FinancialNippon Ichi Software

Nippon Ichi Software Q1 FY2026 Financial Results (Japanese GAAP)

12 Aug 202516 pages~5 min full read

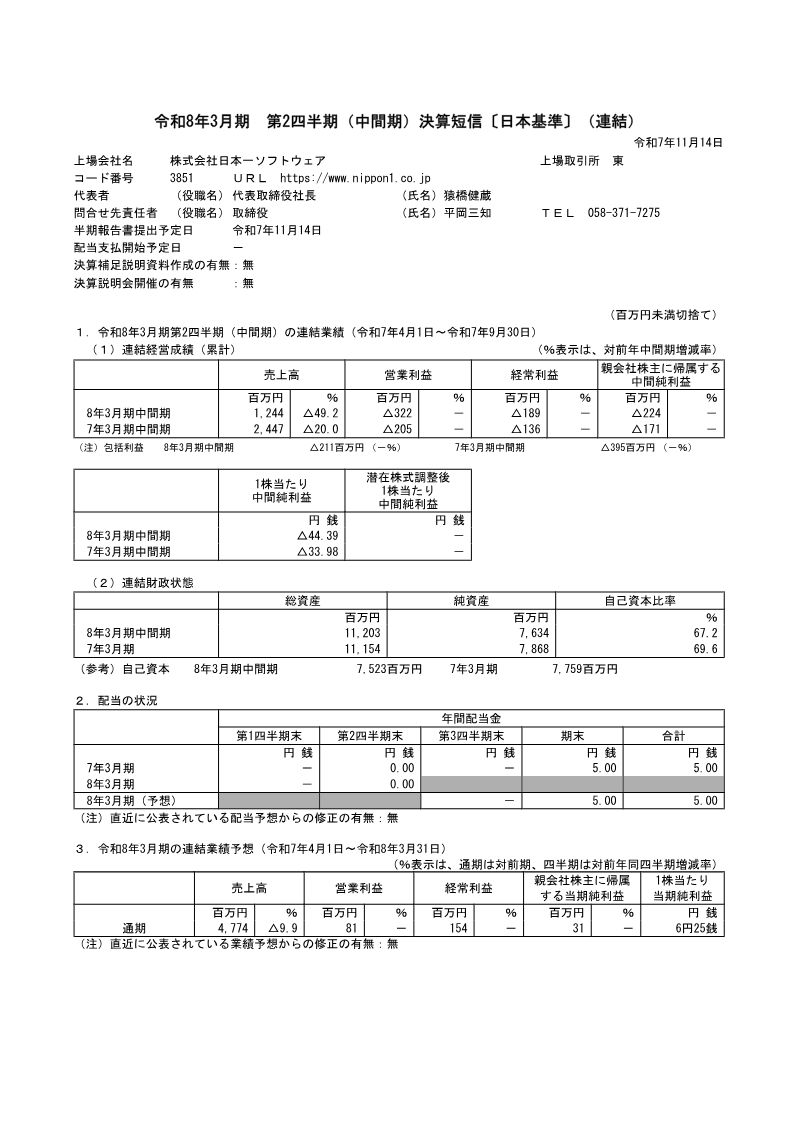

Nippon Ichi Software reported a 52.5% year-over-year decline in Q1 net sales to 480 million yen, resulting in a net loss of 169 million yen for the period ending June 30, 2025.

The core entertainment segment experienced a 54.4% revenue drop to 450 million yen, which management attributed to the timing of major title releases like Fuuraiki 5 and Renju shifting to the second quarter.

Despite the Q1 operating loss of 174 million yen, the company maintained its full-year forecast of 4.77 billion yen in sales and 81 million yen in operating income.

The company’s financial position remains stable with an equity ratio of 68.6% and total assets of 10.8 billion yen, supported by a cash and deposit balance of 5.5 billion yen.

The student dormitory business segment grew revenue by 25.4%, though it remains a minor contributor to the company's overall financial portfolio.

Strategic focus continues to center on multi-platform digital distribution via Steam, PlayStation Network, and the Nintendo eShop, alongside ongoing international localization efforts.

Nippon Ichi Software’s financial results for the first quarter of the fiscal year ending March 31, 2026, reveal a challenging period characterized by significant year-over-year declines in revenue and continued operating losses. Covering the period from April 1, 2025, to June 30, 2025, the data shows consolidated net sales fell 52.5% to 480 million yen. While the operating loss of 174 million yen represented a slight improvement over the 256 million yen loss in the previous year's first quarter, the ordinary loss widened to 135 million yen, and the net loss attributable to owners of the parent increased to 169 million yen.

The entertainment segment, which constitutes the core of the business, saw sales drop 54.4% to 450 million yen. Management attributes this performance to the timing of product cycles, noting that major titles like Fuuraiki 5 and Renju were still in development during the quarter with releases scheduled for the second quarter. Despite the downturn in domestic package software sales, the company maintained its focus on multi-platform digital distribution via PlayStation Network, Nintendo eShop, and Steam, alongside international localization efforts in North America, Europe, and Asia. The smaller student dormitory business saw a 25.4% increase in revenue but remained a minor component of the overall corporate portfolio.

The financial position remains stable with total assets of 10.8 billion yen and an equity ratio of 68.6%. Cash and deposits increased to 5.5 billion yen, though net assets decreased by 337 million yen due to the quarterly loss and foreign currency translation adjustments. Despite the weak start to the fiscal year, the company maintained its full-year forecast of 4.77 billion yen in sales and 81 million yen in operating income, suggesting an expectation of recovery driven by upcoming software releases. The results have undergone a formal interim review by independent auditors, confirming the accuracy of the financial statements under Japanese accounting standards.