ReportGames Workshop Group

Half-Yearly Report: 26 Weeks to 26 November 2023

20 pages~51 min full read

Key insights

3 takeaways · ~1 min read- 01

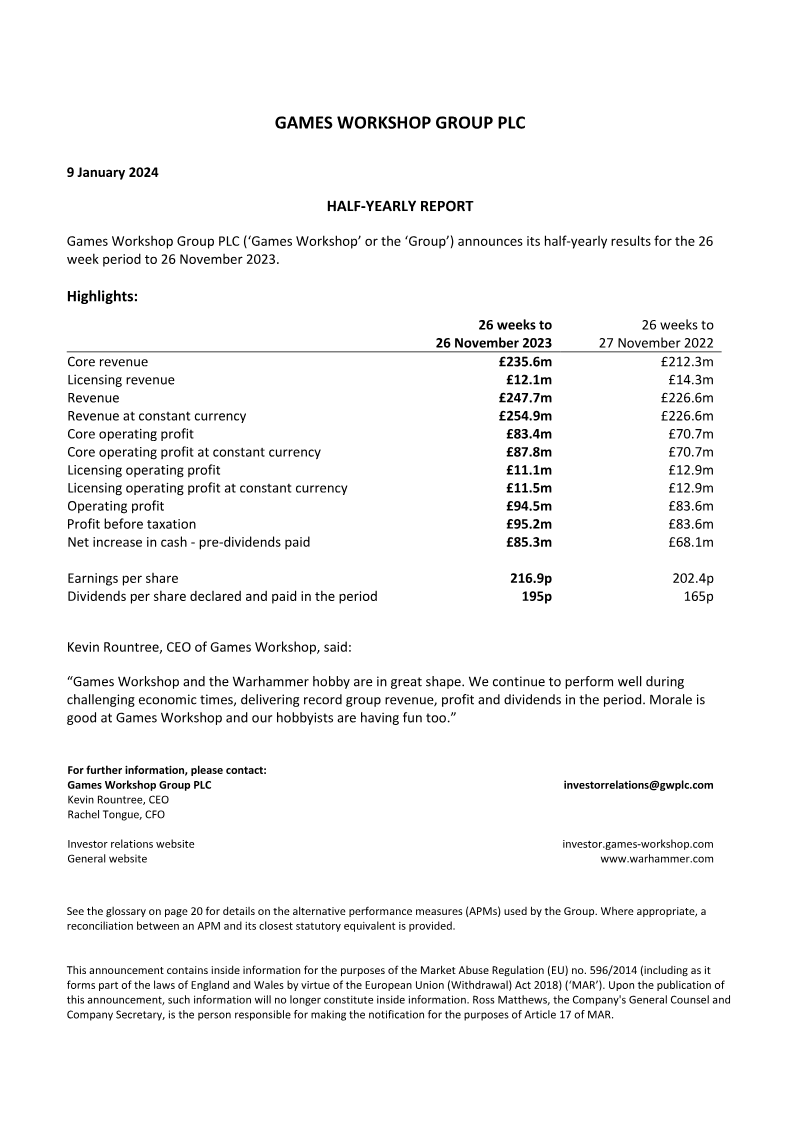

Games Workshop Group PLC reported total revenue growth for the 26-week period ending 26 November 2023 compared to the same period in 2022.

See it on page 1 - 02

Core revenue increased to £235.6 million for the 26 weeks to 26 November 2023, up from £212.3 million during the equivalent period in 2022.

See it on page 2 - 03

Licensing revenue declined to £12.1 million for the 26 weeks ending 26 November 2023, compared to £14.3 million in the prior year's period.

See it on page 5