Related Documents

Report

Africa Games Industry Report

The African video games industry represents a rapidly expanding mobile-first frontier, characterized by a player population that surged from 77 million in 2015 to 186 million in 2021. With annual revenues projected to surpass $1 billion by 2024, the continent is positioning itself to replicate the success of other emerging markets like Brazil and India. Growth is currently concentrated in regional hubs across South Africa, Nigeria, Ghana, and Kenya, where a young demographic is increasingly integrating local cultural themes into digital entertainment. This evolution is supported by a complex value chain where mobile gaming accounts for the vast majority of engagement, mirroring global trends where mobile platforms generate over $92 billion in annual revenue. Despite this potential, the ecosystem remains in a nascent stage, with 63% of studios operating for five years or less and 59% of developers never having secured external investment. While high-profile deals such as Carry1st’s $27 million funding round and GBarena’s $15 million acquisition of Galactech signal growing investor confidence, the broader market is still dominated by hobbyists. Only 36% of developers currently earn a living from their work, and over half of those rely exclusively on domestic revenue. Technical development is heavily centralized around the Unity engine, which is utilized by 64% of the market, reflecting the industry's focus on accessible mobile content. Significant structural barriers continue to impede the transition from a hobbyist community to a professionalized global competitor. Infrastructure deficits are the primary concern, with 60% of industry participants citing poor power supply and high internet costs as critical obstacles. Furthermore, government support is nearly non-existent, currently reaching only 3% of the sector. To achieve sustainable maturity, the industry requires a coordinated effort to stabilize infrastructure, formalize talent pipelines, and attract informed investors who understand the unique dynamics of the African market. Addressing these catalysts is essential for transforming local creative potential into a robust, revenue-generating economic sector.

Games Industry AfricaMar 2024

Report

State of African Games 2026

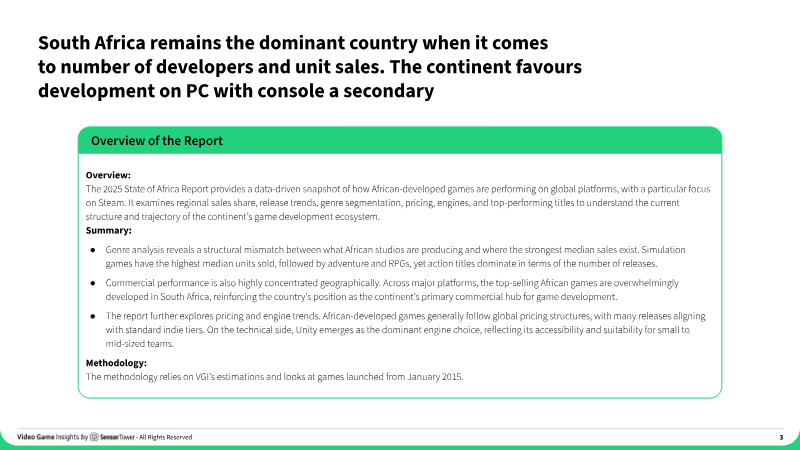

The analysis delivers a data‑driven overview of African‑developed video games, concentrating on performance across global platforms—primarily Steam, with supplemental PlayStation and Xbox data—from 2015 through 2025. Its central thesis is that the continent’s game‑development ecosystem is emerging rapidly yet remains highly concentrated, especially in South Africa, and is transitioning from volume‑driven growth to a focus on higher‑quality, strategically positioned titles. South Africa accounts for the overwhelming share of both developers and commercial success, supplying all titles in the top‑ten sales list and driving the continent’s 2 % share of Steam unit sales—higher than the Middle East and comparable to Oceania. Releases peaked in 2023 with 23 Steam titles before falling to 11 in 2025, suggesting a shift toward longer development cycles. Genre analysis reveals a mismatch: simulation games achieve the highest median sales (≈372 k units), followed by adventure and RPGs, while action titles dominate the release count. Pricing follows global indie norms, with most games priced between $5.99 and $19.99; premium pricing above $21.99 appears in only a small fraction of titles. Unity is the leading engine (≈18 % of releases), Unreal accounts for about 7 %, and the remaining 73 % use a diverse set of smaller tools, reflecting a decentralized technical landscape. Methodologically, the study relies on Video Game Insights estimations for games launched after 1 January 2015, employing internal sales‑estimation algorithms that convert review counts and apply the Boxleiter method to infer unit sales and revenue. The scope encompasses all major platforms, covers the entire African continent, and isolates trends in genre, pricing, engine choice, and geographic distribution. Conclusions point to a transitional phase where success will depend less on release volume and more on distinctive cultural content, genre diversification, and broader support structures beyond South Africa. If these dynamics persist, the African game‑development sector is poised to evolve from an emerging participant to a recognized creative force within the global industry.

Sensor TowerJan 2026

Report

Games Industry in 2025

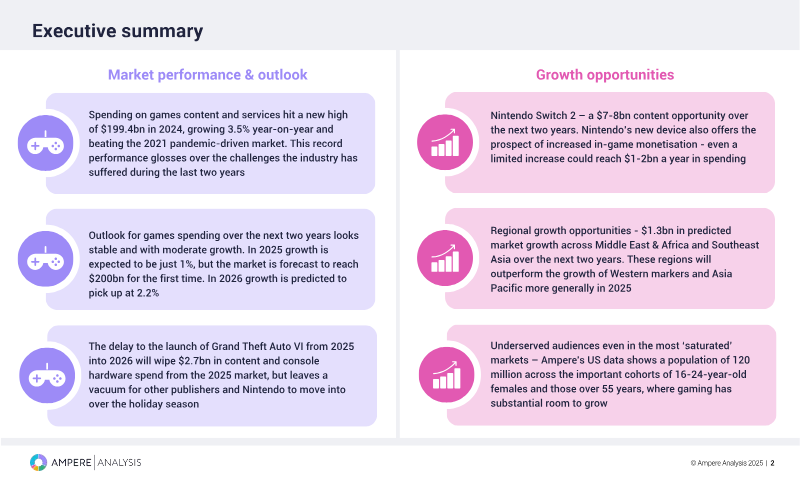

The global games content and services market reached a record $199.4 billion in 2024, a 3.5% year-on-year increase that surpassed pandemic-era peaks. Despite this financial milestone, the industry faces significant structural challenges, including widespread layoffs, studio closures, and a shift toward de-risking strategies. Growth is expected to slow to 0.9% in 2025, largely due to the delay of Grand Theft Auto VI into 2026, which is projected to remove $2.7 billion from the 2025 console market. However, the industry is forecast to surpass the $200 billion threshold for the first time in 2025, with growth accelerating to 2.2% in 2026. Key growth opportunities center on new hardware and emerging markets. The anticipated launch of the Nintendo Switch 2 in 2025 represents a $7-8 billion content opportunity, with significant potential for increased in-game monetization. Geographically, the Middle East, Africa, and Southeast Asia are expected to outperform Western markets, with the Middle East and Africa projected to grow by 6.3% in 2025. Additionally, significant headroom exists in mature markets like the U.S. by targeting underserved cohorts, specifically females aged 16-24 and adults over 55. The industry is navigating a transition in monetization and platform dynamics. In-game spending accounts for 77% of total revenue, while physical media is expected to dwindle to just 2% of the market by 2026. To combat escalating AAA development costs, publishers are increasingly utilizing remakes, remasters, and transmedia franchise strategies. While mobile gaming remains the largest segment at 58% market share, PC gaming showed the strongest growth in 2024 at 5.7%. The analysis utilizes proprietary market modeling, financial KPIs, and quantitative consumer research across global regions to provide a comprehensive outlook through 2026.

Ampere AnalysisJan 2025

Report

Gaming 2025 (Epyllion)

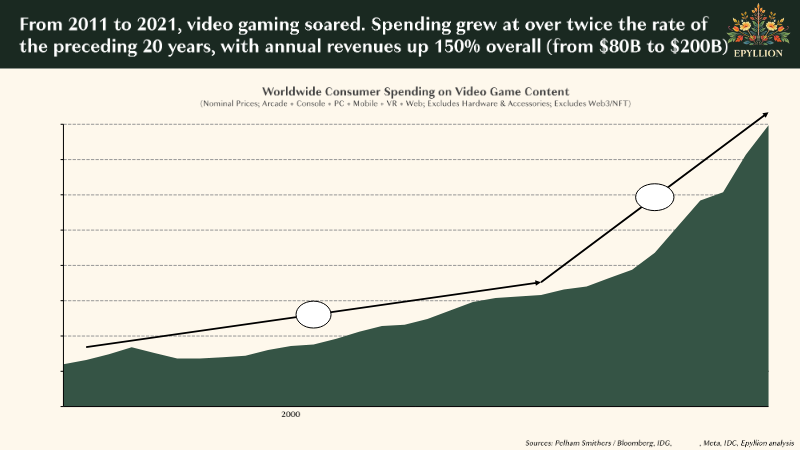

The global video game industry has transitioned from a decade of rapid expansion into a period of contraction and market maturation. Following the 2011–2021 growth wave, the sector now faces a "zero-sum" environment characterized by stagnant player spending, plummeting stock values, and a collapse in venture capital. This downturn has triggered an unprecedented wave of studio closures and mass layoffs as publishers move away from risky new ventures to focus on aggressive multiplatform strategies for established franchises. While the industry maintains a higher net headcount than in 2022, the current climate is defined by an oversupply of content competing for limited consumer hours, with the top ten titles capturing 60% of all sales. Market dominance is increasingly concentrated in "Black Hole" titles and User-Generated Content (UGC) platforms like Roblox and Fortnite. These ecosystems leverage deep social integration and digital entitlements to create a "lock-in" effect that makes it difficult for new live-service titles to gain traction. While the PC ecosystem is gaining momentum over traditional consoles due to its larger libraries and native social tools like Discord, the handheld market is poised for a shift with the impending launch of the "Switch 2" and Valve’s expansion of SteamOS. Furthermore, the rise of high-quality AAA titles from China and localized media in emerging markets is successfully challenging Western dominance by prioritizing domestic cultural themes and lower hardware specifications. Future growth is expected to be driven by technological innovation and regulatory shifts rather than traditional software sales. Generative AI is being deployed to create autonomous virtual agents and lower development costs, while major publishers are aggressively pursuing programmatic in-game advertising to offset decades of price deflation. Simultaneously, the deregulation of mobile app stores is expected to improve developer margins by 10–20%, enabling new cloud-native experiences and third-party storefronts. By 2030, nearly one billion mobile devices will be capable of running high-fidelity console-spec games, positioning emerging regional markets as the primary engine for the industry’s next economic cycle.

EpyllionJan 2025