Related Documents

Financial

FY2026 2Q Financial Results Briefing Material

Bushiroad Inc. achieved a steady financial performance through the second quarter of fiscal year 2026, reporting net sales of 14,072 million yen for the period and cumulative first-half sales of 27,839 million yen. This 4.6% year-over-year increase reflects a resilient business model that balances traditional entertainment segments with expanding global reach. While the core Trading Card Game segment experienced a minor dip due to a lighter release schedule, the successful launch of the hololive OFFICIAL CARD GAME and a rising overseas sales ratio of 43.5% provided a stable foundation. Growth was further bolstered by high attendance in the Sports segment, particularly for New Japan Pro-Wrestling and STARDOM, alongside a significant foreign exchange gain. The company has already reached 64.6% of its full-year operating profit forecast, supported by the expansion of the PalVerse figure brand and consistent console game releases. Strategic focus remains on the worldwide mobile launch of HUNTER×HUNTER NEN×SURVIVOR in early 2026 and major product updates for flagship titles like Weiβ Schwarz and Cardfight!! Vanguard. Although the third quarter is expected to be a transitional period characterized by higher marketing expenditures and product specification updates, the full-year consolidated forecast remains unchanged. Long-term growth initiatives are centered on international IP utilization and capital efficiency. A strategic alliance with GENDA Inc. aims to accelerate global expansion, while the planned cancellation of 6,000,000 treasury shares in late 2025 underscores a commitment to enhancing shareholder returns. By integrating live events, digital gaming, and physical merchandise across domestic and international markets, the organization is positioning itself to navigate short-term transitional costs while securing a broader global footprint.

BushiroadJan 2026

Financial

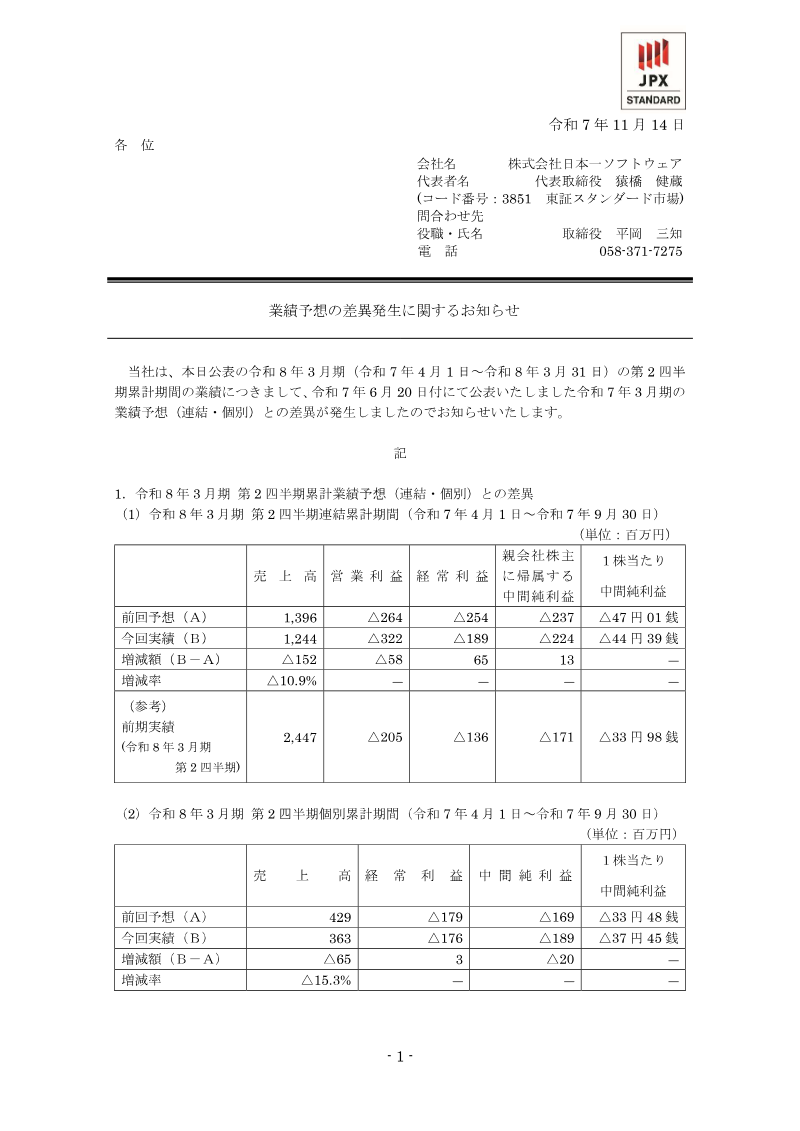

Notice Regarding Differences in Earnings Forecasts

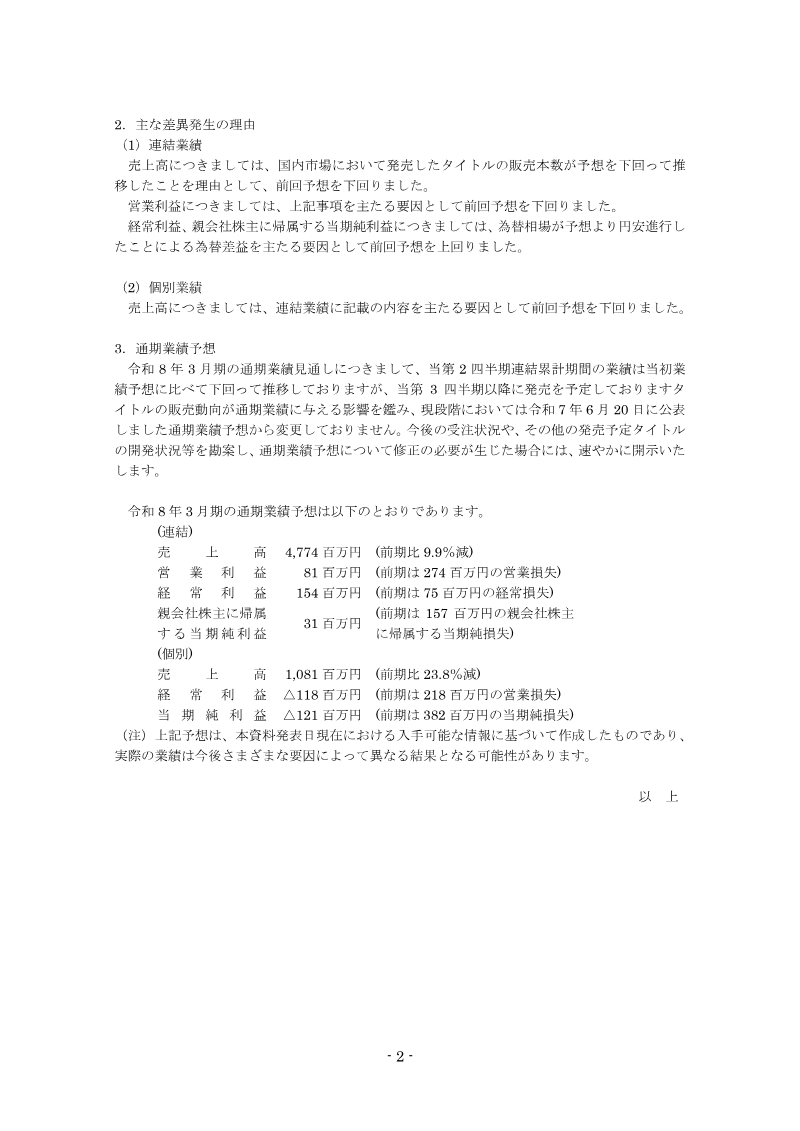

The notice serves to inform shareholders of a variance between the company’s actual second‑quarter performance for the fiscal year ending March 2026 and the forecast issued on 20 June 2025. For the consolidated period April 1 to 30 September 2025, net sales reached ¥1,244 million, 10.9 % below the prior estimate of ¥1,396 million, while operating profit fell to a loss of ¥322 million versus the projected ¥264 million loss. Net profit attributable to the parent’s shareholders declined to ¥44 million per share from the forecasted ¥47 million. On a standalone basis, sales were ¥363 million, 15.3 % lower than the ¥429 million expected, and net profit per share slipped to ¥45 million from ¥48 million. The primary driver of the shortfall was weaker domestic demand for newly released titles, which reduced unit sales below expectations. Conversely, a stronger yen depreciation generated foreign‑exchange gains that lifted both ordinary profit and net profit relative to the forecast. Despite the quarterly miss, the company retains its full‑year outlook unchanged. The revised full‑year consolidated forecast anticipates sales of ¥4,774 million, a 9.9 % decline year‑on‑year, with operating profit turning positive to ¥81 million after a prior loss, ordinary profit of ¥154 million, and net profit attributable to shareholders of ¥31 million. On a standalone basis, full‑year sales are projected at ¥1,081 million, down 23.8 % YoY, with ordinary loss of ¥118 million and net loss of ¥121 million. The company commits to updating the outlook promptly should subsequent developments warrant revision.

Nippon Ichi SoftwareNov 2025

Financial

FY2026 1Q Financial Results Briefing Material

Bushiroad’s financial performance for the first quarter of fiscal year 2026 reflects a period of significant expansion and profitability, characterized by a 12.2% increase in net sales to 13,766 million yen and a 227% surge in operating profit. This growth was primarily catalyzed by the trading card game segment, which benefited from the successful launches of the Godzilla and hololive official card games. Strategic shifts, including the transition to a single reporting segment and reduced research and development costs within the digital games unit, further bolstered the operating profit margin to 12.1%. The geographic scope of operations has shifted increasingly toward international markets, with overseas sales reaching a record 44.5% of total revenue. This global momentum is supported by the strong performance of established titles like Weiß Schwarz and the release of Hunter × Hunter NEN×IMPACT. While merchandise sales saw a slight year-on-year decline due to high prior-year comparisons, the live entertainment division maintained positive momentum through sold-out events in Shanghai and Japan. The company has already achieved 37.1% of its full-year operating profit target, positioning it well to meet annual forecasts. Future growth is anchored in an integrated "IP Developer" and "One-Stop Media Mix" strategy, which seeks to synchronize anime, digital games, and live events to maximize brand value. Key initiatives include the global expansion of the PalVerse brand, strategic investments in production partners like YUHODO and SANZIGEN, and large-scale events such as Bushiroad EXPO 2026. By leveraging cross-company alliances and high-profile intellectual properties like BanG Dream!, the organization aims to solidify its role as a global platform company capable of scaling both internal and third-party content across the entertainment landscape.

BushiroadNov 2025

Financial

Consolidated Financial Statements for the First Quarter of Fiscal Year Ending March 31, 2026 (Japanese GAAP)

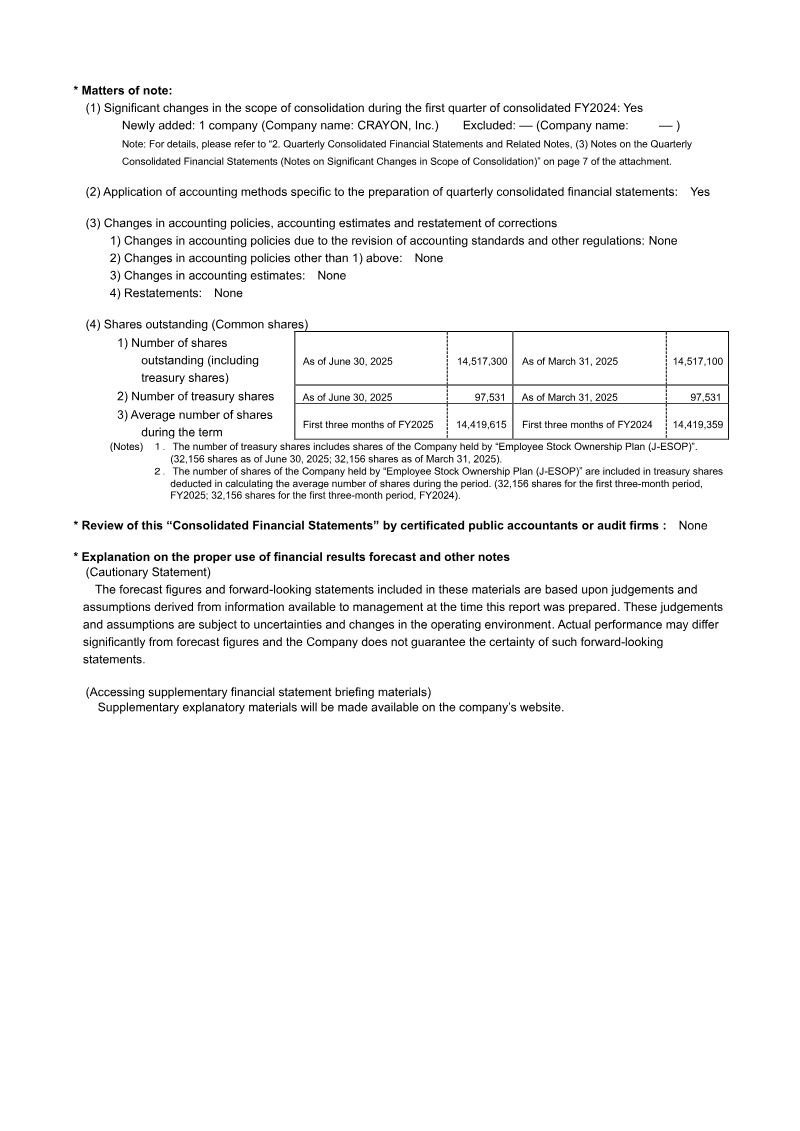

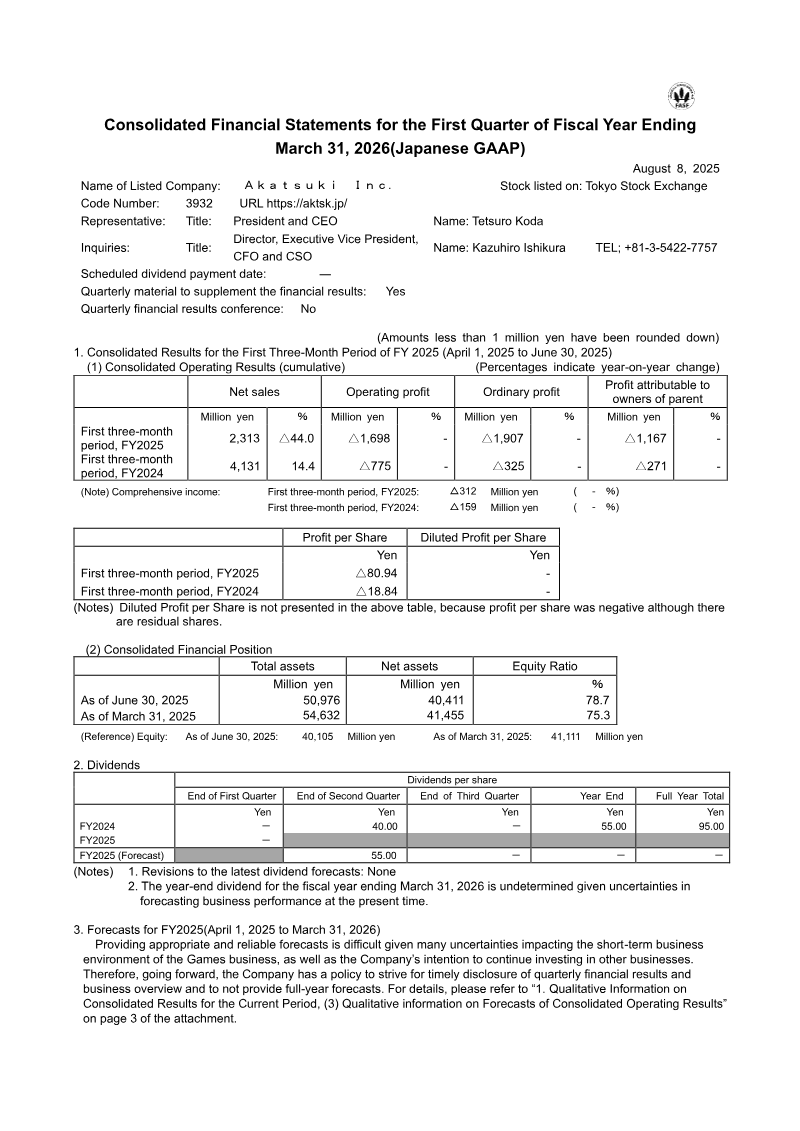

Akatsuki Inc. experienced a significant downturn in financial performance during the first quarter of the fiscal year ending March 31, 2026, characterized by a 44.0% year-on-year decline in net sales to ¥2,313 million. This contraction led to a widened operating loss of ¥1,698 million and a net loss of ¥1,167 million. The primary driver of this decline was the Games business, where revenue plummeted 52.3% to ¥1,782 million. This segment’s performance was impacted by a strategic portfolio review and a transition period for flagship titles such as Dragon Ball Z Dokkan Battle, resulting in a segment loss of ¥1,643 million. Furthermore, the company recorded a ¥103 million extraordinary loss stemming from the discontinuation of a specific game title and subsequent organizational restructuring. Despite these challenges in the core gaming sector, the newly reclassified IP Solutions segment emerged as a growth driver, with revenue increasing 167.2% to ¥298 million and achieving a segment profit of ¥122 million following the consolidation of CRAYON, Inc. Conversely, the Comics business saw an 18.3% revenue decline, though it successfully returned to a modest segment profit of ¥20 million. Total assets decreased by ¥3,656 million during the period, settling at ¥50,976 million, yet the company maintains a robust financial foundation with a high equity ratio of 78.7%. The current strategic trajectory involves a pivot toward large-scale, 3D multi-device projects designed for global markets. This shift aims to stabilize the Games segment by moving beyond traditional mobile constraints while leveraging the momentum found in IP-driven solutions. While the immediate financial results reflect the costs of reorganization and the volatility of existing game lifecycles, the emphasis remains on long-term scalability and the diversification of revenue streams across the broader entertainment landscape.

AkatsukiAug 2025