Related Documents

Report

Factbook: Third Quarter of Fiscal Year Ending March 31, 2026

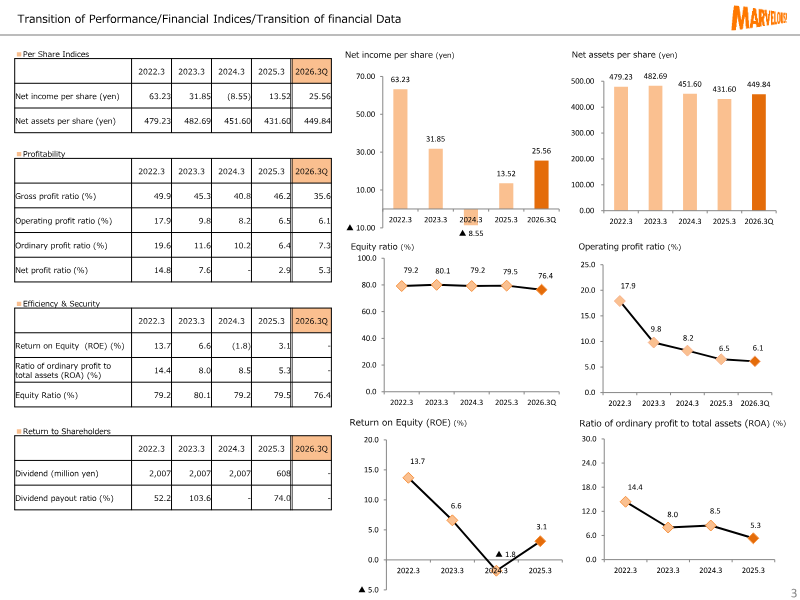

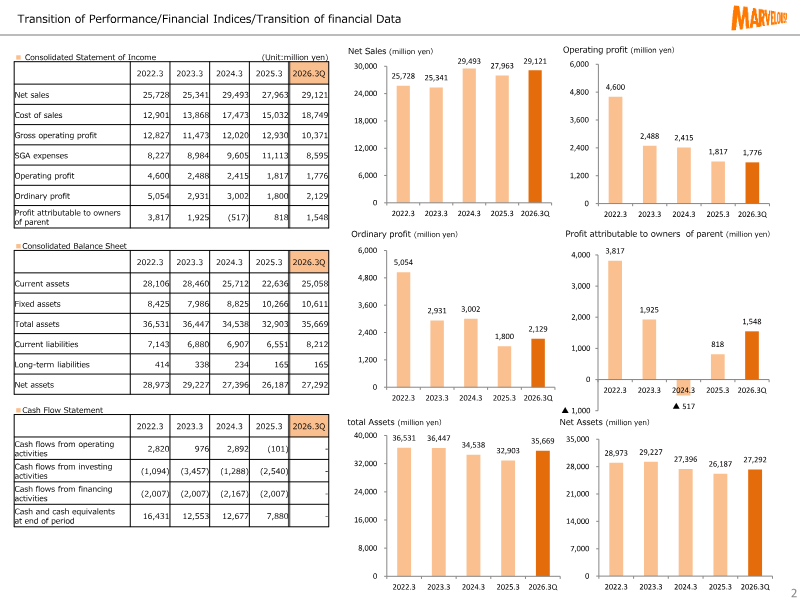

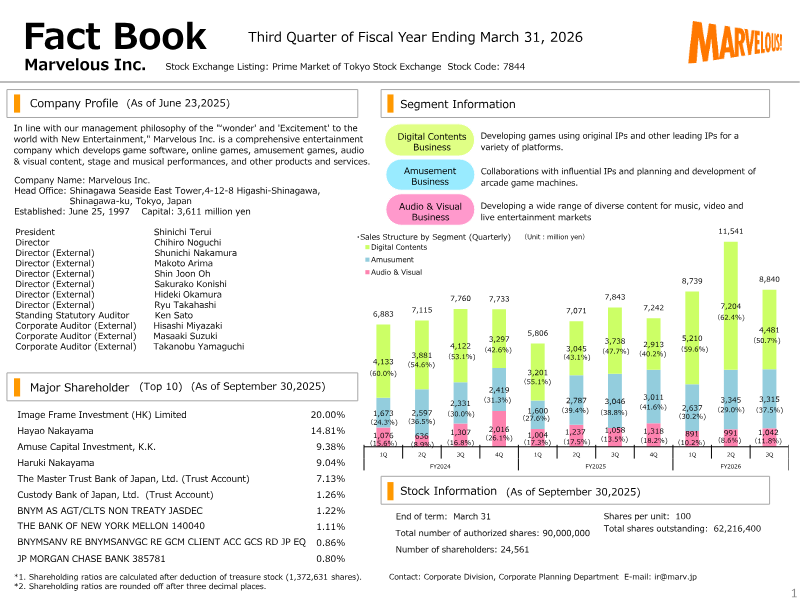

Marvelous Inc., listed on Tokyo’s Prime Market, released its third‑quarter financial results for the fiscal year ending March 31 2026. The company’s core business spans digital content, amusement, audio‑visual production and live entertainment, with a focus on original IPs and collaborations. Revenue rose to ¥29.1 billion in Q3, up 4.5% from the prior quarter and 10.6% year‑on‑year, driven primarily by digital content sales of ¥7.2 billion and amusement revenue of ¥3.0 billion. Gross operating profit reached ¥10.4 billion, a 12% increase over Q2 and a 9% rise versus the same period last year, reflecting improved cost control in production and marketing. Operating profit fell to ¥1.8 billion, a 12% decline from Q2, largely due to higher selling‑general‑administrative expenses of ¥8.6 billion compared with ¥7.9 billion in Q2. Net income attributable to shareholders was ¥1.5 billion, down 18% from Q2, with a net profit margin of 5.3%. The company’s cash‑flow position remained solid, with operating cash flow of ¥2.8 billion and a cash‑equivalent balance of ¥16.4 billion at quarter end. Geographically, the report covers Japan and overseas markets where Marvelous operates. The data derive from consolidated financial statements prepared under Japanese GAAP, covering all subsidiaries and affiliates. Key metrics such as return on equity (13.7%) and asset turnover (0.82) indicate healthy profitability, while dividend payout remained at 52% of net income. Overall, the quarter shows revenue growth but margin pressure from higher operating costs, prompting management to focus on cost efficiency and portfolio diversification.

Marvelous

Financial

Financial Results Briefing Session of Fiscal Year Ended December 31, 2025 [17,284KB]

GungHo Online Entertainment’s FY 2025 financial briefing outlines a strategic pivot from Japan‑centric mobile development toward global expansion, emphasizing action titles on consoles and PCs. The company reports a 64.1 % overseas net‑sales ratio in FY 2025, up from 47.7 % in 2019 and 56.2 % in 2020, reflecting intensified sales in North America and Europe through new releases such as “Let It Die: Inferno” on PlayStation 5, Steam, and Nintendo Switch. The launch of nine global titles in 2025, including the “Ragnarok” series and “Puzzle & Dragons,” is highlighted as a key growth driver, with the latter celebrating its 5 000‑day anniversary and hosting cross‑platform events to boost user activity. Financially, consolidated net sales fell by 1.3 % YoY to ¥125.3 billion, driven mainly by declines in mobile titles and “Ragnarok”‑related revenue under subsidiary Gravity. Operating profit contracted by 9.3 % YoY to ¥276 million, as SG&A expenses rose due to increased advertising spend and personnel costs following the full acquisition of Alim in December 2024. Non‑consolidated results remained flat, but mobile sales slipped and Gravity’s “Ragnarok” titles underperformed, contributing to the consolidated loss. The briefing covers a global geographic scope—North America, Europe, Latin America, and Asia—with a 2025 focus on launching titles in over 150 countries. Methodologically, data derive from consolidated financial statements and quarterly performance metrics, with a clear emphasis on aligning product development with international market demand.

GungHo Online Entertainment

Report

Square Enix Special Feature: Erdrick Trilogy Reimagined

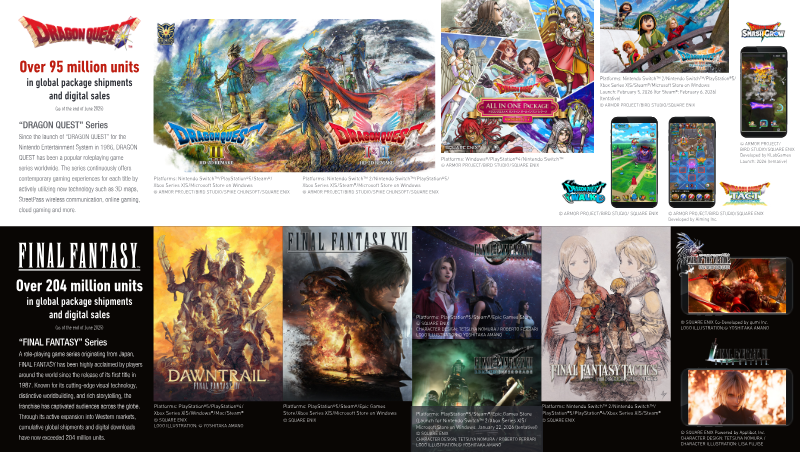

The Dragon Quest franchise continues to expand its global footprint, reaching over 95 million units in total shipments and digital sales as of June 2025. A central focus of the current release strategy is the reimagining of the foundational Erdrick Trilogy through HD-2D remakes. Dragon Quest I & II HD-2D Remake is scheduled for a February 5, 2026, launch on a wide array of platforms, including the Nintendo Switch 2, PlayStation 5, Xbox Series X|S, and PC via Steam and the Microsoft Store. This multi-platform approach reflects a broader commitment to utilizing contemporary technology to modernize classic role-playing experiences for a global audience. Beyond the core Dragon Quest series, the broader portfolio demonstrates significant market penetration across several flagship intellectual properties. The Final Fantasy franchise has surpassed 204 million units globally as of mid-2025, supported by the ongoing expansion of Final Fantasy XIV: Dawntrail and the continued rollout of Final Fantasy VII Rebirth across various ecosystems. Additionally, the Kingdom Hearts series, a collaborative effort with Disney, has achieved over 38 million units in sales, with new entries currently in development for unspecified launch windows. The strategic roadmap emphasizes cross-platform accessibility and the revitalization of legacy content. By targeting next-generation hardware like the Nintendo Switch 2 alongside established consoles and PC storefronts, there is a clear intent to maximize reach across diverse geographic markets. This strategy is complemented by a robust pipeline of mobile and niche titles, including Dragon Quest Tact and various entries in the Bravely Default and Octopath Traveler series, ensuring a steady cadence of content across the role-playing game segment through 2026.

Square EnixSept 2025

Financial

Fact Book 2021

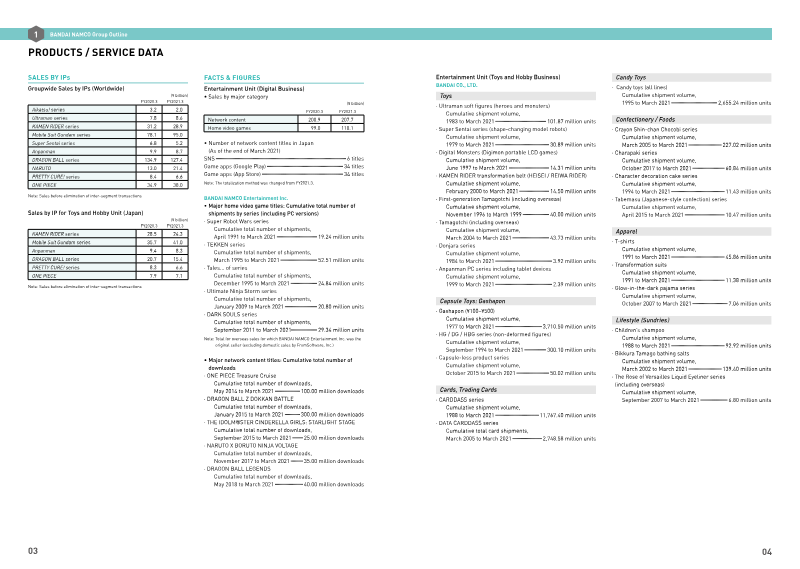

The 2021 Fact Book presents a comprehensive overview of Bandai Namco Holdings’ strategic direction, emphasizing its transformation into a globally integrated entertainment conglomerate and its commitment to corporate social responsibility. Central to the narrative is the thesis that sustained growth across toys, video games, animation and amusement can be achieved through diversified product portfolios, expansive international operations, and proactive sustainability initiatives. The company’s evolution is traced from a collection of independent toy, arcade‑machine and media firms to a unified group after the 2005‑2007 merger of Bandai and Namco. Key milestones include the launch of flagship lines such as Gundam models (over 500 million units shipped), Tamagotchi (exceeding 20 million units), and Zatchbell Battle (300 million units), as well as the development of major video‑game franchises—TEKKEN, DARK SOULS III and Tales—collectively surpassing 50 million sales. International expansion is evident through subsidiaries and regional headquarters in North America, Europe and Asia, reinforced by repeated listings on the Tokyo Stock Exchange and industry recognitions such as Cannes Best Actor and TSE awards. Environmental and social performance data for fiscal year 2021 highlight a suite of CSR actions, including CO₂ reduction targets, supply‑chain safety measures and work‑life‑balance programmes, all framed within the “NEXT STAGE” mid‑term plan aimed at deepening engagement with a mature fan base and broadening cross‑media offerings. The Fact Book thus underscores Bandai Namco’s dual focus on market leadership and sustainable corporate practices across a worldwide footprint and multiple entertainment segments.

Bandai NamcoSept 2021