Related Documents

Financial

FY2025 Consolidated Financial Results [Japanese GAAP]

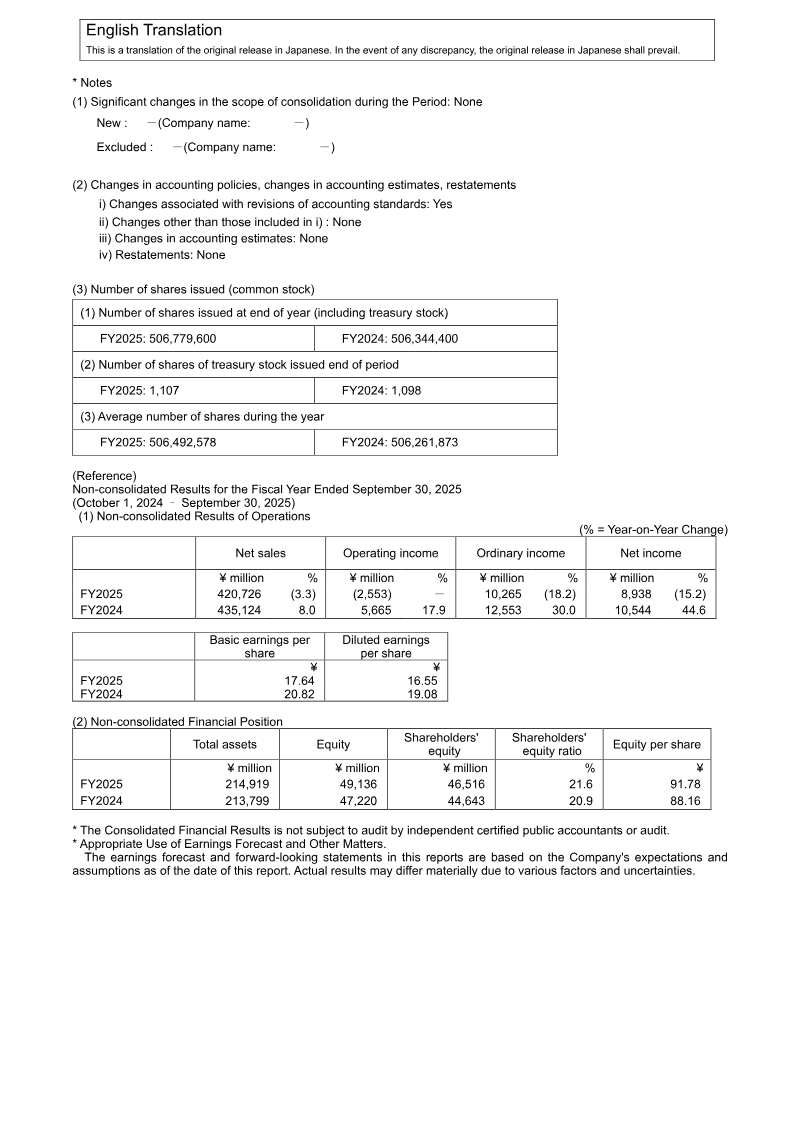

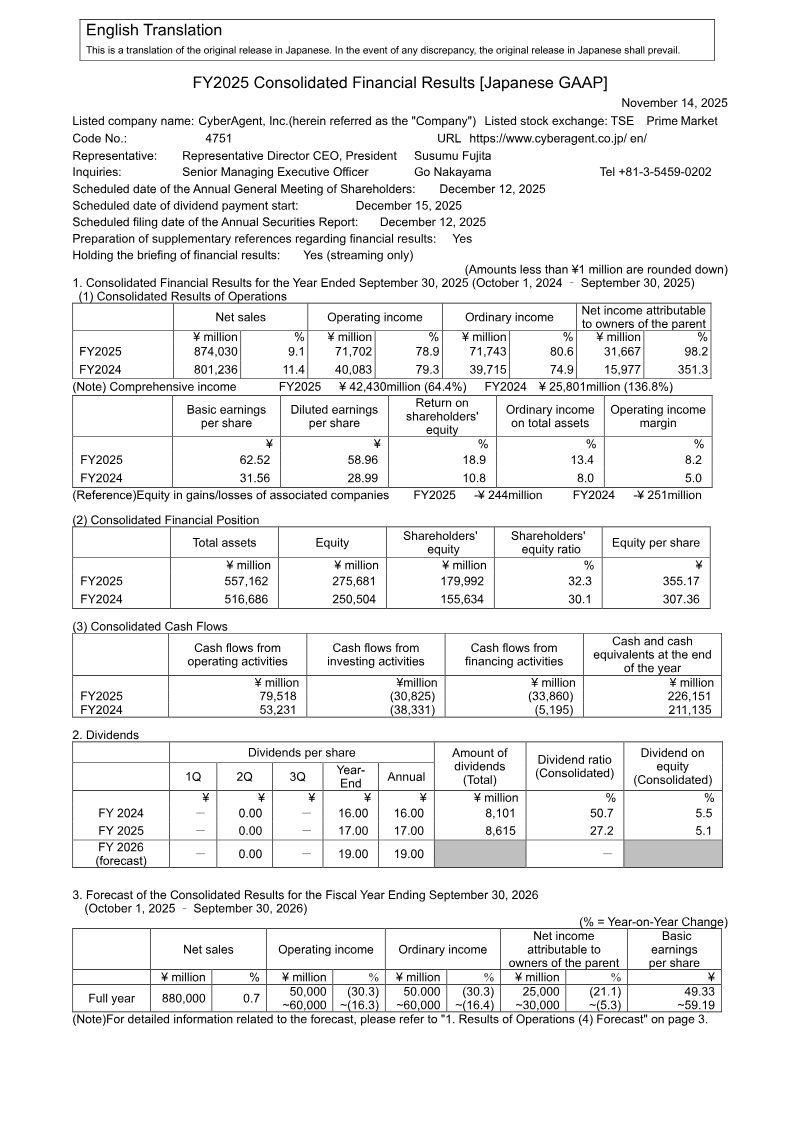

CyberAgent achieved a significant financial recovery during the 2025 fiscal year, characterized by a 9.1% increase in net sales to ¥874,030 million and a 78.9% surge in operating income to ¥71,702 million. This performance was underpinned by the Media & IP segment returning to profitability for the first time in a decade, generating ¥7.29 billion in operating income. The Game Business served as the primary engine for growth, with its operating income nearly doubling to ¥60.06 billion. This success in the gaming sector was attributed to aggressive overseas expansion and the adoption of high-margin external payment methods, which more than offset a ¥727 million extraordinary loss related to a patent infringement settlement between subsidiary Cygames and Konami Digital Entertainment. The company’s financial position strengthened considerably over the period, with net income attributable to the parent doubling to ¥31.67 billion and cash flows from operating activities rising to ¥79,518 million. Strategic capital management included a ¥20,000 million redemption of convertible bonds and the acquisition of subsidiary shares. To better leverage synergies surrounding the ABEMA platform, the corporate structure was reorganized to integrate secondary operations into the newly designated Media & IP Business segment. Looking toward the 2026 fiscal year, the outlook remains cautious despite the recent momentum. While consolidated net sales are projected to grow modestly to ¥880,000 million, operating income is expected to contract to a range between ¥50,000 and ¥60,000 million. This forecast suggests a period of reinvestment or market stabilization following the exceptional gains realized in the gaming and media sectors during the previous year. The results reflect a consolidated Japanese market focus with increasing international contributions from the gaming portfolio.

CyberAgentNov 2025

Financial

Consolidated Financial Results for the Fiscal Year Ended December 31, 2025 [IFRS]

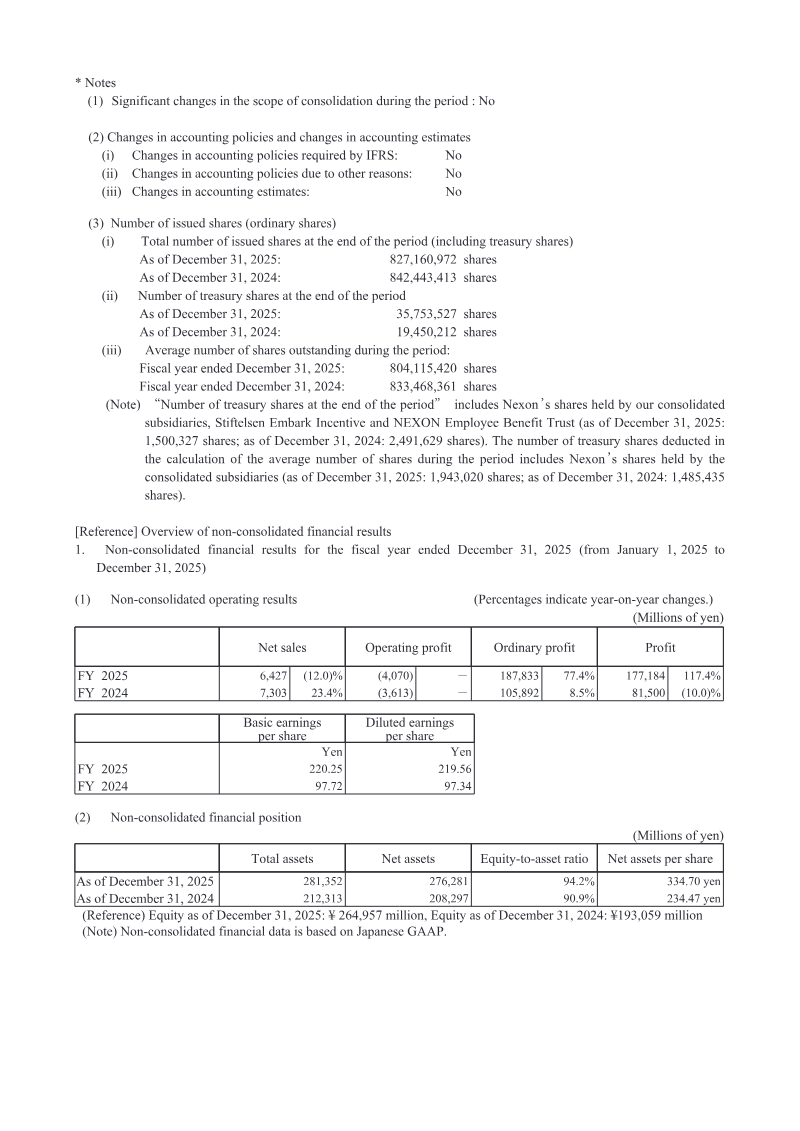

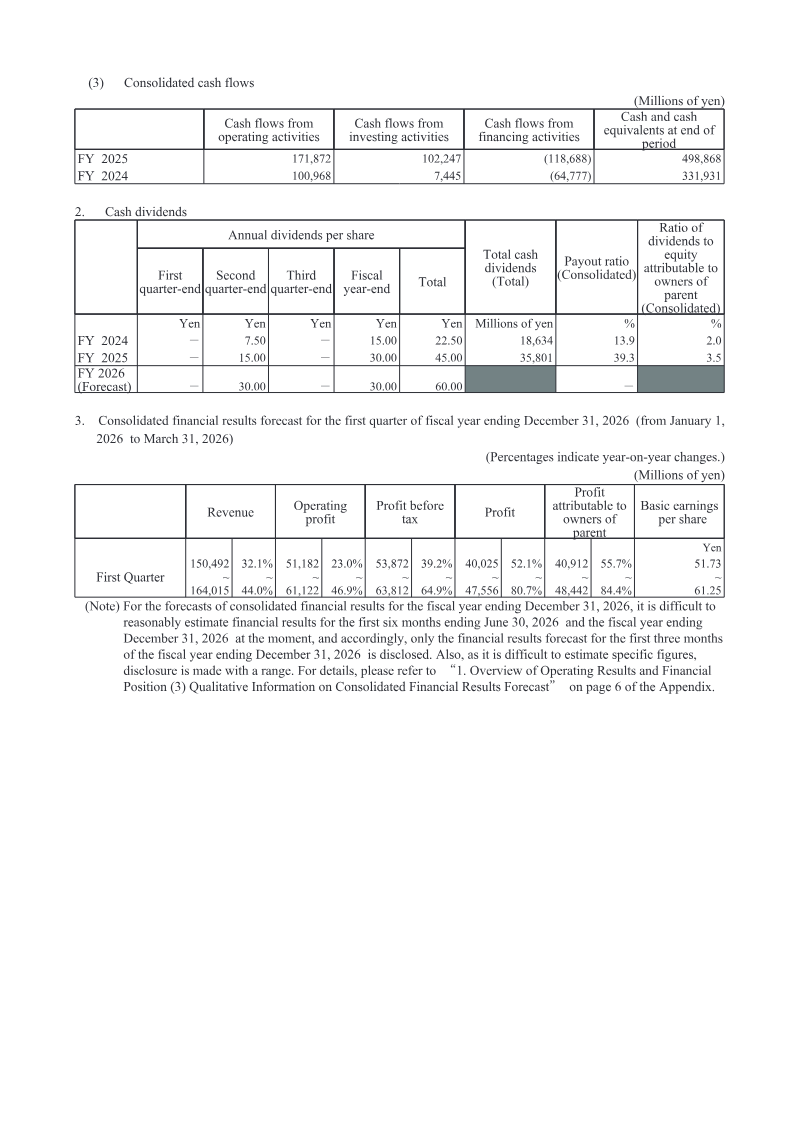

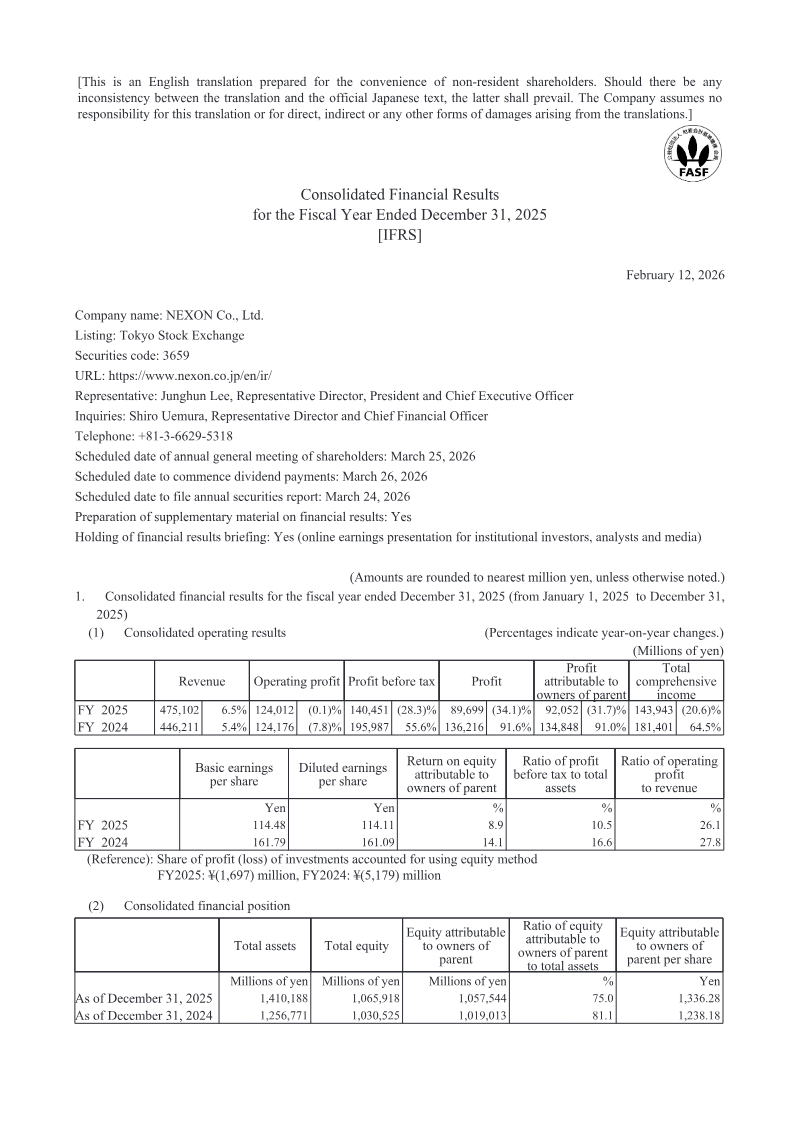

Nexon Group achieved record-breaking consolidated revenue of ¥475.1 billion for the fiscal year ended December 31, 2025, representing a 6.5% year-on-year increase. This growth was primarily driven by the Korea segment, which contributed ¥400.7 billion, and a robust performance in the PC online market. Key intellectual properties, including Dungeon&Fighter and MapleStory, alongside the successful launch of ARC Raiders, underpinned this expansion. Despite the revenue gains, profit attributable to owners fell 31.7% to ¥92.1 billion. This decline was largely influenced by foreign exchange losses, increased marketing and royalty expenses, and an ¥8.6 billion impairment loss on equity method investments. The financial position remains strong, characterized by a cash reserve of ¥498.9 billion and total assets reaching ¥1.41 trillion. Net cash from operating activities rose significantly to ¥171.9 billion, while investing activities turned positive due to ¥197.6 billion in proceeds from the sale and redemption of securities. To enhance shareholder value and capital efficiency, the annual dividend was doubled to ¥45.00 per share, and the board approved the cancellation of approximately 36.5 million treasury shares. These actions followed a substantial ¥96.9 billion allocation toward treasury share purchases during the fiscal year. Looking forward to the first quarter of 2026, revenue is projected to grow between 32.1% and 44.0% year-on-year, reaching up to ¥164.0 billion. This optimistic outlook is supported by the continued momentum of the MapleStory franchise and the integration of recent releases like Mabinogi Mobile. While the Dungeon&Fighter franchise may face a temporary revenue decline, the overall trajectory suggests a pivot toward aggressive growth. The company continues to leverage its free-to-play microtransaction model across PC and mobile platforms to maintain its dominant market position in Korea and expand its footprint in North American and European markets.

NEXON Co.Feb 2026

Presentation

Financial Results Briefing FY2025

GungHo Online Entertainment is currently undergoing a fundamental strategic pivot, transitioning from a primary focus on the domestic Japanese mobile market toward a global, multi-platform distribution model. This evolution targets North America and Europe specifically through the development of action-oriented intellectual properties for console and PC. The success of this shift is evidenced by the dramatic rise in the overseas net sales ratio, which is projected to reach 66% in fiscal year 2025, up from just 11.4% in 2016. Key drivers for this international expansion include the upcoming launch of Let It Die: Inferno and the continued global scaling of the Ragnarok and Puzzle & Dragons franchises across more than 150 countries. Despite this aggressive geographic expansion, the company faces immediate financial headwinds characterized by a contraction in consolidated net sales and operating profit. Quarterly performance data reveals a downward trajectory over a four-year period, with peak values declining from over 16,000 to approximately 7,750 in the most recent quarter. This downturn is largely attributed to softening sales of legacy mobile titles and a reactional decrease in revenue from the subsidiary Gravity. To stabilize these core assets, the company is utilizing high-profile collaborations with major brands such as Sanrio and Digimon to maintain domestic user engagement while simultaneously preparing for the launch of Ragnarok Online 3 in major Asian markets. The long-term outlook centers on a diversified portfolio that balances established mobile revenue with new, high-scale global releases. While current financial indicators reflect a period of contraction and volatility, the commitment to 100-player raid mechanics in upcoming titles and the expansion of Ragnarok X: Next Generation into EMEA markets signal a move toward more technologically ambitious projects. Ultimately, the transition toward a global-first strategy represents a necessary adaptation to the maturing domestic mobile landscape, aiming to replace declining legacy revenue with sustainable growth from international console and PC audiences.

GungHo Online EntertainmentFeb 2026

Financial

FY2025 Presentation Material

CyberAgent achieved record consolidated net sales of 874 billion yen for the 2025 fiscal year, marking nearly three decades of uninterrupted growth. This performance was characterized by a significant recovery in profitability, as operating income surged nearly 79% to 71.7 billion yen. The primary catalyst for this expansion was the gaming segment, which saw operating income nearly double due to the success of several new hit titles and a six-fold increase in overseas sales following aggressive global expansion. Furthermore, the Media and IP segment reached a major milestone by achieving profitability for the first time since the launch of the ABEMA streaming service, which saw record viewership and a doubling of active users for its original programming. While the gaming and media sectors flourished, the advertising division experienced a 14% decline in operating profit. This contraction resulted from heavy internal investments in artificial intelligence intended to drive long-term structural changes. Despite these costs, overall group sales grew by over 6%, supported by the establishment of new animation studios and expanded global distribution partnerships. The company’s strategic focus remains on diversifying its IP portfolio and leveraging external payment methods to improve margins within its digital storefronts. Looking toward the 2026 fiscal year, the outlook remains stable with projected sales of 880 billion yen, though operating income is expected to moderate to between 50 and 60 billion yen. This conservative forecast accounts for the inherent volatility of the gaming market and the high performance bar set by recent hits. Additionally, the organization is preparing for a significant leadership transition scheduled for late 2025, during which founder Susumu Fujita will transition to Chairman, and Takahiro Yamauchi will assume the role of President to lead the next phase of the company's evolution.

CyberAgentNov 2025