is projected to generate $175.8 billion in 2021, representing a marginal 1.1% year-on-year decline. This temporary contraction is primarily driven by pandemic-related supply chain disruptions, hardware shortages, and significant delays in AAA game releases, which have disproportionately impacted the console and PC segments. Despite these challenges, mobile gaming continues to expand, accounting for $90.7$ billion or 51% of total market revenue. The Asia-Pacific region remains the dominant force in the industry, contributing over half of all global revenue and supporting 55% of the world’s three billion players. The long-term outlook for the industry remains robust, with total revenues expected to surpass $218 billion by 2024. This growth is fueled by the permanent acceleration of the metaverse trend, which has transitioned video games from mere entertainment products into essential social hubs. This shift has revitalized the virtual reality sector, particularly following the commercial success of the Oculus Quest 2, and has spurred a wave of consolidation through high-profile mergers and acquisitions. While privacy changes such as the removal of Apple’s IDFA present new hurdles for mobile marketing, the segment’s 4.4% growth indicates continued resilience. Strategic decision-making in this evolving landscape relies on granular performance metrics and consumer insights across dozens of global markets. By tracking key performance indicators such as monthly active users and retention rates for thousands of titles, stakeholders can navigate the complexities of game development and transaction advisory. Ultimately, the integration of social connectivity, immersive hardware, and mobile accessibility ensures that the gaming industry will continue its upward trajectory beyond the immediate disruptions of the early 2020s.

NewzooJan 2021

Report

Global Games Market Report 2022

The global games market entered a corrective phase in 2022, with annual revenues projected to decline by 4.3% to $184.4 billion. This contraction follows a period of unsustainable pandemic-driven expansion and is further exacerbated by macroeconomic inflation, supply chain disruptions, and a sparse release schedule for major titles. Despite this short-term dip, the industry maintains a massive engagement base of 3.2 billion players and is expected to resume an upward trajectory, reaching an estimated $211.2 billion by 2025. While mature markets like North America and Asia-Pacific are experiencing revenue declines, emerging mobile-first regions such as Latin America and the Middle East & Africa continue to show positive growth. The industry is currently undergoing a structural shift toward platform-agnostic ecosystems and hybrid monetization strategies. As traditional mobile advertising faces challenges from privacy policy changes like Apple’s IDFA, console and PC developers are increasingly adopting programmatic in-game advertising to monetize the hundreds of millions of players who do not make direct purchases. This shift is supported by major platform holders like Sony and Microsoft, who are integrating non-intrusive, blended advertisements to create recurring revenue streams. Furthermore, the rise of user-generated content, cloud gaming, and blockchain-based models is redefining how players interact with and derive value from digital environments. Future market stability is increasingly tied to ecosystem-based analysis rather than hardware-specific metrics, reflecting a broader trend of cross-platform play and industry consolidation. Regulatory shifts in China have also prompted a strategic pivot toward global expansion in other emerging markets. As the industry evolves, success will likely depend on balancing diverse monetization models with authentic player experiences, while leveraging new technologies in virtual reality and cloud infrastructure to maintain long-term engagement across a diversifying global audience.

NewzooJan 2022

Report

Newzoo Metaverse Report 2021

The metaverse represents the evolution of gaming from a service into a persistent, infinitely scaling platform characterized by social interaction, user-generated content, and functioning economies. Driven by technological advancements and the social shifts of the COVID-19 era, virtual spaces now host non-gaming activities like concerts and brand activations that attract tens of millions of participants. This transition is supported by a highly receptive consumer base, with 70% of gamers expecting these social hubs to increase their playtime. The industry is moving toward a direct-to-avatar economy where digital identity and creator-led markets are central to engagement across platforms like Roblox, Fortnite, and Avakin Life. Blockchain technology serves as a primary catalyst for this shift, enabling decentralized economies and play-to-earn models that provide players with true digital ownership. While current hurdles include high transaction fees and environmental concerns associated with early NFT models, the sector is transitioning toward scalable, green solutions like Layer 2 protocols. Establishing interoperable digital identities and seamless marketplaces is essential for aligning the economic interests of developers and creators. Furthermore, the move toward Web 3.0 requires a shift in the digital supply chain toward player-owned assets and open standards, such as Pixar’s Universal Scene Description, to ensure cross-platform collaboration. Despite this momentum, significant structural and technical challenges remain. Achieving massive concurrency—moving beyond sharded instances to thousands of users in a single persistent world—requires cloud-native infrastructure and radical improvements in network protocols. Additionally, the industry must navigate regional fragmentation caused by government regulations and the need for modernized IP laws. Ethical risks, including deepfakes, unmoderated content, and identity theft, necessitate a focus on safety and open standards. Ultimately, the games industry is positioned to lead the development of a mobile-accessible, community-driven metaverse that complements physical reality through democratized monetization and high-fidelity digital twins.

NewzooJan 2021