FinancialNippon Ichi Software

Notice Regarding Differences in Earnings Forecasts

14 Nov 20252 pages~2 min full read

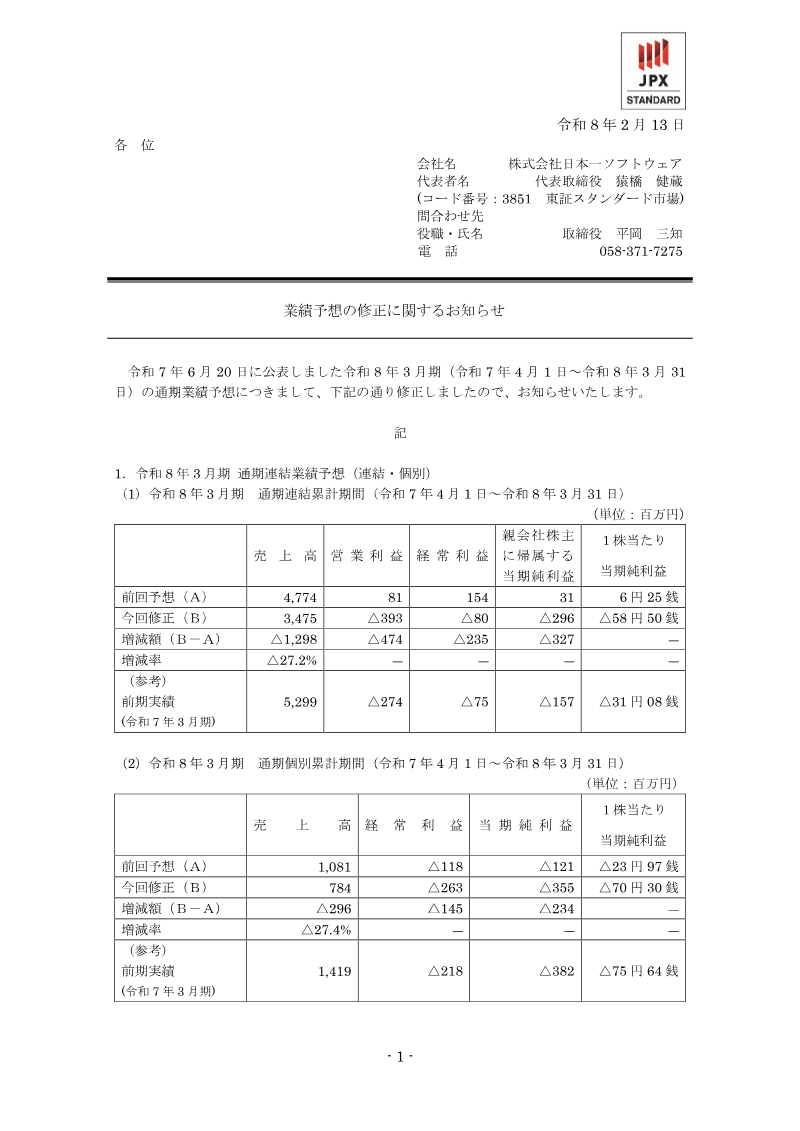

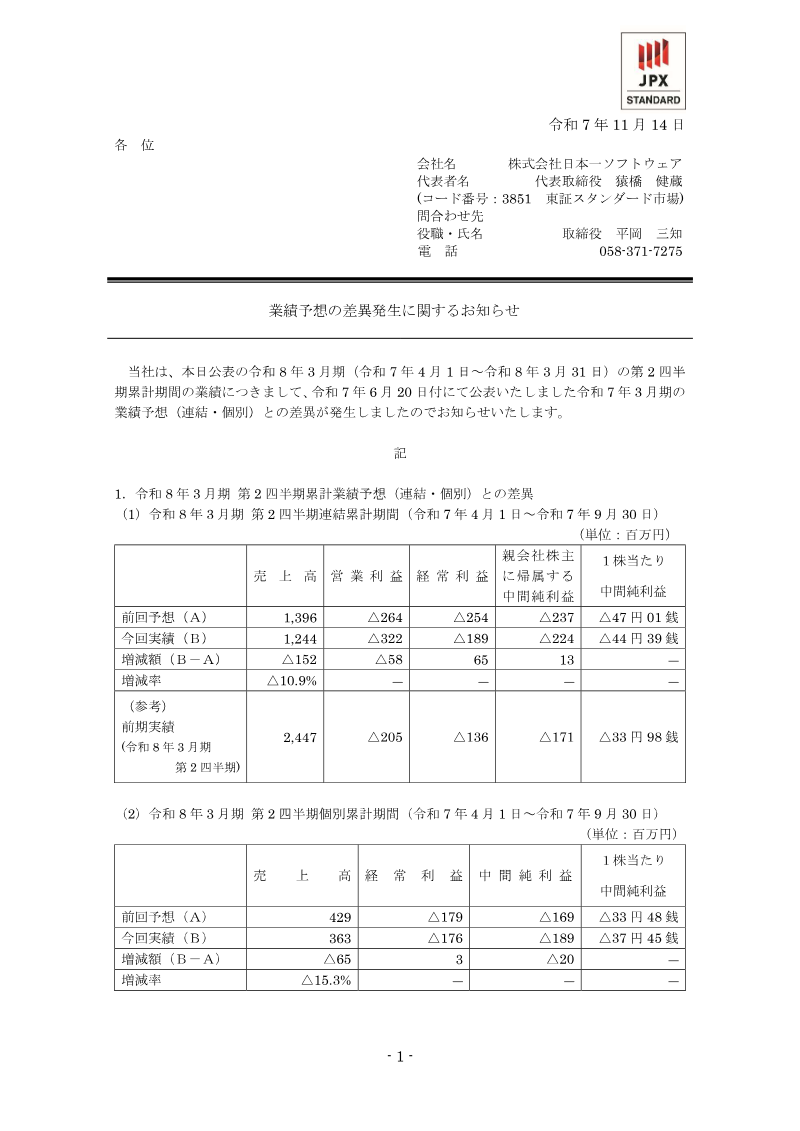

The company missed its Q2 fiscal 2026 consolidated net sales target by 10.9%, reporting ¥1,244 million against a forecast of ¥1,396 million.

See it on page 1Operating losses for the second quarter widened to ¥322 million, exceeding the projected loss of ¥264 million.

See it on page 1Weaker-than-expected domestic demand for new game titles was the primary driver for the revenue shortfall and reduced unit sales.

See it on page 2Foreign-exchange gains resulting from yen depreciation partially offset the quarterly performance gap, helping to lift ordinary and net profit figures relative to forecasts.

See it on page 1Despite the Q2 miss, the company has maintained its full-year consolidated outlook, which projects ¥4,774 million in sales and an operating profit of ¥81 million.

See it on page 2Standalone performance was weaker than consolidated results, with Q2 sales of ¥363 million missing the forecast by 15.3%.

See it on page 2The notice serves to inform shareholders of a variance between the company’s actual second‑quarter performance for the fiscal year ending March 2026 and the forecast issued on 20 June 2025. For the consolidated period April 1 to 30 September 2025, net sales reached ¥1,244 million, 10.9 % below the prior estimate of ¥1,396 million, while operating profit fell to a loss of ¥322 million versus the projected ¥264 million loss. Net profit attributable to the parent’s shareholders declined to ¥44 million per share from the forecasted ¥47 million. On a standalone basis, sales were ¥363 million, 15.3 % lower than the ¥429 million expected, and net profit per share slipped to ¥45 million from ¥48 million. The primary driver of the shortfall was weaker domestic demand for newly released titles, which reduced unit sales below expectations. Conversely, a stronger yen depreciation generated foreign‑exchange gains that lifted both ordinary profit and net profit relative to the forecast.

Despite the quarterly miss, the company retains its full‑year outlook unchanged. The revised full‑year consolidated forecast anticipates sales of ¥4,774 million, a 9.9 % decline year‑on‑year, with operating profit turning positive to ¥81 million after a prior loss, ordinary profit of ¥154 million, and net profit attributable to shareholders of ¥31 million. On a standalone basis, full‑year sales are projected at ¥1,081 million, down 23.8 % YoY, with ordinary loss of ¥118 million and net loss of ¥121 million. The company commits to updating the outlook promptly should subsequent developments warrant revision.