Related Documents

Report

Guide to Growing Chinese Gaming Apps Overseas

Chinese gaming developers are aggressively expanding their global footprint by leveraging sophisticated monetization models and high-volume, AI-driven marketing strategies. The primary objective for these publishers is to balance the high revenue potential of mature markets like the United States, Japan, and South Korea against the rising costs of user acquisition. By prioritizing video advertising, which currently yields the highest Day 7 return on ad spend at 21%, developers are successfully capturing market share in competitive strategy and RPG segments. Success in these international territories is increasingly predicated on hyper-localization and technological integration. Publishers are utilizing generative AI to streamline the production of localized ad creatives, voice-overs, and performance-tested copy, allowing for rapid iteration and regional customization. Leading titles demonstrate that high-engagement gameplay loops—such as the inclusion of social hangout spaces, customizable home systems, and minigame integrations—are essential for sustaining long-term retention. These efforts are further bolstered by strategic partnerships with local influencers and the implementation of innovative, time-limited gacha mechanics. To maintain consistent growth, developers are diversifying their engagement tactics through gamified live events, including seasonal collections and interactive board-style challenges. These features, combined with trial character systems, allow publishers to cater to varied player motivations while maintaining a steady revenue stream. By synthesizing competitive intelligence with agile content updates, Chinese gaming apps are effectively navigating the complexities of global expansion, ensuring that both monetization and user interest remain high across diverse geographic regions.

EAJan 2025

Report

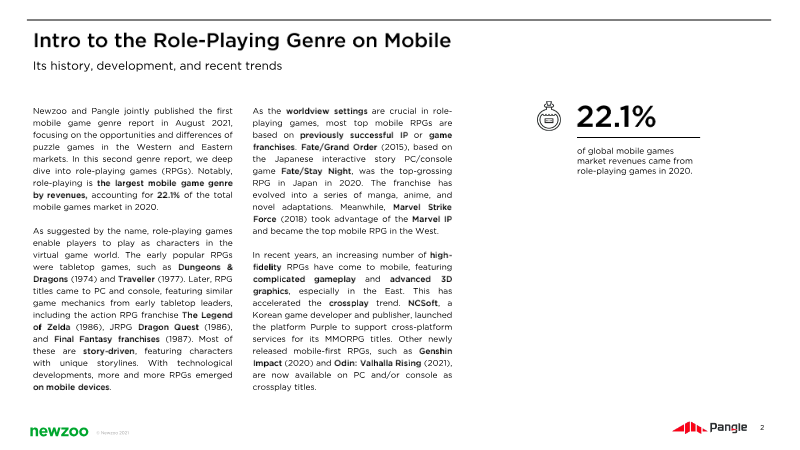

Mobile Game Genre Report: Role-Playing Games 2021

Role-playing games represent the most lucrative segment of the global mobile gaming market, generating $18.5 billion in 2020 and accounting for nearly a quarter of all mobile gaming revenue. This market is geographically concentrated in East Asia, where China, Japan, and South Korea collectively generate over 70% of the genre's global earnings. The landscape is characterized by the dominance of domestic publishers and a heavy reliance on established intellectual properties from movies, literature, and PC ports, which account for approximately half of the top-performing titles. The Marvel franchise serves as a primary example of this trend, exerting a pervasive influence on player acquisition and revenue generation through its immense brand saturation. While IP-based titles leverage organic recognition, original properties must utilize aggressive influencer marketing and high-quality creative advertisements to compete. Long-term sustainability in the genre is driven by consistent content updates, social competitive mechanics, and time-limited gacha systems. Although in-app purchases remain the primary revenue driver—particularly among high-income male audiences—there is a significant shift toward hybrid monetization. Approximately 83% of players now accept non-disruptive rewarded video ads as a means to progress without direct spending. To navigate evolving privacy regulations and tracking challenges, developers are increasingly prioritizing high-value user signals within the first 24 hours of gameplay. Interactive playable ads have emerged as a highly effective acquisition tool, occasionally increasing eCPMs by over 200%. By combining traditional spending triggers like battle passes and limited-time events with sophisticated ad integration, publishers are successfully monetizing both high-spending "whales" and non-paying users to maintain growth in an increasingly competitive global market.

PangleJan 2021

Report

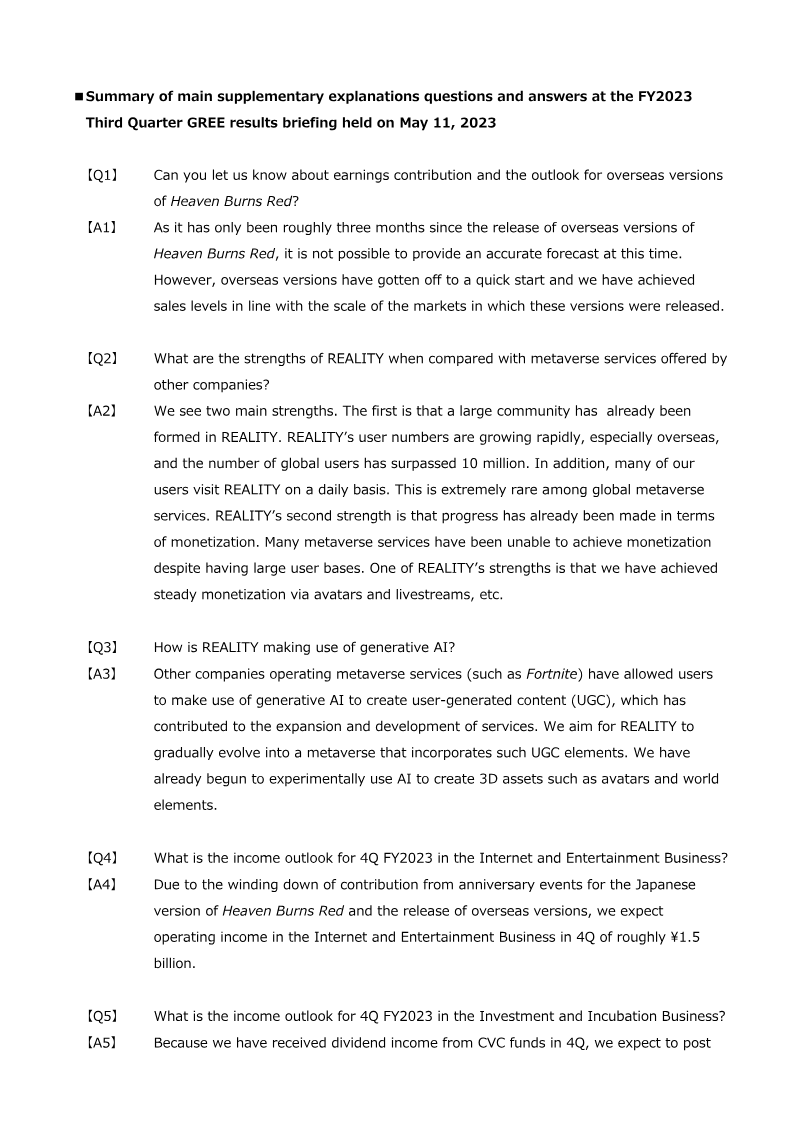

FY2023 Third Quarter GREE Results Briefing: Summary of Supplementary Explanations

The briefing clarifies GREE’s financial outlook and strategic positioning for FY2023, focusing on the third quarter results. It reports that overseas releases of “Heaven Burns Red” have begun to generate sales consistent with market size, though a precise forecast remains unavailable due to the short time frame. In the Internet and Entertainment segment, operating income for Q4 is projected at approximately ¥1.5 billion, reflecting a decline from the Japanese version’s anniversary event contributions but offset by overseas expansion. The company highlights its metaverse platform, REALITY, as a key growth driver. REALITY boasts over 10 million global users, with daily engagement rates that surpass many competitors, and has achieved steady monetization through avatar sales and livestreaming. GREE plans to enhance the platform with generative AI, enabling user‑generated 3D content such as avatars and world elements, mirroring approaches seen in other metaverse services. For the Investment and Incubation Business, Q4 operating income is expected to reach roughly ¥0.5 billion, largely supported by dividend receipts from corporate venture capital funds. Overall, the briefing underscores GREE’s focus on expanding overseas markets, monetizing its metaverse ecosystem, and leveraging AI to sustain growth across its entertainment and investment portfolios.

GREE

Financial

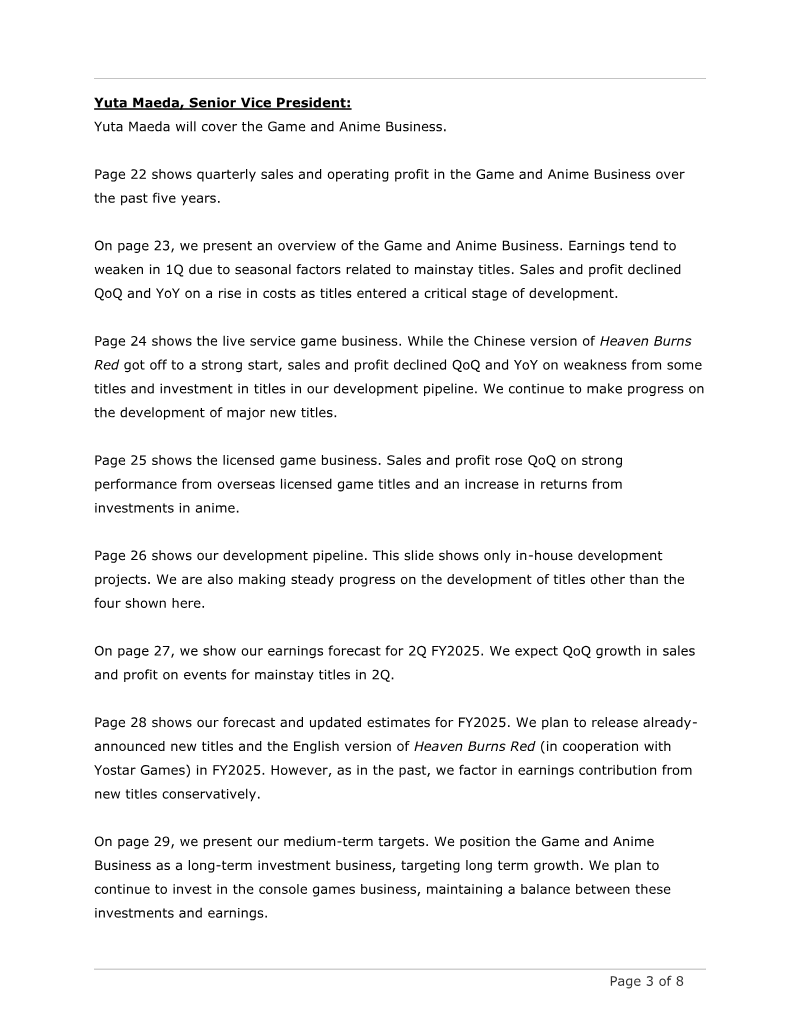

FY2025 First Quarter Financial Results Briefing

The briefing presents FY2025 first‑quarter results for GREE, Inc., highlighting a net sales figure of ¥12.9 billion and an operating loss of ¥0.1 billion, largely driven by valuation losses in the Investment Business and foreign‑exchange impacts from yen appreciation. While Game and Anime, Metaverse, and DX segments exceeded forecasts—thanks to strong performance of the Chinese version of *Heaven Burns Red*, continued growth in platform and VTuber services, and solid DX profitability—the Investment Business posted a ¥0.8 billion operating loss due to crypto‑asset valuation declines and write‑downs on maturing funds. Variable costs rose from advertising spend and investment losses, whereas fixed costs remained relatively stable. Geographically, the company operates globally with significant overseas assets; the report notes a ¥1.4 billion FX loss affecting ordinary and net profit. The management plan positions Metaverse and DX as continuous‑growth businesses targeting a 120–140 % CAGR in operating profit, while Game and Anime are treated as long‑term investment assets. Medium‑term targets emphasize aggressive investment in VTuber talent and DX product development, with expectations of profitability from the VTuber segment by FY2026 and accelerated growth in DX by FY2027. Methodologically, the briefing relies on quarterly financial statements, segment‑level performance data, and investment portfolio valuations. The Investment Business’s dual GP/LP structure is explained to contextualize volatility, with an emphasis on long‑term stability despite short‑term losses. Overall, the company projects FY2025 results in line with prior forecasts but anticipates slightly lower Game and Anime sales, offset by higher operating profit from continuous‑growth segments.

GREE