Related Documents

Financial

Semi‑Annual Report: April 1 2024 – September 30 2024

Nippon Ichi Software’s semi-annual report for the period of April 1, 2024, to September 30, 2024, details a challenging fiscal first half characterized by a transition to a net loss position. The primary thesis of the report reflects a strategic focus on strengthening development and sales capabilities amid a volatile global economic environment marked by rising prices and geopolitical uncertainty. Despite these headwinds, the group continues to invest in its core entertainment business while maintaining secondary operations in student dormitory management. Financial data indicates a significant downturn compared to the previous year. Net sales fell by 20.0% to 2,447 million yen, resulting in an operating loss of 205 million yen and a net loss attributable to owners of the parent of 171 million yen. This contrast is sharp against the prior year’s net profit of 290 million yen. The entertainment segment, which accounts for the vast majority of revenue, saw a 20.6% decline in sales, attributed partly to the timing of major releases. Key activities during the period included the domestic launch of titles such as Disgaea 7: Vows of the Virtueless (Complete Edition) and preparations for the group’s first simultaneous global release, Phantom Brave: The Lost Hero. The scope of the report covers consolidated operations across Japan, North America, Europe, and Asia. Geographically, the group relies heavily on the localization and distribution of its titles through digital platforms like Steam, PlayStation Network, and Nintendo eShop. Methodologically, the findings are based on consolidated financial statements prepared under Japanese accounting standards and subjected to a quarterly review by Tokai Kaikeisha. While the group faced a decrease in total assets to 10.58 billion yen and a negative operating cash flow of 284 million yen, it maintains a robust equity ratio of 71.4%, suggesting continued long-term financial stability despite short-term earnings volatility.

Nippon Ichi SoftwareNov 2024

Financial

Nippon Ichi Software Securities Report FY2024

Nippon Ichi Software concluded its 31st fiscal year on March 31, 2024, reporting consolidated net sales of ¥5.34 billion, a 10.5% increase over the previous year. This growth was primarily driven by the entertainment segment, which accounts for over 98% of total revenue, bolstered by strong digital sales and the international performance of titles such as Disgaea 7. Despite the rise in top-line revenue, operating profit declined by 46.2% to ¥401 million, and ordinary profit fell 10.5% to ¥842 million. These contractions are attributed to rising manufacturing costs, increased advertising expenditures, and higher general administrative expenses. The geographic distribution of revenue underscores a heavy reliance on the North American market, which contributed ¥3.14 billion, or 58.8% of total sales. NIS America remains a critical subsidiary in managing these international operations, particularly through partnerships with major entities like Nintendo and Koei Tecmo America. To mitigate risks associated with high dependency on existing franchises and foreign exchange volatility, management is prioritizing the development of new intellectual property with a domestic sales target of 200,000 units per title. This strategy involves enhancing graphic quality and strengthening internal development systems to remain competitive amid shifting hardware trends. Financially, the group maintains a stable foundation with ¥5.36 billion in cash and deposits, though it saw an increase in long-term debt to ¥8.8 billion to fund capital investments, including significant land acquisitions. Critical audit matters identified for the period include the valuation of ¥674.6 million in game content inventories and the estimation of ¥426.7 million in refund liabilities for overseas sales. Despite these complexities, internal controls over financial reporting were deemed effective, ensuring the accuracy of the group’s financial position as it seeks to balance rising development costs with the pursuit of global market expansion.

Nippon Ichi SoftwareJun 2024

Financial

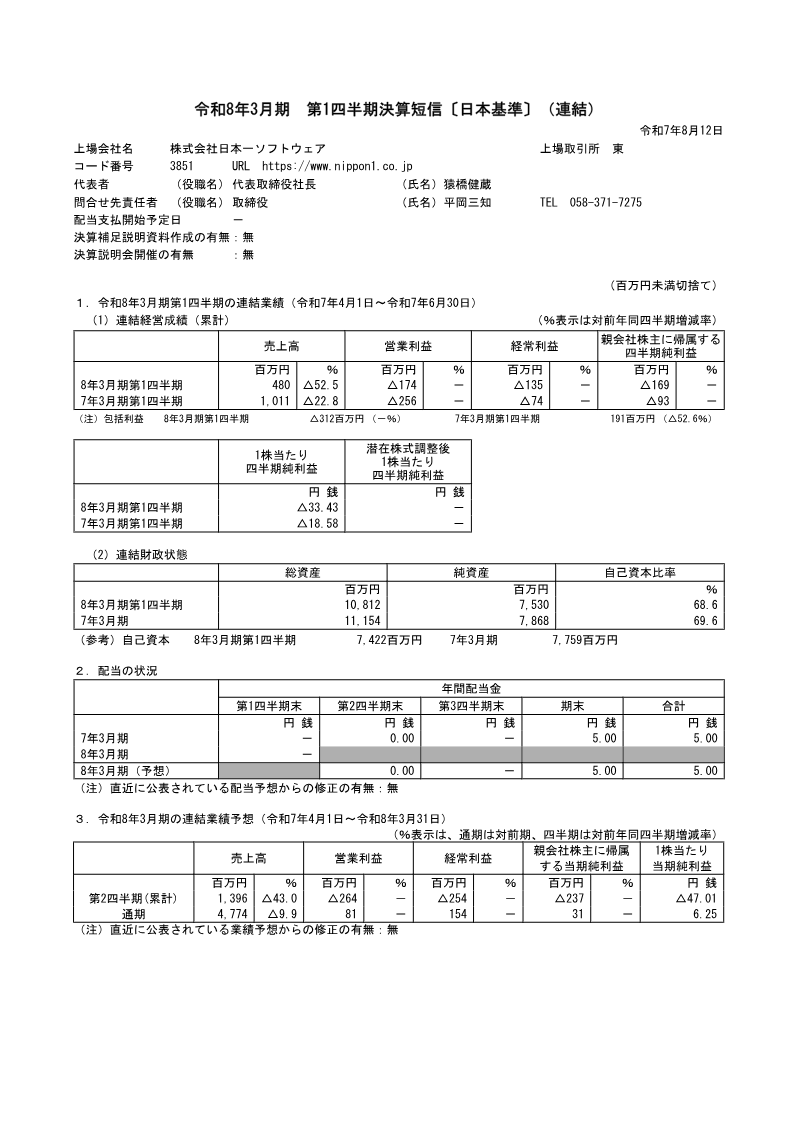

Nippon Ichi Software Q1 FY2026 Financial Results (Japanese GAAP)

Nippon Ichi Software’s financial results for the first quarter of the fiscal year ending March 31, 2026, reveal a challenging period characterized by significant year-over-year declines in revenue and continued operating losses. Covering the period from April 1, 2025, to June 30, 2025, the data shows consolidated net sales fell 52.5% to 480 million yen. While the operating loss of 174 million yen represented a slight improvement over the 256 million yen loss in the previous year's first quarter, the ordinary loss widened to 135 million yen, and the net loss attributable to owners of the parent increased to 169 million yen. The entertainment segment, which constitutes the core of the business, saw sales drop 54.4% to 450 million yen. Management attributes this performance to the timing of product cycles, noting that major titles like Fuuraiki 5 and Renju were still in development during the quarter with releases scheduled for the second quarter. Despite the downturn in domestic package software sales, the company maintained its focus on multi-platform digital distribution via PlayStation Network, Nintendo eShop, and Steam, alongside international localization efforts in North America, Europe, and Asia. The smaller student dormitory business saw a 25.4% increase in revenue but remained a minor component of the overall corporate portfolio. The financial position remains stable with total assets of 10.8 billion yen and an equity ratio of 68.6%. Cash and deposits increased to 5.5 billion yen, though net assets decreased by 337 million yen due to the quarterly loss and foreign currency translation adjustments. Despite the weak start to the fiscal year, the company maintained its full-year forecast of 4.77 billion yen in sales and 81 million yen in operating income, suggesting an expectation of recovery driven by upcoming software releases. The results have undergone a formal interim review by independent auditors, confirming the accuracy of the financial statements under Japanese accounting standards.

Nippon Ichi SoftwareAug 2025

Financial

Nippon Ichi Software Securities Report FY2025

Nippon Ichi Software faced a challenging 32nd fiscal year ending March 31, 2025, characterized by a transition from profitability to a consolidated net loss of ¥157 million. While net sales remained relatively stable at approximately ¥5.3 billion—supported by robust North American performance and digital download revenue—the company recorded an operating loss of ¥274 million. This downturn was primarily driven by a 21.3% surge in manufacturing costs, increased research and development investments for high-performance consoles, and significant extraordinary losses related to affiliated companies. The geographic scope of operations highlights a heavy reliance on the North American market, which contributed ¥3.06 billion to total sales, and a concentrated distribution network where four major partners account for nearly 32% of revenue. To mitigate risks associated with high development costs and dependence on core intellectual properties like the Disgaea series, management is implementing a strategy to develop new titles capable of exceeding 200,000 domestic sales. This recovery plan is supported by a new organizational structure led by President Kenzo Saruhashi, who assumed his role in January 2025. From a governance and financial perspective, the company maintains a stable asset base of ¥111.5 billion, including ¥5.19 billion in cash and equivalents, despite a decrease in retained earnings. The group is prioritizing internal reserves for talent acquisition and game development while maintaining a year-end dividend of 5 yen per share. Independent auditors confirmed the effectiveness of internal controls and the fairness of financial reporting, specifically noting the valuation of work-in-progress as a key audit matter. Moving forward, the company aims to balance fiscal recovery with long-term growth initiatives, including a commitment to management diversity and the strengthening of its global development and sales capabilities.

Nippon Ichi SoftwareJun 2025