Related Documents

Financial

3rd Quarter Report: Fiscal Year Ending March 31, 2026

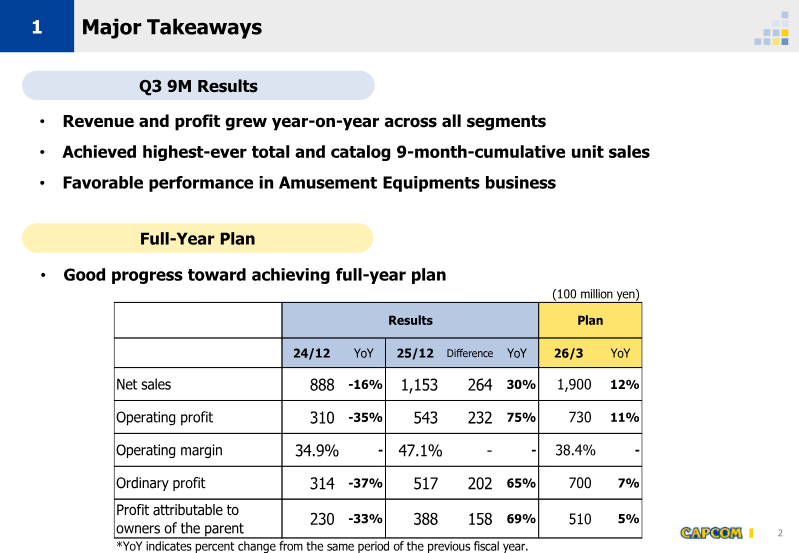

This financial report details Capcom’s consolidated performance for the third quarter of the fiscal year ending March 31, 2026. The findings indicate significant year-on-year growth in both revenue and profit across all business segments, driven primarily by the sustained performance of catalog titles and strong results in the amusement equipment division. Net sales reached 115.3 billion yen, a 30% increase over the previous year, while operating profit rose 75% to 54.3 billion yen. These results place the company on a favorable trajectory to meet its full-year targets of 190 billion yen in net sales and 730 billion yen in operating profit. The Digital Contents segment remains the primary driver of growth, with unit sales reaching a record 9-month high of 34.6 million units. Catalog titles accounted for 96.4% of these sales, underscoring the long-term value of core franchises such as Resident Evil, Monster Hunter, and Street Fighter. Notably, Monster Hunter Wilds surpassed 11 million cumulative units, while Resident Evil 4 and Street Fighter 6 continued to show steady growth. Digital sales now represent 94.1% of total units, with PC platforms alone accounting for over 55% of the volume. Geographically, overseas markets dominate the business, representing nearly 90% of total unit sales. Beyond software, the Arcade Operations and Amusement Equipments segments reported double-digit growth. Arcade sales rose 12% following the opening of new stores and the expansion of specialty formats, while Amusement Equipments saw a 74% surge in net sales due to the strong performance of smart slot titles like Shin Onimusha 3. The company’s strategic outlook remains focused on leveraging its leading brands through upcoming releases such as Resident Evil Requiem and Monster Hunter Stories 3, alongside cross-media expansions including a new Devil May Cry anime and a live-action Street Fighter film.

CapcomFeb 2026

Financial

Q4 2025 Interim Report

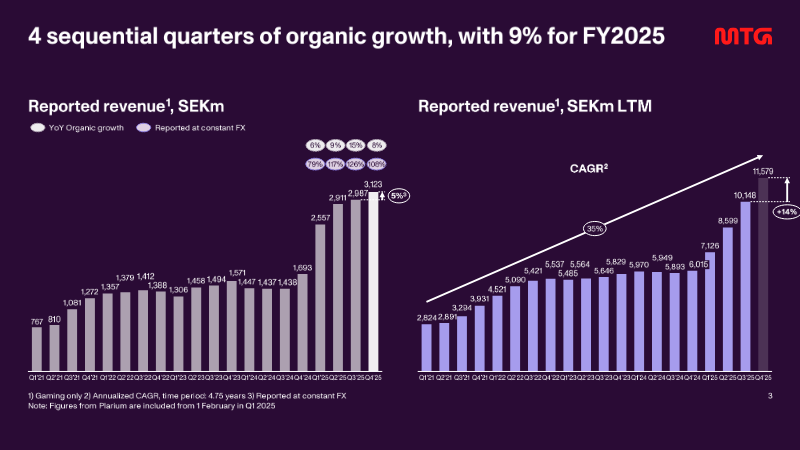

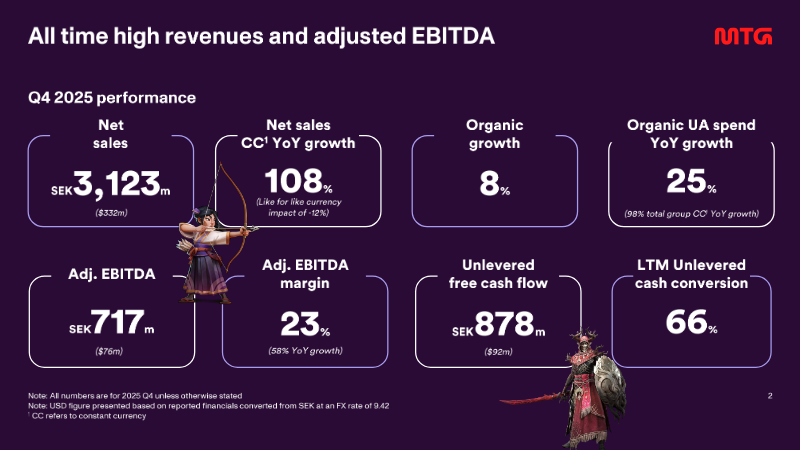

The interim filing presents the fourth‑quarter 2025 financial results for a midcore‑casual gaming group, emphasizing a record‑setting revenue run and the successful execution of a transformation agenda that includes the integration of the Plarium acquisition and the rollout of a new district structure in early 2026. Revenue reached SEK 3,123 million, reflecting 108 % organic growth year‑on‑year and a 25 % increase on a constant‑currency basis, while adjusted EBITDA rose to SEK 717 million, delivering a 23 % margin that matches the full‑year figure. Unlevered free cash flow amounted to SEK 878 million, with a cash‑conversion rate of 66 % and a leverage ratio of five times EBITDA, underscoring robust liquidity and disciplined capital management. User‑acquisition spending accelerated, representing 38 % of quarterly revenue—up from 37 % in the prior quarter—and grew 76 % on a reported basis, driven by heightened investment in original studios, new casual titles, and the racing franchise. The direct‑to‑consumer channel expanded by 600 basis points to 32 % of total revenue, reflecting a strategic shift toward higher‑margin in‑app purchases. Across the fiscal year, the company posted a 9 % organic revenue increase, with word‑games, racing, and RAID franchises delivering the strongest quarter‑end performance. Operating cash flow for the quarter stood at SEK 840 million, while adjusted net income was SEK 1,390 million, translating to an adjusted EPS of SEK 11.33. The financial outcomes exceed guidance and position the firm to meet its medium‑term outlook, with a pre‑IPO study for PlaySimple concluded and the midcore transformation progressing as planned.

Modern Times GroupFeb 2026

Financial

Q3 2025 Investor Presentation

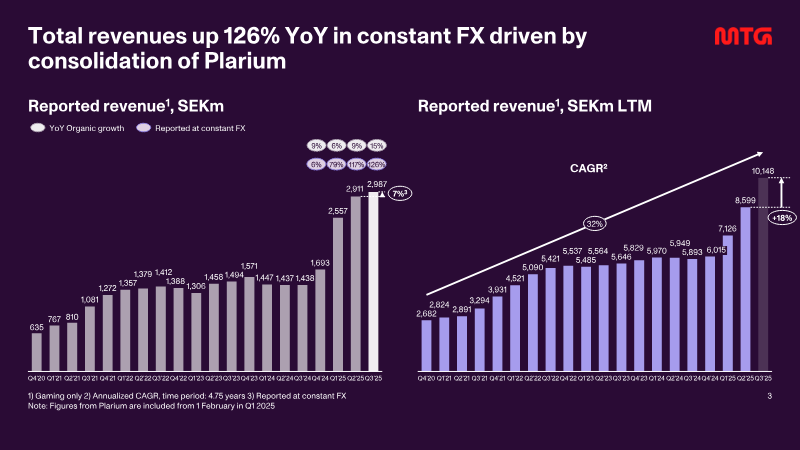

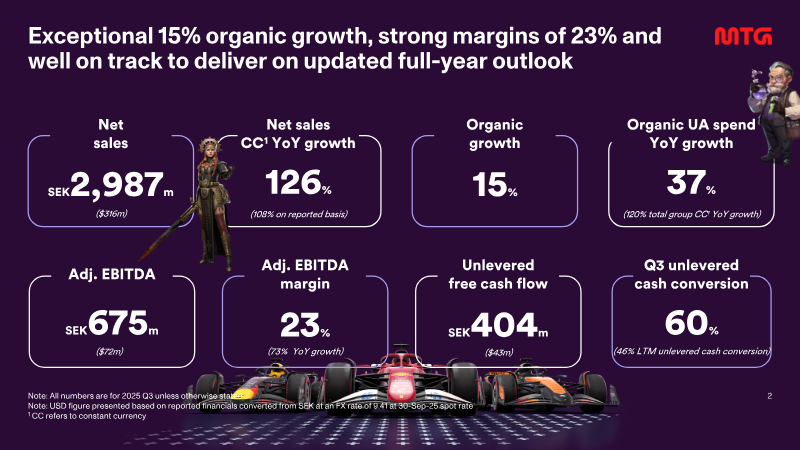

The presentation delivers a quarterly performance update and revised full‑year outlook for a mid‑core and casual gaming group, emphasizing the impact of organic growth and the recent integration of Plarium. In Q3 2025 the company recorded SEK 2.987 billion in net sales, a 15 % year‑over‑year organic increase and a 126 % rise in constant‑currency revenue driven largely by the Plarium consolidation. Adjusted EBITDA reached SEK 675 million, translating to a 23 % margin, while unlevered EBITDA margin stood at 60 % and free cash flow amounted to SEK 404 million, supporting a 60 % cash‑conversion rate. User‑acquisition spend rose sharply, with original studios increasing spend by 37 % and total group spend climbing 120 % on a constant‑currency basis, now representing roughly 37 % of revenue. Core metrics such as ARPDAU improved quarter‑over‑quarter, notably on the Snowprint title, while daily active users remained broadly flat after accounting for the Kongregate divestment and Plarium acquisition. The franchise portfolio showed double‑digit growth in PlaySimple, Warhammer 40,000: Tacticus, and a strong performance from RAID: Shadows Legends anchored by the Teenage Mutant Ninja Turtles IP. Based on these results the company raised its FY 2025 guidance, targeting 7‑9 % organic revenue growth and total revenue of SEK 11.4‑11.7 billion, with an adjusted EBITDA margin of 21‑24 %. The outlook underscores confidence in continued scaling of live‑ops, new‑title launches and disciplined investment in user acquisition.

Modern Times GroupNov 2025

Financial

CD Projekt Group FY 2024 Earnings

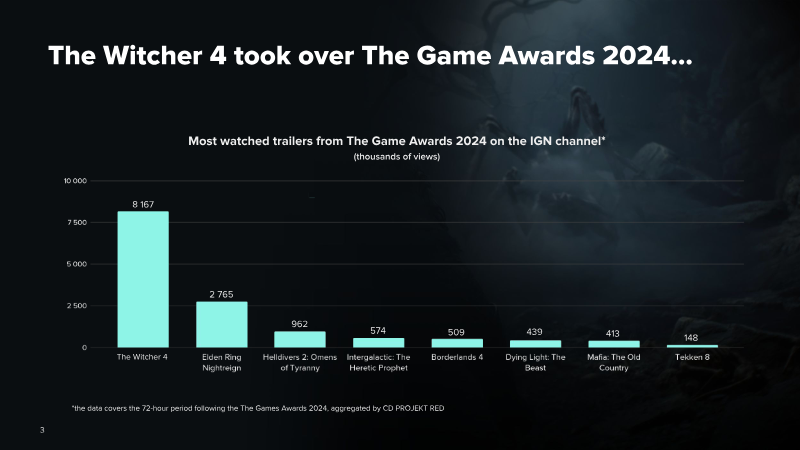

CD Projekt Group presents its FY 2024 earnings, outlining financial performance, operational milestones and a long‑term growth outlook for the studio and its portfolio. The report emphasizes the commercial impact of The Witcher 4, which captured 53 % of press coverage in the 72 hours after The Game Awards 2024, generating 2 150 articles and becoming the most discussed title among peers such as Elden Ring and Final Fantasy. Development capacity expanded to 411 staff, with 650 developers allocated across The Witcher 4, Orion, Sirius, Hadar, the Witcher Remake and several unannounced projects. Revenue for the year fell 20 % year‑on‑year to PLN 1.23 billion, while cost of sales decreased to PLN 377.9 million, delivering a gross profit of PLN 852.2 million and EBIT of PLN 469.0 million. Net profit reached PLN 481.1 million, reflecting a net‑profit margin of roughly 39 % in 2023 and an expected rise to 47.7 % in 2024, with a target of 58.5 % by

CD ProjektMar 2025