Back to Library

Report

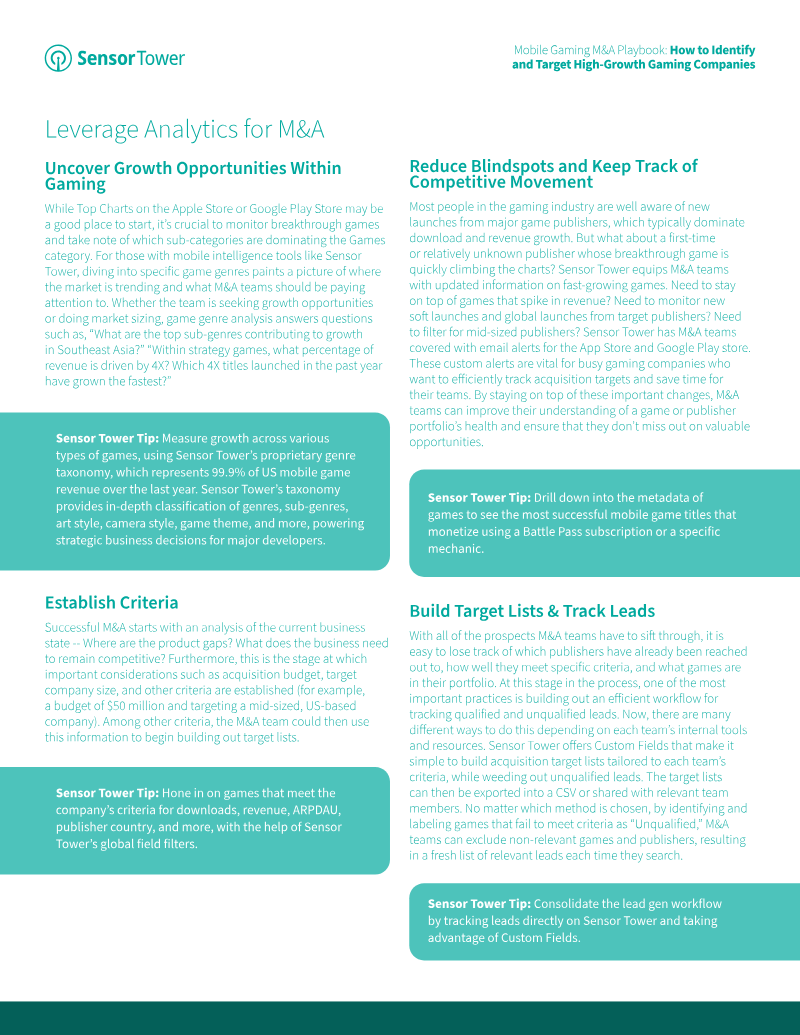

Mobile Gaming M&A Playbook: How to Identify and Target High-Growth Gaming Companies

By Sensor Tower

1 January 20225 pages2,208 words

Summary

The mobile gaming industry is experiencing a period of rapid consolidation, driven by a market projected to reach $138 billion in player revenue by 2025. This strategic guide outlines how major publishers and investors utilize mergers and acquisitions to mitigate competitive threats, diversify portfolios, and capture new audience segments. By examining high-profile deals—such as Electronic Arts’ $2.1 billion acquisition of Glu Mobile and Zynga’s expansion into hyper-casual and golf genres—the analysis demonstrates that M&A has become a primary vehicle for growth in an increasingly crowded global market. The primary thesis posits that successful M&A requires a data-driven approach to identify synergies and growth opportunities. Key objectives for acquirers include buying out competition, acquiring specialized talent, and gaining scale in specific sub-genres like sports or merge games. For example, the acquisition of Ludia by Jam City illustrates how smaller developers gain access to global resources and corporate expertise, while larger entities bolster their reputations as preferred partners for major intellectual property brands. Methodologically, the findings rely on Sensor Tower’s proprietary store intelligence and genre taxonomy, which covers 99.9% of U.S. mobile gaming revenue. The scope is global, focusing on market activity from 2020 through late 2021, a period that saw over 280 deals valued at $39 billion in the first quarter of 2021 alone. The guide concludes that navigating this landscape requires rigorous evaluation of target health, including revenue trends, ARPDAU, and geographic presence, to ensure acquisitions are well-timed and strategically aligned with broader industry shifts.

Tags

Part of Collections

Pages

View all

Citation

Citation

Generating citation...