The 2026 US venture capital outlook projects a cautiously optimistic landscape, driven largely by an explosive surge in early‑stage activity and the continued dominance of artificial intelligence (AI) startups. AI firms now command 65 % of venture capital, fueling near‑record first‑financing counts and setting a high bar for late‑stage valuations. While liquidity remains the primary constraint—exit values are projected below $300 billion and limited LP enthusiasm persists—the emergence of improved secondary markets and a potential rebound in initial public offerings are expected to alleviate pressure. Multistage firms that focus on seed rounds are poised to sustain growth across both early and later stages, yet emerging managers may face fundraising challenges that could curtail diversification.

A widening gap between AI‑focused, high‑growth startups and their slower‑moving peers is evident. In Q3 2025 the United States hosted 830 active unicorns with a record $3.9 trillion post‑money valuation, yet many of these firms are liquidity‑constrained and struggle to secure follow‑on funding. AI companies dominate late‑stage deals, with median Series C and D+ valuations reaching $838 million; AI rounds exceed non‑AI deals by roughly 26 % at Series D+, underscoring investor confidence in the AI boom while highlighting potential risks if public AI valuations contract.

Fundraising is projected to rebound to $100‑$130 billion in 2026, largely driven by recycled distributions that are expected to account for roughly 70 % of new commitments. Strong exit activity through 2025 and renewed interest in AI‑focused funds—such as a $10 billion Andreessen Horowitz vehicle—underpin this outlook. However, risks remain: a potential liquidity reversal or recession‑induced sentiment decline could keep commitments below $100 billion, tempering the projected recovery.

PitchBook · 2024

PitchBook · 2024

PitchBook · 2024

PitchBook · 2024

PitchBook · 2023

PitchBook · 2023

PitchBook · 2023

PitchBook · 2023

PitchBook

UnitedHealth Group

InvestGame · 2026

Boston Consulting Group · 2026

COLOPL · 2026

Aream & Co · 2026

Bushiroad · 2026

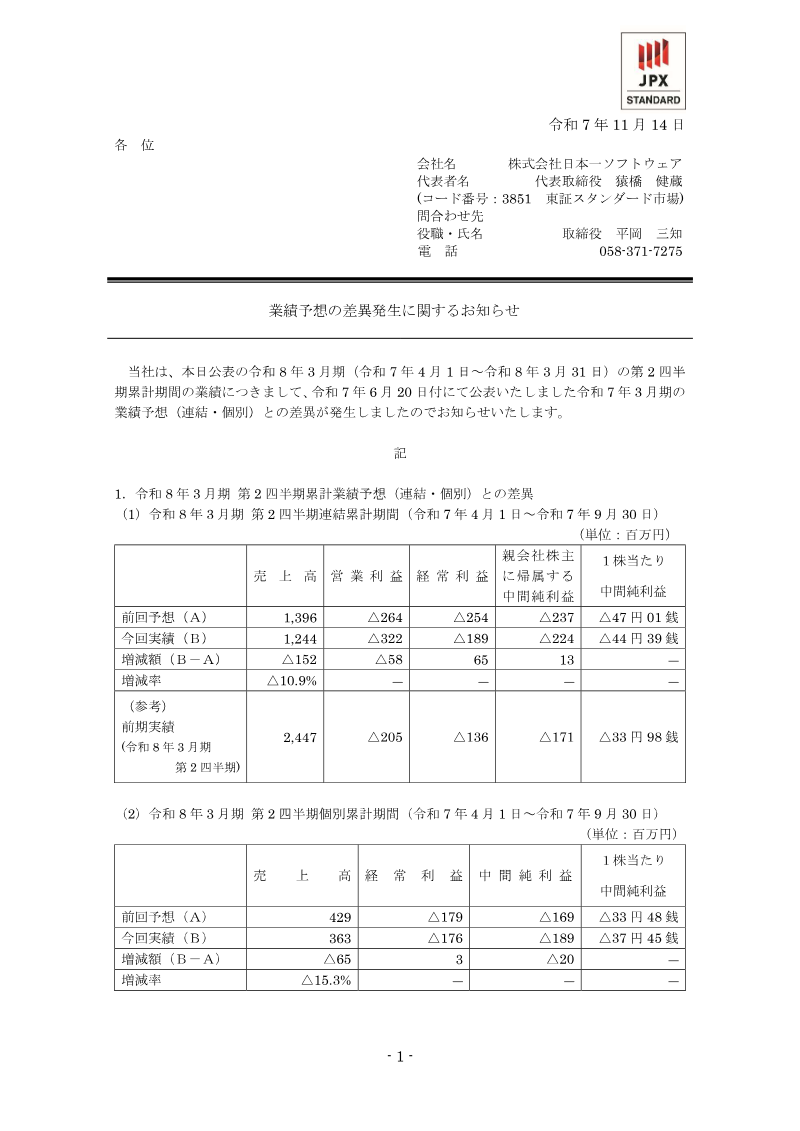

Nippon Ichi Software · 2025

Nippon Ichi Software · 2025

Take-Two Interactive · 2025

Bushiroad · 2025

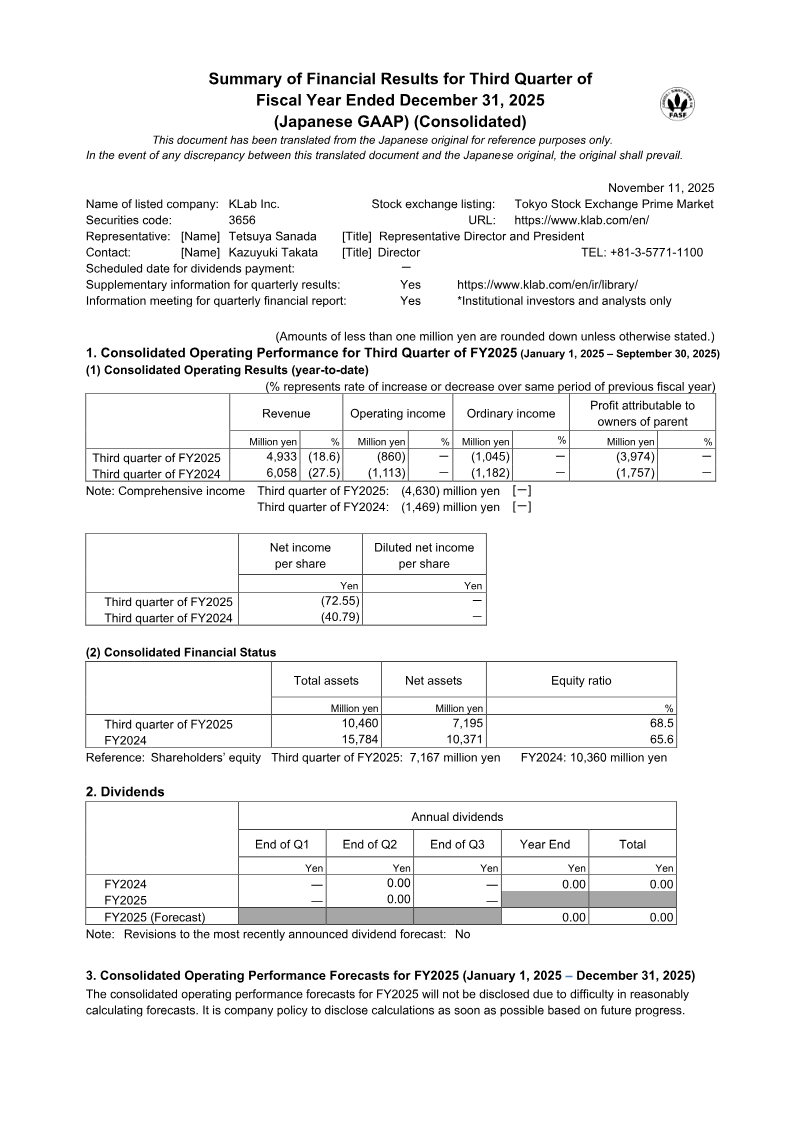

KLab · 2025

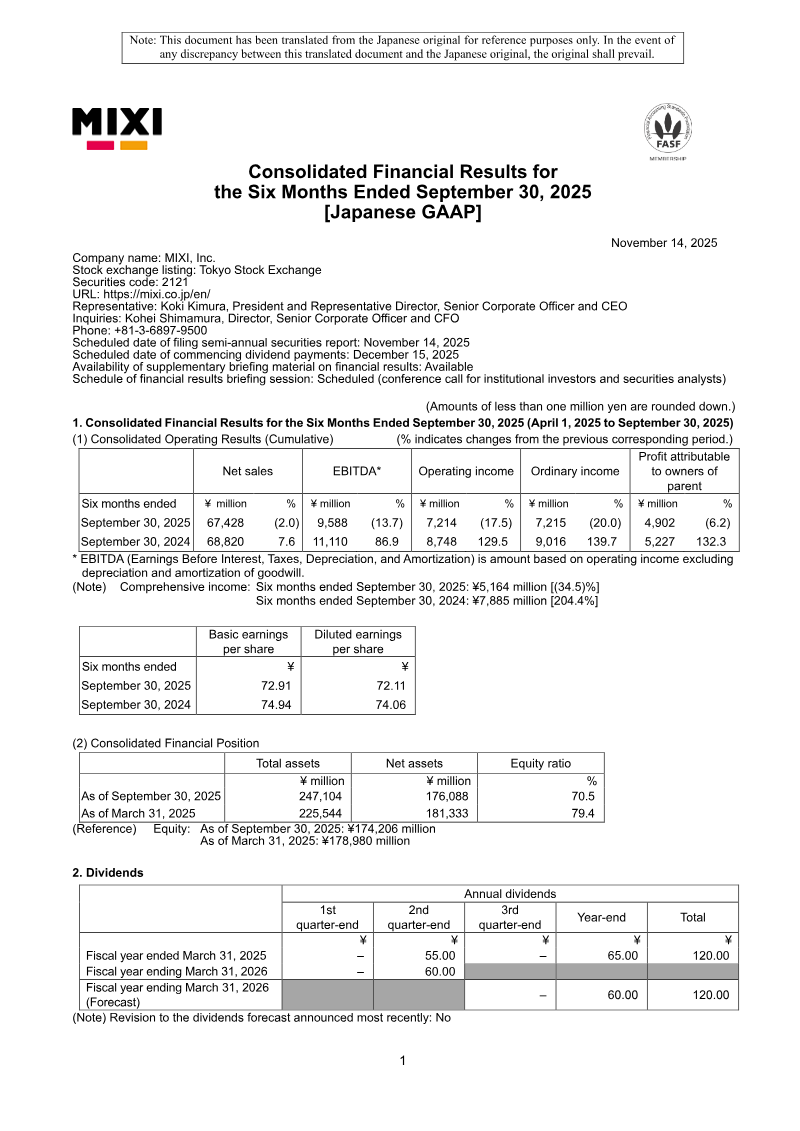

MIXI, Inc. · 2025